Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The U.S. EV charging stations market has witnessed significant growth, with a market size valued at USD ~ billion in 2025. This growth is largely driven by the surge in electric vehicle (EV) adoption across the country, coupled with government initiatives like the National Electric Vehicle Infrastructure (NEVI) program, which is designed to enhance charging infrastructure. The infrastructure expansion is also accelerated by major investments from both public and private sectors, particularly in urban areas and highways. The increasing shift toward sustainable energy and the rising need for accessible, reliable EV charging networks are expected to continue driving this upward trend in 2026 and beyond.

Key cities such as Los Angeles, San Francisco, and New York are central to the U.S. EV charging stations market, largely due to the high concentration of EVs, favorable policies, and the presence of a robust charging infrastructure. Additionally, states like California, Texas, and New York lead the way with their government-backed EV incentives and charging station deployment plans. The dominance of these regions is attributed to strong state support for clean energy, a high rate of EV adoption, and a growing consumer demand for convenient and fast charging options. These areas continue to attract investments, making them the hub for the nation’s EV infrastructure growth.

Market Segmentation

By Charging Type

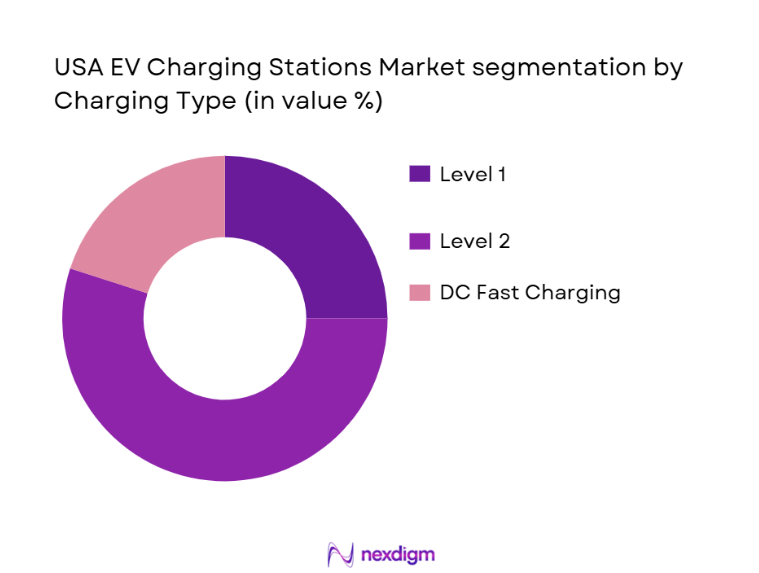

The U.S. EV charging stations market is segmented by charging types into Level 1, Level 2, and DC Fast Charging. Among these, Level 2 charging is expected to dominate the market in 2025. This is due to its balance of cost and charging speed, making it a popular choice for both residential and commercial charging stations. The widespread adoption of Level 2 chargers can be attributed to their affordability compared to DC Fast Chargers, alongside their suitability for longer-duration, overnight charging at home or in public spaces. Level 2 chargers are commonly used in workplaces, retail locations, and residential complexes due to their efficiency and relatively lower installation cost.

By Connector Standard

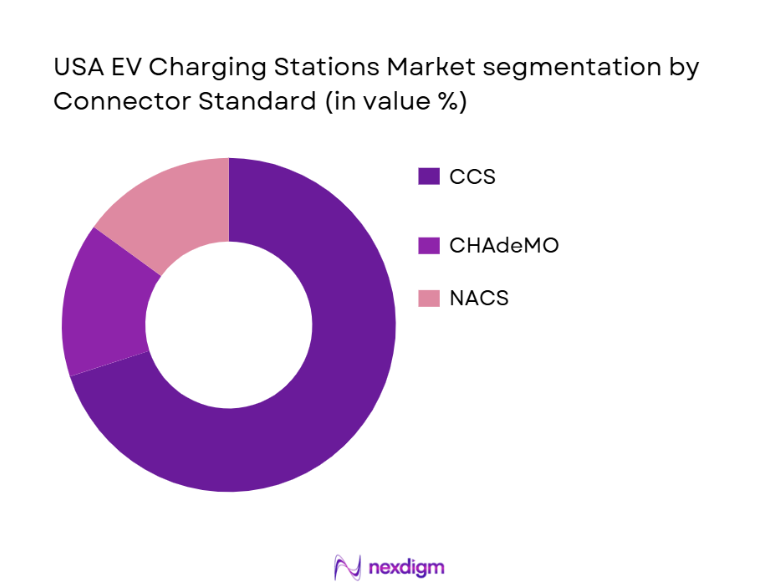

The market is also segmented by Connector Standard, with CCS (Combined Charging System) dominating the market share in 2024. This segment is driven by the widespread adoption of CCS connectors by both automakers and charging networks. The convenience of using a universal connector, supported by major EV manufacturers like General Motors, BMW, and Ford, has contributed to CCS’s popularity across the U.S. As more EV models adopt CCS as the standard connector, the adoption rate is expected to further increase, cementing its position as the dominant connector type in the market. The other types of connectors, like CHAdeMO, continue to lose market share, primarily due to the limited number of models supporting them.

Competitive Landscape

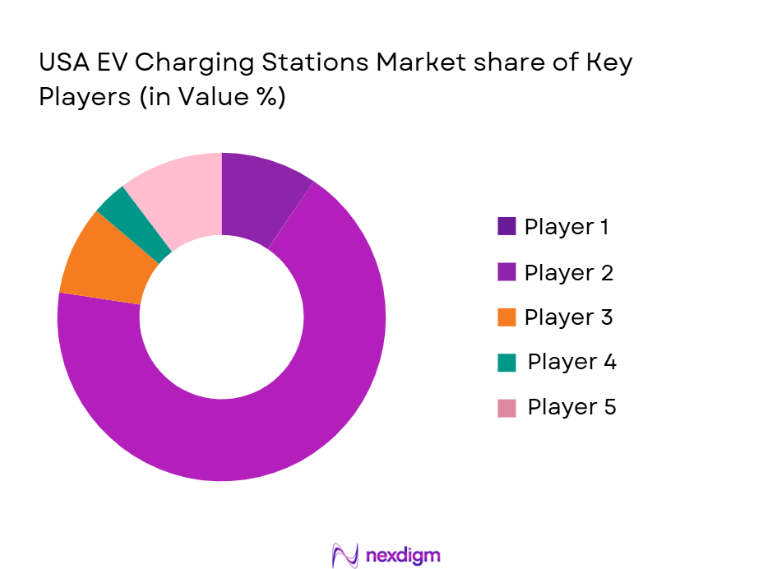

The U.S. EV charging stations market is dominated by several key players, each offering unique charging infrastructure solutions, software platforms, and charging services. The competition is characterized by a mix of global and local players, with companies like ChargePoint, Tesla, and EVgo leading the charge in infrastructure deployment. These companies benefit from strong brand recognition, significant capital investment, and extensive networks of EV charging stations. The competitive environment is marked by continuous innovation, with a focus on expanding coverage, enhancing charging speed, and developing user-friendly technologies.

| Company Name | Establishment Year | Headquarters | Product Offering | Number of Charging Stations | Partnerships | Revenue (2024) |

| ChargePoint | 2007 | California | ~ | ~ | ~ | ~ |

| Tesla | 2003 | California | ~ | ~ | ~ | ~ |

| EVgo | 2010 | California | ~ | ~ | ~ | ~ |

| Blink Charging | 2009 | Florida | ~ | ~ | ~ | ~ |

| Electrify America | 2017 | California | ~ | ~ | ~ | ~ |

USA EV Charging Stations Market Analysis

Growth Drivers

Government Support and Incentives

The U.S. government has significantly bolstered the EV charging infrastructure through programs such as the National Electric Vehicle Infrastructure (NEVI) program, offering substantial funding for the development of EV charging stations across the country. This support is aimed at expanding the public charging network to accommodate the growing number of electric vehicles on the road.

Rising EV Adoption

The increasing shift toward electric vehicles, spurred by consumer demand for eco-friendly alternatives and automaker commitments to electric mobility, is driving the need for expanded EV charging infrastructure. Automakers like Tesla, Ford, and GM are ramping up their electric vehicle offerings, fueling demand for a robust charging network to support this transition.

Market Challenges

High Installation Costs

Despite strong growth, the high upfront costs of installing EV charging stations—particularly DC fast chargers—remain a significant challenge. The expense associated with both hardware and grid infrastructure upgrades limits the pace at which networks can expand, especially in underserved areas.

Grid Capacity and Infrastructure Limitations

Many regions face grid capacity issues when attempting to expand charging infrastructure. The increased demand for charging stations can put additional pressure on the local grid, especially in high-demand areas, requiring substantial upgrades to ensure that charging networks are reliable and efficient.

Opportunities

Wireless Charging Technology

The emerging development of wireless charging offers an exciting opportunity for the market, particularly in the realm of urban mobility. If adopted widely, this technology could simplify the charging process, eliminate the need for cables, and improve overall user experience.

Integration with Renewable Energy Sources

There is a growing opportunity to integrate solar and wind energy with charging stations. This could reduce the reliance on the grid, lower operational costs, and make charging stations more sustainable, aligning with the broader trend toward renewable energy adoption in transportation.

Future Outlook

Over the next few years, the U.S. EV charging stations market is expected to show remarkable growth. This will be driven by continued government support, technological advancements, and a shift toward eco-friendly vehicles. Key trends include increased investment in ultra-fast charging technologies, integration with smart grids, and the rise of wireless charging solutions. Additionally, major car manufacturers are committing to 100% electric vehicle production, fueling the demand for more expansive and advanced charging networks. As the adoption of electric vehicles increases, the charging infrastructure will continue to evolve, providing more opportunities for growth and innovation in the market.

Major Players

- ChargePoint

- Tesla

- EVgo

- Blink Charging

- Electrify America

- ABB Ltd.

- Siemens AG

- Schneider Electric

- Leviton Manufacturing Co.

- Shell Recharge

- BP Pulse

- ClipperCreek

- Greenlots

- Volta Charging

- FLO

Key Target Audience

- Automobile Manufacturers

- Government and Regulatory Bodies

- Utility Providers and Grid Operators

- Charging Infrastructure Developers and Operators

- Venture Capital Firms and Investment Firms

- EV Owners and Fleet Operators

- Commercial and Residential Property Developers

- Retail and Hospitality Chains

Research Methodology

Step 1: Identification of Key Variables

This phase involves creating an ecosystem map of stakeholders in the U.S. EV charging stations market. Desk research is utilized, drawing from secondary data sources and proprietary databases to define and categorize variables impacting market dynamics, including technological advancements, regulatory trends, and consumer behavior.

Step 2: Market Analysis and Construction

Historical data on market penetration, infrastructure deployment, and service quality metrics is analyzed to build a comprehensive understanding of the market. This phase includes studying government policies, infrastructure investments, and the dynamics of service provider competition.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations will be conducted through interviews with industry leaders, infrastructure developers, and service providers. These experts will validate market hypotheses and provide insights on operational challenges, technological innovation, and growth drivers.

Step 4: Research Synthesis and Final Output

The final step involves gathering firsthand data from stakeholders, including EV manufacturers and public authorities, to confirm insights derived from previous steps. This process ensures the integration of qualitative and quantitative findings to generate a detailed market analysis.

- Executive Summary

- Research Methodology (Market Definitions, Abbreviations, Data Collection Framework, BottomUp Capacity & Deployment Forecast, TopDown Revenue Forecast, Charging Count Methodology, Forecast Assumptions & Pricing Normalization, Limitations & Boundary Conditions)

- Definition & Scope

- Market Genesis & Evolution

- Regulatory & Policy Landscape

- Charging Ecosystem & Value Chain

- Plug & Connector Standards

- Public vs Private Charging Models

- Growth Drivers

EV Penetration & ICE PhaseOut Policies

Federal & State Incentives

Technological Advancements

Fleet Electrification Trends - Market Challenges

High CapEx & Grid Capacity Constraints

Interoperability & Standardization Issues

RealEstate & Permitting Barriers

Utilization vs Underutilization Risks - Market Dynamics and Future Trends

Charging Vehicle Forecast vs Charge Points Needed

Smart Grid & V2G Integration

Renewable Energy & Storage Coupling

Wireless & Robotic Charging Emergence

CaaS & Digital Monetization Trends - Government Regulations & Infrastructure Programs

Federal Policies (NEVI, Bipartisan Infrastructure Acts)

StateLevel Initiatives

Subsidy & Incentive Mapping

Standard Compliance, Safety & Zoning

- Market by Revenue 2019-2025

- Market by Installed Charge Points 2019-2025

- Market by Charging Category 2019-2025

- Market by Connector Adoption 2019-2025

- Market by Ownership Model 2019-2025

- By Charging Type (In Value%)

Level 1

Level 2

DC Fast Charging - By Connector Standard (In Value%)

CCS

CHAdeMO

NACS

Wireless Charging - By Market EndUse (In Value%)

Residential Charging

Public Charging

Commercial Charging

Fleet / EV Logistics - By Operator Model (In Value%)

Charge Point Operators

Independent Stations

OEMbacked Networks

Public-Private Partnership Models - By Deployment Location (In Value%)

Urban Areas

Suburban Areas

Highway / Corridor Charging

Rural Areas - By Infrastructure Ownership (In Value%)

Private Ownership

Public Ownership

Hybrid - By Charging Network Business Models (In Value%)

Hardware Sales

Software Platforms

CaaS - By Revenue Streams (In Value%)

Hardware Revenue

Software Revenue

CPO Recurring Revenue

Energy Sales

ValueAdded Services

- Market Concentration Analysis

- Revenue & Charge Point Market Share

- Competitive Positioning Map (Price vs Coverage)

- Strategic Benchmark Matrix

- Investment Activity & M&A Overview

- CrossComparison Parameters (Network Coverage, Charging Output Capability, Business Model, Technology Stack, Capital & R&D Intensity, Interoperability, Strategic Alliances & Partner Ecosystems, Deployment Speed & Rollout Execution)

- Competitive Profile of Key Players

ChargePoint, Inc.

Tesla, Inc.

EVgo Services LLC

Electrify America LLC

Blink Charging Co.

bp pulse (EV Solutions)

ABB Ltd.

SemaConnect, Inc.

General Electric Company

Tritium (EV Chargers)

Greenlots / Shell Recharge

Monta (Network Software)

ClipperCreek, Inc.

Leviton Manufacturing Co.

Enel X / JuiceBox Solutions - Technology & Innovation Mapping

Smart Charging Platforms

Ultrafast & Modular Chargers

Software & Management Tools

V2G & Load Balancing

Future Technologies - Price & Commercial Benchmarking

Charging Pricing Models

Cost of Installation & BoM Trends

ROI Models by Deployment Type

ValueAdded Service Economics

- EV Driver Charging Preferences & Frequency

- Willingness to Pay & Pricing Elasticity

- Enterprise Buyer Needs (Fleet / Commercial)

- Decision Process for Site Hosts

- By Revenue 2026-2030

- By Installed Port Count 2026-2030

- By Charging Type Mix 2026-2030

- By EndUse Segment 2026-2030

- By Connector Adoption 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now