Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA Emergency Braking Systems market generated approximately USD ~ billion in revenue, supported by National Highway Traffic Safety Administration data and financial disclosures from leading ADAS suppliers. Market expansion is driven by mandatory crash avoidance regulations, increasing integration of advanced driver assistance systems in new vehicles, and strong demand from electric vehicle manufacturers. Rising urban traffic density and federal safety rating programs continue to accelerate OEM adoption across passenger and commercial vehicle segments nationwide.

Major automotive production hubs including Michigan, Ohio, California, and Texas play a critical role in system integration and large scale manufacturing due to concentrated OEM facilities and supplier networks. Detroit remains strategically significant because of its established ecosystem and advanced vehicle testing infrastructure. California leads technological innovation through autonomous mobility research and semiconductor development clusters. Southern manufacturing corridors further strengthen supply chain efficiency, enabling faster deployment of emergency braking technologies across multiple vehicle platforms.

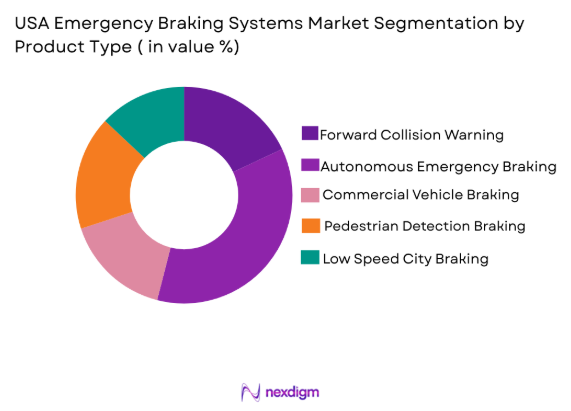

By Product Type

USA Emergency Braking Systems market is segmented by product type into Forward Collision Warning with Automatic Braking, Autonomous Emergency Braking for Passenger Vehicles, Commercial Vehicle Emergency Braking Systems, Pedestrian Detection Integrated Braking Systems, and Low Speed City Emergency Braking Systems. Recently, Autonomous Emergency Braking for Passenger Vehicles has a dominant market share due to widespread OEM standardization, strong consumer preference for advanced safety features, insurance incentives linked to crash reduction, and regulatory testing protocols encouraging default inclusion in new vehicles.

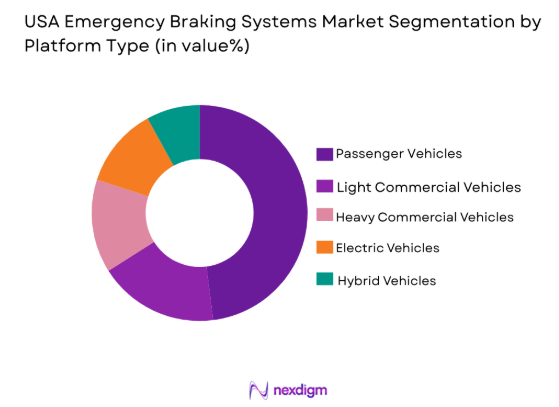

By Platform Type

USA Emergency Braking Systems market is segmented by platform type into Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, and Hybrid Vehicles. Recently, Passenger Cars has a dominant market share due to higher production volumes, regulatory focus on passenger vehicle safety compliance, increasing consumer safety awareness, and broader integration of ADAS suites in mid range and premium vehicle models compared to commercial fleets.

Competitive Landscape

The USA Emergency Braking Systems market demonstrates moderate consolidation, with a limited number of automotive suppliers controlling advanced sensor integration and braking control software platforms. Strategic partnerships between semiconductor providers, ADAS developers, and vehicle manufacturers significantly influence innovation cycles and procurement contracts. Technology leadership, regulatory compliance expertise, and strong OEM relationships define competitive positioning across this market.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Sensor Integration Capability |

| Robert Bosch LLC | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ |

USA Emergency Braking Systems Market Analysis

Growth Drivers

Federal Safety Mandates and Crash Avoidance Regulations

The increasing enforcement of crash avoidance standards by the National Highway Traffic Safety Administration is significantly accelerating the deployment of emergency braking systems across passenger and commercial vehicles in the United States. Regulatory frameworks encouraging automatic emergency braking integration in new vehicle models are compelling manufacturers to standardize these systems across trim levels rather than limiting them to premium variants. Insurance industry pressure and safety rating programs further reinforce compliance incentives by rewarding manufacturers that meet advanced safety benchmarks. As safety compliance becomes a prerequisite for competitive positioning, OEMs are allocating higher budgets toward advanced braking technologies. Fleet operators are also responding to regulatory oversight by upgrading vehicles to reduce liability exposure and accident rates. The convergence of safety mandates with consumer expectations is narrowing optional feature gaps and making emergency braking systems a baseline requirement. Regulatory harmonization across states is reducing uncertainty for suppliers and facilitating long term production planning. Collectively, these policy driven factors are creating sustained structural demand for technologically advanced emergency braking systems.

Rising Integration of ADAS in Electric and Connected Vehicles

The rapid expansion of electric vehicle production in the United States is strengthening demand for advanced driver assistance technologies, including autonomous emergency braking. Electric vehicle manufacturers typically integrate high end safety suites to differentiate offerings in a competitive mobility landscape. Connected vehicle architectures enable real time data processing and sensor fusion, improving braking response accuracy and predictive collision avoidance capabilities. Consumer preference for technologically sophisticated vehicles encourages OEMs to bundle emergency braking within broader ADAS packages. Semiconductor advancements and software defined vehicle platforms are making integration more scalable across vehicle segments. Investment in artificial intelligence based perception systems enhances reliability under complex traffic conditions. Supply chain localization for EV components further supports stable deployment of braking technologies. These combined factors position emergency braking systems as a foundational element of next generation vehicle platforms in the United States.

Market Challenges

High System Integration and Calibration Costs

The integration of radar, camera, and control unit technologies into vehicle architectures requires complex calibration processes that increase production expenses. Advanced braking systems must be precisely aligned with steering, suspension, and electronic control units to ensure functional accuracy. Manufacturing lines often require specialized testing infrastructure, raising capital expenditure for OEMs and suppliers. Smaller manufacturers may face financial constraints when scaling advanced safety systems across multiple models. Post collision recalibration and maintenance procedures can increase lifecycle service costs for consumers and fleet operators. Variability in vehicle platform design adds engineering complexity, limiting standardized module deployment. Supply chain disruptions in semiconductor availability can further elevate component pricing. These cost pressures may slow adoption among lower priced vehicle segments.

Performance Limitations Under Adverse Environmental Conditions

Emergency braking systems rely heavily on sensor accuracy, which can be compromised by heavy rain, snow, fog, or glare conditions. Radar and camera sensors may experience reduced detection reliability in complex urban environments. False positives or delayed activation can affect consumer trust in automated braking interventions. Continuous software refinement is required to improve predictive modeling and object recognition capabilities. Testing and validation under diverse environmental scenarios increase research and development expenditure. Commercial fleets operating across varied climates require enhanced robustness standards. Regulatory scrutiny over system performance failures may increase compliance burdens. These operational challenges necessitate ongoing innovation to maintain reliability and public confidence.

Opportunities

Expansion into Commercial Fleet Safety Modernization Programs

Growing emphasis on reducing road fatalities and insurance liabilities is encouraging logistics providers and public transportation agencies to modernize fleets with advanced emergency braking systems. Commercial vehicle operators face regulatory oversight that incentivizes the integration of crash avoidance technologies. Fleet wide deployment can deliver measurable reductions in accident related downtime and repair costs. Insurance providers increasingly offer premium adjustments for vehicles equipped with certified safety technologies. Retrofitting programs create additional revenue streams beyond OEM installations. Data analytics from fleet telematics platforms can enhance braking system optimization and predictive maintenance strategies. Partnerships between technology providers and fleet managers support scalable implementation frameworks. This opportunity strengthens long term demand in both private and public sector transportation networks.

Integration with Autonomous and Semi Autonomous Driving Ecosystems

The progression toward higher levels of vehicle autonomy increases reliance on automated braking systems as critical safety redundancies. Emergency braking modules serve as foundational control mechanisms within autonomous driving stacks. Software defined vehicle architectures enable continuous improvement through over the air updates, enhancing braking algorithms over time. Collaboration between semiconductor firms and automotive manufacturers accelerates sensor fusion advancements. Regulatory pilots for autonomous mobility services further expand real world testing environments. Urban smart mobility initiatives support data driven traffic management systems that complement vehicle based braking technologies. Consumer trust in autonomous mobility is strengthened when reliable emergency braking functionality is demonstrated. These dynamics create strategic growth pathways for system providers within the evolving mobility ecosystem.

Future Outlook

The USA Emergency Braking Systems market is expected to experience sustained growth over the next five years driven by regulatory reinforcement, EV adoption, and continuous advancements in sensor fusion technologies. Increasing integration within software defined vehicle platforms will enhance scalability and cost efficiency. Federal safety evaluations and state level incentives are likely to accelerate standardization across mid range vehicles. Demand from fleet modernization programs and autonomous mobility pilots will further strengthen market expansion across passenger and commercial platforms.

Major Players

- Robert Bosch LLC

- Continental AG

- ZF Friedrichshafen AG

- Denso Corporation

- Aptiv PLC

- Magna International Inc

- Valeo SA

- Hyundai Mobis

- Autoliv Inc

- Mobileye Global Inc

- Hitachi Astemo

- NXP Semiconductors

- Texas Instruments Automotive

- Veoneer Inc

- Knorr Bremse AG

Key Target Audience

- Automotive OEM manufacturers

- Automotive suppliers

- Electric vehicle manufacturers

- Fleet operators

- Logistics and transportation companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive component distributors

Research Methodology

Step 1: Identification of Key Variables

Key performance indicators including installation rates, regulatory mandates, OEM production volumes, and technology penetration were identified to frame the research boundaries. Secondary sources such as federal transportation databases and corporate disclosures were analyzed to establish baseline data integrity.

Step 2: Market Analysis and Construction

Market modeling incorporated vehicle production data, ADAS penetration metrics, and supplier revenue disclosures to construct a comprehensive industry framework. Segmentation analysis was conducted based on product and platform classifications relevant to emergency braking technologies.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, automotive engineers, and regulatory analysts were consulted to validate assumptions regarding adoption rates and compliance drivers. Cross verification of technology trends ensured realistic forecasting alignment.

Step 4: Research Synthesis and Final Output

Quantitative and qualitative insights were consolidated into structured analytical outputs. Findings were reviewed for internal consistency and regulatory relevance before finalization of the comprehensive market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing federal safety mandates for collision avoidance technologies

Rising consumer preference for advanced driver assistance systems

Expansion of electric and hybrid vehicle production

Technological advancements in sensor fusion and artificial intelligence

Growing urban traffic density increasing accident prevention demand - Market Challenges

High system integration and calibration costs

Performance limitations in adverse weather conditions

Cybersecurity risks in connected vehicle architectures

Complex interoperability across vehicle platforms

Liability concerns related to autonomous intervention systems - Market Opportunities

Integration with semi-autonomous and autonomous driving platforms

Expansion in commercial fleet safety upgrades

Collaboration with smart city infrastructure initiatives

- Trends

Increased bundling of emergency braking within ADAS packages

Shift toward AI driven predictive braking algorithms

Adoption of over the air software updates for braking systems

Growth of multi sensor fusion architectures

Rising demand for pedestrian and cyclist detection capabilities

- Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standards related to crash avoidance

National Highway Traffic Safety Administration performance assessments

State level mandates encouraging ADAS adoption in fleet vehicles

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Forward Collision Warning with Automatic Braking

Autonomous Emergency Braking for Passenger Vehicles

Commercial Vehicle Emergency Braking Systems

Pedestrian Detection Integrated Braking Systems

Low Speed City Emergency Braking Systems - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Hybrid Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Retrofit Systems

Integrated ADAS Suites

Standalone Braking Modules

Software Upgrade Enabled Systems - By End User Segment (In Value%)

Individual Vehicle Owners

Fleet Operators

Logistics and Transportation Companies

Ride Sharing Service Providers

Government and Municipal Transport Agencies - By Procurement Channel (In Value%)

Direct OEM Contracts

Supplier Agreements

Government Safety Mandated Procurement

Aftermarket Distribution Networks

Online Automotive Retail Platforms - By Material / Technology (in Value %)

Radar Based Braking Systems

Camera Based Vision Systems

LiDAR Integrated Braking Systems

Ultrasonic Sensor Assisted Systems

Sensor Fusion and AI Based Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Technology Integration Level, Sensor Configuration, OEM Partnerships, Aftermarket Presence, Pricing Strategy)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Robert Bosch LLC

Continental Automotive Systems

ZF Friedrichshafen AG

Aptiv PLC

Denso Corporation

Magna International Inc

Autoliv Inc

Mobileye Global Inc

Valeo SA

Hyundai Mobis

Hitachi Astemo

NXP Semiconductors

Texas Instruments Automotive

Veoneer Inc

Knorr Bremse AG

- Fleet operators prioritizing accident reduction and insurance cost savings

- Passenger vehicle buyers demanding enhanced safety ratings

- Logistics companies integrating safety technologies to comply with regulations

- Municipal agencies adopting advanced braking systems in public transport fleets

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now