Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA Freight Aggregator Market reached approximately USD ~ billion, supported by rapid digitization of freight brokerage and increasing demand for real-time capacity matching across fragmented carrier networks. The market is driven by e-commerce fulfillment growth exceeding USD ~ trillion in merchandise value and national freight expenditures surpassing USD ~ trillion, which amplify the need for digital load aggregation, automated pricing, and multimodal coordination platforms among shippers and logistics intermediaries.

Major logistics hubs such as Chicago, Dallas–Fort Worth, Los Angeles, Atlanta, and Memphis dominate freight aggregation activity due to dense intermodal infrastructure, large distribution clusters, and concentration of third-party logistics providers. These regions handle freight volumes exceeding USD ~ billion annually across trucking and intermodal corridors, fostering adoption of digital freight platforms to manage high shipment frequency, tight delivery windows, and complex carrier ecosystems across retail, manufacturing, and consumer goods supply chains.

Market Segmentation

By Service Type:

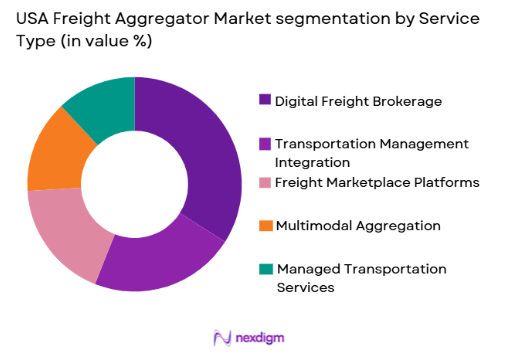

USA Freight Aggregator Market is segmented by service type into digital freight brokerage, transportation management integration, freight marketplace platforms, multimodal aggregation, and managed transportation services. Recently, digital freight brokerage has a dominant market share due to factors such as real-time pricing capabilities, strong carrier networks, and high shipper demand for automated tendering. Growth in e-commerce shipments and volatile spot rates has intensified reliance on digital brokerage platforms that provide instant capacity matching and dynamic pricing across nationwide trucking lanes, reinforcing their leading position within the aggregation ecosystem.

By End User:

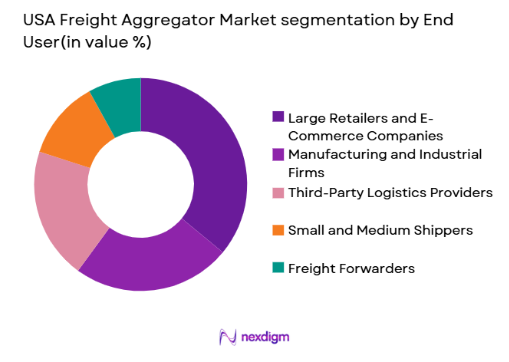

USA Freight Aggregator Market is segmented by end user into large retailers and e-commerce companies, manufacturing and industrial firms, third-party logistics providers, small and medium shippers, and freight forwarders. Recently, large retailers and e-commerce companies hold a dominant market share due to factors such as high shipment volumes, omnichannel fulfillment requirements, and demand for nationwide carrier access. Their complex distribution networks require automated load matching, real-time visibility, and scalable capacity procurement, making freight aggregators essential for managing peak seasonal demand and tight delivery commitments across national logistics corridors.

Competitive Landscape

The USA Freight Aggregator Market exhibits moderate consolidation, with a mix of digital-native freight platforms and established logistics technology providers shaping competition. Large players leverage extensive carrier networks, advanced pricing algorithms, and nationwide coverage to secure enterprise shippers, while mid-sized aggregators differentiate through specialized verticals or multimodal capabilities. Strategic partnerships with transportation management systems and visibility platforms enhance ecosystem integration, reinforcing the influence of leading firms across digital brokerage and freight marketplace segments.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Carrier Network Size |

| Uber Freight | 2017 | USA | ~ | ~ | ~ | ~ | ~ |

| C.H. Robinson | 1905 | USA | ~ | ~ | ~ | ~ | ~ |

| RXO | 2022 | USA | ~ | ~ | ~ | ~ | ~ |

| Echo Global Logistics | 2005 | USA | ~ | ~ | ~ | ~ | ~ |

| Loadsmart | 2014 | USA | ~ | ~ | ~ | ~ | ~ |

USA Freight Aggregator Market Analysis

Growth Drivers

Expansion of E-Commerce Fulfillment and Omnichannel Distribution Networks:

The rapid expansion of e-commerce fulfillment and omnichannel retail distribution networks has fundamentally reshaped freight procurement requirements across the United States logistics sector. Retailers and manufacturers increasingly operate distributed inventory models involving regional fulfillment centers, micro-warehouses, and direct-to-consumer shipping nodes that generate high-frequency shipment flows across diverse lanes. Freight aggregators enable automated load matching and real-time carrier selection, which is critical for meeting accelerated delivery expectations across nationwide markets. The growth of online retail exceeding USD 1.1 trillion in merchandise value intensifies demand for flexible truckload and less-than-truckload capacity procurement. Aggregation platforms reduce manual brokerage interactions and provide dynamic pricing aligned with fluctuating demand patterns across seasons and regions. Large shippers require continuous access to carrier capacity across fragmented trucking markets, where over 90 percent of carriers operate small fleets. Digital aggregation technology integrates pricing, booking, and tracking into unified workflows, enabling logistics teams to manage shipment complexity at scale. The shift toward same-day and next-day delivery models further amplifies reliance on real-time freight procurement systems. As fulfillment networks continue decentralizing, freight aggregators become essential infrastructure for coordinating capacity across dispersed distribution nodes.

Carrier Network Fragmentation and Need for Unified Capacity Access

: The structural fragmentation of the United States trucking industry creates persistent inefficiencies in matching freight demand with available carrier capacity across regional and national routes. More than one million trucking companies operate domestically, with the majority managing fewer than ten trucks, resulting in limited visibility for shippers seeking consistent coverage across lanes. Freight aggregators address this fragmentation by consolidating carrier availability, pricing data, and compliance credentials into centralized digital platforms. Unified capacity access enables shippers and logistics providers to source transportation across thousands of carriers without maintaining individual relationships. Aggregators also improve asset utilization by reducing empty miles through broader load distribution and dynamic network balancing. Fragmented carrier markets historically required extensive manual brokerage coordination, leading to delays and pricing inconsistencies. Digital aggregation systems automate tendering and booking processes, increasing efficiency and transparency across freight procurement workflows. Growing shipment variability driven by seasonal demand and regional disruptions further strengthens reliance on aggregated capacity networks. Shippers prioritize scalable access to nationwide carriers capable of supporting volatile demand across trucking and intermodal modes. The consolidation of carrier data and booking capabilities within freight aggregators therefore represents a foundational driver of market growth.

Market Challenges

Integration Complexity with Legacy Transportation Management and ERP Systems:

Freight aggregators must integrate with diverse legacy transportation management and enterprise resource planning systems widely used by shippers and logistics providers across the United States. Many large enterprises operate customized or outdated logistics software architectures lacking standardized data interfaces, complicating digital platform connectivity. Integration projects often require extensive configuration, data mapping, and workflow redesign before aggregation tools can function effectively within existing operations. Disparate data formats across EDI, API, and manual systems create inconsistencies in shipment visibility and booking automation processes. Enterprises may also resist replacing established logistics workflows due to operational risk and transition costs associated with technology change. Limited interoperability slows adoption among industrial and manufacturing sectors where legacy systems remain entrenched. Aggregators must invest heavily in middleware, connectors, and onboarding support to bridge technological gaps between platforms and shipper systems. Implementation timelines can extend across months, delaying return on investment and reducing adoption momentum. Integration challenges also hinder real-time pricing and visibility accuracy, undermining platform value propositions. As logistics digitalization accelerates, overcoming legacy system constraints remains a significant barrier to widespread freight aggregator deployment.

Volatility of Freight Rates and Exposure to Spot Market Fluctuations:

Freight aggregators operate within transportation markets characterized by substantial rate volatility driven by fuel costs, seasonal demand, economic cycles, and capacity imbalances. Spot trucking rates in the United States can fluctuate sharply across months and regions, affecting pricing stability for both shippers and carriers using aggregation platforms. Shippers relying heavily on spot-based digital procurement may face unpredictable transportation costs during capacity shortages or peak seasons. Aggregators must balance dynamic pricing responsiveness with rate transparency and predictability expectations from enterprise customers. Rapid rate swings also complicate algorithmic pricing models that depend on historical lane data and demand forecasting. Carrier participation on platforms may vary with market conditions, affecting capacity availability and service reliability. Economic downturns or freight recessions can reduce shipment volumes, directly impacting transaction-based revenue models of aggregators. Conversely, capacity shortages during demand surges can strain carrier networks and booking success rates. Maintaining stable service quality across volatile freight cycles requires sophisticated analytics and diversified capacity sourcing strategies. Persistent exposure to freight rate volatility therefore represents a structural challenge affecting profitability and adoption stability in the market.

Opportunities

Expansion of Multimodal Digital Aggregation Across Rail and Intermodal Networks: The

integration of rail and intermodal transportation services into digital freight aggregation platforms presents a major opportunity for market expansion across the United States logistics ecosystem. Intermodal freight volumes exceeding USD 120 billion create substantial demand for unified digital booking across trucking and rail corridors. Aggregators that extend beyond truckload brokerage into multimodal coordination can provide end-to-end capacity procurement for long-haul shipments. Rail-linked aggregation enables cost optimization and emissions reduction, aligning with shipper sustainability goals and network efficiency strategies. Intermodal services also support capacity diversification during trucking shortages, enhancing platform resilience and shipper reliability. Digital coordination of drayage, rail linehaul, and final delivery stages increases visibility across complex shipment journeys. Historically fragmented rail booking processes are increasingly digitized, allowing integration into unified aggregation marketplaces. Large retailers and manufacturers seek multimodal optimization to manage rising transportation costs across long-distance lanes. Aggregators capable of orchestrating multimodal networks can differentiate through expanded service scope and higher-value logistics solutions. The convergence of trucking and rail aggregation therefore represents a significant growth opportunity within the evolving freight technology landscape.

Embedded Freight Procurement Within Enterprise and E-Commerce Platforms:

Embedding freight aggregation capabilities directly within enterprise resource planning, warehouse management, and e-commerce order management systems represents a transformative opportunity for market expansion. Shippers increasingly prefer freight booking integrated seamlessly into operational workflows rather than accessed through standalone platforms. Embedded aggregation allows automatic load creation and carrier selection at the point of order processing, reducing manual logistics intervention. E-commerce marketplaces generating billions in shipment value require integrated logistics execution capabilities to support merchants and fulfillment partners. Software providers and aggregators are forming partnerships to integrate freight procurement APIs into enterprise applications and digital commerce platforms. Embedded solutions enhance user adoption by aligning transportation procurement with core business processes such as inventory allocation and order routing. Integration at transaction level also improves data accuracy and shipment planning efficiency across supply chains. Aggregators gain access to high transaction volumes through platform ecosystems rather than individual shipper onboarding. This model supports scalable growth and recurring usage across distributed user bases. The embedding of freight aggregation into enterprise and commerce systems therefore offers a strategic pathway for expanding market penetration and platform utilization.

Future Outlook

The USA Freight Aggregator Market is expected to expand steadily over the next five years as digital procurement becomes standard across freight sourcing workflows. Advancements in AI-driven pricing, multimodal integration, and real-time visibility will strengthen platform capabilities and adoption. Regulatory focus on supply chain transparency and emissions reporting will encourage digital coordination tools. Growth in e-commerce fulfillment and distributed manufacturing logistics will further increase demand for scalable aggregation platforms nationwide.

Major Players

- Uber Freight

- C.H. Robinson

- RXO

- Echo Global Logistics

- Loadsmart

- Transfix

- DAT Freight and Analytics

- Truckstop

- project44

- FourKites

- MercuryGate

- Descartes Systems Group

- Trimble Transportation

- Blue Yonder

- J.B. Hunt 360

Key Target Audience

- Retail and E-commerce Companies

- Manufacturing and Industrial Firms

- Third-Party Logistics Providers

- Freight Brokerages

- Transportation Carriers

- Government and Regulatory Bodies

- Investments and Venture Capitalist Firms

- Supply Chain Technology Providers

Research Methodology

Step 1: Identification of Key Variables

Market variables such as freight volumes, digital brokerage penetration, carrier fragmentation, and logistics technology adoption were identified. Data sources included transportation statistics, company disclosures, and logistics infrastructure indicators to define market boundaries.

Step 2: Market Analysis and Construction

The market size was constructed using freight expenditure benchmarks, digital brokerage revenue data, and shipment transaction volumes. Segmentation frameworks were developed across service type and end user to reflect aggregation adoption patterns.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through industry reports, logistics operator insights, and technology provider perspectives. Expert review ensured consistency with freight procurement trends, carrier network structures, and digital platform adoption levels.

Step 4: Research Synthesis and Final Output

Validated data and qualitative insights were synthesized into structured market analysis. Competitive positioning, segmentation shares, and growth dynamics were aligned to produce a comprehensive view of the USA Freight Aggregator Market.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

E-Commerce Fulfillment Scale Increasing Time-Definite Shipping Demand

Shipper Demand for Real-Time Visibility and Exception Management

Carrier Fragmentation Driving Need for Unified Capacity Access

Digital Procurement Adoption in Transportation Sourcing Workflows

Pressure to Reduce Empty Miles and Improve Network Utilization - Market Challenges

Carrier Compliance and Onboarding Friction Across Networks

Data Quality Gaps Across EDI, APIs, and Telemetry Streams

Price Volatility and Spot Market Exposure for Shippers

Interoperability Constraints with Legacy TMS and ERP Systems

Cybersecurity Risks Across Multi-Party Data Sharing - Market Opportunities

Embedded Freight Booking Inside Shipper and Marketplace Workflows

Expansion of Aggregation for Intermodal and Rail-Linked Services

Sustainability Reporting and Carbon Accounting as a Bundled Service - Trends

Rise of Automated Tendering and Dynamic Load Matching

Greater Use of Predictive ETA and Disruption Forecasting

Growth of Drop Trailer and Power-Only Network Coordination

Convergence of Brokerage, TMS, and Visibility into Unified Platforms

Expansion of Digital Payments and Freight Finance Features - Government Regulations & Defense Policy

FMCSA Compliance Digitization for Safety, Insurance, and Credentialing

Data Privacy and Cybersecurity Requirements for Supply Chain Platforms

Port, Border, and Infrastructure Modernization Policies Affecting Freight Flows - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Digital Freight Brokerage Platforms

Transportation Management Systems Integrations

Freight Marketplace and Bidding Engines

Carrier Connectivity and Capacity Aggregation Networks

Managed Transportation and Control Tower Platforms - By Platform Type (In Value%)

Web-Based Platforms

Mobile-First Platforms

API-Driven Embedded Logistics Platforms

Enterprise SaaS Platforms

Multi-Modal Visibility Platforms - By Fitment Type (In Value%)

Standalone Freight Aggregator Platforms

TMS-Integrated Aggregator Modules

ERP-Integrated Logistics Extensions

E-Commerce Platform Plug-Ins

3PL and 4PL Integrated Aggregation Suites - By EndUser Segment (In Value%)

Large Retail and E-Commerce Shippers

Manufacturing and Industrial Shippers

3PLs and Freight Forwarders

SME Shippers and Private Fleets

Brokerages and Logistics Service Providers - By Procurement Channel (In Value%)

Direct Enterprise Contracting

Platform Subscriptions and Seat Licensing

Transaction-Based Spot Market Booking

Channel Partners and System Integrators

Marketplace Onboarding via Carrier Portals - By Material / Technology (in Value %)

Cloud-Native Microservices Architecture

Real-Time Visibility and Telematics Data Layers

AI-Based Pricing and Capacity Matching

API and EDI Connectivity Tooling

Cybersecurity and Compliance Automation

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Service Coverage Footprint, Modal Coverage Mix, Shipment Size Focus, Pricing and Monetization Model, API and EDI Connectivity Depth, Carrier Network Density, Value-Added Service Breadth, Compliance and Credentialing Capabilities, Industry Vertical Focus, Customer Segment Focus)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Uber Freight

C.H. Robinson

TQL

Echo Global Logistics

RXO

Blue Yonder

Descartes Systems Group

Trimble Transportation

project44

FourKites

Transfix

Loadsmart

DAT Freight and Analytics

Truckstop

MercuryGate

- Retail and e-commerce shippers prioritize speed-to-booking and peak surge capacity access

- Manufacturers focus on multimodal planning, routing guide compliance, and cost control

- 3PLs and forwarders emphasize carrier network depth and interoperability with shipper systems

- SMEs value simplified onboarding, transparent pricing, and managed support options

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now