Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA EV thermal interface materials market is valued at USD ~ billion, primarily driven by the rapid expansion of the electric vehicle (EV) industry, which demands enhanced thermal management solutions to ensure the safety and efficiency of critical vehicle components. As EV adoption continues to increase and battery systems grow in power density, the need for efficient and reliable thermal interface materials is more important than ever. This market is heavily influenced by factors such as increasing electric vehicle production, rising energy density requirements in batteries, and the focus on reducing vehicle emissions, driving substantial demand for high-performance TIMs in the automotive industry.

The dominant cities in the USA contributing to the growth of the EV thermal interface materials market include Detroit, Michigan, Silicon Valley, California, and Los Angeles. Detroit, being the heart of the U.S. automotive industry, remains a key hub for automotive OEMs and Tier-1 suppliers. Silicon Valley’s prominence in advanced technology and innovation also influences the market, with numerous startups and R&D firms specializing in next-generation materials. Los Angeles plays a critical role as a major EV consumer market. Together, these regions represent the core of U.S. EV manufacturing, technological advancement, and EV adoption.

Market Segmentation

By Product Type

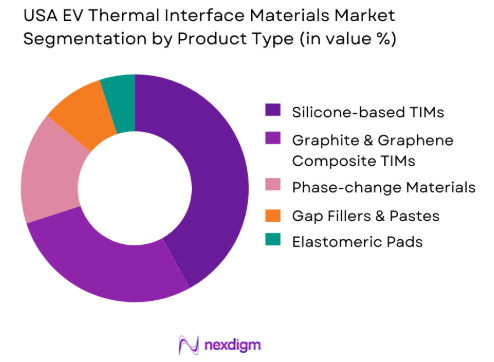

The USA EV thermal interface materials market is segmented by product type into silicone-based TIMs, graphite and graphene composite TIMs, phase-change materials, gap fillers, and elastomeric pads. Among these, silicone-based TIMs hold a dominant market share. This dominance can be attributed to their high thermal conductivity and electrical insulation properties, which are vital for managing heat in various components such as battery packs and power electronics. Additionally, silicone-based TIMs offer excellent durability in high-temperature conditions, making them ideal for EV applications where both efficiency and safety are paramount.

By Application Type

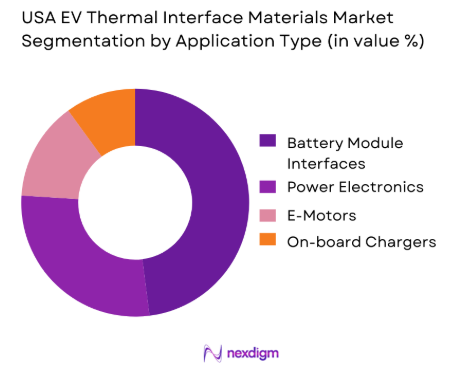

The USA EV thermal interface materials market is also segmented by application type, including battery module interfaces, power electronics, e-motors, and on-board chargers. The battery module interface segment dominates, driven by the need to address the high power density and heat dissipation challenges associated with EV batteries. As battery systems become larger and more energy-dense, the demand for effective thermal interface materials increases to prevent thermal runaway and optimize overall battery performance. This trend is further supported by advancements in battery technology and increased regulatory focus on battery safety and efficiency.

Competitive Landscape

The USA EV thermal interface materials market is dominated by a few major players, including 3M and global brands like Henkel, Laird Performance Materials, Momentive, and Dow Inc. This consolidation highlights the significant influence of these key companies. These players leverage their strong brand presence, extensive product portfolios, and deep R&D investments to stay ahead in the highly competitive market. Their dominance is further reinforced by their established relationships with major EV OEMs and tier-1 suppliers, ensuring a continuous demand for high-performance TIMs.

| Company | Establishment Year | Headquarters | Product Portfolio | R&D Investment | Distribution Network | Market Focus | Revenue Generation | Customer Base | Geographic Presence |

| 3M | 1902 | St. Paul, MN | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Henkel | 1876 | Düsseldorf, Germany | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Laird Performance Materials | 2005 | London, UK | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Momentive | 2006 | Waterford, NY | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Dow Inc. | 1897 | Midland, MI | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

USA EV Thermal Interface Materials Market Analysis

Growth Drivers

Higher Pack Energy Density Driving Tighter Thermal Margins

As battery pack energy densities continue to rise, the need for efficient thermal management becomes increasingly critical. Higher energy densities lead to greater heat generation during both charging and discharging cycles, tightening the thermal margins within battery packs. This makes effective thermal management solutions essential to prevent overheating, ensure safe operation, and enhance battery lifespan. Advanced thermal interface materials (TIMs), such as thermal pastes and phase change materials, are in greater demand to manage the heat generated by high-density energy packs. The increased focus on high energy density pushes innovation in thermal management technologies to maintain performance and safety.

Fast Charging Adoption Increasing Heat Flux Requirements

The adoption of fast charging technologies is driving the need for more advanced thermal management solutions. Fast charging significantly increases the heat flux within battery packs, requiring robust cooling solutions to dissipate the excess heat and prevent damage to the battery cells. The higher current associated with fast charging generates more heat, which can degrade battery performance or lead to safety hazards if not properly managed. As the industry shifts towards ultra-fast charging platforms, the demand for efficient heat dissipation technologies, such as high-performance thermal materials, continues to grow to meet the heat management challenges posed by fast charging.

Challenges

Qualification Lead Times and Platform Lock-In Effects

One of the key challenges in adopting new thermal management materials is the lengthy qualification lead times required for new technologies to meet industry standards. In sectors such as automotive or consumer electronics, rigorous testing and certification processes are essential to ensure the reliability and safety of thermal solutions. These qualification processes can be time-consuming, which delays the implementation of advanced thermal materials. Additionally, the platform lock-in effect, where manufacturers are tied to existing thermal management systems due to compatibility or contract limitations, can restrict the adoption of newer, more effective solutions. Overcoming these challenges requires more agile testing and validation processes and the ability to integrate new materials into established platforms.

Dispensing Process Variability and Yield Sensitivity

Another significant challenge is the variability in the dispensing process and its impact on yield sensitivity. In the production of battery packs and electronic devices, the application of thermal materials, such as greases, gels, and adhesives, must be precise to ensure optimal heat transfer and prevent overheating. However, inconsistencies in the dispensing process—whether in terms of volume, uniformity, or application technique—can lead to performance issues, including poor heat dissipation or material wastage. This variability can affect the overall efficiency of the thermal management system and lead to yield losses, complicating the scaling of production and increasing manufacturing costs.

Opportunities

Next Generation Low Pump-Out Greases and Stable Gels

The development of next-generation low pump-out greases and stable gels presents a promising opportunity for improving thermal management in battery systems. These materials are designed to remain stable under high temperatures and mechanical stress, ensuring consistent thermal performance over time. Low pump-out greases reduce the risk of material migration, which can degrade thermal efficiency and lead to hot spots in battery packs. Stable gels, which offer enhanced thermal conductivity, also help maintain optimal heat dissipation. These advanced materials are crucial for ensuring the longevity and safety of high-density energy packs and are particularly beneficial in high-performance applications such as fast charging.

High Conductivity Gap Fillers for Ultra-Fast Charging Platforms

The development of high conductivity gap fillers for ultra-fast charging platforms offers an exciting opportunity in the thermal management market. As fast charging becomes more widespread, the need for efficient heat dissipation solutions intensifies. High conductivity gap fillers are designed to fill small gaps between components, improving the overall thermal path and ensuring that heat is efficiently transferred away from sensitive components like battery cells and power electronics. These materials enable ultra-fast charging platforms to handle the increased heat flux associated with rapid energy transfer while maintaining safe operating temperatures. Their integration into fast-charging systems is crucial for enabling higher charging speeds without compromising the safety and performance of the battery.

Future Outlook

In the coming years, the USA EV thermal interface materials market will continue to grow, driven by advancements in battery technology and the increasing demand for energy-efficient EVs. Innovations in material science, particularly in the development of graphene-based and phase-change materials, will reshape the market landscape, offering manufacturers more effective solutions for managing heat in high-performance vehicle systems.

Major Players

- 3M

- Henkel

- Laird Performance Materials

- Momentive

- Dow Inc.

- Parker Hannifin Corporation

- Indium Corporation

- AI Technology

- Fujipoly

- Henkel AG

- Wakefield-Vette

- Shin-Etsu Chemical Co., Ltd.

- Lord Corporation

- Sumitomo Electric Industries

- Thermagon

Key Target Audience

- Automotive OEMs

- EV Battery Manufacturers

- Thermal Management Suppliers

- EV Tier-1 Component Manufacturers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies (U.S. Department of Energy)

- Automotive Aftermarket

- System Integrators

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying key variables impacting the EV thermal interface materials market, focusing on product performance, material costs, and technology adoption. This process relies on secondary research and market interviews to gather industry insights.

Step 2: Market Analysis and Construction

This phase includes assessing historical market data to identify trends and forecast future growth. A comprehensive market model is constructed based on product categories, key drivers, and technological innovations, ensuring accuracy in predictions.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations are conducted to validate the hypotheses, ensuring that market dynamics and assumptions align with industry realities. These interviews are key in refining and confirming our market outlook.

Step 4: Research Synthesis and Final Output

The final phase synthesizes all collected data, combining both primary and secondary sources to finalize the market analysis and provide actionable insights for stakeholders in the EV thermal interface materials market.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, EV thermal interface materials taxonomy, market sizing logic by material consumption per vehicle and pack, value attribution across interface points and form factors, primary interview program with OEMs Tier 1s and material suppliers, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Evolution of EV Thermal Management Materials

- Thermal Interface Role in Battery Safety Power Density and Fast Charging

- EV Pack and E Drive Interface Point Mapping

- Qualification Cycles and Automotive Grade Validation Requirements

- Supply Chain Structure Across Formulators Converters and Tier 1 Integrators

- Growth Drivers

Higher pack energy density driving tighter thermal margins

Fast charging adoption increasing heat flux requirements

Shift toward structural packs and integrated thermal designs

OEM focus on safety validation and thermal runaway mitigation

Domestic battery and EV manufacturing capacity expansion - Challenges

Qualification lead times and platform lock in effects

Dispensing process variability and yield sensitivity

Material outgassing contamination and reliability constraints

Thermal aging under high voltage and cycling stress

Supply risk for specialty fillers and silicone inputs - Opportunities

Next generation low pump out greases and stable gels

High conductivity gap fillers for ultra fast charging platforms

Non silicone alternatives for contamination sensitive electronics

Automation ready materials for high throughput dispensing lines

Recycling compatible materials and low VOC manufacturing - Trends

Move toward higher conductivity with lower density materials

Increased use of multi functional TIMs with insulation properties

Standardization of interface designs across vehicle platforms

Greater collaboration between material formulators and pack designers

Rising demand for in line quality control and traceable batches - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Volume Consumption, 2019–2024

- By Battery Pack vs Power Electronics Revenue Split, 2019–2024

- By ASP and Form Factor Mix, 2019–2024

- By Fleet Type (in Value %)

Battery electric passenger vehicles

Electric commercial vans and light trucks

Heavy duty electric trucks and buses

Performance and premium EV platforms

Off highway and specialty electrified vehicles - By Application (in Value %)

Cell to module thermal interfaces

Module to cold plate interfaces

Pack lid and enclosure thermal pathways

Inverter and power electronics heat spreading

E motor and stator thermal conduction interfaces - By Technology Architecture (in Value %)

Thermal greases and pastes

Gap fillers and dispensable gels

Thermal pads and elastomeric sheets

Phase change materials

Thermally conductive adhesives and underfills - By Connectivity Type (in Value %)

Direct OEM specification and nomination

Tier 1 integrated thermal subsystem supply

Converter and die cut kit supply model

Contract manufacturing and co development programs

Authorized distribution and service supply - By End-Use Industry (in Value %)

EV OEMs and platform engineering teams

Battery pack integrators and module assemblers

Cell manufacturers and gigafactory operators

Power electronics suppliers

Thermal management subsystem suppliers - By Region (in Value %)

West Coast EV manufacturing corridor

South Central battery belt

Midwest automotive manufacturing region

Southeast EV and battery investments region

Northeast engineering and retrofit clusters

- Positioning driven by conductivity stability manufacturability and qualification depth

- Partnership models between TIM suppliers OEMs and battery manufacturers

- Cross Comparison Parameters (thermal conductivity at operating conditions, viscosity and dispense window, pump out and bleed resistance, dielectric strength and insulation needs, adhesion and reworkability behavior, operating temperature range and thermal cycling stability, outgassing and contamination risk, line speed compatibility and curing profile)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles of Companies

3M

Henkel

Dow

DuPont

Laird Performance Materials

Parker Chomerics

Momentive

Shin Etsu Chemical

Wacker Chemie

Saint Gobain

Rogers Corporation

Panasonic Industry

Fujipoly

Indium Corporation

Lord Corporation

- OEM material nomination criteria and validation checkpoints

- Battery pack engineering priorities for thermal performance and serviceability

- Manufacturing process constraints and dispense equipment compatibility

- Cost drivers across grams per vehicle and scrap rates

- Supplier scorecards for quality responsiveness and change control

- By Value, 2025–2030

- By Volume Consumption, 2025–2030

- By Battery Pack vs Power Electronics Revenue Split, 2025–2030

- By ASP and Form Factor Mix, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now