Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA EV insulation materials market is valued at USD ~ billion, driven by the rapid adoption of electric vehicles and the increasing focus on improving battery safety and efficiency. As automakers continue to innovate with new battery chemistries and electric drivetrains, insulation materials that manage heat dissipation, electromagnetic interference (EMI), and noise reduction have become crucial. The market is driven by regulatory pressures to meet safety standards, reduce energy consumption, and optimize vehicle performance. In addition, the shift toward sustainable and lightweight materials is expected to further fuel market demand, as automakers seek to enhance the overall energy efficiency of EVs.

The USA is home to several key regions that dominate the EV insulation materials market. The Midwest, particularly Michigan, is a hub for automotive manufacturing and EV production, contributing significantly to the demand for insulation materials. California is also a major player, known for its innovative approach to electric vehicle technology and a large consumer market for EVs. These regions are supported by strong OEMs, such as General Motors and Tesla, as well as battery manufacturers, which continue to drive technological advancements and material requirements in insulation. Additionally, global supply chain hubs in the USA further boost demand.

Market Segmentation

By Material Type

In the USA EV insulation materials market, thermal insulation dominates the material type segment due to the increasing focus on battery thermal management and safety. As EV battery packs require effective heat regulation to prevent thermal runaway and ensure long-term performance, materials like thermal interface materials (TIM), aerogels, and foams are gaining significant traction. These materials help maintain the battery at an optimal temperature, which directly impacts the vehicle’s efficiency and safety. The growing demand for high-performance, lightweight thermal materials that offer superior heat resistance is driving this segment.

By Application

Battery insulation is the dominant application in the USA EV insulation materials market. As the adoption of EVs continues to rise, ensuring battery safety and performance has become paramount. Battery insulation materials help manage temperature fluctuations within the battery pack, which is critical in preventing thermal runaway, a significant safety risk. These materials also enhance energy efficiency by minimizing heat loss. With innovations in battery technology and increasing consumer demand for electric vehicles, battery insulation remains a priority for OEMs and material suppliers.

Competitive Landscape

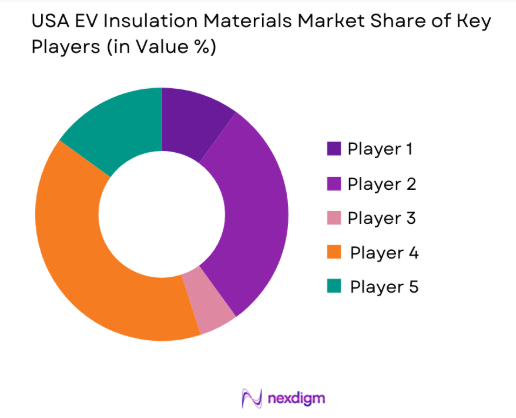

The USA EV insulation materials market is dominated by a few major players, including 3M, Saint-Gobain, and BASF. These companies are leaders in innovation, providing advanced materials for thermal, electrical, and acoustic insulation needs in electric vehicles. Their dominance is bolstered by their extensive global supply chains, strong R&D capabilities, and strategic partnerships with automotive OEMs and battery manufacturers.

| Company | Establishment Year | Headquarters | Material Expertise | R&D Investment | Supply Chain | Global Presence | Manufacturing Plants |

| 3M Company | 1902 | St. Paul, Minnesota | ~ | ~ | ~ | ~ | ~ |

| Saint-Gobain | 1665 | Courbevoie, France | ~ | ~ | ~ | ~ | ~ |

| BASF SE | 1865 | Ludwigshafen, Germany | ~ | ~ | ~ | ~ | ~ |

| Morgan Advanced Materials | 1856 | Windsor, UK | ~ | ~ | ~ | ` | ~ |

| Zotefoams plc | 1994 | Croydon, UK | ~ | ~ | ~ | ~ | ~ |

USA EV Insulation Materials Market Analysis

Growth Drivers

Higher Pack Voltage Architectures Increasing Insulation Criticality

The shift toward higher voltage architectures in electric vehicle (EV) battery packs is driving an increased need for advanced insulation solutions. As battery pack voltage increases, the risk of electrical faults, short circuits, and thermal runaway becomes more significant. To prevent these issues, effective insulation systems are essential to maintain the safety and performance of the battery. The rising focus on higher energy densities and the push for faster, more powerful EVs means that insulation materials must evolve to handle greater electrical loads, preventing accidents and ensuring the reliability of these advanced battery systems.

Fast Charging Platforms Raising Thermal and Fire Safety Requirements

The growth of fast-charging platforms for electric vehicles is driving the need for enhanced thermal and fire safety solutions. As fast-charging rates increase, so does the heat generated within the battery pack, leading to higher risks of thermal runaway and potential fires. Fast-charging platforms require robust insulation systems capable of managing high temperatures and mitigating the risk of fire or other safety hazards. This growth in fast-charging infrastructure creates an urgent need for insulation materials that can withstand extreme temperatures, provide effective heat dissipation, and maintain safety standards under rapid charging conditions.

Challenges

Qualification Lead Times and Platform Lock-in Effects

One of the primary challenges in the adoption of new insulation technologies is the lengthy qualification lead times required to meet safety and performance standards. Battery pack manufacturers typically face long testing and certification processes before new insulation materials or systems can be used in production. This extended timeline can delay the adoption of improved materials. Additionally, the platform lock-in effect, where manufacturers are committed to existing insulation systems due to design and compatibility requirements, can hinder the flexibility needed to integrate newer, more effective solutions. These factors slow down innovation and the implementation of next-generation insulation technologies.

Trade-offs Between Weight, Thickness, and Insulation Performance

A significant challenge in designing insulation materials for battery packs is balancing weight, thickness, and insulation performance. To meet the performance and safety requirements, insulation must provide adequate protection against electrical faults and thermal risks. However, adding insulation increases the overall weight and thickness of the battery pack, which can reduce the vehicle’s range and performance. Manufacturers must navigate these trade-offs to create materials that provide the necessary protection without sacrificing energy efficiency, vehicle weight, or performance. This balance is crucial for developing high-performance EVs with safe and reliable battery systems.

Opportunities

Next-Generation Thermal Runaway Barrier Solutions with Lower Mass

The development of next-generation thermal runaway barrier solutions presents an opportunity to improve safety while minimizing the mass of the battery pack. By designing lighter, more efficient materials that can prevent thermal runaway without adding excessive weight, manufacturers can create safer battery systems that do not compromise vehicle performance. These advanced barrier solutions would provide better thermal management, helping to prevent overheating and fire hazards during fast charging or under heavy use, making them an attractive addition to future EV battery packs that prioritize both safety and energy efficiency.

Multifunctional Materials Combining Insulation, Sealing, and NVH

The opportunity to develop multifunctional materials that combine insulation, sealing, and noise, vibration, and harshness (NVH) properties is an emerging trend in the automotive sector. These materials can offer integrated solutions that provide thermal and electrical insulation, seal the battery pack from contaminants, and reduce noise and vibration. By combining multiple functions into one material, manufacturers can reduce the complexity and cost of battery pack designs while improving performance across multiple dimensions. These multifunctional materials provide an efficient, streamlined approach to enhancing battery safety, durability, and user experience in electric vehicles.

Future Outlook

The USA EV insulation materials market is expected to see continued growth over the next five years, fueled by the ongoing advancements in electric vehicle technology, particularly in battery efficiency, safety, and thermal management. Innovations in materials, such as lighter, more efficient foams and composites, will play a significant role in meeting the needs of EV manufacturers. As governments continue to promote green energy solutions and electric vehicle adoption, the demand for high-performance insulation materials will continue to rise, leading to new opportunities for manufacturers.

Major Players

- 3M Company

- Saint-Gobain

- BASF SE

- Morgan Advanced Materials

- Zotefoams plc

- Unifrax LLC

- Dow Chemical

- Covestro AG

- Elmelin Ltd.

- Pyrophobic Systems Ltd.

- Parker Hannifin Corporation

- Von Roll Holding AG

- Autoneum Holding AG

- Alder Pelzer Holding GmbH

- Covestro AG

Key Target Audience

- Automobile Manufacturers (OEMs)

- Battery Manufacturers

- Tier 1 & Tier 2 Suppliers

- Raw Material Suppliers

- Electric Vehicle Regulatory Bodies (e.g., NHTSA, EPA)

- Charging Infrastructure Providers

- Material Suppliers

- Investments and Venture Capitalist Firms

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the critical variables influencing the USA EV insulation materials market, including market drivers, material types, and key applications. Secondary research will be conducted to collect comprehensive industry data and trends.

Step 2: Market Analysis and Construction

We will analyze historical data from the past five years, assessing trends in material demand and pricing, and creating detailed market models. We will consider factors such as regional variations and consumer behavior in EV markets.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and tested with industry experts through structured interviews. This will include discussions with OEMs, battery manufacturers, and material suppliers to validate data points and assumptions.

Step 4: Research Synthesis and Final Output

The final phase will involve synthesizing all collected data and insights, refining the conclusions through direct engagement with key stakeholders in the EV industry, ensuring an accurate and validated market outlook.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, EV insulation materials taxonomy, market sizing logic by material consumption per vehicle and pack, value attribution across electrical thermal and acoustic functions, primary interview program with OEMs Tier 1s converters and material suppliers, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Evolution of EV Insulation Requirements

- Insulation Role in High Voltage Safety Thermal Control and NVH

- EV Architecture Mapping Across Battery Pack E Drive and Harness Systems

- Qualification Standards and Validation Pathways for EV Grade Materials

- Supply Chain Structure Across Formulators Converters and Tier 1 Integrators

- Growth Drivers

Higher pack voltage architectures increasing insulation criticality

Fast charging platforms raising thermal and fire safety requirements

OEM focus on thermal runaway containment and propagation resistance

Expansion of domestic EV and battery production capacity

Stricter validation and traceability expectations for safety materials - Challenges

Qualification lead times and platform lock in effects

Trade offs between weight thickness and insulation performance

Supply risk for specialty fillers silicones and aramid inputs

Manufacturing variability in converting and lamination processes

Recycling compatibility and end of life material separation issues - Opportunities

Next generation thermal runaway barrier solutions with lower mass

Multifunctional materials combining insulation sealing and NVH

Localization of converting kitting and rapid prototyping services

Non silicone alternatives for contamination sensitive electronics

High volume automation friendly formats for pack assembly lines - Trends

Shift toward multifunctional hybrid insulation stacks

Increased use of aerogels and advanced composites in packs

Standardization of insulation architectures across vehicle platforms

Rising demand for documented compliance and batch traceability

Design for recyclability influencing material selection and formats - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Volume Consumption, 2019–2024

- By Battery Pack vs Power Electronics Revenue Split, 2019–2024

- By ASP and Material Family Mix, 2019–2024

- By Fleet Type (in Value %)

Battery electric passenger vehicles

Plug in hybrid passenger vehicles

Electric commercial vans and light trucks

Heavy duty electric trucks and buses

Off highway and specialty electrified vehicles - By Application (in Value %)

Battery pack thermal runaway barrier layers

Busbar and cell interconnect insulation

Power electronics potting and encapsulation

E motor slot and winding insulation

High voltage cable and connector insulation - By Technology Architecture (in Value %)

Thermal and fire barrier mats and sheets

Electrical films laminates and tapes

Silicone gaskets foams and seals

Coatings potting compounds and encapsulants

Aerogels and advanced insulation composites - By Connectivity Type (in Value %)

Direct OEM specification and nomination

Tier 1 integrated subsystem supply

Converter and die cut kit supply model

Contract manufacturing and co development programs

Authorized distribution and service supply - By End-Use Industry (in Value %)

EV OEMs and platform engineering teams

Battery pack integrators and module assemblers

Cell manufacturers and gigafactory operators

Power electronics suppliers

Wiring harness and connector suppliers - By Region (in Value %)

West Coast EV manufacturing corridor

South Central battery belt

Midwest automotive manufacturing region

Southeast EV and battery investments region

Northeast engineering and retrofit clusters

- Positioning driven by safety performance manufacturing scalability and qualification depth

- Partnership models between insulation suppliers OEMs and battery manufacturers

- Cross Comparison Parameters (dielectric strength at pack voltage, thermal runaway barrier performance, flammability rating and compliance, thickness and weight per interface, maximum continuous operating temperature, chemical resistance to electrolytes and coolants, adhesive compatibility and bond durability, converting capability and lead time)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles of Companies

3M

DuPont

Saint Gobain

Henkel

Dow

BASF

SGL Carbon

Morgan Advanced Materials

Rogers Corporation

Parker Hannifin Chomerics

Lydall

Aspen Aerogels

Wacker Chemie

Momentive

Von Roll

- OEM nomination criteria and validation checkpoints

- Battery pack engineering priorities for safety serviceability and manufacturability

- Process constraints for lamination die cutting and adhesive application

- Cost drivers across grams per vehicle yield and scrap rates

- Supplier scorecards for quality responsiveness and change control

- By Value, 2025–2030

- By Volume Consumption, 2025–2030

- By Battery Pack vs Power Electronics Revenue Split, 2025–2030

- By ASP and Material Family Mix, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now