Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Electric Bus market demonstrates significant growth driven by expanding public transportation electrification programs and strong federal investment in zero-emission mobility. Based on a recent historical assessment, the market generated approximately USD ~ billion in revenue, supported by large procurement programs initiated by public transit agencies and school districts. Government initiatives such as the Federal Transit Administration’s Low or No Emission Vehicle Program and Environmental Protection Agency clean transportation funding have accelerated adoption of battery electric buses across municipal and regional transit fleets.

Major metropolitan areas such as Los Angeles, New York City, Seattle, San Francisco, and Chicago represent dominant adoption hubs due to advanced charging infrastructure, high public transit usage, and strong environmental policy frameworks supporting zero-emission mobility. These cities operate large transit fleets and receive substantial federal and state funding dedicated to electrified public transport systems. Transit authorities in California, Washington, and New York lead implementation initiatives due to strict air-quality regulations and long-term decarbonization mandates.

Market Segmentation

By Product Type

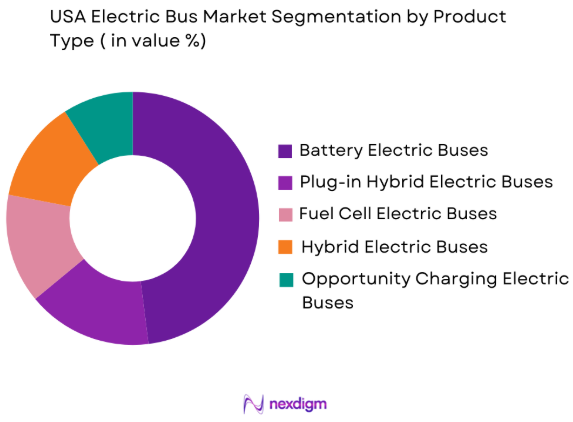

USA Electric Bus market is segmented by product type into battery electric buses, plug-in hybrid electric buses, fuel cell electric buses, hybrid electric buses, and opportunity charging electric buses. Recently, battery electric buses have a dominant market share due to factors such as widespread charging infrastructure deployment, lower operational emissions, and government funding programs that prioritize fully zero-emission vehicles. Public transit agencies increasingly prefer battery electric platforms due to simplified drivetrain architecture and improved energy efficiency. Major manufacturers have also expanded production of battery electric buses, offering longer driving ranges and advanced battery management systems. Federal funding programs further prioritize zero-emission vehicles, encouraging transit agencies to shift away from hybrid technologies.

By End User

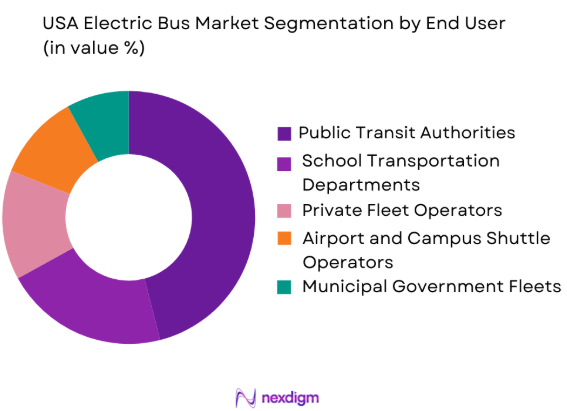

USA Electric Bus market is segmented by end users into public transit authorities, school transportation departments, private fleet operators, airport and campus shuttle operators, and municipal government fleets. Recently, public transit authorities have a dominant market share due to large fleet electrification initiatives supported by federal funding and state environmental policies. Urban transit agencies operate extensive bus fleets and prioritize replacing diesel buses with zero-emission alternatives to meet air-quality standards and climate commitments. Government grants and subsidies encourage transit authorities to accelerate electric bus procurement while expanding charging infrastructure.

Competitive Landscape

The USA Electric Bus market exhibits moderate consolidation with several established electric vehicle manufacturers competing alongside traditional bus manufacturers transitioning toward electrified platforms. Companies focus on advanced battery technologies, fleet electrification services, and integrated charging solutions to strengthen competitive positioning. Federal funding initiatives and large municipal procurement programs have intensified competition among suppliers, encouraging innovation in battery capacity, vehicle range, and operational efficiency. Strategic partnerships with transit authorities and infrastructure providers play an important role in securing long-term contracts.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Battery Technology |

| BYD Motors | 1995 | Shenzhen, China | ~ | ~ | ~ | ~ | ~ |

| Proterra | 2004 | California, USA | ~ | ~ | ~ | ~ | ~ |

| New Flyer Industries | 1930 | Manitoba, Canada | ~ | ~ | ~ | ~ | ~ |

| Blue Bird Corporation | 1927 | Georgia, USA | ~ | ~ | ~ | ~ | ~ |

| Lion Electric Company | 2008 | Quebec, Canada | ~ | ~ | ~ | ~ | ~ |

USA Electric Bus Market Analysis

Growth Drivers

Expansion of Federal and State Zero Emission Transit Programs

Government funding programs supporting zero-emission transportation have accelerated electric bus adoption across the United States. Federal initiatives provide financial incentives for transit agencies to replace diesel fleets with electric alternatives, helping reduce the high upfront cost of electric buses. Public transportation authorities increasingly prioritize electrification due to environmental regulations and national decarbonization targets. These programs also support charging infrastructure development required for reliable fleet operations. Grants often cover vehicle procurement, charging systems, and electrical upgrades. Collaboration between government bodies and transit operators further strengthens implementation of electrification programs. State-level incentives complement federal programs, encouraging wider adoption. Growing regulatory pressure continues pushing transit agencies toward zero-emission public transport solutions nationwide.

Rapid Advancements in Electric Bus Battery Technology

Ongoing advancements in battery technology have improved the performance and practicality of electric buses in public transit systems. Modern lithium-ion batteries provide higher energy density, enabling longer operating ranges for buses serving urban routes. Enhanced battery management systems increase charging efficiency while improving operational safety and reducing downtime. Manufacturers are investing in research and development to extend battery lifespan and limit degradation over time. Improved battery chemistry supports reliable operations under diverse climatic conditions. High-capacity battery packs allow buses to complete extended routes with fewer charging interruptions. Fast-charging technology and advanced energy monitoring systems further optimize fleet efficiency and strengthen electric bus viability.

Market Challenges

High Initial Procurement Costs of Electric Bus Fleets

Electric buses require higher initial investment than conventional diesel buses, creating financial challenges for many transit agencies. The cost gap largely stems from expensive battery systems and advanced electric drivetrain technologies. Public transportation authorities often operate under tight budget constraints, making large-scale fleet electrification difficult. Although government incentives help offset some expenses, funding gaps remain for many agencies. Charging infrastructure installation also adds significant capital costs. Upgrading electrical grids, modifying bus depots, and installing charging systems require additional investment. Lengthy municipal budget approval processes can delay procurement decisions. Smaller transit agencies with limited financial capacity face even greater adoption barriers.

Charging Infrastructure Deployment and Grid Integration Complexity

Electric bus adoption requires extensive charging infrastructure, creating logistical and technical challenges for transit agencies. Charging stations must be strategically installed in bus depots or along transit routes to maintain reliable operations. Transit authorities must coordinate closely with electricity providers to ensure sufficient power supply for charging systems. High-capacity chargers often require upgrades to local electrical infrastructure. Grid capacity constraints may limit the ability to charge multiple buses simultaneously during peak hours. Infrastructure planning must also consider route scheduling and fleet management. Depot layouts often require redesign to integrate charging equipment and electrical systems. Construction approvals and permitting procedures can delay deployment timelines. Utilities must maintain consistent electricity supply to avoid operational disruptions, making infrastructure development a key implementation challenge.

Opportunities

Large Scale Electrification of School Bus Fleets

School bus electrification programs present a significant growth opportunity within the USA Electric Bus market. Government funding initiatives encourage school districts to replace diesel buses with electric alternatives. Electric school buses help reduce emissions in school zones and residential communities. Funding programs prioritize these vehicles because of their environmental and health advantages. School transportation routes are typically predictable, making them suitable for electric vehicle deployment. Charging infrastructure can be installed at centralized depots where buses remain parked overnight. Electric school buses also support vehicle to grid integration, allowing stored energy to be supplied back to electricity networks when not in use.

Integration of Smart Fleet Management and Charging Optimization Systems

Integration of digital fleet management technologies creates strong opportunities for electric bus operators. Advanced telematics systems enable real time monitoring of battery health, energy consumption, and vehicle performance. Fleet operators can optimize route planning based on battery capacity and charging availability. Smart charging platforms help transit agencies control electricity demand and reduce operating costs. Predictive maintenance systems allow early detection of technical issues before service disruptions occur. Data analytics tools improve fleet scheduling and operational efficiency. Charging infrastructure can also integrate with renewable energy systems to lower emissions. Collaboration between technology providers and transit agencies continues expanding intelligent fleet management adoption.

Future Outlook

The USA Electric Bus market is expected to witness sustained expansion driven by government policy support, environmental regulations, and increasing investment in clean transportation infrastructure. Transit agencies are accelerating fleet electrification strategies while manufacturers continue improving battery efficiency and vehicle range. Technological advancements in fast-charging systems and smart fleet management solutions will further strengthen operational efficiency. Rising environmental awareness and urban air-quality concerns are expected to continue driving demand for zero-emission buses across metropolitan transit systems.

Major Players

- BYD Motors

- Proterra

- New Flyer Industries

- Gillig LLC

- Blue Bird Corporation

- Lion Electric Company

- GreenPowerMotor Company

- Volvo Bus Corporation

- Daimler Buses

- Hyundai Motor Company

- ENC (ElDoradoNational California)

- Phoenix Motorcars

- IC Bus

- Thomas Built Buses

- Motiv Power Systems

Key Target Audience

- Public transportation authorities

- Electric vehicle manufacturers

- Electric charging infrastructure providers

- Fleet management solution providers

- Automotivecomponentsuppliers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Renewable energy companies

Research Methodology

Step 1: Identification of Key Variables

The research process begins by identifying key market variables influencing the USA Electric Bus market including fleet electrification programs, government incentives, battery technologies, and charging infrastructure development. Market demand drivers, regulatory frameworks, and technological innovation trends are evaluated to establish the core parameters used in the research model.

Step 2: Market Analysis and Construction

Comprehensive market analysis is conducted using data collected from transportation authorities, regulatory agencies, industry associations, and company reports. Market size construction incorporates procurement data, electric bus deployment statistics, and infrastructure investment trends to ensure accurate estimation of industry development.

Step 3: Hypothesis Validation and Expert Consultation

Market assumptions are validated through consultation with industry experts including electric vehicle manufacturers, transit agencies, and energy infrastructure providers. Expert insights help refine market drivers, competitive dynamics, and emerging technological trends shaping the electric bus ecosystem.

Step 4: Research Synthesis and Final Output

All validated data points are synthesized into a structured analytical framework combining quantitative market evaluation with qualitative industry insights. The final output provides a comprehensive assessment of market dynamics, competitive landscape, and long-term growth opportunities within the USA Electric Bus market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Federal and State Incentives Supporting Zero Emission Public Transport

Rising Urban Air Quality Regulations and Emission Reduction Targets

Expansion of Charging Infrastructure for Electric Public Transport Fleets - Market Challenges

High Initial Procurement Costs for Electric Bus Fleets

Charging Infrastructure Deployment and Grid Integration Complexity

Battery Replacement and Lifecycle Cost Management - Market Opportunities

Large Scale Electrification of School Bus Fleets Across States

Integration of Smart Fleet Management and Telematics Systems

Expansion of Hydrogen Fuel Cell Electric Bus Pilot Programs - Trends

Adoption of Long Range High Capacity Battery Electric Buses

Deployment of Opportunity Charging and Fast Charging Networks

Partnerships Between Transit Agencies and Clean Energy Providers - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Battery Electric Buses

Plug-in Hybrid Electric Buses

Fuel Cell Electric Buses

Hybrid Electric Buses

Opportunity Charging Electric Buses - By Platform Type (In Value%)

Transit Buses

School Buses

Intercity Coaches

Shuttle Buses

Airport Electric Buses - By Fitment Type (In Value%)

OEM Factory Built Electric Buses

Retrofitted Diesel to Electric Buses

Modular Electric Bus Platforms

Integrated Smart Electric Buses

Lightweight Composite Electric Buses - By End User Segment (In Value%)

Public Transit Authorities

School District Transportation Departments

Private Fleet Operators

Airport and Campus Shuttle Operators

Municipal and Government Fleets - By Procurement Channel (In Value%)

Government Fleet Procurement Programs

Direct OEM Contracts

Public Transport Authority Tenders

Leasing and Fleet Financing Programs

Public Private Partnership Procurement

- Market Share Analysis

- Cross Comparison Parameters (Battery Technology Type, Battery Capacity Range, Charging Infrastructure Compatibility, Charging Time Duration, Vehicle Range Per Charge, Energy Consumption Efficiency, Passenger Carrying Capacity, Procurement Contract Type)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Proterra Inc.

BYD Motors Inc.

New Flyer Industries

Gillig LLC

Blue Bird Corporation

Lion Electric Company

GreenPower Motor Company

Daimler Buses North America

Volvo Bus Corporation

Motiv Power Systems

ENC (ElDorado National California)

Phoenix Motorcars

IC Bus (Navistar)

Thomas Built Buses

Hyundai Motor Company

- Transit agencies accelerating fleet electrification programs

- School districts replacing diesel buses with zero emission alternatives

- Private fleet operators adopting electric buses for corporate mobility

- Municipal authorities investing in sustainable urban transport systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now