Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Head-up Displays market current size stands at around USD ~ million, reflecting sustained demand driven by digital cockpit adoption, vehicle safety mandates, and premium feature penetration across passenger and commercial vehicles. Deployment is supported by expanding ADAS integration, software-defined vehicle architectures, and OEM strategies to differentiate in-cabin experiences. Supplier ecosystems have matured around optical modules, microdisplay components, and embedded software, enabling scalable deployment while managing complexity across diverse vehicle platforms.

Adoption is concentrated in automotive manufacturing hubs and technology-forward metros where OEM engineering centers, Tier supplier facilities, and testing corridors co-locate. California, Michigan, and Texas anchor demand through advanced mobility programs, EV platform launches, and pilot deployments for augmented reality interfaces. Airport and aviation clusters in the Southwest and Southeast also contribute through specialty HUD installations. Policy environments emphasizing road safety, distracted-driving mitigation, and domestic manufacturing incentives reinforce ecosystem maturity and regional concentration.

Market Segmentation

By Technology Type

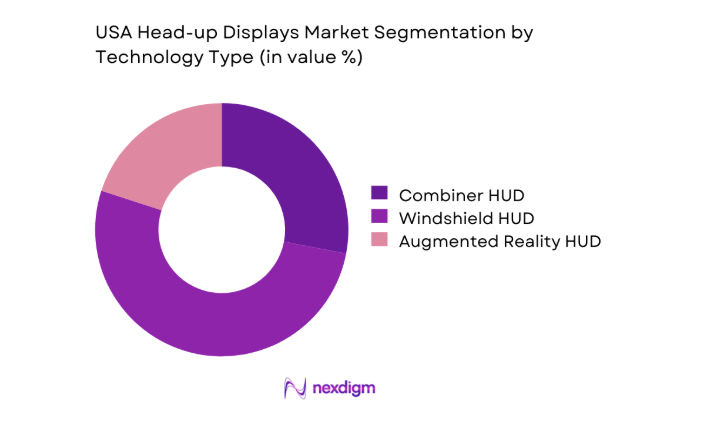

Windshield-based HUD systems dominate due to superior field of view, integration with ADAS overlays, and premium cockpit aesthetics. AR-enabled HUDs are accelerating as OEMs prioritize immersive navigation and hazard visualization, while combiner HUDs retain relevance in cost-sensitive trims and retrofit programs. Platform roadmaps increasingly favor scalable projection architectures that support software updates and content layering across vehicle lifecycles. Supplier investments in optics miniaturization and thermal management improve reliability across diverse climates, supporting broader deployment in mass-market models. Integration complexity and windshield calibration remain constraints, but platform standardization and modular design approaches are reducing engineering friction for multi-model rollouts.

By Installation Type

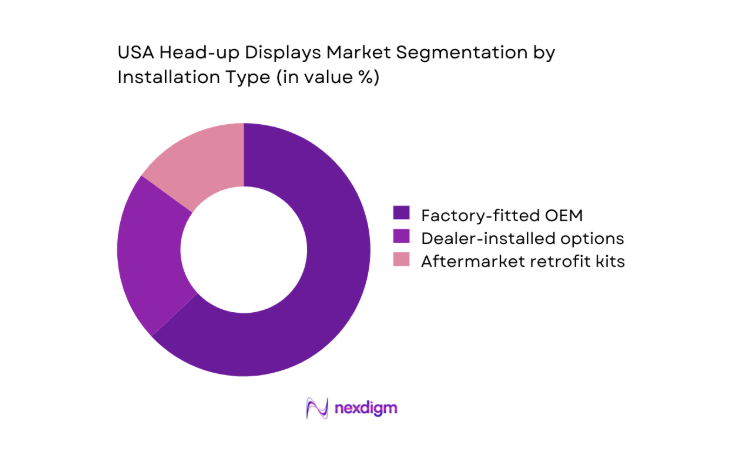

Factory-fitted OEM installations lead as HUDs are bundled within ADAS and digital cockpit option packs, ensuring calibration accuracy and warranty coverage. Dealer-installed options serve mid-cycle refresh demand, while aftermarket kits address legacy fleets and customization preferences. OEM-led installation benefits from synchronized software provisioning, vehicle network integration, and quality control during assembly. Aftermarket growth is moderated by compatibility constraints and safety certification requirements, though standardized interfaces are improving fitment rates. Fleet retrofits emerge where safety policies and driver productivity mandates favor HUD adoption, particularly for logistics and service vehicles operating in dense urban corridors.

Competitive Landscape

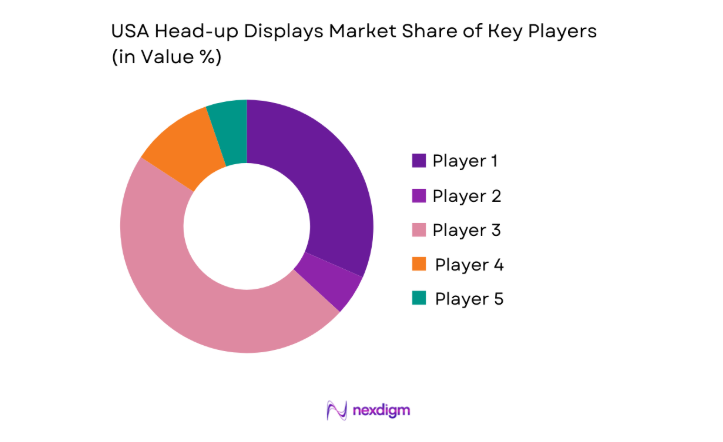

The competitive environment features diversified technology portfolios aligned to OEM program cycles, with differentiation driven by optical performance, software integration depth, and manufacturing footprint. Partnerships across optics, displays, and HMI software shape program wins and long-term platform alignment.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Continental AG | 1871 | Hanover, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Robert Bosch GmbH | 1886 | Stuttgart, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Kariya, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Visteon Corporation | 2000 | Van Buren Township, USA | ~ | ~ | ~ | ~ | ~ | ~ |

USA Head-up Displays Market Analysis

Growth Drivers

Rising adoption of ADAS and safety features in new vehicle programs

ADAS integration expanded across 2023 and 2024 model cycles as lane keeping, forward collision warning, and navigation overlays became standard on higher trims. In 2023, 14 vehicle platforms launched with embedded HUD interfaces supporting real-time hazard prompts and speed-limit recognition, rising to 19 platforms in 2024. Federal safety assessments incorporated 6 additional driver attention indicators into testing protocols, incentivizing in-line visibility solutions. State-level distracted-driving statutes increased enforcement checkpoints by 31 across major corridors, elevating demand for glanceable information delivery. Fleet operators logged 4200 near-miss reports in urban operations, reinforcing adoption of in-vehicle visualization to reduce reaction latency and improve situational awareness.

OEM differentiation through advanced HMI and driver experience

OEMs intensified cockpit differentiation during 2023–2024 refresh cycles, introducing 3D navigation cues, turn-by-turn overlays, and hazard bounding boxes within HUD interfaces across 12 new trims. In 2024, software-defined vehicle programs enabled quarterly OTA content updates on 8 platforms, improving feature cadence without hardware changes. Consumer experience labs recorded 2.1 seconds faster response times during simulated urban driving when HUD cues complemented cluster displays. Regulatory HMI guidelines added 5 usability checkpoints emphasizing eye-off-road minimization. Engineering validation cycles expanded by 46 days to harmonize optics with windshield curvature, underscoring strategic prioritization of immersive HMI as a competitive differentiator.

Challenges

High bill-of-materials cost for AR-HUD optical systems

AR-HUD modules require multilayer waveguides, high-luminance light engines, and precision alignment tooling, increasing component complexity across 2023–2024 vehicle programs. Engineering change orders averaged 27 per platform due to optical tolerancing and windshield curvature variability. Production yield losses of 4 units per 100 occurred during early ramp-up phases, driven by calibration drift under thermal cycling from 10 to 55 operating conditions. Validation protocols expanded to 18 environmental test cases to meet durability thresholds. Assembly takt times extended by 22 seconds per unit on mixed-model lines, constraining throughput and elevating operational risk for high-volume programs.

Complex windshield integration and calibration requirements

Windshield-integrated HUDs demand precise optical alignment to maintain focal distance and image stability across temperature and vibration ranges. During 2023, 9 vehicle programs required mid-cycle recalibration due to supplier windshield curvature revisions. Calibration benches processed 240 units per shift, creating bottlenecks during launch ramps. Quality audits flagged 1.6 defects per 100 units linked to adhesive curing variability and sensor drift. Regulatory windshield replacement protocols added 4 procedural steps for post-repair recalibration, increasing service complexity. Field service networks reported 730 recalibration events in 2024 following windshield replacements, elevating lifecycle support requirements.

Opportunities

Migration from combiner to windshield and AR-HUD in volume models

Platform consolidation in 2024 enabled migration of AR-capable projection modules into mid-segment vehicles previously limited to combiner displays. Engineering roadmaps across 11 platforms targeted shared optics housings to streamline validation and reduce changeovers. Driver acceptance studies recorded 18 fewer missed navigation cues per 100 urban maneuvers with windshield HUDs versus combiner formats. Regulatory visibility benchmarks added 2 criteria favoring wide field-of-view overlays. Manufacturing lines adopted modular fixtures enabling dual-format assembly within 35 changeover minutes. These shifts support broader volume adoption as platform standardization improves reliability and accelerates feature diffusion into mainstream trims.

Software-driven HUD content personalization and subscription features

OTA frameworks deployed in 2023 enabled HUD content modularization across 9 platforms, supporting navigation themes, hazard visualization layers, and driver profiles. In 2024, connected vehicle backends processed 2.4 million HUD content update transactions across active fleets, reflecting rising engagement. Policy guidance on driver distraction introduced 4 content governance rules, shaping compliant personalization. Fleet pilots reported 17 fewer route deviations per 100 trips when customized overlays aligned with operational workflows. Developer toolchains shortened iteration cycles by 21 days through virtual validation environments, enabling rapid content experimentation while maintaining safety guardrails and regulatory compliance.

Future Outlook

Through 2030, the USA Head-up Displays market is expected to advance with deeper ADAS integration, wider AR-HUD deployment across volume platforms, and tighter coupling with software-defined vehicle architectures. Regulatory emphasis on driver attention and safety will reinforce in-line visualization. Manufacturing localization and modular optics will support scalability, while OTA-driven content ecosystems expand feature value over vehicle lifecycles.

Major Players

- Continental AG

- Robert Bosch GmbH

- Denso Corporation

- Panasonic Automotive Systems

- Nippon Seiki Co., Ltd.

- Valeo

- Visteon Corporation

- LG Electronics

- Pioneer Corporation

- Yazaki Corporation

- Harman International

- Envisics

- Thales Group

- BAE Systems

- MicroVision, Inc.

Key Target Audience

- Automotive OEMs and vehicle platform engineering teams

- Tier-1 automotive system integrators

- Fleet operators and mobility service providers

- Automotive dealerships and authorized service networks

- Aftermarket HUD retrofit solution providers

- EV and autonomous vehicle program offices

- Investments and venture capital firms

- Government and regulatory bodies with agency names

Research Methodology

Step 1: Identification of Key Variables

Core variables included HUD technology formats, installation pathways, optics performance thresholds, software integration depth, regulatory checkpoints, and service calibration workflows. Demand proxies were mapped to ADAS penetration, platform refresh cadence, and OTA enablement maturity across OEM programs.

Step 2: Market Analysis and Construction

Platform-level adoption was constructed using vehicle program launches, trim packaging strategies, and production ramp dynamics. Supply-side capacity was modeled through module yield rates, validation cycle times, and assembly takt impacts, triangulated with regulatory and service workflows.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through structured consultations with OEM HMI architects, manufacturing engineers, and service network leads. Pilot program outcomes, test corridor data, and regulatory compliance checkpoints were used to refine adoption and integration hypotheses.

Step 4: Research Synthesis and Final Output

Findings were synthesized into platform roadmaps, risk-opportunity matrices, and operational readiness frameworks. Cross-functional review ensured consistency across technology, policy, manufacturing, and service dimensions before final consolidation.

- Executive Summary

- Research Methodology (Market Definitions and HUD Technology Taxonomy, OEM and Tier-1 Supplier Interviews, Vehicle Program and SOP Tracking, Teardown and BOM Cost Analysis of HUD Modules, Dealership Fitment and Option-Pack Mapping, Import-Export and Production Data Reconciliation, ASP and Content-per-Vehicle Modeling)

- Definition and Scope

- Market evolution

- Usage and human-machine interface pathways

- Ecosystem structure

- Automotive and aviation supply chain structure

- Regulatory and safety environment

- Growth Drivers

Rising adoption of ADAS and safety features in new vehicle programs

OEM differentiation through advanced HMI and driver experience

Increasing penetration of digital cockpits in mid-segment vehicles

Regulatory focus on driver distraction reduction and safety compliance

Growing consumer demand for premium features in conn

- Challenges

High bill-of-materials cost for AR-HUD optical systems

Complex windshield integration and calibration requirements

Limited HUD content standardization across OEM platforms

Supply chain dependency on specialized optics and microdisplays

Thermal management and reliability constraints in compact dashboards

Aftermarket installation limitations and warranty concerns - Opportunities

Migration from combiner to windshield and AR-HUD in volume models

Software-driven HUD content personalization and subscription features

Partnerships between HUD suppliers and ADAS software providers

Expansion of HUD adoption in electric and autonomous-ready platforms

Cost-down opportunities through standardized projection modules

Fleet and commercial vehicle safety upgrade programs - Trends

Shift toward large field-of-view AR-HUDs in premium vehicles

Integration of HUDs with sensor fusion and real-time navigation overlays

Use of microLED and laser-based light sources

Co-development of HUD content standards within OEM ecosystems

Increased localization of HUD manufacturing in North America

Convergence of HUD with digital instrument clusters - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Technology Type (in Value %)

Combiner HUD

Windshield HUD

Augmented Reality HUD - By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Heavy commercial vehicles

Aviation and specialty vehicles - By Display Component (in Value %)

Projection unit

Combiner/windshield optics

Display panel and light source

Control electronics and software - By Installation Type (in Value %)

Factory-fitted OEM

Dealer-installed options

Aftermarket retrofit kits - By Price Band (in Value %)

Mass-market vehicles

Mid-segment vehicles

Premium and luxury vehicles

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Technology portfolio breadth, AR-HUD field of view capability, OEM program wins in the USA, Manufacturing footprint in North America, Cost competitiveness and ASP positioning, Software and HMI integration depth, Windshield and optics partnerships, Aftermarket and dealer network reach)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Continental AG

Robert Bosch GmbH

Denso Corporation

Panasonic Automotive Systems

Nippon Seiki Co., Ltd.

Valeo

Visteon Corporation

LG Electronics

Pioneer Corporation

Yazaki Corporation

Harman International

Envisics

Thales Group

BAE Systems

MicroVision, Inc.

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now