Download PDF

Download PDFMarket Overview

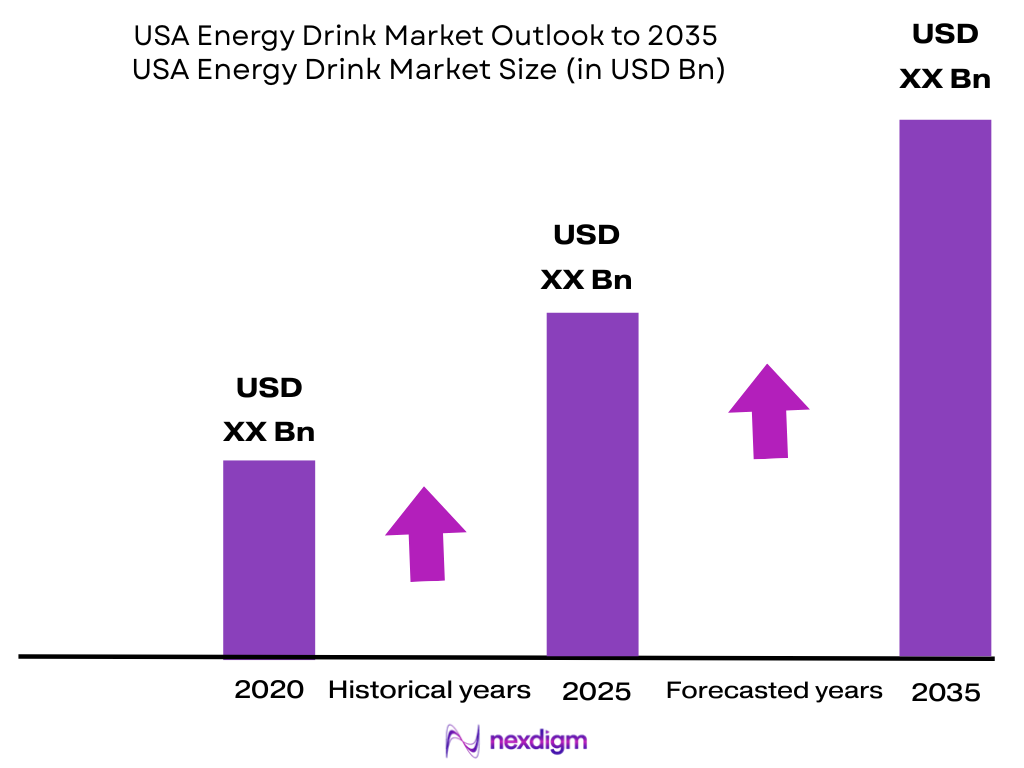

The USA energy drink market is valued at USD ~ billion, based on latest audited industry revenue, compared with USD ~ billion generated by the global energy drinks market in the immediately preceding historical base. Demand is driven by male consumers aged 18–34, athletes, busy professionals, and consumers seeking cognitive and physical performance, while low-sugar, sugar-free, natural-caffeine and functional formulations are reshaping product preference.

The USA market is concentrated around high-density urban and Sun Belt consumption corridors, led by New York, Los Angeles, Chicago, Houston, Phoenix, Dallas, San Diego and San Antonio due to large young-adult populations, commuting intensity, convenience-store traffic, gym culture and mass retail density. New York has 8,478,072 residents, Los Angeles 3,878,704, Chicago 2,721,308, Houston 2,390,125, Phoenix 1,673,164, and Dallas 1,326,087, strengthening beverage velocity and cold-vault turnover.

Market Segmentation

By Product Type

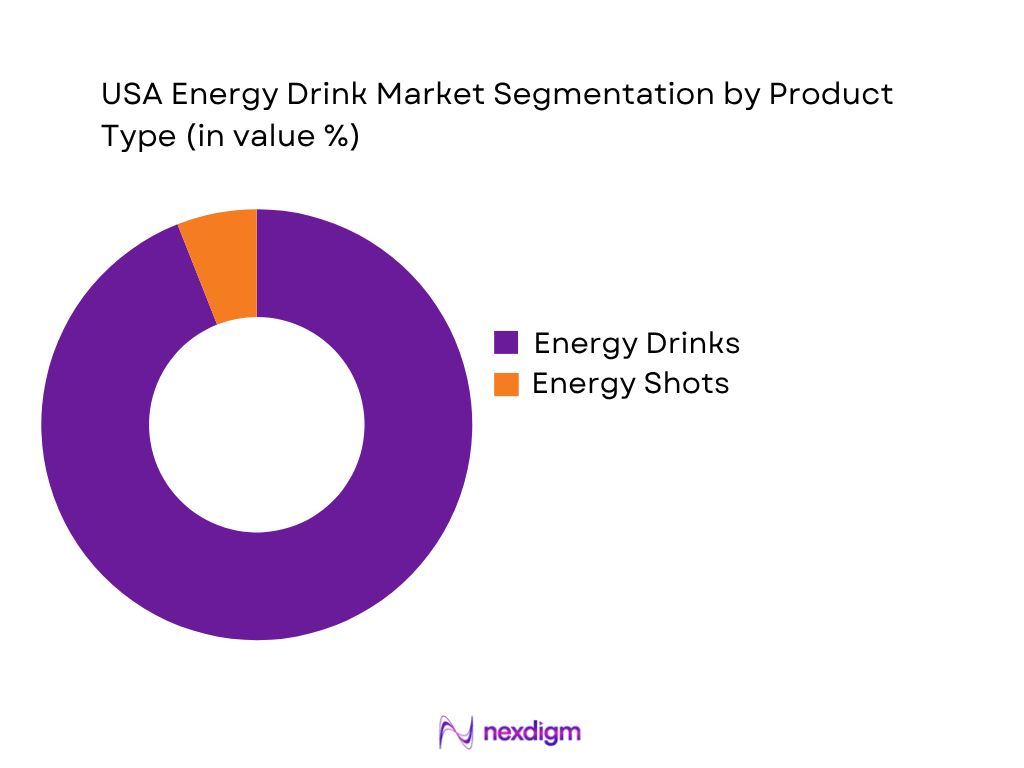

USA Energy Drink market is segmented by product type into energy drinks and energy shots. Energy drinks dominate the market with 94.0% share because ready-to-drink cans and bottles serve the largest number of consumption occasions, including commuting, work, study, gym, gaming and late-night productivity. The segment benefits from wide retail availability across supermarkets, hypermarkets, convenience stores and online channels, along with strong brand franchises such as Red Bull, Monster, Celsius, Rockstar, C4 and Ghost. Major brands support the segment through flavor extensions, zero-sugar variants, performance claims, esports sponsorships, extreme-sports marketing and multipack formats. Energy shots remain relevant for compact caffeine delivery, but their narrower use case, smaller shelf space and dependence on checkout placement limit their share compared with full-size RTD energy drinks.

By Packaging Type

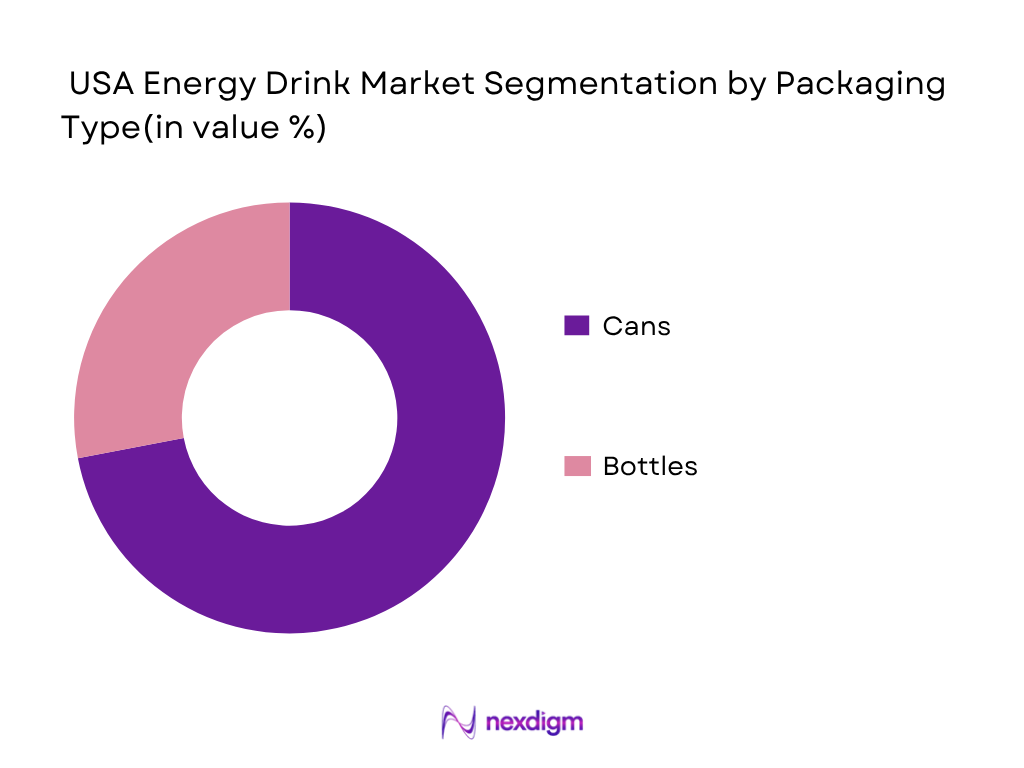

By Packaging Type: USA Energy Drink market is segmented by packaging type into cans, bottles and other formats. Cans dominate the market with 92.5% share because aluminum cans are highly aligned with the economics and consumption behavior of the category. They chill quickly, protect flavor and carbonation, fit cold-vault shelving, support impactful branding, and are easy to transport in single-serve and multipack formats. Leading energy drink brands use cans as their core pack architecture, especially 8.4 oz, 12 oz, 16 oz and slim-can formats. Retailers also prefer cans because they stack efficiently, maintain shelf stability and support fast replenishment in convenience stores and grocery cold sections. Bottled energy drinks have a smaller position, largely linked to non-carbonated, coffee-based, hydration-energy and premium functional formats.

Competitive Landscape

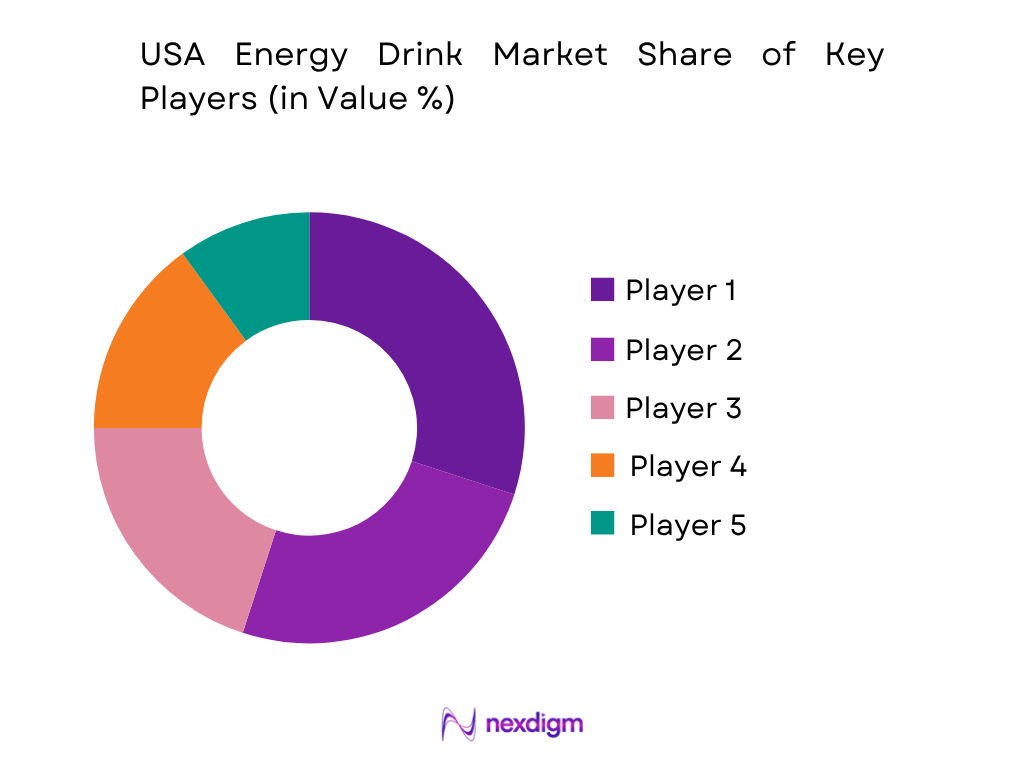

The USA energy drink market is consolidated at the top but increasingly fragmented in the challenger layer. Red Bull and Monster remain entrenched through brand equity, national distribution, sports sponsorships and high cold-vault visibility. Celsius, C4, Ghost, Alani Nu, Rockstar and 5-hour ENERGY have expanded competition through fitness positioning, zero-sugar formats, creator-led marketing, performance claims and channel-specific distribution. M&A has intensified, including Keurig Dr Pepper’s majority stake in Ghost and Celsius’s acquisition of Alani Nutrition, indicating that large beverage groups are using portfolio expansion to secure high-growth functional beverage demand.

| Company | Establishment Year | Headquarters | Core Energy Portfolio | Market Positioning | Packaging Strength | Distribution Strength | Product Innovation Focus | Strategic Edge |

| Red Bull GmbH / Red Bull North America | 1984 | Fuschl am See, Austria / Santa Monica, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Monster Beverage Corporation | 1935 | Corona, California | ~ | ~ | ~ | ~ | ~ | ~ |

| Celsius Holdings | 2004 | Boca Raton, Florida | ~ | ~ | ~ | ~ | ~ | ~ |

| PepsiCo | 1965 | Purchase, New York | ~ | ~ | ~ | ~ | ~ | ~ |

| Keurig Dr Pepper | 2018 | Burlington, Massachusetts / Frisco, Texas | ~ | ~ | ~ | ~ | ~ | ~ |

USA energy drink market Analysis

Growth Drivers

Expanding Workforce, Commuting Intensity and Daily Energy Occasions

The USA energy drink market is supported by a large working and mobile consumer base that creates repeat consumption occasions around commuting, shift work, study, gym usage and long workdays. The U.S. economy generated USD 28.75 trillion in GDP and USD 84,534 GDP per capita, indicating strong household purchasing capacity for discretionary functional beverages. The U.S. population reached 340.1 million, expanding the total addressable consumer base for packaged beverages. Daily mobility remains structurally important, with U.S. drivers covering 3.279 trillion vehicle-miles on roads, reinforcing convenience-store and gas-station beverage consumption. The Census Bureau also reported a 27.2-minute mean one-way travel time to work, supporting energy drink demand for morning, afternoon and late-day alertness occasions.

High Convenience-Store Reach and Cold-Vault Beverage Accessibility

Convenience retail remains a core growth driver for USA energy drinks because the category depends heavily on single-serve chilled purchases, impulse conversion and fuel-stop traffic. The U.S. convenience-store network included 151,975 stores, while 122,620 locations sold motor fuels, creating a dense last-mile retail network for energy drink brands. This aligns with high road mobility, as U.S. drivers logged 3.279 trillion vehicle-miles, supporting frequent beverage missions near highways, workplaces and urban corridors. Macroeconomic support also remains strong, with the World Bank reporting U.S. GDP at USD 28.75 trillion and GDP per capita at USD 84,534, enabling premium single-serve formats, multipacks, zero-sugar extensions and functional beverage experimentation. The channel’s operational fit with cans, chilled vaults and quick basket trips makes it especially relevant for Red Bull, Monster, Celsius, C4, Ghost, Rockstar and Alani Nu.

Market Challenges

Caffeine Scrutiny and Youth-Consumption Risk

Caffeine exposure is a major market-specific challenge for USA energy drinks because the category’s functional promise is directly linked to stimulant content. The FDA states that 400 milligrams of caffeine per day is generally not associated with negative effects for most adults, and compares that amount with roughly 2 to 3 standard 12-fluid-ounce cups of coffee. This creates a clear regulatory and communications boundary for high-caffeine energy drink brands, especially those positioned around performance, gaming, fitness and productivity. The CDC also notes that 3 to 5 in every 10 adolescents are reported to consume energy drinks, while the American Academy of Pediatrics recommends that adolescents do not consume them. With U.S. GDP per capita at USD 84,534, premium access is strong, but brand owners must manage labeling, serving-size clarity, caffeine disclosure and responsible marketing.

Retail Shelf Saturation and Velocity Pressure in Convenience Channels

The USA energy drink market faces intense shelf-space pressure because leading brands, challenger brands, private labels, energy shots, sports drinks, RTD coffee and hydration beverages compete for the same cold-vault real estate. The U.S. has 151,975 convenience stores and 122,620 fuel-selling convenience stores, which makes the channel large but also highly contested by fast-moving beverage categories. For energy drink manufacturers, this creates dependence on SKU velocity, promotional execution, distributor relationships, cooler-door placement and retailer category resets. The challenge is amplified by the large U.S. consumer base of 340.1 million, where national retail access is valuable but expensive to defend operationally. Macroeconomic capacity is strong, with GDP at USD 28.75 trillion, but retailers prioritize products that rotate quickly, carry strong brand pull and justify limited chilled shelf space.

Market Opportunities

Zero-Sugar, Low-Calorie and Better-for-You Energy Formulations

The strongest product opportunity in the USA energy drink market is the expansion of zero-sugar, low-calorie and cleaner-label formulations that retain energy functionality while reducing health-related friction. The CDC reported that at least 1 in 4 adults in every U.S. state and territory had obesity, creating a consumer environment where sugar-heavy beverages face stronger resistance and reformulated products have better positioning. FDA guidance around 400 milligrams of caffeine for most adults gives manufacturers a clear benchmark for responsible caffeine positioning, while allowing differentiation through natural caffeine, B-vitamins, electrolytes, amino acids and nootropic stacks. With U.S. GDP per capita at USD 84,534, consumers have the spending capacity to trade up to premium functional SKUs when benefits are clear and label claims are credible.

Urban, Campus, Gym and Mobility-Led Channel Expansion

The USA energy drink market has a strong opportunity to deepen penetration in urban retail, campuses, gyms, vending, micro-markets and workplace foodservice because these environments match high-frequency energy occasions. The World Bank-linked urban population indicator reports 284,043,692 people living in U.S. urban areas, supporting dense retail catchments for single-serve functional beverages. Major cities strengthen this demand base: New York City had 8,584,629 residents and Los Angeles had 3,869,089, creating large clusters of students, commuters, service workers, fitness users and office professionals. U.S. drivers also covered 3.279 trillion vehicle-miles, validating mobility-led sales through gas stations, travel stops and convenience stores. With the national economy at USD 28.75 trillion, brands can justify investment in targeted distribution, sampling, cooler placements and occasion-specific pack architecture.

Future Outlook

The USA Energy Drink market is expected to record a forecast CAGR of 8.37% during 2026–2035, with the market projected to reach USD 54.89 billion by 2035. Growth will be led by the normalization of energy drinks as everyday functional beverages, not just extreme-sports or late-night products. Zero-sugar formulations, natural caffeine, hydration-energy hybrids, gaming-focused products, gym-channel demand and premium flavor innovation will continue to expand consumption occasions.

The future market will be shaped by three structural shifts. First, traditional high-sugar formulations will continue losing momentum to sugar-free, low-calorie and clean-label variants. Second, channel growth will become more balanced as convenience stores remain critical but mass, club, grocery and online retail gain incremental volume. Third, competitive differentiation will move from caffeine alone toward benefit stacks, including focus, hydration, electrolytes, amino acids, vitamins, adaptogens and lifestyle-specific branding.

Regulatory scrutiny will remain a restraint, particularly around caffeine dosage, youth marketing, advertising claims and beverage classification. Companies with clear labeling, disciplined caffeine communication, strong retailer compliance and transparent functional claims will be better positioned. The most attractive white spaces include female-focused energy, workplace productivity beverages, campus retail, natural energy, low-stimulant products, pre-workout adjacency and subscription-led variety packs.

Major Players

- Red Bull North America

- Monster Beverage Corporation

- Celsius Holdings

- PepsiCo

- Keurig Dr Pepper

- Nutrabolt

- Ghost Lifestyle

- Alani Nutrition

- Bang Energy

- Rockstar Energy

- Prime Hydration

- ZOA Energy

- G Fuel

- Uptime Energy

- Living Essentials Marketing / 5-hour ENERGY

Key Target Audience

- Energy drink manufacturers and brand owners

- Functional beverage companies

- Carbonated soft drink companies entering energy beverages

- Convenience store and fuel retail chains

- Supermarket, mass merchandiser and club retail operators

- Packaging suppliers and aluminum can manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies (U.S. Food and Drug Administration, Federal Trade Commission, Consumer Product Safety Commission, state attorneys general, Alcohol and Tobacco Tax and Trade Bureau)

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map covering energy drink brands, bottlers, co-packers, ingredient suppliers, distributors, retailers, gyms, e-commerce platforms and regulatory stakeholders. Key variables include retail sales, manufacturer sales, units sold, price per ounce, caffeine strength, packaging format, channel penetration, ACV distribution, SKU velocity and repeat purchase behavior.

Step 2: Market Analysis and Construction

Historical market data is compiled from public market research sources, company disclosures, trade publications, retail channel indicators and product-level benchmarking. The analysis reviews product type, packaging type, pricing architecture, distribution channel mix, innovation frequency and brand-level activity to construct the USA Energy Drink market revenue base.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through interviews with beverage distributors, convenience retail category managers, grocery buyers, beverage consultants, co-packers, fitness retail operators and e-commerce beverage sellers. These consultations help verify pricing, shelf allocation, promotional pressure, consumer demand shifts, product margins and distribution bottlenecks.

Step 4: Research Synthesis and Final Output

The final phase triangulates bottom-up brand and SKU evidence with top-down functional beverage and retail-channel indicators. The output is refined by comparing company performance, product launches, M&A activity, consumer demand patterns and regulatory risks to produce a validated view of market size, segmentation, competition and future outlook.

- Executive Summary

- Research Methodology (market definitions, product inclusion-exclusion, RTD energy drink classification, caffeine threshold assumptions, retail scan triangulation, distributor interviews, brand benchmarking, channel checks, consumer cohort validation, top-down and bottom-up sizing)

- Definition and Scope

- Market Genesis and Evolution

- Energy Drink Category Business Cycle

- Category Role within Functional Beverages

- Growth Drivers (category tailwinds, channel expansion, consumer behavior, innovation frequency, pricing power)

- Market Challenges (regulatory risk, health concerns, channel saturation, input cost pressure, brand churn)

- Market Trends and Opportunities (white spaces, innovation themes, unmet demand, route-to-market expansion)

- Swot Analysis

- Porter’s Five Forces

- By Retail Sales Value (2020-2025)

- By Manufacturer Sales Value (2020-2025)

- By Volume (2020-2025)

- By Product Format (In Value %)

RTD Canned Energy Drinks

Energy Shots

Powdered Energy Mixes

Energy Concentrates - By Caffeine Strength (In Value %)

Low-Caffeine Energy Drinks

Standard-Caffeine Energy Drinks

High-Caffeine Energy Drinks

Natural-Caffeine Energy Drinks

Multi-Stimulant Energy Drinks - By Distribution Channel (In Value %)

Convenience Stores and Gas Stations

Supermarkets and Grocery Chains

Mass Merchandisers and Club Stores

Drugstores

E-Commerce and DTC - By Region (In Value %)

Northeast

Midwest

South

West

- Market Share of Major Players (retail sales value, unit sales, volume, off-premise share, channel share)

- Cross Comparison Parameters (caffeine mg per serving, zero-sugar SKU mix, flavor innovation frequency, cold-vault ACV distribution, DSD and bottler network strength, price per fluid ounce, social media and influencer reach, convenience-store velocity)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

Red Bull North America

Monster Beverage Corporation

Celsius Holdings

Keurig Dr Pepper

PepsiCo

The Coca-Cola Company

Nutrabolt

Ghost Lifestyle

Alani Nutrition

Bang Energy

Rockstar Energy

Prime Hydration

ZOA Energy

G Fuel

Uptime Energy

- FDA Classification Framework

- Caffeine Disclosure and Warning Practices

- Advertising and Youth Marketing Oversight

- School, Campus and Institutional Restrictions

- Health Claim and Performance Claim Compliance

- By Retail Sales Value (2026-2035)

- By Manufacturer Sales Value (2026-2035)

- By Volume (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now