Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA Gearboxes market is valued at USD ~ billion, supported by data from the U.S. Census Bureau’s Annual Survey of Manufactures and industry revenue disclosures from leading gearbox manufacturers. The market is primarily driven by sustained investments in industrial automation, renewable energy installations, automotive production, and infrastructure development. Growth in wind turbine deployment and advanced manufacturing systems continues to elevate demand for high-performance mechanical power transmission systems across multiple industrial sectors.

Major manufacturing hubs such as Texas, Ohio, Michigan, Illinois, and California dominate the USA Gearboxes market due to strong automotive, energy, aerospace, and heavy machinery industries. These states benefit from advanced industrial infrastructure, skilled labor availability, and established supply chain ecosystems. Proximity to automotive OEMs, wind energy farms, and industrial equipment manufacturers strengthens regional demand, while federal infrastructure funding and reshoring initiatives further reinforce domestic production and gearbox consumption.

Market Segmentation

By Product Type

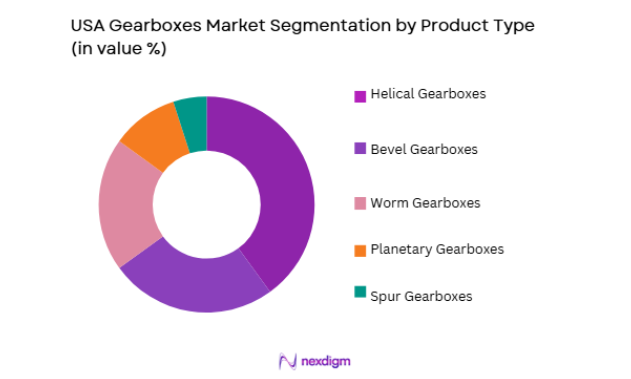

USA Gearboxes market is segmented by product type into helical gearboxes, bevel gearboxes, worm gearboxes, planetary gearboxes, and spur gearboxes. Recently, helical gearboxes have a dominant market share due to factors such as superior load capacity, higher efficiency, quieter operation, and widespread application across manufacturing, automotive assembly lines, and heavy machinery sectors. Their ability to handle high torque transmission with minimal vibration makes them ideal for industrial automation systems and conveyor applications. Strong OEM preference, established domestic manufacturing capabilities, and compatibility with modern electric motor systems further reinforce their leadership position across the USA industrial ecosystem.

By End-Use Industry

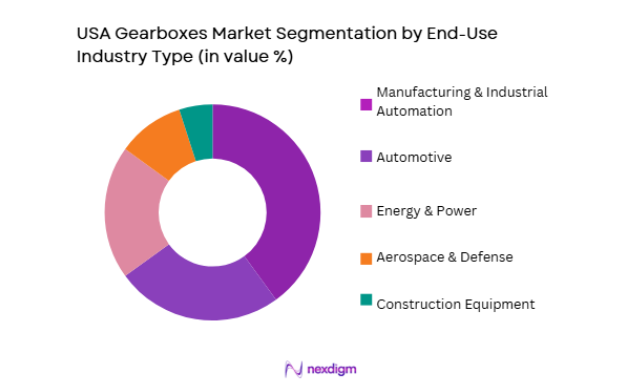

USA Gearboxes market is segmented by end-use industry into automotive, energy and power, manufacturing and industrial automation, aerospace and defense, and construction equipment. Recently, manufacturing and industrial automation has a dominant market share due to strong adoption of robotics, smart factories, and advanced material handling systems across the United States. Increased capital expenditure in automation upgrades, growth in e-commerce warehousing facilities, and reshoring of production facilities significantly elevate gearbox integration into conveyor systems, CNC machines, and robotic arms. Continuous modernization initiatives and government-backed infrastructure expansion programs further sustain strong demand from this segment.

Competitive Landscape

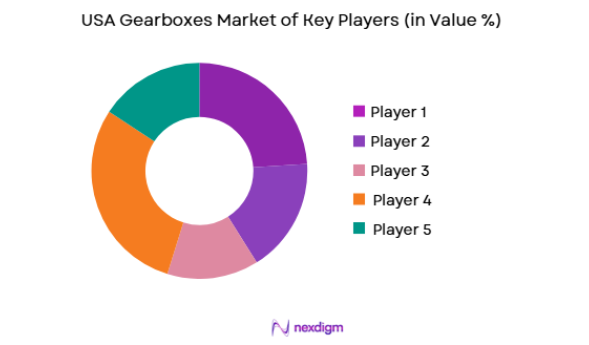

The USA Gearboxes market is moderately consolidated, with established multinational corporations and strong domestic manufacturers controlling significant production capacity and distribution networks. Leading players focus on advanced gear design, energy efficiency, and customized industrial solutions. Strategic acquisitions, technology partnerships, and investments in smart gearbox monitoring systems influence competitive intensity, while regional manufacturing presence ensures proximity to automotive and renewable energy customers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Footprint |

| Timken Company | 1899 | USA | ~ | ~ | ~ | ~ | ~ |

| Regal Rexnord | 1955 | USA | ~ | ~ | ~ | ~ | ~ |

| Dodge Industrial | 1878 | USA | ~ | ~ | ~ | ~ | ~ |

| SEW-Eurodrive | 1931 | Germany | ~ | ~ | ~ | ~ | ~ |

| Bonfiglioli USA | 1956 | Italy | ~ | ~ | ~ | ~ | ~ |

USA Gearboxes Market Analysis

Growth Drivers

Expansion of Renewable Energy and Industrial Automation Demand

The accelerating deployment of wind energy farms and automated production systems across the United States is significantly increasing demand for high performance gearboxes in turbines, robotics, and material handling systems. Growing installation of wind turbines requires durable planetary and helical gear systems capable of handling variable loads and continuous operation under demanding environmental conditions. Industrial automation investments driven by reshoring strategies and smart manufacturing initiatives further expand gearbox integration in robotics, conveyor networks, and CNC machinery. Federal infrastructure funding programs are strengthening domestic manufacturing capacity and stimulating equipment modernization across multiple sectors. Rising adoption of electric vehicles and advanced assembly technologies in automotive production facilities increases demand for precision gear reduction systems that ensure efficiency and torque stability. The expansion of warehouse automation and e commerce logistics networks supports continuous installation of gear driven conveyor and packaging equipment throughout distribution centers. Technological improvements in gear materials, lubrication systems, and predictive maintenance sensors enhance operational lifespan and reduce downtime, making advanced gearboxes more attractive to industrial buyers. Increased capital expenditure by energy utilities and manufacturing enterprises reinforces long term procurement contracts for gearbox manufacturers, thereby sustaining steady revenue generation. Continuous modernization of legacy industrial plants also drives replacement demand for upgraded, energy efficient gear systems across established manufacturing regions. These interconnected industrial transformations collectively sustain robust demand momentum within the USA Gearboxes market.

Reshoring of Manufacturing and Infrastructure Modernization Initiatives

Strong policy emphasis on domestic manufacturing resilience and supply chain localization is stimulating capital investment in heavy industrial equipment and mechanical power transmission systems throughout the United States. Incentives supporting semiconductor fabrication plants, electric vehicle battery factories, and advanced materials production facilities create extensive requirements for high torque industrial gear drives. Public infrastructure modernization programs covering transportation networks, water systems, and energy grids further increase demand for construction equipment and mechanical drives utilizing specialized gearboxes. Expansion of oil and gas operations, alongside modernization of refineries and petrochemical plants, requires rugged gearbox solutions capable of continuous operation in high stress environments. Defense production programs and aerospace manufacturing growth stimulate precision gearbox integration into aircraft assembly lines and specialized equipment. Urban development projects and large scale commercial construction contribute to sustained equipment utilization, reinforcing replacement cycles for industrial gear systems. Adoption of automation in small and medium manufacturing enterprises broadens the customer base for compact and modular gearbox solutions. Technological integration of condition monitoring and digital diagnostics enhances reliability expectations and encourages upgrading from legacy systems. Increasing emphasis on energy efficiency standards promotes selection of advanced gear designs with reduced friction losses and optimized load distribution. Collectively, these structural investments strengthen long term growth prospects for the USA Gearboxes market by expanding industrial capacity and reinforcing domestic equipment procurement.

Market Challenges

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuating prices of alloy steel, cast iron, and specialty metals significantly affect production costs for gearbox manufacturers operating within the United States. Dependence on both domestic and imported raw materials exposes companies to geopolitical uncertainties, tariff adjustments, and transportation bottlenecks that complicate procurement planning. Rising energy costs increase manufacturing overhead, particularly for heat treatment and precision machining processes essential for gear durability. Supply chain disruptions linked to global shipping constraints and port congestion can delay component deliveries and extend production lead times. Small and mid sized manufacturers face margin pressure when unable to pass cost increases directly to customers operating under fixed contracts. Inventory management becomes complex during periods of demand unpredictability, resulting in either excess stock or fulfillment delays. Increased compliance requirements and quality assurance standards add operational expenses that compound raw material cost volatility. Competitive pricing pressure from international suppliers further constrains profitability within domestic markets. Currency fluctuations may also impact imported component pricing and complicate budgeting for multinational firms. These cumulative cost pressures create significant operational uncertainty for participants in the USA Gearboxes market.

Technological Substitution and Electrification Trends Reducing Mechanical Complexity

Rapid adoption of direct drive systems and advanced electric motor technologies presents structural challenges for traditional gearbox demand in selected applications. Certain wind turbine models and electric vehicle architectures increasingly explore gearless configurations that minimize mechanical transmission components. Continuous innovation in high torque electric motors reduces dependency on multi stage gear reduction in light industrial applications. Compact integrated motor drive solutions offer lower maintenance requirements, which may attract cost sensitive industrial buyers. Manufacturers must invest heavily in research and development to remain competitive against emerging drivetrain technologies. Transition toward lightweight materials and alternative motion control systems can limit conventional gearbox usage in specific sectors. Increasing customer expectations for digital integration require embedding sensors and smart monitoring capabilities, raising product development expenses. Smaller manufacturers may struggle to finance technological upgrades necessary to maintain relevance in evolving industrial ecosystems. Environmental regulations promoting energy efficiency intensify pressure to optimize mechanical transmission losses. These evolving technological dynamics introduce structural adaptation challenges within the USA Gearboxes market.

Opportunities

Integration of Smart Gearboxes with Predictive Maintenance Technologies

Advancements in sensor technology and industrial Internet of Things platforms create significant opportunities for gearbox manufacturers to develop intelligent systems capable of real time performance monitoring. Embedding vibration sensors, temperature trackers, and load measurement devices enhances operational transparency for industrial operators. Predictive maintenance capabilities reduce unplanned downtime and extend equipment lifespan, delivering measurable cost savings to end users. Industrial facilities increasingly prioritize data driven asset management strategies, creating demand for digitally connected gearbox solutions. Integration with cloud based analytics platforms enables remote diagnostics and centralized performance oversight across multiple facilities. Service based revenue models built around maintenance contracts and performance optimization expand profitability beyond initial equipment sales. Collaboration with automation software providers strengthens product differentiation and technological leadership. Increasing adoption of Industry 4.0 frameworks across American manufacturing plants accelerates readiness for smart mechanical components. Enhanced reliability expectations in energy and infrastructure projects reinforce preference for intelligent gearbox systems. These trends collectively position digital integration as a high value growth pathway within the USA Gearboxes market.

Expansion of Renewable Energy Infrastructure and Grid Modernization Projects

Accelerated investment in wind power installations and grid modernization programs offers substantial growth avenues for advanced gearbox applications. Large scale wind turbines require high durability planetary gear systems capable of handling variable rotational loads under demanding environmental conditions. Federal and state level renewable energy incentives stimulate project development across multiple regions, increasing procurement volumes for turbine components. Modernization of electrical grids and energy storage facilities supports installation of mechanical systems reliant on efficient torque transmission. Replacement of aging wind turbine components generates consistent aftermarket demand for refurbishment and gearbox upgrades. Offshore wind expansion initiatives introduce requirements for corrosion resistant and high reliability gear systems engineered for marine conditions. Increasing corporate sustainability commitments encourage utilities and industrial players to invest in renewable energy assets. Manufacturing of renewable energy equipment domestically further stimulates gearbox demand within turbine assembly plants. Continuous improvements in material science and lubrication technologies enhance gearbox lifespan in renewable applications. These infrastructure developments create sustained opportunity within the USA Gearboxes market.

Future Outlook

Over the next five years, the USA Gearboxes market is expected to experience stable expansion driven by renewable energy growth, industrial automation upgrades, and infrastructure modernization. Technological innovation in smart gear systems and predictive maintenance solutions will reshape competitive differentiation. Regulatory support for domestic manufacturing and energy efficiency standards will reinforce procurement activity. Demand from wind energy, electric vehicle production, and advanced manufacturing facilities will remain central to market momentum.

Major Players

- Timken Company

- Regal Rexnord

- Dodge Industrial

- SEW-Eurodrive

- Bonfiglioli USA

- Siemens AG

- ABB Ltd

- Sumitomo Drive Technologies

- Nord Drivesystems

- Rexnord Corporation

- Dana Incorporated

- Gleason Corporation

- David Brown Santasalo

- Boston Gear

- Emerson Electric Co.

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive OEMs

- Renewable energy developers

- Industrial automation integrators

- Construction equipment manufacturers

- Aerospace and defense contractors

- Oil and gas operators

Research Methodology

Step 1: Identification of Key Variables

Key variables such as production volume, industrial demand indicators, raw material pricing, renewable energy capacity additions, and manufacturing output were identified. Secondary data from government databases and company financial reports were consolidated. Market boundaries and segmentation logic were clearly defined.

Step 2: Market Analysis and Construction

Quantitative analysis was conducted using industry revenue disclosures, trade statistics, and manufacturing shipment data. Segment level modeling was performed to estimate product and end use distribution. Data triangulation ensured accuracy across multiple verified sources.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, supply chain managers, and equipment manufacturers were consulted to validate demand assumptions. Feedback was incorporated to refine segment dominance and technology trends. Cross verification strengthened reliability of projections.

Step 4: Research Synthesis and Final Output

All validated findings were synthesized into structured insights covering market size, segmentation, competition, and outlook. Analytical consistency checks were performed. Final documentation was prepared following standardized reporting protocols.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of industrial automation and robotics adoption

Rising demand for renewable energy driven gearbox systems

Growth in heavy machinery and construction activities - Market Challenges

Volatility in raw material prices including steel and alloys

High maintenance costs and downtime risks

Intense competition from low cost imports - Market Opportunities

Increasing electrification of vehicles requiring precision gear systems

Modernization of aging industrial infrastructure

Adoption of smart and sensor integrated gearboxes - Trends

Integration of IoT enabled condition monitoring in gear systems

Shift toward lightweight and high efficiency gearbox designs

Growing preference for energy efficient transmission solutions - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Helical Gearboxes

Bevel Gearboxes

Worm Gearboxes

Planetary Gearboxes

Spur Gearboxes - By Platform Type (In Value%)

Industrial Machinery

Automotive and Commercial Vehicles

Wind Turbines

Material Handling Equipment

Mining and Construction Equipment - By Fitment Type (In Value%)

OEM Installations

Aftermarket Replacement

Retrofitted Systems

Modular Integrated Units

Custom Engineered Gearboxes - By EndUser Segment (In Value%)

Automotive Manufacturing

Energy and Power Generation

Oil and Gas Industry

Aerospace and Defense

Heavy Engineering and Mining - By Procurement Channel (In Value%)

Direct Sales Contracts

Authorized Distributors

Industrial Equipment Dealers

- Market Share Analysis

- Cross Comparison Parameters (Product Portfolio Diversity, Technology Integration Level, Manufacturing Capacity,Aftermarket Service Network, Pricing Strategy Gearbox Type Coverage, Torque Range Capability, Power Transmission Efficiency, Application Industry Focus, OEM Integration Depth, Aftermarket Penetration, Manufacturing Footprint, Vertical Integration Level, Lead Time Flexibility)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dana Incorporated

Regal Rexnord Corporation

Timken Company

Gleason Corporation

Curtiss Wright Corporation

Twin Disc Incorporated

SEW Eurodrive USA

Bonfiglioli USA

Sumitomo Drive Technologies USA

Nord Drivesystems USA

Rossi Gearmotors USA

Emerson Power Transmission

Brevini USA

Boston Gear

David Brown Santasalo

- Automotive manufacturers prioritize high durability and efficiency gear systems

- Energy producers demand robust gearboxes for wind and thermal plants

- Oil and gas operators require corrosion resistant and heavy duty units

- Industrial automation firms focus on compact and precision transmission solutions

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now