Download PDF

Download PDFMarket Overview

The USA Flexible Packaging Market was valued at USD ~ Billion in 2024 and is anticipated to expand at a CAGR of ~% during 2026–2035. The market is primarily driven by sustained growth in food and beverage, pharmaceutical, and e-commerce packaging demand, alongside significant capacity investment from both established and private equity-backed converters. According to Towards Packaging, the U.S. flexible packaging market was valued at USD ~ billion in 2025 and is expected to reach approximately USD ~ billion by 2035, growing at a CAGR of 4.30%. According to the Flexible Packaging Association (FPA), flexible packaging accounts for roughly 20% of the total USD 213.4 billion U.S. packaging market, making it the second-largest packaging segment behind corrugated, with the industry directly employing more than 85,000 people and exporting nearly 9% of total U.S. flexible packaging shipments.

Market Segmentation

By Material

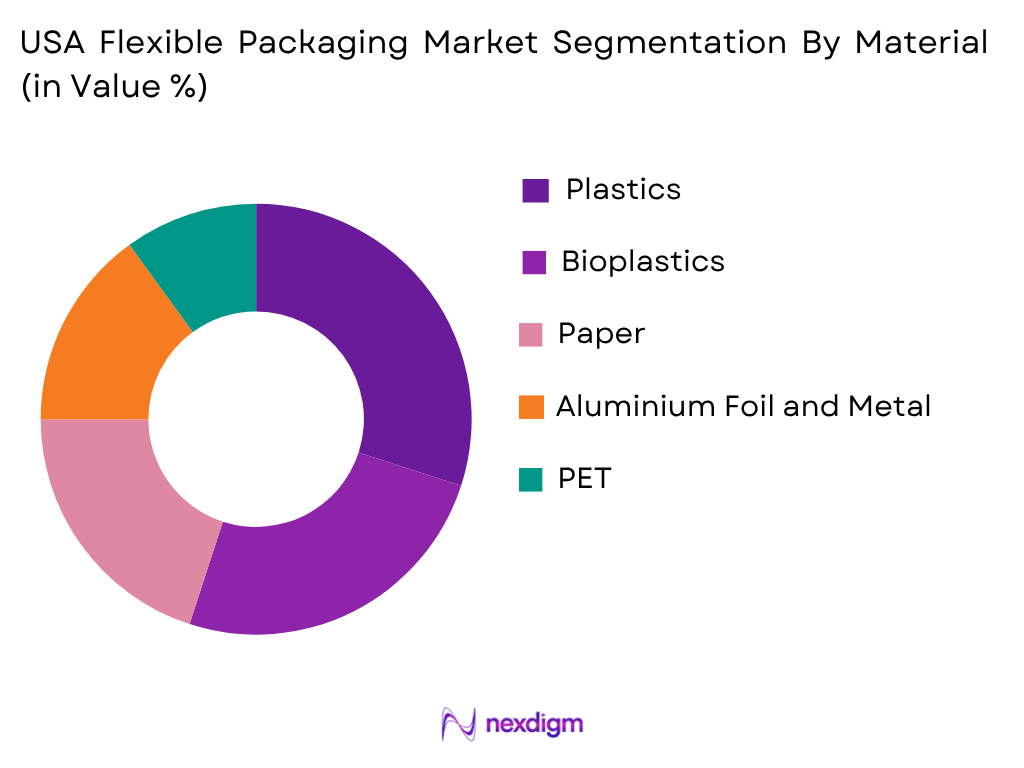

Among these, Plastics dominate the USA Flexible Packaging Market, accounting for more than 69% of revenue share in 2024, according to Mordor Intelligence, owing to the cost-effectiveness of plastics compared to glass and metal, alongside inherent properties such as excellent moisture and gas barrier resistance, light weight, puncture resistance, and transparency. Plastic pouches and bags remain convenient for consumers due to their ease of use and resealable features, reinforcing plastics’ continued dominance despite growing sustainability pressure. Bioplastics represent the fastest-growing material segment, with a projected CAGR of 5.4% from 2024 to 2030 according to Grand View Research, driven by increasing demand for sustainable and environmentally friendly packaging solutions made from renewable resources such as plant starches or cellulose. Films, paper, and resins remain the largest converter input costs, representing nearly 75% of material purchases, according to the FPA’s 2025 State of the U.S. Flexible Packaging Industry report.

By Application

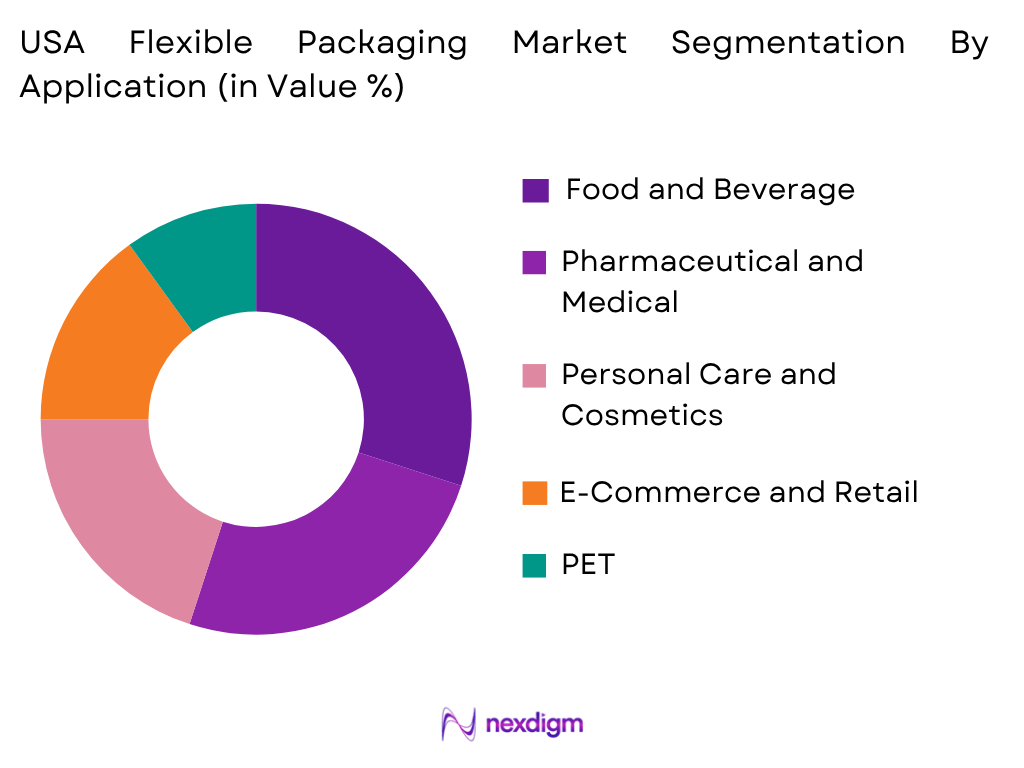

The Food and Beverage segment dominates the USA Flexible Packaging Market, accounting for approximately 44.5% of flexible packaging demand, according to the Flexible Packaging Association’s 2025 State of the Industry presentation, with shelf-stable goods, salty snacks, confectionery, and produce representing the largest uses within the food sector. The largest market for flexible packaging overall is food, spanning retail and institutional channels, accounting for about 50% of total shipments, according to FPA facts and figures. The Pharmaceutical and Medical segment, representing around 17% of demand, is projected to witness the fastest CAGR during the forecast period, driven by increased use of flexible packaging in medical contexts, with composite flexible packaging optimising application and sales while requiring high-precision, high-quality adhesive manufacturing processes. Demand for healthcare and pharmaceutical pouches continues to be driven by over-the-counter medications, wellness products, and diagnostics requiring sterile, easy-to-carry packaging formats.

Competitive Landscape

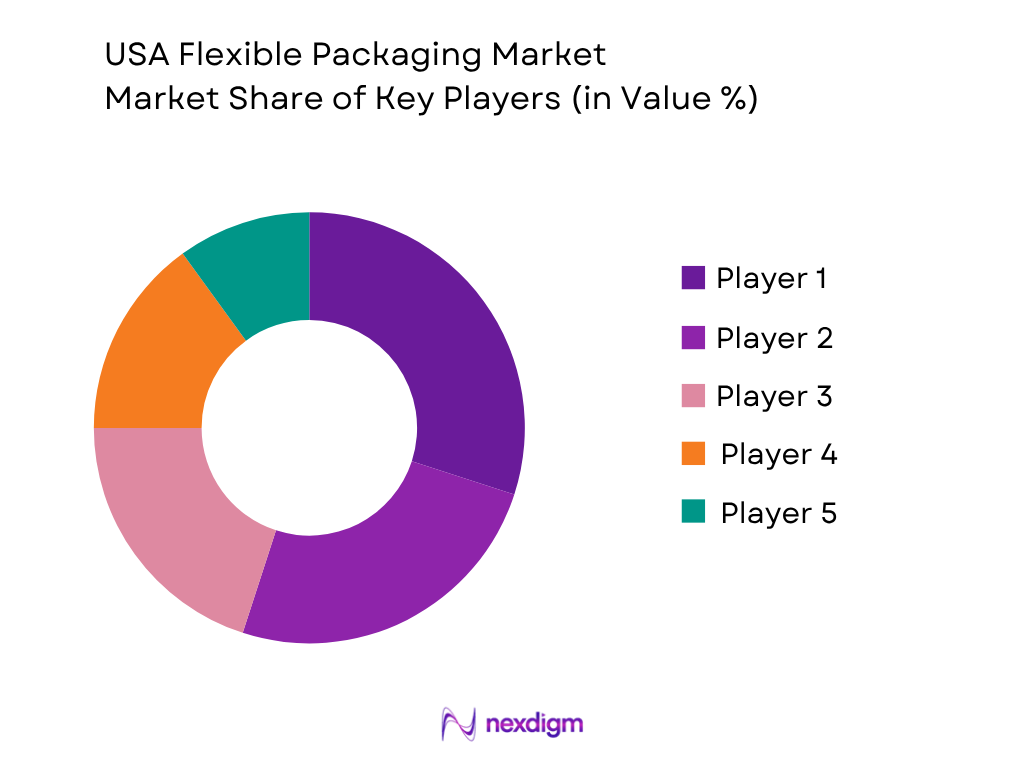

The USA Flexible Packaging Market is highly competitive and fragmented, with many players of varying sizes holding relatively small individual market shares, according to Grand View Research. The market’s competitive structure was fundamentally reshaped by Amcor’s USD 8.43 billion acquisition of Berry Global, which closed on April 30, 2025, combining two of the industry’s largest players into a single entity with an extensive North American manufacturing footprint. Family-owned and privately held converters continue to play a significant role in the market: American Packaging Corporation, founded in 1902 and based in Columbus, Wisconsin, operates six Centers of Excellence across the United States, while Printpack Inc., founded in 1956 in Atlanta, Georgia, generates approximately USD 1.1 billion in revenue through manufacturing facilities across the United States, Mexico, China, and India. Private equity-backed ProAmpac, founded in 2015 and headquartered in Cincinnati, Ohio, has grown rapidly through acquisitions, including its September 2025 purchase of PAC Worldwide Corporation and a December 2025 agreement with Transcontinental for its Canadian packaging business, reflecting the sustained pace of M&A-driven consolidation across the industry.

| Company | Establishment Year | Headquarters | Primary Product Portfolio | Flexible Packaging Portfolio

|

Manufacturing Presence | Major End-Use Industries | Key Strategic Focus | Certifications & Compliance |

| American Packaging Corporation | 1902 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Printpack Inc. | 1956 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| ProAmpac LLC | 2015 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Amcor PLC | 1896 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Sealed Air Corporation | 1960 | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

USA Flexible Packaging Market Analysis

Growth Drivers

Sustained Growth in Food, Beverage, and Pharmaceutical Packaging Demand

The USA flexible packaging market is experiencing sustained growth due to steady demand from the food and beverage, healthcare, and personal care industries. Food applications remain the dominant driver of flexible packaging demand, accounting for approximately 44.5% of total demand, according to the Flexible Packaging Association’s 2025 State of the Industry presentation, with shelf-stable goods, salty snacks, confectionery, and produce representing the largest uses within the food sector. Financially, converters saw a rebound in profitability in 2024, with profit before taxes for flexible packaging converters rising above the average for all U.S. manufacturing, and FPA members projecting 4.8% industry growth in 2025, bringing the value-added segment of the market to an estimated USD 44.6 billion. Major brand investment continues to reinforce this trend: Mars confirmed USD 2 billion in U.S. manufacturing investments through 2026, including a USD 240 million Utah confectionery site capable of producing nearly 1 billion units annually with a packaging brief centred on recycle-ready film.

Rising E-Commerce Penetration and Consumer Demand for Convenient Formats

Growing e-commerce penetration and consumer preference for convenient, resealable packaging formats are significant drivers of the USA flexible packaging market. As of January 2025, there were 288.45 million online shoppers in the United States, according to the B2B eCommerce Association, with flexible packaging increasingly used in compact, protective, and brand-enhancing formats for direct-to-consumer shipping and subscription boxes. Consumers increasingly prefer resealable pouches, stand-up bags, and lightweight films that enhance shelf life and reduce transportation costs, while features such as zip locks, spouts, and tear notches continue to boost the attractiveness of flexible formats for busy consumers. Hotpack’s May 2025 opening of a USD 100 million, 70,000-square-foot plant in New Jersey to supply custom food-service packaging, creating 200 jobs, illustrates the continued capacity investment being driven by this sustained shift toward convenience-oriented and food-service flexible packaging formats.

Market Challenges

Fragmented State-by-State Extended Producer Responsibility Compliance

The USA Flexible Packaging Market faces a fragmented and increasingly complex regulatory landscape, as seven U.S. states currently have Extended Producer Responsibility (EPR) laws in effect or approaching implementation: California, Colorado, Maine, Maryland, Minnesota, Oregon, and Washington, according to the Flexible Packaging Association. Oregon’s EPR programme is fully in effect, with Colorado’s beginning in January 2026, and Dan Felton, FPA president and CEO, expects several additional states to pass similar legislation within the next few years. California’s SB 54 mandates packaging-waste-reduction contributions that can exceed USD 0.12 per pound for non-recyclable formats, incentivising rapid design shifts toward mono-polyethylene and coated paper structures, according to Mordor Intelligence. This state-by-state patchwork creates significant compliance complexity for manufacturers operating across multiple markets, requiring converters to navigate varying fee structures, reporting requirements, and recyclability definitions simultaneously.

Multi-Layer Film Recycling Infrastructure Gaps

Flexible packaging remains a hard-to-recycle product in the current state of American recycling infrastructure, constrained by limited curbside access, nascent store drop-off networks, and immature end markets, according to FPA president and CEO Dan Felton. The industry must demonstrate proof of concept and scalable solutions for collection, sorting, and reuse, as recycling is not meaningful unless collected material is actually processed into new products. While 25 states now explicitly allow advanced, molecular, or chemical recycling technologies, classified as manufacturing rather than waste management, other states including Maryland, New York, Oregon, Rhode Island, and Vermont are weighing restrictions that would prevent advanced recycling from counting toward recyclability or recycled-content targets, creating regulatory uncertainty for converters investing in these technologies to help scale film recovery and enable recycled content in food-contact packaging.

Market Opportunities

Mono-Material Recyclable Films and Advanced Recycling Technology

Rising brand owner sustainability commitments present a substantial opportunity for flexible packaging converters investing in mono-material recyclable film technology and advanced recycling infrastructure. The Flexible Packaging Association is collaborating with the newly formed Flexible Film Recycling Alliance (FFRA), launched in 2024, alongside the increasingly prominent PRO Circular Action Alliance (CAA), to expand recovery infrastructure and develop viable markets for reclaimed material, with FFRA completing its first year of initiatives focused on data collection and consumer education. Berry Global’s collaboration with Printpack to introduce the Preserve PE PCR recyclable pouch, which is How2Recycle pre-qualified and contains 30% FDA-compliant post-consumer recycled resin content, illustrates the type of cross-industry partnership increasingly needed as consumer packaged goods companies embed post-consumer resin targets directly into long-term procurement contracts.

Continued Consolidation Through Mergers and Acquisitions

The USA Flexible Packaging Market’s fragmented competitive structure continues to drive significant merger and acquisition activity, presenting opportunities for both strategic acquirers and acquisition targets. Following Amcor’s USD 8.43 billion acquisition of Berry Global, which closed in April 2025, subsequent 2025 transactions included Crestview Partners’ March 2025 acquisition of Smyth Companies from Novacap, Constantia Flexibles’ June 2025 acquisition of a majority stake in Aluflexpack AG to expand pharmaceutical-lidding and high-barrier pouch capacity, and Astara Capital Partners’ October 2025 continuation vehicle combining Garlock Flexibles and C-P Flexible Packaging. ProAmpac’s own acquisition of PAC Worldwide Corporation in September 2025 and its subsequent agreement with Transcontinental for its Canadian packaging business further illustrate how mid-sized, private equity-backed converters continue to pursue scale and geographic expansion, positioning well-capitalised acquirers to capture growing demand while providing attractive exit opportunities for family-owned and regional converters.

Future Outlook

The USA Flexible Packaging Market is expected to witness steady expansion over the forecast period, supported by sustained demand growth across food and beverage, pharmaceutical, and e-commerce applications, continued investment from both large multinational converters and private equity-backed mid-sized players, and accelerating adoption of mono-material recyclable and post-consumer recycled content packaging. Continued state-level EPR law expansion, growing investment in advanced recycling technology, and ongoing industry collaboration through initiatives such as the Flexible Film Recycling Alliance will further shape the market’s sustainability trajectory. The market is also likely to benefit from continued consolidation following the Amcor-Berry Global merger and subsequent M&A activity, even as the industry continues to navigate a fragmented and evolving state-by-state regulatory landscape, multi-layer film recycling infrastructure gaps, and raw material price volatility tied to petroleum-based polymer costs.

Major Players

- Amcor plc

- Sealed Air Corporation

- Mondi plc

- Constantia Flexibles Group GmbH

- Transcontinental Inc.

- Sonoco Products Company

- Huhtamaki Oyj

- Novolex Holdings, LLC

- Winpak Ltd.

- Coveris Holdings S.A.

- American Packaging Corporation

- Printpack Inc.

- ProAmpac LLC

- Hood Packaging Corporation

- Smyth Companies, LLC

Key Target Audience

- Flexible Packaging Manufacturers and Converters

- Food & Beverage Processing Companies

- Pharmaceutical and Medical Device Manufacturers

- Personal Care and Cosmetics Manufacturers

- Retailers and E-Commerce Fulfilment Operators

- Investment and Private Equity Firms

- Government and Regulatory Bodies (U.S. Food and Drug Administration (FDA), State Extended Producer Responsibility (EPR) Programmes, Flexible Packaging Association (FPA))

- Packaging Machinery and Raw Material Suppliers

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying the complete ecosystem of the USA Flexible Packaging Market, including raw material and resin suppliers, flexible packaging converters, printing and lamination technology providers, food and beverage manufacturers, retailers, and regulatory authorities. Extensive secondary research is conducted using company annual reports, government publications, trade associations, customs statistics, industry journals, and proprietary databases to determine the variables influencing market demand, pricing, production, consumption, and technological developments.

Step 2: Market Analysis and Construction

Historical market information is collected and analysed to estimate market size, production volumes, import-export activity, application-wise demand, and pricing trends. A combination of top-down and bottom-up approaches is used to estimate market revenues and validate segment-level performance. Consumption patterns across food and beverage, pharmaceutical, personal care, and industrial applications are evaluated to establish an accurate representation of the industry.

Step 3: Hypothesis Validation and Expert Consultation

The preliminary findings are validated through Computer-Assisted Telephone Interviews (CATIs) and structured discussions with flexible packaging manufacturers, procurement managers, distributors, brand owners, regulatory experts, and senior executives operating within the U.S. food, beverage, and consumer goods industries. These interviews help verify market assumptions, competitive developments, technology adoption trends, pricing dynamics, and future investment opportunities while refining the overall market estimates.

Step 4: Research Synthesis and Final Output

The final stage integrates insights obtained from primary interviews with quantitative information collected through secondary sources. Data triangulation techniques are applied to reconcile differences between supply-side and demand-side estimates, ensuring robust market forecasting. The report is then reviewed through multiple quality assurance checkpoints to deliver a comprehensive analysis covering market size, segmentation, competitive landscape, future outlook, and strategic recommendations for industry stakeholders.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Market Sizing Approach, Top-Down Analysis, Bottom-Up Analysis, Demand-Side Assessment, Supply-Side Assessment, Primary Industry Interviews, Secondary Research Validation, Data Triangulation, Forecasting Framework, Limitations and Future Conclusions)

- Definition and Scope

- Market Evolution and Industry Genesis

- Timeline of Major Industry Developments

- Flexible Packaging Industry Value Chain Analysis

- Supply Chain Analysis

- Growth Drivers (Growth of Food and Beverage Packaging Demand, Rising E-Commerce and Direct-to-Consumer Shipping, Growth of Pharmaceutical and Medical Packaging, Consumer Demand for Convenient Resealable Formats, Brand Owner Sustainability Commitments, Multinational Manufacturing Capacity Investment)

- Market Challenges (Fragmented State-by-State EPR Compliance Landscape, Multi-Layer Film Recycling Infrastructure Gaps, Raw Material Price Volatility, Limited Curbside Recycling Access, Competition from Rigid Packaging Alternatives, Import Competition from Asian Converters)

- Market Opportunities (Mono-Material Recyclable Film Development, Advanced and Molecular Recycling Technology, Post-Consumer Recycled Content Integration, Fibre-Based Flexible Packaging Innovation, Smart Labelling and QR Code Integration, Consolidation Through Mergers and Acquisitions)

- Market Trends (Amcor-Berry Global Consolidation, Growth of Private Equity-Backed Converters, State-Level EPR Law Expansion, Rise of Recycle-Ready Film Design, AI-Assisted Manufacturing Optimisation, Flexible Film Recycling Alliance Initiatives)

- Government Regulations (State Extended Producer Responsibility (EPR) Laws, California SB 54, FDA Food Contact Packaging Regulations, State-Level Recycled Content Mandates, Advanced Recycling Classification Standards, Import Compliance)

- Import and Export Analysis (Export Shipment Volume, Major Export Destinations (Colombia, South Korea, Trinidad and Tobago), Major Import Sources (Vietnam, India, China), HS Code Analysis, Trade Balance)

- Raw Material Availability Analysis (Domestic Polyethylene and Polypropylene Resin Supply, Paperboard and Kraft Paper Supply, Aluminium Foil Supply, Bioplastic Feedstock Availability, Adhesive and Coating Supply)

- Technology Landscape (Cast and Blown Film Extrusion, Multi-Layer Lamination, Advanced (Molecular) Recycling Technology, Digital and Flexographic Printing, AI-Assisted Production Monitoring)

- Sustainability Assessment (Mono-Material Recyclable Design, Post-Consumer Recycled Content Adoption, Compostable Film Development, Store Drop-Off Recycling Programmes, Flexible Film Recycling Alliance Initiatives)

- PESTLE Analysis

- SWOT Analysis

- Porter’s Five Forces Analysis

- Stakeholder Ecosystem

- Competition Ecosystem

- By Market Value (2020-2025)

- By Volume Consumption (2020-2025)

- By Average Selling Price (2020-2025)

- By Material (In Value %)

Plastics

Paper

Aluminium Foil and Metal

Bioplastics - By Product Type (In Value %)

Pouches

Bags

Films and Wraps

Rollstock

Labels - By Application (In Value %)

Food and Beverage

Pharmaceutical and Medical

Personal Care and Cosmetics

Household and Industrial

E-Commerce and Retail - By End User (In Value %)

Food and Beverage Manufacturers

Pharmaceutical and Healthcare Manufacturers

Personal Care and Cosmetics Manufacturers

Retailers and E-Commerce Fulfilment

Industrial and Agricultural Users - By Region (In Value %)

Midwest

South

West

Northeast

- Market Share of Major Players (By Value, Volume, Material Type, Application Industry, Product Category)

- Cross Comparison Parameters (Product Portfolio Breadth, Recyclable Material Capability, Printing Technology Range, Application Technical Support Capability, Manufacturing Capacity, Regulatory Compliance & Certifications, Customer Base Across Industries, Innovation & New Product Launch Frequency)

- SWOT Analysis of Major Players

- Pricing Analysis by Product Category and Material

- Production Capacity Analysis

- Manufacturing Footprint Analysis

- Distribution Network Analysis

- Innovation Benchmarking

- Detailed Profiles of Major Companies

Amcor plc

Sealed Air Corporation

Mondi plc

Constantia Flexibles Group GmbH

Transcontinental Inc.

Sonoco Products Company

Huhtamaki Oyj

Novolex Holdings, LLC

Winpak Ltd.

Coveris Holdings S.A.

American Packaging Corporation

Printpack Inc.

ProAmpac LLC

Hood Packaging Corporation

Smyth Companies, LLC

- Consumption Pattern Analysis (Industrial Usage, Batch Size, Product Category Penetration, Seasonal Demand, Reformulation Activity)

- Purchasing Criteria (Barrier Performance, Recyclability, Cost Efficiency, Print Quality, Supply Consistency, Shelf Life Extension)

- Procurement and Supplier Selection Analysis

- Sustainable Packaging Adoption Assessment

- Premium vs Conventional Packaging Demand

- Product Attribute Preference Analysis (Barrier Properties, Seal Integrity, Recyclability, Print Definition, Lightweighting, Ease of Opening)

- Consumer Sustainability Influence on Packaging Choice

- Pain Point Analysis

- Decision-Making Process

- By Market Value (2026-2035)

- By Volume Consumption (2026-2035)

- By Average Selling Price (2026-2035)

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now