Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA HbA1c Monitoring Devices market is valued at USD ~ billion, which plays a critical role in managing diabetes, one of the most prevalent chronic diseases in the country. The demand for these devices is primarily driven by the increasing number of diabetes diagnoses and the need for continuous monitoring for proper management. Furthermore, advances in home-based monitoring devices are transforming the landscape, offering patients more autonomy in managing their health. The accessibility and convenience of these devices are contributing significantly to their market growth.

The USA market is led by major metropolitan areas such as New York, California, and Texas, where the highest number of diabetes patients reside. These regions benefit from well-established healthcare infrastructure, insurance coverage, and government-supported health initiatives. As a result, they create a stable demand for HbA1c monitoring devices. Additionally, the USA benefits from global players who influence technology and product innovations in the market, such as those from Europe and Asia, further contributing to growth and shaping local consumer preferences.

Market Segmentation

By Device Type

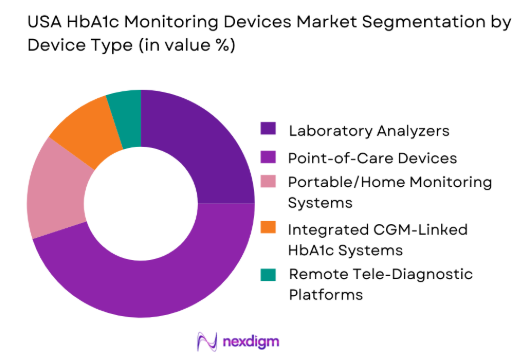

The USA HbA1c Monitoring Devices market is segmented by device type into laboratory analyzers, point-of-care (POC) devices, portable/home monitoring systems, integrated continuous glucose monitoring (CGM) linked HbA1c systems, and remote tele-diagnostic platforms. Point-of-care (POC) devices dominate this segment. Their rapid testing capabilities and integration into clinical environments, particularly within urgent care and outpatient settings, have made them a preferred choice. As demand for faster, more accessible diagnostics increases, POC devices continue to play a pivotal role, enabling healthcare providers to deliver timely care and results.

By End-Use Industry / Customer Type

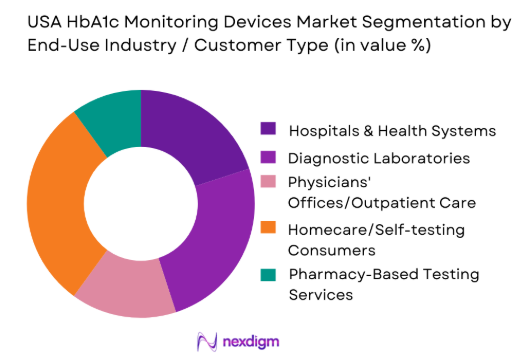

The market is further segmented by end-use industry into hospitals & health systems, diagnostic laboratories, physicians’ offices, homecare/self-testing consumers, and pharmacy-based testing services. Homecare/self-testing consumers have the largest share in this segment. The shift toward patient-centric care and growing interest in managing diabetes independently has increased the demand for home-use HbA1c devices. These devices provide patients with convenience and the ability to monitor their health regularly, empowering them to make informed decisions about their diabetes care.

Competitive Landscape

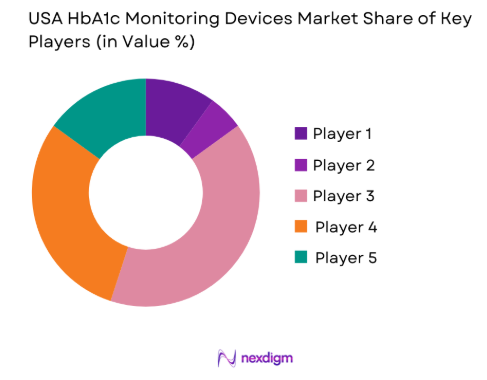

The USA HbA1c Monitoring Devices market is dominated by a few major players, including Abbott Diagnostics and global brands like Roche Diagnostics, Bio-Rad Laboratories, and Siemens Healthineers. This consolidation highlights the significant influence of these key companies. Their strong R&D capabilities, regulatory approvals, and broad distribution networks have allowed them to capture significant market shares, ensuring a competitive environment.

| Company | Establishment Year | Headquarters | Product Range | Regulatory Approvals | Market Reach | R&D Investment | Customer Support |

| Abbott Diagnostics | 1888 | Chicago, USA | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Basel, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Bio-Rad Laboratories | 1952 | Hercules, USA | ~ | ~ | ~ | ~ | ~ |

| Siemens Healthineers | 1847 | Erlangen, Germany | ~ | ~ | ~ | ~ | ~ |

| EKF Diagnostics | 2004 | London, UK | ~ | ~ | ~ | ~ | ~ |

USA HbA1c Monitoring Devices Market Analysis

Growth Drivers

Rising Diabetes Prevalence and Increased Monitoring Frequency

The growing prevalence of diabetes is driving the demand for frequent and efficient monitoring solutions. As more people are diagnosed with diabetes, particularly Type 2, the need for regular monitoring of glucose levels and other related metrics, such as HbA1c, becomes essential for effective disease management. With diabetes becoming a global health crisis, patients and healthcare providers are increasingly focused on early detection and ongoing management of the condition. This leads to more frequent monitoring, creating a growing market for diabetes testing tools, including HbA1c testing, continuous glucose monitoring (CGM), and other diagnostic technologies.

Shift to Value-Based Care and Outcomes Linked Diabetes Management

The shift towards value-based care models is another significant driver for the growth of diabetes management solutions. Under value-based care, healthcare providers are incentivized to improve patient outcomes and reduce the overall cost of care. For diabetes, this means a focus on long-term management and better patient adherence to treatment plans, rather than just addressing acute care needs. As a result, there is an increasing demand for tools and technologies that enable continuous monitoring, improve patient engagement, and provide actionable data to both patients and healthcare providers. This trend encourages the use of comprehensive diabetes management platforms that help reduce complications and hospital admissions.

Challenges

Analytical Performance Variability Across Methods and Settings

One of the key challenges in diabetes testing is the variability in analytical performance across different testing methods and settings. Different devices, whether for HbA1c or glucose monitoring, can yield inconsistent results depending on factors such as the technology used, calibration, or even environmental conditions in decentralized settings. This lack of standardization can make it difficult for healthcare providers to rely on results, especially when comparing data across various testing sites, from hospitals to home care environments. Ensuring consistency in analytical performance is crucial for the effectiveness of diabetes management, and without it, patient outcomes may be compromised.

Preanalytical and Sample Handling Issues in Decentralized Sites

Preanalytical and sample handling issues are significant challenges, particularly in decentralized testing environments like home care or ambulatory settings. Proper handling of samples is critical to obtaining accurate and reliable results, but decentralized testing sites often lack the standardization of processes found in clinical laboratories. Inaccurate sample collection, improper storage, or transportation of specimens can lead to erroneous results, which can negatively impact clinical decision-making. These challenges highlight the need for better training, equipment, and processes to ensure that testing in non-laboratory settings is as reliable as in more controlled environments.

Opportunities

CLIA Waived Expansion for Rapid HbA1c Testing in Ambulatory Care

The expansion of CLIA-waived tests for rapid HbA1c testing presents an opportunity to increase access to diabetes management tools in ambulatory care settings. CLIA-waived tests are those that meet specific standards for safety and accuracy, allowing them to be used in a variety of healthcare environments without complex oversight. By offering rapid HbA1c testing in ambulatory care, more patients can receive timely results without needing to visit specialized labs, improving patient adherence to treatment plans and facilitating better diabetes management. This move towards decentralizing testing could lead to more frequent monitoring and earlier intervention, which is key in managing diabetes effectively.

Bundled Diabetes Monitoring Programs Combining HbA1c and CGM

Bundled diabetes monitoring programs that combine HbA1c testing with continuous glucose monitoring (CGM) offer significant opportunities for improving patient care and outcomes. By integrating these two diagnostic methods, healthcare providers can offer a more comprehensive approach to diabetes management. HbA1c provides a long-term view of glucose control, while CGM offers real-time, dynamic data on glucose levels, helping to identify patterns and fluctuations that are important for immediate management. This combination not only provides patients with more accurate and actionable data but also promotes better adherence to treatment plans, reducing the risk of complications and improving long-term health outcomes.

Future Outlook

Over the next few years, the USA HbA1c Monitoring Devices market is expected to experience continued growth, driven by both technological advancements and changing healthcare policies. The integration of digital health platforms with monitoring devices will enhance the ease of managing diabetes. Furthermore, as the healthcare industry increasingly embraces value-based care, there will be a heightened demand for devices that contribute to more efficient and effective patient management.

Major Players

- Abbott Diagnostics

- Roche Diagnostics

- Bio-Rad Laboratories

- Siemens Healthineers

- EKF Diagnostics

- Tosoh Bioscience

- HemoCue

- ARKRAY, Inc.

- Trinity Biotech

- i-SENS

- Convergent Technologies

- Erba Mannheim

- OSANG Healthcare

- ApexBio

- Mindray

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies (FDA, CDC)

- Healthcare providers (Hospitals, clinics)

- Medical device manufacturers

- Pharmaceutical companies focused on diabetes management

- Insurance companies

- Health technology startups & innovators

- Distributors and wholesalers of medical devices

Research Methodology

Step 1: Identification of Key Variables

The research begins by identifying critical variables affecting the market, such as healthcare infrastructure, regulatory factors, and technological innovations. Secondary data sources, including government and industry reports, are leveraged to create a comprehensive ecosystem map.

Step 2: Market Analysis and Construction

Historical market data is gathered to assess the current market landscape. Key metrics, such as penetration rates and revenue generation, are analyzed to construct a detailed understanding of the market size and dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations provide critical insights into emerging trends, technology adoption, and industry shifts. These consultations involve interviews with key stakeholders, including healthcare providers, manufacturers, and regulators, to validate hypotheses and ensure data accuracy.

Step 4: Research Synthesis and Final Output

The final report is synthesized using a combination of top-down and bottom-up analysis, incorporating both secondary and primary research. Expert insights and verified data are merged to produce a comprehensive, accurate market report.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, HbA1c testing taxonomy and care setting mapping, market sizing logic by instrument installed base and test volume, revenue attribution across analyzers reagents cartridges and controls, primary interview program with labs health systems payers and distributors, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Evolution of HbA1c Testing in the USA

- Diabetes Burden and Screening Frequency Drivers

- Care Pathway Mapping Across Lab Testing POCT and Home Use

- Reimbursement and Coding Landscape for HbA1c Testing

- CLIA Waiver Implications for Point of Care HbA1c Adoption

- Growth Drivers

Rising diabetes prevalence and increased monitoring frequency

Shift to value based care and outcomes linked diabetes management

Expansion of point of care testing in primary care settings

Quality measures tied to HbA1c control targets

Growth of retail clinics and convenient care models - Challenges

Analytical performance variability across methods and settings

Preanalytical and sample handling issues in decentralized sites

Reimbursement pressure and cost containment in routine testing

Operator training and quality control burden in POCT

Workflow integration barriers for EHR and LIS connectivity - Opportunities

CLIA waived expansion for rapid HbA1c testing in ambulatory care

Bundled diabetes monitoring programs combining HbA1c and CGM

Automation and high throughput upgrades in reference laboratories

Connectivity led differentiation through QC analytics and compliance tools

Home testing pathways linked to telehealth diabetes coaching - Trends

Migration toward cartridge based rapid testing in clinics

Greater emphasis on NGSP alignment and IFCC traceability

Integration of HbA1c results into population health dashboards

Rising demand for low maintenance analyzers with minimal calibration

Standardization of POCT governance and competency programs - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Test Volume, 2019–2024

- By Installed Base, 2019–2024

- By Lab vs Point of Care Revenue Split, 2019–2024

- By Fleet Type (in Value %)

Hospital health system laboratories

Independent reference laboratories

Physician office laboratories and clinics

Retail clinics and pharmacy based care

Home testing and consumer self monitoring - By Application (in Value %)

Diabetes diagnosis support

Routine glycemic control monitoring

Therapy adjustment and medication titration

Population screening and employer wellness

Preoperative and inpatient glycemic risk assessment - By Technology Architecture (in Value %)

HPLC based HbA1c analyzers

Immunoassay based HbA1c analyzers

Enzymatic assay based HbA1c systems

Boronate affinity based HbA1c systems

Lab integrated high throughput analyzers

Single use cartridge based point of care devices - By Connectivity Type (in Value %)

Standalone analyzers with local reporting

LIS integrated laboratory analyzers

EHR integrated point of care workflows

Cloud connected quality management platforms

Remote service monitoring and predictive maintenance - By End-Use Industry (in Value %)

Clinical laboratories and pathology networks

Primary care and endocrinology practices

Retail health operators and pharmacy chains

Payers and value based care organizations

Public health programs and screening providers - By Region (in Value %)

Northeast

Midwest

South

West

- Competitive ecosystem structure across lab analyzer vendors POCT specialists and diagnostics distributors

- Positioning driven by NGSP alignment workflow integration and service footprint

- Cross Comparison Parameters (NGSP certification and method alignment, IFCC traceability readiness, analytical precision and bias performance, turnaround time per test, sample type and minimum volume, throughput capacity and automation fit, connectivity options for LIS and EHR, reagent and consumable cost per reportable result)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles

Abbott

Roche Diagnostics

Siemens Healthineers

Tosoh Bioscience

Bio Rad Laboratories

Beckman Coulter

EKF Diagnostics

Trinity Biotech

PTS Diagnostics

Nova Biomedical

ARKRAY

Sebia

Menarini Diagnostics

DiaSys Diagnostic Systems

Randox Laboratories

- Lab director priorities for throughput accuracy and method standardization

- Clinic buyer priorities for turnaround time simplicity and workflow fit

- POCT coordinator governance models and compliance requirements

- Payer influence on testing frequency and site of care selection

- Total cost of ownership drivers across instrument reagent and service

- By Value, 2025–2030

- By Test Volume, 2025–2030

- By Installed Base, 2025–2030

- By Lab vs Point of Care Revenue Split, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now