Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA farm equipment powertrain components engine drivetrain and transmission market is valued at approximately USD ~ billion based on a recent historical assessment, driven by replacement cycles in high horsepower tractors, expanding precision agriculture adoption, and sustained farm mechanization investments. Powertrain demand is closely linked to OEM production volumes and aftermarket refurbishment activity, with drivetrain and transmission systems accounting for a substantial share of component value due to engineering complexity and durability requirements (Association of Equipment Manufacturers).

Dominant regions within the USA farm equipment powertrain components engine drivetrain and transmission market include Midwest manufacturing clusters such as Illinois, Iowa, and Wisconsin, supported by dense agricultural equipment OEM ecosystems and supplier networks. These states host major assembly and component plants, advanced machining capabilities, and agricultural testing infrastructure, while proximity to large-scale grain and corn production regions ensures concentrated equipment deployment and service demand, reinforcing regional leadership in powertrain production and integration.

Market Segmentation

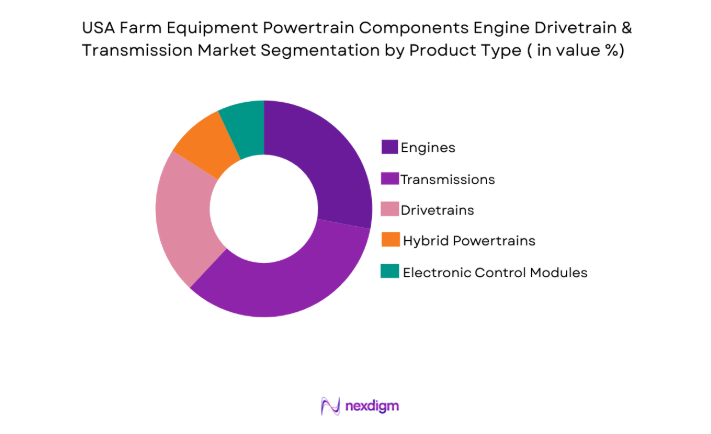

By Product Type

USA farm equipment powertrain components engine drivetrain and transmission market is segmented by product type into engines, transmissions, drivetrains, hybrid powertrains, and electronic control modules. Recently, transmissions have a dominant market share due to factors such as high value per unit, technological complexity, integration with precision farming systems, and demand for continuously variable and power shift configurations across high horsepower tractors and harvesters.

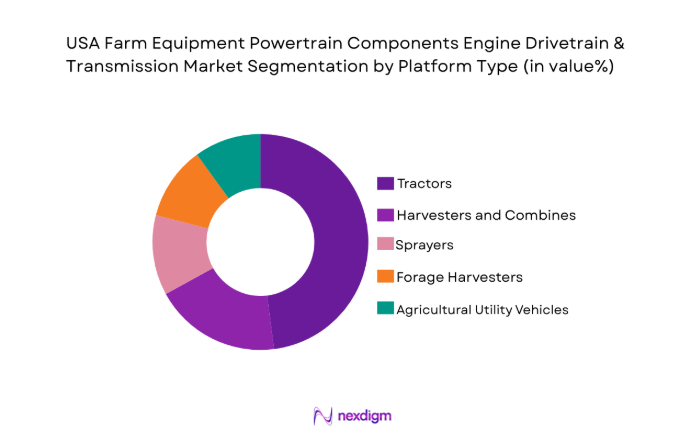

By Platform Type

USA farm equipment powertrain components engine drivetrain and transmission market is segmented by platform type into tractors, combine harvesters, sprayers, forage harvesters, and agricultural utility vehicles. Recently, tractors have a dominant market share due to factors such as largest installed base, broad horsepower range coverage, year-round utilization, and continuous replacement and upgrade cycles in row crop and mixed farming operations.

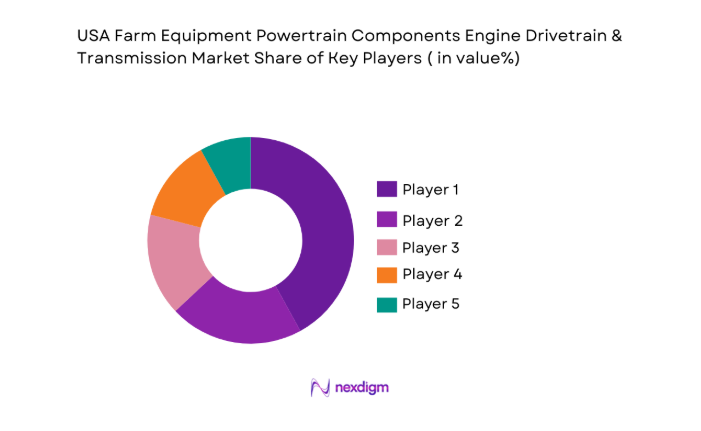

Competitive Landscape

The USA farm equipment powertrain components engine drivetrain and transmission market exhibits moderate consolidation with a mix of integrated agricultural OEMs and specialized drivetrain and transmission suppliers. Major players maintain competitive advantage through vertically integrated manufacturing, remanufacturing programs, and long-term OEM supply contracts, while global powertrain technology firms expand presence via electrified and hybrid drivetrain development.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Agricultural OEM Integration |

| Deere & Company | 1837 | USA | ~ | ~ | ~ | ~ | ~ |

| CNH Industrial | 2013 | UK/Netherlands | ~ | ~ | ~ | ~ | ~ |

| AGCO Corporation | 1990 | USA | ~ | ~ | ~ | ~ | ~ |

| Cummins | 1919 | USA | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

USA Farm Equipment Powertrain Components Engine Drivetrain & Transmission Market Analysis

Growth Drivers

High Horsepower Tractor Replacement and Upgrade Cycle

The USA farm equipment powertrain components engine drivetrain and transmission market is strongly influenced by replacement demand from aging high horsepower tractor fleets used in large scale grain and row crop agriculture, where machines often exceed optimal service life due to intensive seasonal utilization and increasing mechanical stress loads. Farmers prioritize upgrading to newer tractors equipped with advanced transmissions such as continuously variable or power shift systems that improve fuel efficiency, traction control, and compatibility with precision agriculture implements, thereby increasing demand for modern drivetrain assemblies and integrated powertrain modules. Replacement cycles accelerate when maintenance costs and downtime risks rise, especially during planting and harvesting seasons when equipment reliability directly affects crop yield outcomes and operational profitability for commercial farms. OEMs and suppliers benefit from both new equipment sales and aftermarket replacement of engines, transmissions, and driveline components, creating dual revenue streams across equipment lifecycle phases. Powertrain complexity has increased significantly with electronic control integration and emission compliant engine architectures, raising average component value and replacement cost, which further expands market size in monetary terms even when unit volumes remain stable. Larger farm operations in the USA continue consolidating land holdings and adopting higher horsepower equipment to improve productivity per labor unit, driving sustained demand for heavy duty powertrain systems capable of operating wide implements and precision agriculture technologies. The shift toward automation assisted steering and implement control systems also requires transmissions capable of smooth variable speed operation and torque management, reinforcing preference for advanced drivetrain platforms over mechanical gear systems. Financing availability and favorable commodity income cycles support capital expenditure on equipment upgrades, indirectly stimulating demand for associated powertrain components. Remanufacturing programs offered by OEMs and component suppliers encourage refurbishment of engines and transmissions rather than complete machine replacement, maintaining strong aftermarket powertrain turnover and parts demand. Consequently, the ongoing high horsepower tractor replacement and upgrade cycle remains a foundational growth driver for the USA farm equipment powertrain components engine drivetrain and transmission market.

Precision Agriculture Integration Requiring Advanced Powertrain Control Systems

The USA farm equipment powertrain components engine drivetrain and transmission market is expanding due to increasing integration of precision agriculture technologies that require electronically controlled engines, transmissions, and drivetrains capable of synchronized operation with GPS guidance, variable rate application systems, and automated implement control platforms. Modern agricultural operations rely on precise speed regulation and torque delivery to maintain optimal seeding density, spraying accuracy, and harvesting efficiency, necessitating advanced transmission architectures such as continuously variable systems and electronically managed power shift gearboxes. Powertrain components now incorporate sensors, control units, and telematics connectivity to communicate with farm management systems and machine automation software, increasing component complexity and value while expanding replacement and upgrade opportunities. Farmers adopting precision agriculture expect improved fuel efficiency and reduced soil compaction through optimized torque distribution and traction control, which can only be achieved through sophisticated drivetrain design and electronic integration. OEMs are therefore embedding digital control layers within engines and transmissions, transforming powertrain assemblies from purely mechanical systems into integrated electromechanical platforms with software functionality. This transition stimulates demand for new generation powertrain modules and retrofitting of older equipment to enable compatibility with precision agriculture tools and data systems. As regulatory pressures on emissions and fuel consumption increase, electronically controlled engines and transmissions help optimize combustion and load management, aligning powertrain technology development with both environmental and productivity goals. Component suppliers invest heavily in mechatronics and control software capabilities to meet OEM requirements, reinforcing technological innovation cycles within the market. Precision agriculture adoption across large US farms continues to expand operational reliance on advanced powertrain performance, sustaining long term demand for integrated engine, drivetrain, and transmission systems. Therefore, precision agriculture integration requiring advanced powertrain control systems represents a major growth driver for the USA farm equipment powertrain components engine drivetrain and transmission market.

Market Challenges

Emission Compliance and Engine Redesign Cost Burden

The USA farm equipment powertrain components engine drivetrain and transmission market faces significant challenges from stringent emission regulations governing off road diesel engines, requiring continuous redesign of combustion systems, exhaust aftertreatment modules, and electronic engine controls to comply with EPA Tier 4 Final and subsequent standards. Compliance engineering increases research and development costs for engine manufacturers and OEMs, while also raising production expenses due to complex components such as diesel particulate filters, selective catalytic reduction systems, and electronic monitoring devices integrated into powertrain architectures. These cost increases elevate the price of new engines and tractors, which can dampen equipment replacement demand among smaller farms and contractors sensitive to capital expenditure fluctuations. Suppliers must also manage regulatory certification processes and testing requirements that extend product development timelines and increase administrative overhead. Emission compliant engines often require specialized maintenance and higher quality fuel or urea based additives, increasing operating complexity and lifecycle cost for end users, which may discourage rapid adoption or replacement cycles. Integrating emission control systems into compact agricultural equipment platforms creates packaging and thermal management challenges that complicate drivetrain and transmission design integration. Regulatory uncertainty regarding future emission thresholds further complicates long term product planning and investment decisions for powertrain manufacturers. Remanufacturing older engines to meet emission standards can be technically difficult and economically unviable, limiting aftermarket opportunities in some equipment segments. The cumulative effect of compliance engineering cost burden and market sensitivity to equipment pricing creates structural pressure on profitability and innovation investment within the USA farm equipment powertrain components engine drivetrain and transmission market. Consequently, emission compliance and engine redesign cost burden remains a persistent market challenge.

Agricultural Income Volatility Affecting Equipment Investment Cycles

The USA farm equipment powertrain components engine drivetrain and transmission market is vulnerable to fluctuations in agricultural commodity prices and farm income levels, which directly influence farmers’ willingness and ability to invest in new machinery or major powertrain replacements. Crop prices for corn, soybeans, and wheat are subject to global supply demand dynamics, weather conditions, and trade policies, creating cyclical income patterns that translate into irregular equipment purchasing behavior. During periods of lower commodity prices, farmers often defer tractor upgrades or major drivetrain overhauls, extending equipment service life beyond optimal mechanical thresholds and reducing short term demand for powertrain components. Equipment financing availability and interest rate changes further amplify this sensitivity, as higher borrowing costs discourage capital intensive machinery purchases. Large commercial farms may maintain investment capacity through scale advantages, but mid size and family farms represent a substantial installed base whose deferred maintenance decisions significantly affect aftermarket powertrain demand. OEM production volumes respond quickly to order cycles, leading to manufacturing variability that cascades into component supplier production planning and inventory management challenges. Drivetrain and transmission components often represent high cost replacement items, making them particularly sensitive to farm income uncertainty compared with smaller consumable parts. Dealers and distributors must balance inventory risk against unpredictable demand timing driven by agricultural profitability conditions. Long term modernization trends support eventual replacement demand, yet short to medium term volatility creates uneven revenue streams across the market. Therefore, agricultural income volatility affecting equipment investment cycles constitutes a major structural challenge for the USA farm equipment powertrain components engine drivetrain and transmission market.

Opportunities

Hybrid and Electrified Agricultural Powertrain Development for Efficiency and Sustainability

The USA farm equipment powertrain components engine drivetrain and transmission market has significant opportunity in the development and deployment of hybrid and electrified powertrain systems that improve fuel efficiency, reduce emissions, and enable advanced torque control in agricultural machinery across diverse operating conditions. Electrified drivetrains can deliver instant torque and precise speed modulation beneficial for tasks such as planting, spraying, and low speed harvesting operations, enhancing productivity and operational accuracy in precision agriculture contexts. Hybrid architectures combining diesel engines with electric assist modules allow downsizing of combustion engines while maintaining power output, reducing fuel consumption and operating cost over equipment lifecycle. Government incentives for low emission off road equipment and sustainability initiatives among large farming enterprises encourage adoption of electrified machinery platforms, creating demand for new powertrain component categories including electric motors, power electronics, and battery integrated transmissions. Electrification also enables regenerative braking and energy recovery in transport operations between fields, improving overall machine efficiency. OEMs investing in electric tractor prototypes and hybrid harvesters require specialized drivetrain integration expertise, opening opportunities for component suppliers to expand product portfolios beyond traditional mechanical systems. Aftermarket retrofit kits enabling partial electrification of existing tractors present additional revenue streams, particularly in specialty crop and controlled environment agriculture segments. Electrified powertrains support quieter operation and reduced vibration, beneficial for livestock and urban fringe farming environments, expanding equipment application scenarios. As agricultural sustainability targets and fuel cost pressures intensify, electrified and hybrid powertrain development represents a transformative opportunity for the USA farm equipment powertrain components engine drivetrain and transmission market.

Remanufacturing and Lifecycle Extension Services for Agricultural Powertrain Systems

The USA farm equipment powertrain components engine drivetrain and transmission market presents substantial opportunity in structured remanufacturing and lifecycle extension programs that refurbish engines, transmissions, and drivetrain assemblies to near new performance levels at lower cost than complete replacement. Agricultural machinery often operates for decades, and powertrain components represent the highest value elements within equipment, making refurbishment economically attractive for farmers seeking reliability without full machine purchase. OEM certified remanufacturing programs ensure component quality, warranty coverage, and compatibility with existing equipment, encouraging adoption across commercial farming operations. Remanufactured powertrain systems reduce material consumption and manufacturing energy requirements, aligning with sustainability goals and circular economy practices increasingly emphasized in agricultural policy frameworks. Dealers benefit from recurring service revenue and parts sales associated with refurbishment cycles, strengthening aftermarket ecosystem stability. Technological upgrades can be incorporated during remanufacturing, such as improved seals, bearings, or electronic controls, enhancing performance beyond original specifications and extending service life. Supply chain constraints and long lead times for new equipment during peak demand periods further increase attractiveness of remanufactured powertrains as faster deployment alternatives. Fleet operators and agricultural contractors managing multiple machines gain cost predictability and reduced downtime through planned refurbishment schedules. As farm operators seek to balance capital expenditure with operational continuity, remanufacturing and lifecycle extension services offer scalable growth potential across both OEM and independent supplier channels. Thus, remanufacturing and lifecycle extension services for agricultural powertrain systems constitute a major opportunity in the USA farm equipment powertrain components engine drivetrain and transmission market.

Future Outlook

The USA farm equipment powertrain components engine drivetrain and transmission market is expected to expand steadily over the next five years supported by continued mechanization upgrades, precision agriculture integration, and emergence of hybrid and electrified drivetrains. OEM innovation in continuously variable transmissions and electronic control systems will raise component value and functionality. Emission and sustainability policies will accelerate powertrain modernization. Strong aftermarket refurbishment demand and large installed machinery base will sustain long term component consumption.

Major Players

- Deere & Company

- CNH Industrial

- AGCO Corporation

- Cummins

- Dana Incorporated

- ZF Friedrichshafen

- BorgWarner

- Schaeffler

- Eaton

- Kubota Engine America

- Yanmar America

- Carraro Group

- Twin Disc

- Allison Transmission

- Caterpillar

Key Target Audience

- Agricultural machinery OEMs

- Power train component manufacturers

- Farm equipment distributors

- Large commercial farming enterprises

- Agricultural contractors

- Government and regulatory bodies

- Investments and venture capitalist firms

- Agricultural cooperatives

Research Methodology

Step 1: Identification of Key Variables

Key variables such as tractor horsepower distribution, installed agricultural machinery base, powertrain replacement cycles, OEM production volumes, and component value hierarchy were identified. Regulatory standards, precision agriculture adoption levels, and electrification trends were also mapped to define demand drivers influencing the USA farm equipment powertrain components engine drivetrain and transmission market.

Step 2: Market Analysis and Construction

Primary and secondary data from agricultural equipment associations, OEM financials, and machinery fleet statistics were integrated to construct market sizing models. Component penetration across equipment categories and lifecycle stages were analyzed to derive segment level value distribution within the USA farm equipment powertrain components engine drivetrain and transmission market.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including drivetrain engineers, OEM procurement specialists, and agricultural machinery dealers were consulted to validate assumptions regarding replacement cycles, technology adoption, and pricing structure. Feedback refined segmentation shares and growth dynamics shaping the USA farm equipment powertrain components engine drivetrain and transmission market.

Step 4: Research Synthesis and Final Output

Validated datasets and qualitative insights were synthesized into structured market estimates, segmentation, competitive analysis, and forecasts. Consistency checks across equipment volumes, component values, and regional deployment ensured analytical integrity of the USA farm equipment powertrain components engine drivetrain and transmission market assessment.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Mechanization upgrades in high horsepower tractor segment

Replacement demand from aging agricultural machinery fleet

Adoption of precision agriculture compatible powertrain systems - Market Challenges

Emission compliance cost pressures on diesel engine manufacturing

Volatility in agricultural commodity income affecting equipment spending

Complexity in integrating electrified powertrain components - Market Opportunities

Expansion of hybrid and electric assist drivetrains in specialty crops equipment

Remanufacturing and lifecycle extension services for powertrain assemblies

Digital monitoring enabled smart transmission systems - Trends

Shift toward continuously variable and hydrostatic transmissions in tractors

Integration of electronic control and telematics in powertrain modules

Lightweight alloy materials adoption in drivetrain components - Government Regulations & Defense Policy

EPA Tier 4 Final emission standards enforcement for agricultural engines

State level clean off road equipment incentive programs

Federal farm equipment modernization and sustainability grants - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Diesel Agricultural Engines

Mechanical Drivetrain Assemblies

Hydrostatic Transmission Systems

Power Shift Transmission Systems

Electric Hybrid Powertrain Modules - By Platform Type (In Value%)

Tractors

Combine Harvesters

Self Propelled Sprayers

Forage Harvesters

Agricultural Utility Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Powertrain Systems

Aftermarket Replacement Powertrain Kits

Remanufactured Engine Assemblies

Transmission Retrofit Packages

Hybrid Conversion Kits - By EndUser Segment (In Value%)

Large Commercial Farms

Mid Size Family Farms

Agricultural Contractors

Agricultural Cooperatives

Government and Research Farms - By Procurement Channel (In Value%)

OEM Direct Supply Agreements

Authorized Dealer Networks

Independent Aftermarket Distributors

Online Agricultural Parts Platforms

Fleet Procurement Contracts - By Material / Technology (in Value %)

Cast Iron Engine Blocks

Aluminum Alloy Transmission Housings

High Strength Steel Gearsets

Electronic Control Unit Integrated Powertrains

Electrified Power Assist Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Engine Power Range, Transmission Type Portfolio, Electrification Capability, OEM Partnerships, Aftermarket Network Strength, Manufacturing Localization, R&D Investment, Remanufacturing Capability, Pricing Tier)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Deere & Company

CNH Industrial

AGCO Corporation

Caterpillar

Cummins

Dana Incorporated

ZF Friedrichshafen

BorgWarner

Schaeffler

Eaton

Kubota Engine America

Yanmar America

Carraro Group

Twin Disc

Allison Transmission

- Large farms prioritizing high durability and fuel-efficient powertrain systems

- Contractors demanding modular and quick replace drivetrain assemblies

- Cooperatives focusing on remanufactured and cost optimized transmissions

- Research farms piloting hybrid and electrified agricultural powertrains

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now