Download PDF

Download PDF Download PDF

Download PDFMarket overview

The USA electric motors market is valued at approximately USD ~ billion based on a recent historical assessment, driven by strong demand across industrial automation, HVAC systems, electric vehicles, and renewable energy installations. Growth is supported by federal infrastructure spending, energy efficiency mandates under the U.S. Department of Energy, and rising electrification across manufacturing and transportation. Replacement of legacy motors with high-efficiency IE3 and IE4 systems further strengthens revenue expansion across commercial and heavy industrial segments.

Dominance is concentrated in states such as Texas, Michigan, Ohio, and California due to their large manufacturing bases, automotive production clusters, and renewable energy investments. The Midwest leads because of automotive and industrial equipment manufacturing density, while California benefits from clean energy policies and electric vehicle production. Texas supports demand through oil and gas operations and large-scale infrastructure projects, creating sustained procurement of high-capacity and specialized electric motor systems.

Market Segmentation

By Product Type

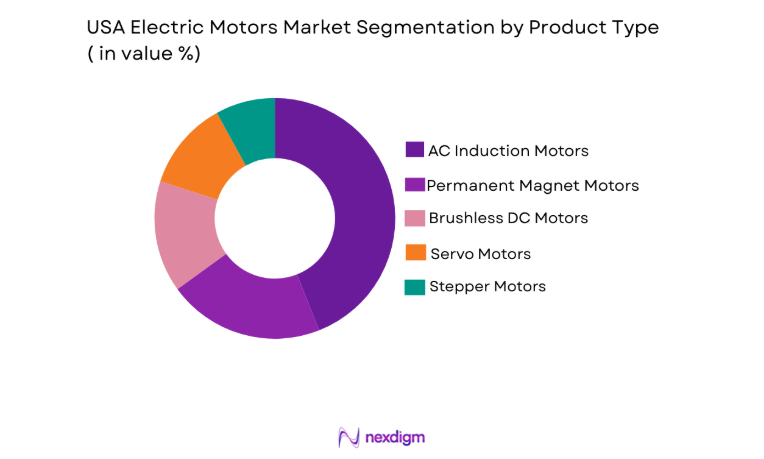

USA Electric Motors Market is segmented by product type into AC induction motors, permanent magnet synchronous motors, brushless DC motors, servo motors, and stepper motors. Recently, AC induction motors has a dominant market share due to extensive adoption across industrial automation, HVAC systems, pumps, compressors, and heavy machinery applications. Their rugged construction, cost efficiency, compatibility with variable frequency drives, and suitability for continuous duty industrial operations drive sustained procurement across manufacturing and infrastructure sectors.

By Platform Type

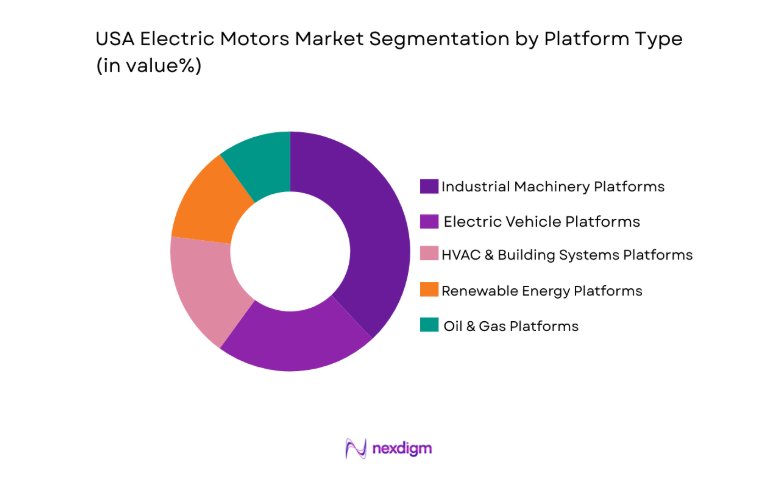

USA Electric Motors market is segmented by platform type into industrial machinery platforms, electric vehicle platforms, HVAC and building systems platforms, renewable energy platforms, and oil and gas platforms. Recently, industrial machinery platforms has a dominant market share due to extensive deployment in automated production lines, robotics, conveyor systems, and heavy processing equipment. High operational reliability requirements, continuous duty cycles, and integration with variable frequency drives support large-scale motor installations across manufacturing ecosystems. Ongoing modernization of factories and expansion of domestic production facilities further reinforce platform-level demand concentration.

Competitive Landscape

The USA electric motors market is moderately consolidated with strong presence of multinational manufacturers and domestic industrial motor specialists. Leading companies leverage advanced efficiency technologies, wide distribution networks, and integrated automation portfolios to sustain competitive advantage. Strategic acquisitions and product portfolio diversification remain common competitive strategies.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Efficiency Class Focus |

| ABB Ltd | 1988 | Zurich, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Siemens AG | 1847 | Munich, Germany | ~ | ~ | ~ | ~ | ~ |

| Nidec Corporation | 1973 | Kyoto, Japan | ~ | ~ | ~ | ~ | ~ |

| Regal Rexnord | 1955 | Wisconsin, USA | ~ | ~ | ~ | ~ | ~ |

| WEG Industries | 1961 | Jaraguá do Sul, Brazil | ~ | ~ | ~ | ~ | ~ |

USA Electric Motors Market Analysis

Growth Drivers

Industrial Automation and Smart Manufacturing Expansion

The rapid transformation of manufacturing facilities across the United States toward Industry frameworks is significantly increasing demand for advanced electric motors integrated with automation systems. Manufacturers are investing heavily in robotics, programmable logic controllers, and digitally enabled production lines, all of which rely on high-performance electric motors to deliver precision and efficiency. The integration of variable frequency drives and servo motors allows optimized speed control and energy savings in automated environments. Federal incentives supporting domestic manufacturing and supply chain reshoring further accelerate equipment upgrades in heavy industries. Automotive, aerospace, and electronics producers are modernizing assembly lines to remain globally competitive, resulting in sustained procurement of AC and servo motors. Smart factories require reliable, durable motors capable of operating continuously under variable load conditions. Increasing adoption of predictive maintenance technologies also encourages installation of digitally compatible motors equipped with sensor interfaces. Energy efficiency regulations established by the Department of Energy mandate replacement of legacy motors with high-efficiency units, further driving capital expenditure across industries. As productivity enhancement and operational cost reduction remain strategic priorities for manufacturers, electric motor installations continue to expand across industrial automation ecosystems.

Electrification of Transportation and Infrastructure Modernization

The accelerating transition toward electric mobility and infrastructure electrification is strengthening the growth trajectory of the electric motors market in the United States. Electric vehicle production requires multiple motor systems including traction motors, cooling systems, and auxiliary drives, generating substantial OEM demand. Public transit electrification initiatives and federal funding under infrastructure development programs contribute to sustained motor procurement across rail and urban mobility sectors. Investments in charging infrastructure, grid upgrades, and renewable integration also require high-capacity industrial motors for pumps, compressors, and power management systems. State-level clean energy policies encourage industrial facilities to transition from fossil-fuel-driven systems to electrically powered alternatives. Data centers supporting digital transformation depend on advanced cooling systems powered by high-efficiency motors. The construction sector increasingly integrates electrically powered machinery to meet sustainability standards. Expansion of offshore wind and solar installations requires precision motor systems for turbine pitch control and tracking mechanisms. Collectively, transportation electrification and infrastructure modernization initiatives create diversified demand channels that reinforce steady market expansion for electric motor manufacturers across residential, commercial, and industrial domains.

Market Challenges

Volatility in Raw Material Prices and Supply Chain Constraints

Electric motor manufacturing relies heavily on copper, electrical steel, rare earth magnets, and aluminum, making the industry vulnerable to global commodity price fluctuations. Disruptions in international trade routes and geopolitical tensions can delay procurement of essential components, increasing production costs. Domestic manufacturers face margin pressure when raw material prices surge unexpectedly. Dependence on imported rare earth elements, particularly for permanent magnet motors, introduces strategic vulnerabilities. Logistics bottlenecks and port congestion may extend lead times for industrial clients requiring large-capacity motors. Smaller manufacturers struggle to absorb price shocks compared to multinational competitors with diversified supply chains. Fluctuating currency rates also impact imported component costs for U.S. based production facilities. Customers may delay capital expenditure decisions during periods of economic uncertainty, affecting order volumes. These combined supply and pricing pressures create operational complexity and necessitate strategic inventory management to maintain production continuity.

High Capital Cost and Regulatory Compliance Requirements

Advanced high-efficiency motors and digitally integrated systems often require higher upfront investment compared to traditional motor technologies. Small and medium enterprises may hesitate to adopt premium efficiency motors despite long-term energy savings. Compliance with Department of Energy efficiency standards and state environmental regulations requires continuous product redesign and certification processes. Testing and validation procedures increase research and development expenditure for manufacturers. Retrofit projects in older facilities can involve complex installation challenges and additional infrastructure modification costs. Market participants must maintain strict adherence to safety and performance standards, increasing administrative overhead. Competition from low-cost imports intensifies pricing pressure in certain product categories. Customers frequently prioritize short-term budget constraints over lifecycle cost advantages, slowing adoption rates. These financial and regulatory constraints collectively moderate the pace of widespread market penetration for high-performance electric motor technologies.

Opportunities

Expansion of High-Efficiency IE4 and IE5 Motor Adoption

Increasing emphasis on sustainability and energy conservation presents significant opportunities for manufacturers specializing in ultra-high-efficiency motor systems. Government initiatives encouraging carbon reduction and industrial decarbonization are driving procurement of IE4 and IE5 motors. Utility incentive programs offer rebates for facilities upgrading to premium efficiency equipment. Corporations pursuing environmental, social, and governance commitments are prioritizing energy efficient machinery investments. Technological advancements in magnetic materials and cooling designs enhance motor performance while reducing energy consumption. Data-driven monitoring platforms enable real-time optimization, strengthening value propositions for advanced motor systems. Retrofitting aging infrastructure across manufacturing plants creates recurring demand cycles. Integration of smart sensors allows predictive diagnostics and improved operational reliability. These dynamics collectively position high-efficiency motor manufacturers to capture sustained long-term growth across industrial and commercial sectors.

Growth in Renewable Energy and Distributed Generation Systems

Rapid deployment of wind, solar, and battery storage installations across the United States generates increasing demand for specialized electric motors. Wind turbines require precision pitch control motors and yaw systems to maximize output efficiency. Solar tracking systems depend on compact, durable motors capable of operating in variable weather conditions. Battery storage facilities utilize advanced cooling systems powered by high-efficiency motors to maintain operational safety. Microgrid installations supporting rural and industrial facilities rely on motorized power management equipment. Federal and state level renewable portfolio standards encourage ongoing infrastructure investment. Electrification of agricultural irrigation systems also increases demand for reliable pump motors. Offshore wind projects along coastal states present high-capacity industrial motor opportunities. Continued renewable expansion combined with grid modernization initiatives establishes strong long-term growth potential within distributed energy ecosystems.

Future Outlook

The USA electric motors market is expected to maintain steady expansion over the next five years driven by automation upgrades, electrification of transportation, and renewable energy deployment. Technological improvements in efficiency classes and smart monitoring capabilities will support premium product adoption. Regulatory frameworks emphasizing energy conservation will encourage replacement demand. Infrastructure modernization and domestic manufacturing initiatives will further strengthen industrial procurement trends.

Major Players

- ABB Ltd

- Siemens AG

- Nidec Corporation

- Regal Rexnord

- WEG Industries

- Toshiba Corporation

- Rockwell Automation

- Franklin Electric

- Baldor Electric Company

- Marathon Electric

- TECO Westinghouse

- Johnson Electric

- Allied Motion Technologies

- Emerson Electric Co.

- General Electric Company

Key Target Audiences

- Investments and venture capitalist firms

- Government and regulatory bodies

- Industrial manufacturing companies

- Automotive OEMs

- Renewable energy developers

- Oil and gas operators

- HVAC equipment manufacturers

- Infrastructure development agencies

Research Methodology

Step 1: Identification of Key Variables

Key performance indicators including revenue generation, production capacity, efficiency standards, and end-use demand trends were identified. Macroeconomic indicators and regulatory benchmarks were mapped to establish baseline evaluation criteria.

Step 2: Market Analysis and Construction

Secondary data from government databases, corporate filings, and energy regulatory authorities were analyzed to construct market size estimates. Cross-validation was conducted using industry trade statistics and production output data.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including engineers, procurement managers, and regulatory specialists were consulted to validate assumptions. Feedback was integrated to refine market segmentation and growth projections.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were consolidated into structured analytical frameworks. Final interpretations were reviewed for consistency, ensuring alignment with regulatory and industrial benchmarks.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Industrial Automation Expansion Across Manufacturing Facilities

Electrification of Transportation and Mobility Systems

Energy Efficiency Regulations and Compliance Standards - Market Challenges

Volatility in Raw Material Pricing

High Initial Capital Investment Requirements

Supply Chain Disruptions and Component Dependencies - Market Opportunities

Growth in Renewable Energy Installations

Adoption of Smart Motor Monitoring Technologies

Expansion of Domestic Manufacturing Initiatives - Trends

Integration of Variable Frequency Drives

Rising Demand for IE4 and IE5 Efficiency Classes

Increased Deployment in Data Centers

Shift Toward Compact High Torque Designs

Digital Twin Integration in Motor Systems - Government Regulations & Defense Policy

Department of Energy Efficiency Standards

Federal Infrastructure Investment Programs

State Level Clean Energy Mandates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

AC Induction Motors

Permanent Magnet Synchronous Motors

Brushless DC Motors

Stepper Motors

Servo Motors - By Platform Type (In Value%)

Industrial Automation Platforms

Electric Vehicle Platforms

HVAC and Building Systems Platforms

Oil and Gas Platforms

Renewable Energy Platforms - By Fitment Type (In Value%)

OEM Installations

Aftermarket Replacements

Retrofit Installations

Integrated Drive Systems

Standalone Motor Units - By EndUser Segment (In Value%)

Industrial Manufacturing

Automotive and Transportation

Oil and Gas Industry

Commercial Buildings

Renewable Energy Developer - By Procurement Channel (In Value%)

Direct Manufacturer Sales

Authorized Distributors

Online Industrial Marketplaces

EPC Contractors

System Integrators - By Material / Technology (in Value %)

Copper Wound Motors

Aluminum Wound Motors

Rare Earth Magnet Motors

High Efficiency IE3 Motors

Ultra High Efficiency IE4 Motors

- Market structure and competitive positioning

Market share snapshot of major players - Cross comparison Parameters (Efficiency Class Focus, Voltage Range, Torque Capacity, Industry Vertical Focus, Distribution Network Strength, R&D Intensity, Digital Integration Capability, Manufacturing Footprint, Aftermarket Service Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ABB

Siemens

Nidec Corporation

Regal Rexnord

WEG

Toshiba Industrial Products

Rockwell Automation

Franklin Electric

Baldor Electric

Marathon Electric

TECO Westinghouse

Johnson Electric

Allied Motion Technologies

Emerson Electric

General Electric

- Growing Automation Investment by Industrial Manufacturers

- Rising Electrification in Automotive OEM Production

- Infrastructure Expansion Driving Commercial Demand

- Renewable Energy Developers Increasing Motor Procurement

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now