Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA hand gloves market is valued at USD ~ billion, rising from USD ~ billion on a historical base, and is forecast to grow at 8.3% CAGR during 2024–2030, reaching USD 10.1 billion. Growth is driven by healthcare modernization, OSHA-led workplace safety compliance, hospital procurement, manufacturing safety programs, and broader adoption of disposable and durable gloves across healthcare, food, chemicals, construction, and industrial operations.

California, Texas, Florida, Ohio, Pennsylvania, Illinois, and New York dominate demand because they combine large hospital networks, high industrial employment, logistics hubs, food processing clusters, and large construction markets. The U.S. has 6,093 hospitals, while healthcare generated 686,000 new jobs and hospitals added 215,000 jobs, increasing glove consumption across clinical, sanitation, laboratory, emergency, and facility-management environments.

Market Segmentation

By Product Type

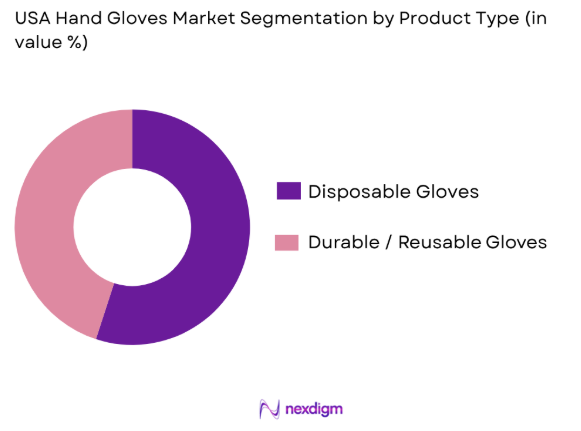

The USA hand gloves market is segmented by product type into disposable gloves and durable or reusable gloves. Recently, disposable gloves have a dominant market share in the USA under the segmentation product type, due to their essential role in infection control, food handling, pharmaceuticals, laboratories, and clinical care. Their single-use nature reduces cross-contamination risk, while nitrile, latex, vinyl, and polyethylene options allow buyers to match glove type with chemical resistance, comfort, cost, and regulatory needs. Healthcare demand remains especially strong because hospitals, dental clinics, diagnostic labs, and ambulatory care centers require frequent glove replacement during patient-facing activities. Grand View Research identifies disposable gloves as the largest U.S. hand protection segment and links demand to healthcare infrastructure and hygiene requirements.

By Material

The USA hand gloves market is segmented by raw material into nitrile gloves, natural rubber or latex, vinyl gloves, neoprene, leather, and others. Recently, nitrile gloves have a dominant market share in the USA under the segmentation raw material, due to their strong puncture resistance, chemical resistance, latex-free profile, and broad use in healthcare, chemicals, manufacturing, automotive repair, food processing, and oil and gas operations. Nitrile is preferred where users need higher protection than vinyl and lower allergy risk than latex. Demand is also supported by powder-free glove adoption and increased buyer preference for gloves that combine dexterity, barrier performance, and durability. Grand View Research notes nitrile as a high-growth raw material segment and links demand to construction, manufacturing, chemicals, mining, and oil and gas applications.

Competitive Landscape

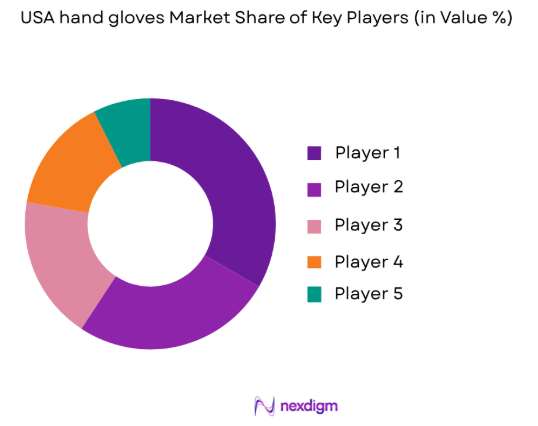

The USA hand gloves market is fragmented but led by global PPE manufacturers, healthcare distributors, and specialized industrial glove suppliers. Major players compete through material innovation, supply-chain reliability, hospital contracting, distributor networks, cut-resistance technology, chemical-protection portfolios, private-label supply, and compliance with FDA, OSHA, ANSI/ISEA, and ASTM requirements.

| Company | Establishment Year | Headquarters | Core Glove Focus | Key End Users | Material Strength | U.S. Distribution Strength | Regulatory Positioning | Market Strategy |

| Ansell Ltd. | 1893 | Richmond, Australia | Medical and industrial gloves | ~ | ~ | ~ | ~ | ~ |

| Medline Industries | 1966 | Northfield, Illinois, USA | Exam, surgical, and healthcare gloves | ~ | ~ | ~ | ~ | ~ |

| MCR Safety | 1974 | Collierville, Tennessee, USA | Industrial safety gloves | ~ | ~ | ~ | ~ | ~ |

| Superior Glove | 1910 | Acton, Ontario, Canada | Cut-resistant and industrial gloves | ~ | ~ | ~ | ~ | ~ |

| SHOWA Group | 1954 | Amsterdam, Netherlands / global operations | Industrial, chemical, and disposable gloves | ~ | ~ | ~ | ~ | ~ |

USA hand gloves Market Analysis

Growth Drivers

Rising Health and Safety Awareness Across Industries

The USA hand gloves market is supported by stronger workplace safety enforcement across industrial, logistics, construction, manufacturing, and healthcare workplaces. OSHA conducted 34,625 inspections in FY 2024, including 17,455 unprogrammed inspections tied to complaints, injuries, fatalities, and referrals. BLS reported 2.5 million nonfatal workplace injuries and illnesses in private industry in 2024, keeping protective gloves relevant for cut, chemical, abrasion, puncture, heat, and contamination risks. This is reinforced by a large macroeconomic base, as the World Bank records U.S. GDP at USD 28.75 trillion in 2024, supporting continued employer spending on PPE compliance.

Increasing Demand in Medical and Healthcare Applications

Medical and healthcare applications remain a core growth driver for the USA hand gloves market because gloves are used in hospitals, emergency departments, laboratories, dental clinics, ambulatory care, and long-term care. CDC data shows 155.4 million emergency department visits, including 43.5 million injury-related visits and 17.8 million visits resulting in hospital admission. AHA’s hospital statistics report 33,679,935 total admissions and 916,752 staffed beds in U.S. hospitals, creating continuous glove demand for examinations, procedures, infection control, cleaning, and patient handling. BLS also reported healthcare added 46,000 jobs in December 2024, increasing glove-consuming clinical labor activity.

Challenges

Regulations and Compliance Standards Across Different Sectors

The USA hand gloves market faces compliance complexity because glove requirements differ across medical, food, chemical, construction, laboratory, and industrial settings. FDA classifies medical gloves as disposable medical devices and references import controls for surgeon’s and patient examination gloves, while OSHA enforcement covers workplace hand protection across hazard-specific environments. FDA import alerts include glove-related entries such as Nitra Med Heavy Powder Free Nitrile Examination Glove with a January 9, 2024 publication date, showing active regulatory screening. OSHA also recorded 34,625 inspections in FY 2024, making documentation, labeling, testing, and sector-specific compliance a continuing operational burden for suppliers.

Environmental Concerns and Disposal of Single-Use Gloves

Environmental pressure is a market-specific challenge because disposable medical and industrial gloves are typically single-use and difficult to recycle after contamination. EPA defines medical waste as waste generated by hospitals, physicians’ offices, dental practices, blood banks, veterinary clinics, medical research facilities, and laboratories, including materials contaminated by blood or body fluids. CDC-reported healthcare utilization remains large, with 155.4 million emergency department visits and 17.8 million admissions from emergency departments, creating repeated glove disposal streams. AHA also reports 916,752 staffed hospital beds, which implies continuous patient-care glove use across shifts, procedures, isolation rooms, sanitation, and emergency care.

Opportunities

Technological Innovations in Glove Materials and Manufacturing

Technological innovation creates future opportunity in the USA hand gloves market as buyers seek gloves with better barrier protection, tactile sensitivity, chemical resistance, cut resistance, and lower allergy risk. FDA identifies medical gloves as disposable products covering examination gloves, surgical gloves, and chemotherapy gloves, creating room for material-specific innovation across clinical use cases. The opportunity is supported by the scale of healthcare demand: CDC reports 155.4 million emergency department visits, while AHA reports 33,679,935 hospital admissions and 916,752 staffed beds. These numbers support demand for improved nitrile, latex-free, biodegradable, accelerator-free, and task-specific gloves across healthcare and industrial procurement.

Expansion of E-commerce and Direct-to-Consumer Channels

E-commerce expansion creates an opportunity for glove manufacturers and distributors to reach clinics, small businesses, food handlers, laboratories, home healthcare users, and industrial buyers through direct online ordering. U.S. Census Bureau data shows seasonally adjusted retail e-commerce sales of USD 289.2 billion in Q1 2024, USD 295.249 billion in Q3 2024, and USD 300.357 billion in Q4 2024. The same source states annual e-commerce sales accounted for 16.1% of total retail sales in 2024, supporting digital procurement of PPE consumables. For gloves, online channels help smaller buyers access bulk packs, specialty materials, and recurring replenishment without traditional distributor dependence.

Future Outlook

Over the next five years, the USA hand gloves market is expected to expand steadily, supported by healthcare workforce growth, stronger infection-prevention practices, rising industrial safety compliance, and higher demand for nitrile and powder-free gloves. Domestic PPE resilience, e-commerce procurement, hospital modernization, and stricter workplace safety programs will shape purchasing decisions. Innovation will focus on biodegradable gloves, improved tactile sensitivity, cut resistance, chemical protection, and supply-chain transparency.

Major Players

- Ansell Ltd.

- Medline Industries

- MCR Safety

- Superior Glove

- SHOWA Group

- 3M Company

- Kimberly-Clark Corporation

- Hartalega Holdings Berhad

- Top Glove Corporation Bhd

- Sempermed USA

- AMMEX Corporation

- Atlantic Safety Products

- Adenna LLC

- The Glove Company

- Delta Plus Group

Key Target Audience

- Glove manufacturers

- PPE distributors and wholesalers

- Hospital procurement departments

- Industrial safety managers

- Food processing companies

- Pharmaceutical and laboratory supply buyers

- Investments and venture capitalist firms

- Government and regulatory bodies: OSHA, FDA, CDC, NIOSH, Department of Labor

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map of manufacturers, distributors, raw material suppliers, healthcare buyers, industrial users, and regulatory bodies in the USA hand gloves market. This step uses desk research, company disclosures, public safety standards, and industry databases to identify demand drivers, price variables, material preferences, and end-use behavior.

Step 2: Market Analysis and Construction

In this phase, historical revenue data, product segmentation, raw material trends, and end-use adoption are compiled and analyzed. The process includes evaluating disposable versus durable glove demand, nitrile adoption, hospital procurement, manufacturing safety requirements, and industrial PPE penetration to structure market estimates and segment shares.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are validated through structured consultations with PPE distributors, healthcare procurement specialists, safety officers, industrial buyers, and glove manufacturers. These discussions help test assumptions related to purchase frequency, material substitution, compliance requirements, supply-chain constraints, and buyer preference shifts.

Step 4: Research Synthesis and Final Output

The final phase consolidates secondary research, company intelligence, regulatory references, and expert validation into a structured market report. Findings are cross-checked across product type, raw material, end-use, and competitive positioning to produce a validated outlook for the USA hand gloves market.

- Executive Summary

- Research Methodology (Market Definitions and Assumptions, Abbreviations, Top‑Down & Bottom‑Up Sizing Approach, E‑Commerce & Retail Channel Data Sources, Primary Research Framework, Secondary Data Validation, Forecasting Models and Assumptions, Limitations and Sensitivity Analyses)

- Definition and Scope

- Ecosystem Genesis and Evolution of Hand Gloves Adoption

- Macro‑Economic and Hand Gloves Demand Drivers

- Material Technology Adoption Index

- Supply Chain Dependency & Characteristics

- Infrastructure Mapping of Hand Gloves Manufacturing and Distribution Channels

- Growth Drivers

Rising Health and Safety Awareness Across Industries

Increasing Demand in Medical and Healthcare Applications

Surge in Disposable Gloves Usage During Pandemic

Rising Industrialization and Workplace Safety Regulations - Challenges

Fluctuating Raw Material Prices and Supply Chain Issues

Regulations and Compliance Standards Across Different Sectors

Competition from Low-Cost Imports

Environmental Concerns and Disposal of Single-Use Gloves - Opportunities

Technological Innovations in Glove Materials and Manufacturing

Expansion of E-commerce and Direct-to-Consumer Channels

Increase in Demand for Specialized Gloves (e.g., for Hazardous Environments)

Growing Focus on Sustainability and Eco-friendly Alternatives - Trends

Growth in Use of Non-Latex and Hypoallergenic Gloves

Shift Towards High-Performance and Durable Gloves

Emerging Trend of Smart Gloves with Integrated Sensors

Rising Adoption of Customizable and Specialty Gloves - Government Regulations & Standards

Workplace Safety Regulations and Standards

FDA Regulations for Medical Gloves

Environmental Guidelines for Disposable Gloves

Import Regulations and Tariffs on Glove Products

Occupational Safety and Health Administration (OSHA) Guidelines - SWOT Analysis

- Porter’s Five Forces

- Stakeholder Ecosystem

- By Retail Value, 2020-2025

- By Unit Sales, 2020-2025

- By Average Selling Price (ASP) and Product Tier, 2020-2025

- By Channel Contribution, 2020-2025

- By Product Type (In Value %)

Disposable Gloves

Industrial Gloves

Medical Gloves

Protective Gloves

Workplace and Safety Gloves

Specialized Gloves - By Material (In Value %)

Nitrile Gloves

Natural Rubber / Latex

Vinyl Gloves

Neoprene

Leather - By End‑User (In Value %)

Consumer Cohort

Healthcare Sector

Industrial Sector

Food Processing and Service

Laboratories

Chemical and Hazardous Material Handling - By Distribution Channel (In Value %)

E-commerce and Online Retail

Brand Flagship Stores

Wholesale and Distribution Channels

Specialized Retailers

Direct Sales

- Market Share by Value and Volume

- Cross‑Comparison Parameters (Product Portfolio Breadth, Material Diversity, Distribution Network Reach, Brand Positioning, Price Point Clustering, After-Sales Service and Warranty, Manufacturing Footprint, Consumer Satisfaction & Retention, Revenue and Growth Metrics)

- SWOT of Major Players

- Pricing Tier Benchmark Analysis

- Major Competitors

Kimberly-Clark

Ansell

Top Glove

Rubberex

Medline Industries

Halyard Health

Cardinal Health

3M

Sempermed

Hartalega

Dynarex

MCR Safety

- Trends and Preferences in Hand Gloves Usage

- Impact of Regulatory Changes on Demand

- Growing Adoption of Medical and Industrial Gloves

- Role of Consumer Preferences in Glove Material Selection

- By Retail Value, 2026-2035

- By Unit Sales, 2026-2035

- By Average Selling Price (ASP) and Product Tier, 2026-2035

- By Channel Contribution, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now