Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA EV Charging Infrastructure market is valued at approximately USD ~ based on a recent historical assessment derived from U.S. Department of Energy Alternative Fuels Data Center infrastructure deployment records and company financial disclosures from major charging network operators. Market expansion is driven by federal funding programs, accelerating electric vehicle adoption across passenger and commercial fleets, and rapid deployment of high-power public charging corridors, alongside increasing utility investments in grid-integrated charging capacity nationwide.

California, Texas, Florida, New York, and Washington dominate the USA EV Charging Infrastructure market due to strong electric vehicle adoption, state-level zero-emission mandates, and extensive public charging investments. These regions benefit from dense urban populations, high vehicle electrification incentives, established utility electrification programs, and concentration of technology providers and charging network operators. Coastal metropolitan corridors and interstate freight routes further reinforce infrastructure clustering and sustained deployment momentum across these leading states.

Market Segmentation

By Product Type

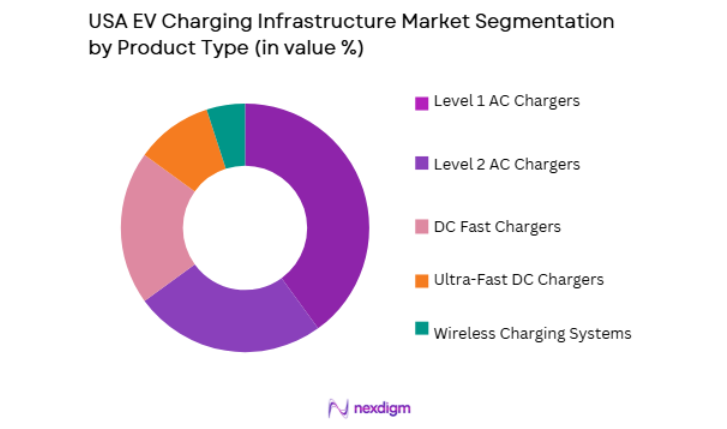

USA EV Charging Infrastructure market is segmented by product type into Level 1 AC Chargers, Level 2 AC Chargers, DC Fast Chargers, Ultra-Fast DC Chargers, and Wireless Charging Systems. Recently, DC Fast Chargers has a dominant market share due to factors such as expanding highway corridor networks, fleet electrification requirements, and demand for reduced charging dwell time in public locations. Public charging operators and utilities prioritize high-power installations to support long-distance travel and commercial vehicle uptime, while federal infrastructure funding programs emphasize fast-charging deployment along major transportation routes. Increasing battery capacities in electric vehicles require higher charging throughput, further reinforcing DC fast charging preference across urban and intercity applications. Retail, hospitality, and municipal sites deploy fast chargers to maximize utilization and revenue per parking space, strengthening commercial viability. Technological advances in power electronics and modular charger architecture have improved installation scalability and reliability, accelerating adoption across network operators nationwide.

By End User

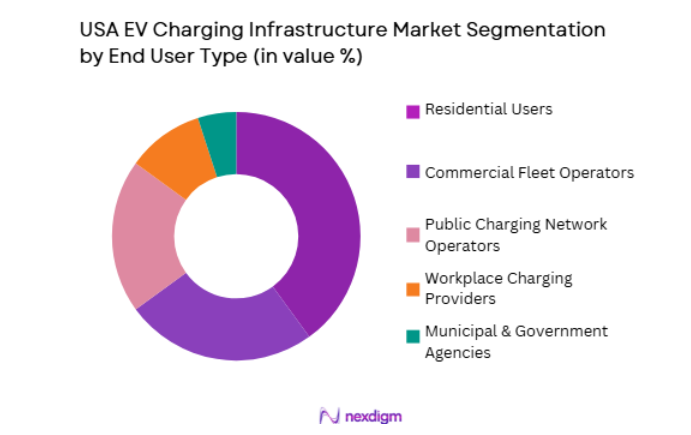

USA EV Charging Infrastructure market is segmented by end user into Residential Users, Commercial Fleet Operators, Public Charging Network Operators, Workplace Charging Providers, and Municipal & Government Agencies. Recently, Public Charging Network Operators has a dominant market share due to factors such as nationwide infrastructure rollout programs, public accessibility requirements, and revenue-generating charging services. Federal and state funding frameworks prioritize open-access charging stations, encouraging private network expansion across highways and urban centers. Public operators deploy large-scale charging hubs to serve diverse vehicle segments, including passenger vehicles, ride-hailing fleets, and light commercial vehicles. Interoperability mandates and roaming agreements further enhance utilization across networks, strengthening their market position. Retail partnerships and site-host agreements expand geographic coverage while reducing capital burden, enabling rapid network growth. Continuous investment from energy companies and infrastructure funds accelerates deployment scale and technological upgrades, consolidating operator dominance across the charging ecosystem.

Competitive Landscape

The USA EV Charging Infrastructure market is moderately consolidated, with major charging network operators and power equipment manufacturers shaping technology standards, deployment scale, and pricing models. Large energy companies and automotive-aligned charging providers are expanding nationwide networks through partnerships and acquisitions, while hardware manufacturers compete through high-power charger innovation and integrated software platforms. Competitive intensity is increasing as utilities, oil majors, and mobility service providers invest in public charging ecosystems and fleet electrification solutions.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Charging Network Size |

| ChargePoint Holdings | 2007 | USA | ~ | ~ | ~ | ~ | ~ |

| EVgo Services | 2010 | USA | ~ | ~ | ~ | ~ | ~ |

| Electrify America | 2017 | USA | ~ | ~ | ~ | ~ | ~ |

| Tesla Energy | 2003 | USA | ~ | ~ | ~ | ~ | ~ |

| Blink Charging | 2009 | USA | ~ | ~ | ~ | ~ | ~ |

USA EV Charging Infrastructure Market Analysis

Growth Drivers

Federal and State EV Infrastructure Funding Programs

The expansion of federal and state funding programs for electric vehicle charging infrastructure is a primary growth driver for the USA EV Charging Infrastructure market, creating sustained capital inflows and reducing investment risk for network developers. Large-scale public funding initiatives prioritize nationwide corridor coverage, urban charging accessibility, and rural deployment, enabling rapid installation of high-power charging stations across diverse geographic regions. Financial incentives, grants, and cost-sharing mechanisms encourage utilities, private operators, and municipalities to invest in charging networks that would otherwise face long payback periods. Standardization requirements tied to funding programs promote interoperability and open-access charging, improving consumer confidence and utilization rates. State-level zero-emission vehicle mandates further reinforce infrastructure expansion by linking vehicle adoption targets with charging availability benchmarks. Public funding also accelerates grid upgrades and interconnection capacity necessary for high-power charging hubs, enabling deployment of ultra-fast chargers. Infrastructure programs stimulate domestic manufacturing of charging equipment and components, strengthening supply chains and reducing procurement costs. Private investors and energy companies leverage public funding to scale commercial charging networks and fleet solutions, amplifying market growth momentum nationwide.

Accelerating Electric Vehicle Adoption Across Passenger and Commercial Fleets

Rapid growth in electric vehicle adoption across passenger cars, light commercial vehicles, and logistics fleets is significantly driving demand for charging infrastructure throughout the USA EV Charging Infrastructure market. Increasing availability of electric vehicle models with longer driving ranges encourages consumers and businesses to transition from internal combustion vehicles, raising the need for accessible and reliable charging networks. Commercial fleet electrification, particularly in delivery, ride-hailing, and municipal transport sectors, requires depot fast-charging infrastructure capable of supporting high-utilization operations. Automakers expanding electric vehicle production volumes collaborate with charging providers to ensure ecosystem readiness, stimulating infrastructure deployment. Rising fuel cost volatility and sustainability commitments among corporations further accelerate fleet electrification investments, translating into higher charging infrastructure demand. Public perception of electric vehicles improves as charging availability expands, creating a positive feedback loop between vehicle adoption and infrastructure rollout. Urban clean-air policies and emissions regulations incentivize businesses and consumers to adopt electric mobility, strengthening charging utilization rates. Growing electrification of heavy-duty and freight transport segments is expected to further intensify infrastructure requirements, sustaining long-term market expansion.

Market Challenges

High Grid Interconnection Costs and Power Capacity Constraints

One of the most significant challenges in the USA EV Charging Infrastructure market is the high cost and complexity of grid interconnection and power capacity upgrades required for high-power charging installations. Fast and ultra-fast charging stations demand substantial electrical capacity, often exceeding existing distribution infrastructure limits in urban and highway locations. Utilities must perform extensive upgrades to substations, transformers, and feeder lines before chargers can be deployed, significantly increasing project timelines and capital expenditure. Interconnection approval processes vary across states and utilities, creating regulatory uncertainty and administrative delays for developers. Power demand spikes from clustered charging hubs also raise concerns about grid stability and load management, requiring advanced energy management systems. Site developers face unpredictable upgrade costs that can exceed hardware installation expenses, affecting project viability. Rural and underserved regions often lack adequate grid capacity, limiting equitable charging deployment. Coordination challenges between utilities, regulators, and private operators further complicate large-scale infrastructure planning and execution nationwide.

Fragmented Standards and Interoperability Limitations Across Networks

The USA EV Charging Infrastructure market faces persistent challenges from fragmented technical standards, connector compatibility issues, and limited interoperability across charging networks. Different charging connector types, communication protocols, and authentication systems create inconsistent user experiences and restrict seamless vehicle-to-charger compatibility. Network operators often maintain proprietary software platforms and payment systems, preventing universal access and roaming functionality for electric vehicle users. Lack of standardization increases equipment costs for site hosts and fleets that must support multiple connector formats or network memberships. Software interoperability gaps hinder real-time data exchange, load management coordination, and network optimization across providers. Regulatory efforts toward open-access and interoperability requirements are still evolving, creating uncertainty for infrastructure investors. Consumers encountering incompatible chargers or payment barriers may lose confidence in electric mobility, reducing utilization rates. Achieving nationwide interoperability requires coordinated industry standards, regulatory enforcement, and technology integration, which remain complex and time-consuming processes across the fragmented charging ecosystem.

Opportunities

Integration of Renewable Energy and Energy Storage with Charging Hubs

The integration of renewable energy generation and stationary energy storage with electric vehicle charging hubs represents a major opportunity for the USA EV Charging Infrastructure market to enhance sustainability and operational efficiency. Solar-powered charging stations and battery storage systems can offset peak electricity demand and reduce grid upgrade requirements for high-power chargers. Energy storage enables load shifting and demand response participation, allowing charging operators to minimize electricity costs and improve profitability. Renewable-integrated charging hubs support corporate decarbonization goals and environmental compliance initiatives for fleet operators and municipalities. Utilities benefit from distributed energy resources co-located with charging infrastructure, improving grid resilience and balancing renewable intermittency. Public funding programs increasingly prioritize low-carbon infrastructure projects, encouraging renewable-powered charging deployments. Energy companies leverage integrated charging and storage systems to create multi-service energy hubs combining mobility and power services. Expansion of renewable-powered charging corridors along highways can enable low-emission long-distance travel and strengthen national clean-transportation strategies.

Electrification of Commercial and Freight Transport Charging Ecosystems

The electrification of medium- and heavy-duty commercial transport presents a significant growth opportunity for the USA EV Charging Infrastructure market through specialized high-capacity charging ecosystems. Freight logistics, port operations, and regional delivery fleets require megawatt-scale charging infrastructure capable of supporting large battery electric trucks and buses. Dedicated depot charging networks for commercial fleets enable predictable utilization and long-term service contracts, improving infrastructure investment returns. Government incentives targeting zero-emission freight corridors and urban delivery electrification accelerate adoption of commercial charging systems. Fleet operators prioritize electrification to reduce fuel costs and meet sustainability commitments, increasing demand for reliable high-power charging infrastructure. Charging providers can develop integrated fleet energy management platforms combining charging, scheduling, and telematics optimization. Ports, distribution centers, and logistics hubs become strategic nodes for high-capacity charging deployment, expanding infrastructure networks beyond passenger vehicle markets. The commercial transport segment offers higher energy throughput per site, strengthening revenue potential and long-term growth prospects for charging infrastructure providers.

Future Outlook

The USA EV Charging Infrastructure market is expected to expand significantly over the next five years, driven by continued electric vehicle adoption, large-scale public funding programs, and expansion of high-power charging networks. Technological advancements in ultra-fast charging, smart energy management, and grid-integrated infrastructure will improve charging speed and efficiency. Regulatory support and zero-emission vehicle mandates will accelerate deployment across urban and freight corridors. Growing fleet electrification and renewable-powered charging hubs will further strengthen long-term market demand.

Major Players

- ChargePoint Holdings

- EVgo Services

- Electrify America

- Tesla Energy

- Blink Charging

- ABB E-mobility

- Siemens eMobility

- Schneider Electric

- Tritium

- Wallbox

- FreeWire Technologies

- Volta Charging

- bp pulse

- SemaConnect

- Delta Electronics

Key Target Audience

- Automotive OEMs

- Charging Network Operators

- Electric Utilities

- Commercial Fleet Operators

- Retail & Hospitality Chains

- Investments and venture capitalist firms

- Government and regulatory bodies

- Energy Infrastructure Developers

Research Methodology

Step 1: Identification of Key Variables

Key market variables including charging capacity, installation rates, EV adoption levels, policy incentives, and infrastructure investments were identified through secondary sources such as government databases, industry reports, and company disclosures. These variables define market size, segmentation, and growth dynamics.

Step 2: Market Analysis and Construction

Market structure and segmentation were constructed by mapping charging technologies, end-user categories, deployment models, and regional infrastructure distribution. Historical deployment data and financial disclosures from charging providers and utilities were synthesized to estimate market values.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings and assumptions were validated through consultations with industry experts, charging infrastructure developers, utilities, and mobility analysts. Expert insights refined growth drivers, challenges, and technology adoption trends influencing infrastructure deployment.

Step 4: Research Synthesis and Final Output

All validated data and insights were integrated into a structured analytical framework to generate market size estimates, segmentation shares, competitive landscape, and future outlook. Consistency checks ensured alignment across datasets and narrative conclusions.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of federal and state EV infrastructure funding programs

Rising electric vehicle adoption across passenger and commercial fleets

Utility grid modernization supporting high-capacity charging deployment - Market Challenges

High installation and grid interconnection costs in urban areas

Power demand management and grid capacity constraints

Fragmented interoperability standards across charging networks - Market Opportunities

Deployment of ultra-fast charging corridors for long-distance travel

Integration of renewable energy and energy storage with charging hubs

Electrification of logistics and last-mile delivery fleets - Trends

Shift toward high-power DC fast charging and megawatt charging

Adoption of smart charging and load management software platforms

Growth of charging-as-a-service and subscription business models - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Level 1 AC Charging Systems

Level 2 AC Charging Systems

DC Fast Charging Systems

Wireless Inductive Charging Systems

Battery Swapping Infrastructure - By Platform Type (In Value%)

Public Charging Networks

Residential Charging Systems

Commercial Fleet Charging Depots

Highway Corridor Charging Stations

Workplace Charging Installations - By Fitment Type (In Value%)

Fixed Ground-mounted Chargers

Wall-mounted Charging Units

Mobile Portable Chargers

Pantograph Overhead Chargers

Integrated Parking-space Chargers - By EndUser Segment (In Value%)

Private EV Owners

Commercial Fleet Operators

Public Transport Authorities

Retail and Hospitality Operators

Municipal and Government Agencies - By Procurement Channel (In Value%)

Direct OEM Procurement

Utility-led Infrastructure Programs

Government Tender Projects

- Market Share Analysis

- Cross Comparison Parameters (Charging Power Output, Connector Standard Compatibility, Network Coverage, Charger Type Portfolio, Software & OCPP Integration, Energy Management Capability, Installation Model, Pricing Model, Service & Maintenance Support, Fleet Charging Solutions, Grid Integration & Load Management, Renewable Energy Integration)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

ChargePoint Holdings

EVgo Services

Electrify America

Tesla Energy

Blink Charging

SemaConnect

ABB E-mobility

Siemens eMobility

Schneider Electric EVlink

Wallbox Chargers

Tritium DCFC

FreeWire Technologies

Volta Charging

Greenlots

bp pulse

- Fleet operators prioritize depot fast charging to reduce downtime

- Municipal agencies invest in public charging for urban adoption

- Retail and hospitality sites deploy chargers to attract customers

- Residential users demand smart home-integrated charging solutions

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now