Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA farm equipment aftermarket and spare parts market reached approximately USD ~ billion based on a recent historical assessment of agricultural machinery parts shipments and replacement demand reported by the Association of Equipment Manufacturers and the U.S. Department of Agriculture. Demand is driven by the large installed base of tractors and combines exceeding ~ million units in operation across farms, along with rising equipment utilization intensity and aging machinery fleets that increase replacement cycles and maintenance expenditure.

The USA farm equipment aftermarket and spare parts market is geographically concentrated in agricultural production regions such as Iowa, Illinois, Nebraska, Kansas, and California, where mechanized farming intensity and equipment density are highest. These states dominate due to extensive row crop cultivation, high-value specialty crop operations, and large-scale commercial farms requiring continuous machinery uptime. Strong dealer networks, logistics infrastructure, and proximity to OEM distribution centers further reinforce regional dominance in aftermarket parts consumption.

Market Segmentation

By Product Type

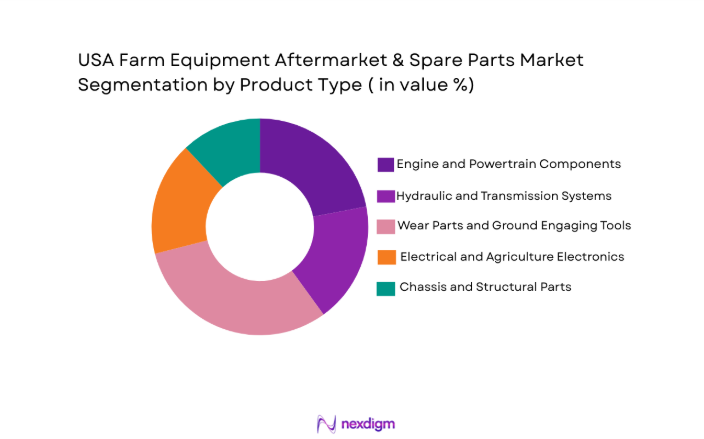

USA farm equipment aftermarket and spare parts market is segmented by product type into engine and powertrain components, hydraulic and transmission systems, wear parts and ground engaging tools, electrical and precision agriculture electronics, and chassis and structural parts. Recently, wear parts and ground engaging tools has a dominant market share due to factors such as frequent soil contact wear, seasonal replacement cycles, high equipment utilization in row crop farming, and broad compatibility across brands and machinery types, resulting in recurring purchase demand and large-volume distribution through dealers and independent retailers.

By Platform Type

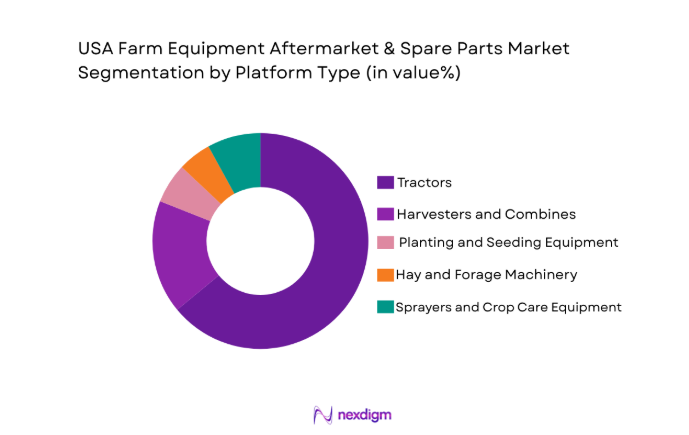

USA farm equipment aftermarket and spare parts market is segmented by platform type into tractors, harvesters and combines, planting and seeding equipment, hay and forage machinery, and sprayers and crop care equipment. Recently, tractors has a dominant market share due to the largest installed fleet across U.S. farms, year-round multi-task utilization, and extensive maintenance needs across engines, hydraulics, tires, and electronic systems, supported by dense dealer service networks and continuous replacement demand across diverse agricultural operations.

Competitive Landscape

The USA farm equipment aftermarket and spare parts market is moderately consolidated, with OEM-affiliated parts divisions of major agricultural machinery manufacturers holding strong positions through dealer networks and proprietary parts ecosystems, while independent aftermarket suppliers and remanufacturing specialists compete on price and cross-brand compatibility. Consolidation has increased through dealer mergers and integrated parts distribution systems, strengthening the influence of large OEM players on pricing, availability, and technology integration in precision agriculture components.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Distribution Network Scale |

| Deere & Company Parts Division | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial Parts & Service | 2013 | UK/Netherlands | ~ | ~ | ~ | ~ | ~ |

| AGCO Parts | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Kubota Tractor Corporation Parts | 1890 | Japan/USA | ~ | ~ | ~ | ~ | ~ |

| Caterpillar Agriculture Parts | 1925 | USA | ~ | ~ | ~ | ~ | ~ |

USA Farm Equipment Aftermarket & Spare Parts Market Analysis

Growth Drivers

Aging High Utilization Agricultural Machinery Fleet

The USA farm equipment aftermarket and spare parts market is fundamentally driven by the aging and intensively utilized agricultural machinery fleet across large-scale commercial farming regions, where tractors, combines, and planting equipment operate for extended hours across multiple seasonal cycles, significantly increasing wear and maintenance requirements and sustaining recurring replacement demand across engine, hydraulic, drivetrain, and soil-engaging components. The installed base of agricultural machinery in the United States is among the largest globally, with millions of tractors and harvesters operating across diverse crop systems and climatic zones, creating a vast addressable aftermarket ecosystem that expands annually as new equipment enters service and older units remain operational beyond original lifecycle expectations due to cost-conscious farm management strategies and high new equipment prices. Farmers increasingly extend machinery service life through refurbishment and component replacement rather than purchasing new equipment, particularly in periods of commodity price volatility and rising capital costs, which elevates expenditure on spare parts, remanufactured assemblies, and maintenance kits distributed through dealer and independent channels. High horsepower tractors and advanced combines used in large row crop farms experience significant mechanical stress due to heavy loads, long operating hours, and demanding field conditions, accelerating component degradation in transmissions, hydraulics, bearings, and ground engaging tools and requiring frequent replacement cycles that reinforce aftermarket revenue streams. Precision agriculture adoption further amplifies aftermarket demand because electronic modules, sensors, control units, and guidance systems require periodic replacement, calibration, and upgrades to maintain performance accuracy and compatibility with evolving farm management platforms. Regional concentration of mechanized agriculture in the Midwest and Plains states creates dense parts consumption clusters supported by extensive dealer and distributor logistics networks that ensure rapid parts availability and service continuity, reinforcing high aftermarket turnover rates. Seasonal farming operations necessitate minimal equipment downtime during planting and harvesting windows, compelling farmers to maintain spare inventories and proactively replace wear components before failure, which increases preventive maintenance parts consumption. Equipment sharing and contractor-based farming services also intensify machinery usage rates, shortening component life cycles and elevating replacement frequency across fleets used for custom harvesting and field operations. Environmental and soil variability across U.S. agricultural regions accelerates wear in soil-contact components such as blades, tines, and coulters, creating consistent recurring demand independent of new equipment sales cycles. These structural characteristics collectively ensure that the aftermarket and spare parts segment grows steadily alongside installed machinery base expansion and utilization intensity rather than solely relying on new equipment sales dynamics.

Expansion of Precision Agriculture and Electronic Component Replacement

The rapid integration of precision agriculture technologies into U.S. farming operations has created a structurally expanding demand segment within the farm equipment aftermarket and spare parts market centered on electronic modules, sensors, connectivity hardware, and control systems that require ongoing replacement, calibration, and upgrades throughout machinery lifecycles, transforming traditional mechanical parts demand patterns into hybrid electro-mechanical aftermarket ecosystems. Modern tractors, combines, and sprayers incorporate advanced guidance systems, GPS receivers, yield monitors, variable rate controllers, telematics units, and onboard computing platforms that are exposed to harsh agricultural operating environments including dust, vibration, temperature extremes, and moisture, leading to higher failure and replacement rates compared to purely mechanical components and generating recurring electronic aftermarket revenue streams. Precision agriculture adoption has expanded significantly across large commercial farms seeking productivity gains, input optimization, and data-driven decision-making, increasing the installed base of electronic-enabled equipment and thereby enlarging the population of components requiring periodic servicing and replacement through dealer service channels and specialized electronics distributors. Software and firmware compatibility requirements further drive hardware replacement cycles, as farmers upgrade equipment to maintain integration with evolving farm management systems, cloud platforms, and digital agronomy services, necessitating replacement of control units and communication modules even before mechanical wear-out occurs. OEMs increasingly design equipment with modular electronic architectures to enable upgrades and serviceability, which simplifies replacement but also increases frequency of aftermarket transactions for sensors, harnesses, controllers, and display units distributed through proprietary parts ecosystems. Data connectivity infrastructure expansion in rural regions has accelerated telematics deployment, expanding the installed base of connectivity hardware subject to wear and obsolescence replacement cycles. Precision planting and spraying systems rely on high-accuracy sensors and actuators whose performance degradation directly impacts crop yield outcomes, incentivizing proactive replacement and maintenance by farmers to preserve operational precision. Dealer service models have evolved to include diagnostics and electronics servicing, creating specialized aftermarket channels dedicated to electronic components and increasing revenue contribution from this segment. As autonomous and semi-autonomous agricultural equipment features gradually enter mainstream adoption, electronic component density per machine rises further, structurally increasing future aftermarket demand intensity. This transition toward electronics-intensive agricultural machinery fundamentally elevates the value and growth trajectory of the spare parts market beyond traditional mechanical wear components.

Market Challenges

Counterfeit and Low Quality Aftermarket Parts Proliferation

The USA farm equipment aftermarket and spare parts market faces a significant structural challenge from the proliferation of counterfeit, substandard, and unverified aftermarket components distributed through informal channels and online marketplaces, which undermines product reliability, erodes farmer trust, and creates safety and performance risks across agricultural machinery operations. Farmers seeking cost savings often procure lower-priced compatible parts from non-authorized distributors or online vendors without verified quality assurance, exposing equipment to premature failures, reduced performance efficiency, and potential secondary damage to high-value machinery assemblies such as engines, transmissions, and hydraulic systems. Counterfeit components frequently replicate OEM branding or packaging, making detection difficult for end users and even some distributors, which dilutes OEM brand equity and diverts legitimate aftermarket revenue while increasing warranty disputes and service liabilities. Substandard metallurgy, poor machining tolerances, and inadequate material specifications in counterfeit wear parts lead to accelerated degradation and inconsistent field performance, particularly in high-stress applications such as tillage tools and drivetrain elements, amplifying equipment downtime risks during critical farming windows. The decentralized structure of the agricultural aftermarket supply chain, involving independent distributors, retailers, and e-commerce sellers, complicates regulatory oversight and enforcement against counterfeit distribution networks. Online sales platforms have enabled cross-border importation of unverified components at scale, bypassing traditional dealer quality controls and expanding counterfeit penetration into rural markets. Farmers operating under tight cost pressures may prioritize upfront price over lifecycle reliability, inadvertently sustaining demand for low-quality parts and perpetuating market fragmentation. OEMs and authorized distributors incur additional costs in traceability systems, authentication technologies, and awareness programs to combat counterfeit infiltration and protect brand integrity. Equipment failures linked to counterfeit parts also damage farmer confidence in aftermarket components broadly, affecting legitimate suppliers and reducing willingness to adopt compatible or remanufactured alternatives. This challenge constrains market value growth potential by shifting revenue toward lower-priced components while increasing service and warranty burdens across the ecosystem.

Supply Chain Volatility in Metals and Electronic Components

The USA farm equipment aftermarket and spare parts market is significantly affected by volatility in raw material and electronic component supply chains, particularly for alloy steels, bearings, castings, and semiconductor-based electronics used in modern agricultural machinery parts, leading to cost fluctuations, lead time variability, and inventory management challenges across OEM and aftermarket distributors. Agricultural machinery spare parts manufacturing depends heavily on specialized steel grades, heat-treated components, and precision-machined assemblies whose production is sensitive to global metal supply dynamics, energy costs, and trade policies, causing unpredictable input cost changes that propagate into aftermarket pricing and availability. Electronic components such as sensors, control modules, and telematics units rely on semiconductor supply chains that have experienced disruptions due to geopolitical tensions, capacity constraints, and logistics bottlenecks, extending replacement lead times and constraining dealer inventory availability for critical electronic spare parts. Dealers and distributors must maintain extensive inventories to support time-sensitive agricultural operations, yet supply volatility complicates forecasting and stocking strategies, increasing working capital requirements and risk of stockouts during peak farming seasons. Farmers depend on rapid parts availability to avoid operational downtime during planting and harvest windows, so delayed supply of critical components directly impacts agricultural productivity and equipment utilization, amplifying the perceived risk of aftermarket reliance. OEMs may prioritize new equipment production over spare parts manufacturing during supply shortages, reducing aftermarket supply volumes and creating price escalation in replacement markets. Global sourcing dependencies for certain castings and electronic assemblies expose the aftermarket to international logistics disruptions and tariff changes, further increasing procurement complexity. Smaller independent distributors lack bargaining power and supply visibility compared to OEM networks, making them more vulnerable to shortages and price swings that erode competitiveness. Price volatility in metals and electronics also discourages long-term procurement contracts and stabilizing pricing structures in the aftermarket. These supply chain uncertainties constrain predictable growth and create operational risks across the farm equipment spare parts ecosystem.

Opportunities

Expansion of Remanufactured and Circular Economy Parts Programs

The USA farm equipment aftermarket and spare parts market has a substantial growth opportunity in the expansion of remanufactured components and circular economy programs that refurbish used engines, transmissions, hydraulics, and electronic assemblies to original performance standards, providing cost-effective and sustainable alternatives to new parts while extending machinery lifecycle and reducing environmental impact. Agricultural equipment owners increasingly seek lower-cost maintenance solutions amid high new equipment prices and income variability, making remanufactured assemblies attractive due to significant cost savings relative to new OEM components without sacrificing operational reliability. Remanufacturing processes restore worn components through disassembly, inspection, machining, replacement of wear elements, and performance testing, creating standardized products with predictable performance and warranty coverage that align with farmer maintenance expectations. Large OEMs have established remanufacturing divisions and core return programs that recover used components from dealers and farms, creating closed-loop supply chains that ensure material reuse and steady remanufactured parts supply. Circular economy initiatives align with sustainability goals in agriculture by reducing material waste, energy consumption, and carbon footprint associated with new component manufacturing, supporting adoption among environmentally conscious farming enterprises and policy-driven sustainability programs. Remanufactured parts also mitigate supply chain volatility by reducing reliance on new raw materials and global component sourcing, enhancing supply resilience in the aftermarket ecosystem. Farmers operating older machinery fleets benefit from availability of remanufactured assemblies compatible with legacy equipment models no longer supported by new OEM production lines. Dealer service networks integrate remanufactured offerings into maintenance packages, increasing service revenue and customer retention through cost-effective lifecycle solutions. Digital traceability and certification systems improve confidence in remanufactured component quality and authenticity, differentiating them from unverified aftermarket alternatives. As agricultural machinery lifecycles extend and sustainability pressures increase, remanufactured parts programs present a structurally expanding opportunity within the U.S. farm equipment aftermarket.

Digital Parts Commerce and Predictive Maintenance Platforms

The USA farm equipment aftermarket and spare parts market presents significant opportunity through digital parts commerce platforms and predictive maintenance technologies that transform traditional reactive replacement models into data-driven, anticipatory service ecosystems enabling timely parts procurement, reduced downtime, and optimized inventory management across agricultural machinery fleets. Online parts catalogs, VIN-based identification systems, and integrated dealer e-commerce portals simplify parts selection and ordering processes for farmers, reducing procurement friction and expanding direct-to-farm distribution channels beyond physical dealership networks. Predictive maintenance technologies leveraging telematics data, sensor monitoring, and equipment diagnostics enable early detection of component wear or failure risk, allowing proactive parts replacement scheduling and improving operational reliability during critical agricultural periods. Farmers increasingly adopt connected machinery platforms that transmit usage, load, and performance data, enabling analytics-driven maintenance recommendations and automated parts ordering integrated with dealer systems. Digital platforms also enable cross-brand parts compatibility identification and transparent pricing, increasing competition and expanding access to aftermarket components across regions lacking dense dealer coverage. Inventory optimization algorithms support distributors in aligning stocking levels with regional demand patterns, reducing stockouts and excess inventory costs. Remote diagnostics and digital service support reduce technician travel and downtime, enhancing aftermarket service efficiency and parts turnover. Integration of digital platforms with remanufacturing and core return logistics streamlines circular parts programs and improves asset recovery rates. As rural connectivity infrastructure improves and precision agriculture adoption deepens, digital aftermarket ecosystems are expected to reshape spare parts distribution and maintenance practices across U.S. agriculture. These platforms create scalable revenue streams for OEMs and independent distributors while enhancing farmer operational efficiency and equipment lifecycle management.

Future Outlook

The USA farm equipment aftermarket and spare parts market is expected to expand steadily over the next five years driven by the aging machinery base, increasing precision agriculture adoption, and growth in remanufactured parts programs. Digital parts commerce, predictive maintenance technologies, and dealer network integration will reshape distribution and service models. Regulatory support for right-to-repair and sustainability initiatives will further stimulate aftermarket demand. Rising equipment utilization intensity across large commercial farms will sustain recurring replacement cycles and long-term market growth.

Major Players

- Deere & Company Parts Division

- CNH Industrial Parts & Service

- AGCO Parts

- Kubota Tractor Corporation Parts

- Caterpillar Agriculture Parts

- Claas of America Parts

- Mahindra North America Parts

- Yanmar America Parts

- Buhler Industries Versatile Parts

- Great Plains Manufacturing Parts

- Kinze Manufacturing Parts

- Alamo Group Aftermarket

- Trelleborg Wheel Systems Agriculture

- Bridgestone Off Road Tire Agriculture

- SKF Agricultural Solutions

Key Target Audience

- Agricultural machinery manufacturers

- Farm equipment dealers and distributors

- Large commercial farming enterprises

- Agricultural cooperatives

- Parts remanufacturing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Agricultural equipment rental companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including installed machinery base, equipment utilization rates, replacement cycles, dealer network density, and component wear intensity were identified from agricultural equipment databases and industry sources. Demand drivers across mechanical and electronic spare parts categories were mapped to farm mechanization patterns and regional crop systems. Supply chain and distribution channel structures were defined across OEM and independent aftermarket ecosystems.

Step 2: Market Analysis and Construction

Market size and segmentation were constructed using machinery population data, parts consumption rates, and average replacement expenditure per equipment class. Product, platform, and regional segmentation structures were aligned with U.S. agricultural mechanization profiles and dealer distribution networks. Competitive positioning and value chain relationships were analyzed across OEM parts divisions, remanufacturers, and independent distributors.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on replacement cycles, parts demand intensity, and remanufacturing penetration were validated through consultations with agricultural equipment dealers, service technicians, and aftermarket distributors. Industry experts reviewed segmentation logic, technology trends, and regional demand dynamics. Feedback was incorporated to refine market drivers, challenges, and opportunity assessments.

Step 4: Research Synthesis and Final Output

Validated data and insights were synthesized into a structured market model integrating installed base growth, utilization intensity, and technology adoption trends. Forecast scenarios incorporated precision agriculture expansion, digital commerce penetration, and remanufactured parts growth. Final outputs were compiled into market narratives, segmentation tables, and competitive landscape analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Aging installed base of tractors and combines extending replacement cycles

Rising mechanization intensity and equipment utilization rates in large farms

Expansion of precision agriculture increasing electronics replacement demand

Cost optimization shift toward repair and remanufacturing over new purchase

Dealer network expansion and digital parts commerce penetration - Market Challenges

Counterfeit and low quality parts proliferation impacting trust

Supply chain volatility in metals and electronics components

Compatibility complexity across multi brand legacy equipment fleets

Skilled service technician shortages in rural regions

Pricing pressure from parallel import aftermarket suppliers - Market Opportunities

Growth in remanufactured assemblies and circular economy programs

Digital parts identification and predictive maintenance platforms

Expansion of e commerce driven direct to farm parts distribution - Trends

Increasing adoption of telematics enabled predictive parts replacement

Dealer consolidation integrating service and parts logistics

Shift toward modular replaceable assemblies in new equipment design

Rapid growth of online parts catalogs and VIN based ordering

Rising demand for precision agriculture sensors and controllers - Government Regulations & Defense Policy

Right to repair legislation affecting OEM parts access policies

Emissions compliance driving engine retrofit and parts upgrades

Trade and tariff policies influencing imported aftermarket components - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Engine & Powertrain Components

Hydraulic & Transmission Systems

Wear Parts & Ground Engaging Tools

Electrical & Precision Farming Electronics

Cabin, Chassis & Structural Parts - By Platform Type (In Value%)

Tractors

Harvesters & Combines

Planting & Seeding Equipment

Hay & Forage Machinery

Sprayers & Crop Care Equipment - By Fitment Type (In Value%)

OEM Genuine Replacement Parts

OEM Licensed Remanufactured Parts

Aftermarket Compatible Parts

Performance Upgrade Kits

Refurbished Assemblies - By EndUser Segment (In Value%)

Large Commercial Farms

Mid Sized Family Farms

Agricultural Contractors

Cooperatives & Agribusiness Enterprises

Government & Institutional Farms - By Procurement Channel (In Value%)

Authorized Dealer Networks

Independent Parts Distributors

Online Aftermarket Platforms

Local Farm Supply Retailers

Direct OEM E Commerce - By Material / Technology (in Value %)

High Strength Alloy Steel Components

Advanced Polymers & Composites

Precision Electronics & Sensors

Wear Resistant Carbide Materials

Additively Manufactured Parts

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Breadth, Distribution Reach, OEM Affiliation, Remanufacturing Capability, Digital Commerce Maturity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Deere & Company Parts Division

CNH Industrial Parts & Service

AGCO Parts

Kubota Tractor Corporation Parts

Caterpillar Agriculture Parts

Claas of America Parts

Mahindra North America Parts

Yanmar America Parts

Buhler Industries Versatile Parts

Great Plains Manufacturing Parts

Kinze Manufacturing Parts

Alamo Group Aftermarket

Trelleborg Wheel Systems Agriculture

Bridgestone Off Road Tire Agriculture

SKF Agricultural Solutions

- Large farms prioritize uptime and OEM guaranteed parts availability

- Contractors demand rapid serviceable modular components across brands

- Family farms rely on local distributors and cost-effective aftermarket parts

- Cooperatives centralize procurement to optimize lifecycle equipment costs

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now