Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA health apps market is valued at USD ~ billion as of 2024, supported by a prior-year baseline of USD ~ million in revenue and a broadening payer/provider pull for remote monitoring, teleconsults, chronic disease self-management, and digital front doors. Monetization is increasingly anchored in subscriptions, B2B/B2B2C contracts (employers, payers, providers), and care-program reimbursement alignment, while consumer demand is reinforced by rising in-app spending across the U.S. app economy and sustained engagement in health tracking use cases.

Market dominance concentrates in San Francisco Bay Area, New York, Boston, Seattle, and Los Angeles due to venture density, major digital health operators, academic medical networks, and enterprise buyer access (national payers, self-insured employers, IDNs). These hubs also benefit from deep talent pools in mobile engineering, AI/analytics, and privacy/security, plus faster pathways to clinical partnerships and distribution through app ecosystems and EHR-connected workflows (patient portals, scheduling, lab results, remote patient monitoring).

Market Segmentation

By App Type

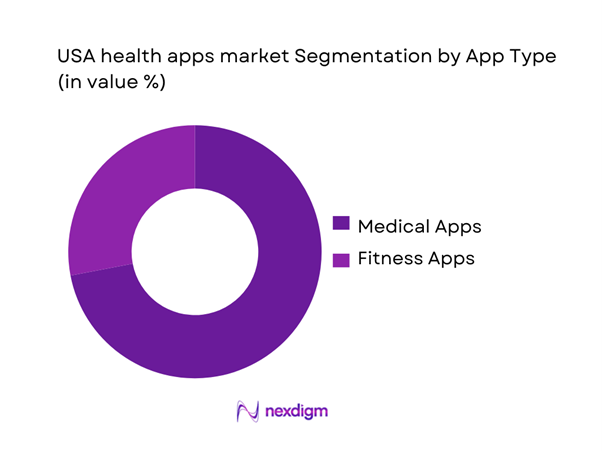

USA health apps are segmented into Medical Apps and Fitness Apps. Recently, Medical Apps have a dominant market share because they sit closer to reimbursable and operational healthcare value pools—virtual visits, remote patient monitoring, chronic care pathways, patient record access, and medication workflows—which are increasingly scaled through provider and payer channels rather than only direct-to-consumer marketing. Medical Apps also benefit from interoperability and platform “stickiness” (patient identity, longitudinal data, reminders, lab results, and care-team messaging), which drives higher retention versus standalone wellness utilities. As clinician shortages and care access pressures persist, enterprise buyers prioritize tools that reduce administrative friction and shift low-acuity interactions to digital channels. This structural pull—plus tighter integration with EHR-linked experiences and connected devices—keeps Medical Apps ahead of Fitness Apps in revenue contribution.

By Platform

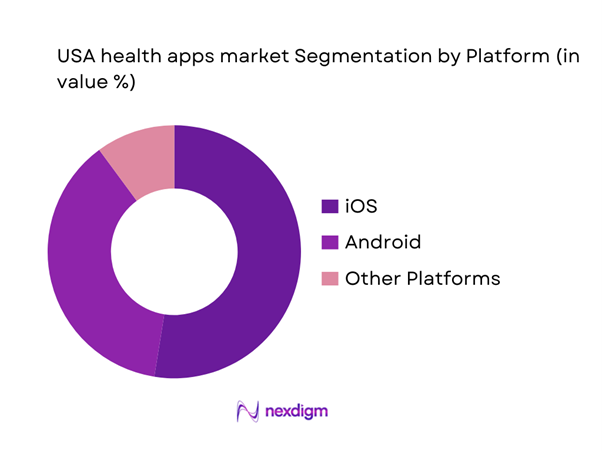

USA health apps are segmented into iOS, Android, and Others. Recently, iOS has a dominant market share because the platform combines high consumer trust, consistent device performance, and a strong wearable-led health stack that supports continuous tracking and premium experiences. Apple’s integrated framework (health data aggregation, permissions, and device interoperability) reduces friction for developers building regulated or clinically sensitive workflows, while users are more likely to pay for subscriptions in categories like fitness coaching, sleep optimization, and mental wellness. The App Store’s stricter review and privacy posture also improves perceived reliability for health-related use cases where data sensitivity is high. In parallel, enterprise deployments—especially those pairing app experiences with iPhone/Apple Watch populations—reinforce iOS as a preferred environment for engagement and retention, sustaining its leadership in platform-driven revenue contribution.

Competitive Landscape

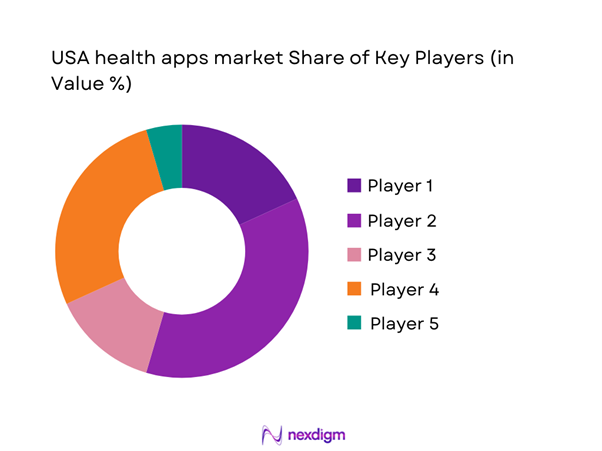

The USA health apps market is competitive but increasingly shaped by a mix of platform orchestrators (Apple/Google), virtual care operators (Teladoc, Amwell), and condition-focused specialists (Headspace/Calm, Omada, Noom). Consolidation occurs through acquisitions and partnerships aimed at expanding modality breadth (telehealth + coaching + monitoring) and strengthening enterprise distribution across payers, providers, and employers.

| Company | Est. Year | HQ | Primary App Focus | Monetization Model | Clinical / Regulatory Posture | Integration Depth (EHR / Devices / APIs) | Primary Buyer Channel | Differentiation Lever |

| Apple (Apple Health) | 1976 | Cupertino, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Google (Google Fit / Health initiatives) | 1998 | Mountain View, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Teladoc Health | 2002 | Purchase, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Headspace Health | 2010 | Santa Monica, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Omada Health | 2011 | San Francisco, USA | ~ | ~ | ~ | ~ | ~ | ~ |

USA Health Apps Market Analysis

Growth Drivers

Employer Benefit Digitization

U.S. employers are increasingly treating health apps as “benefits infrastructure,” because the underlying coverage base is massive and still expanding—creating a bigger addressable user pool for navigation, chronic-condition programs, and mental health apps bundled through employer plans. In the private sector, ~ people were enrolled in employer-sponsored health insurance, up from ~ the prior year—a coverage engine that benefits platforms plug into via single sign-on, eligibility files, and claims feeds. At the same time, benefit cost pressure keeps digitization on the agenda: the U.S. CPI rose ~ (all items), sustaining employer focus on steering care and reducing avoidable utilization. Macro capacity to spend is also high: the U.S. economy produced USD ~ in output and USD ~ GDP per capita, reinforcing the affordability of subscription-based health app bundles for insured, salaried populations. For app vendors, this shows up as faster procurement cycles through benefit aggregators and large employers, higher activation via payroll-linked eligibility, and lower CAC because distribution is “pre-paid” through the benefits channel. As employers widen digital-first offerings (navigation, musculoskeletal care, diabetes prevention, stress management), health apps increasingly compete on measurable outcomes (avoidable claims, improved adherence signals, fewer missed workdays) rather than just downloads—raising the value of enterprise-grade analytics, privacy controls, and clinical governance.

Payer Preventive Health Push

Payers and public programs are pushing prevention and “upstream” engagement because the U.S. healthcare bill is structurally large, and apps are a scalable way to deliver reminders, coaching, and care-gap closure at low marginal cost. National health spending reached USD ~ (total), with major categories such as hospital care at USD ~ and physician/clinical services at USD ~—a cost base that rewards payers for shifting activity away from high-cost settings. Value-based models amplify this behavior: the Medicare Shared Savings Program listed ~ ACOs and ~ assigned beneficiaries, making “digital engagement” (apps, messaging, remote monitoring, navigation) a practical lever for closing quality measures and reducing avoidable admissions across millions of lives. In parallel, innovation tracks include accountable-care models with ~ ACOs participating—another large channel for app-enabled prevention, screening prompts, and longitudinal coaching. Macro context supports sustained payer attention: the U.S. scale of output (USD ~ GDP) enables continued insurance and public spending, while “cost discipline” pressures encourage tools that improve adherence and reduce leakage. In practice, the preventive push translates into payer app marketplaces, condition-specific programs tied to claims and care management, and reimbursement or contract language that increasingly expects digital touchpoints (care navigation, secure messaging, evidence-based content, and data exchange hooks).

Challenges

Consumer Trust Deficit

Trust is a first-order constraint in U.S. health apps because the product is inseparable from sensitive data and behavior change. Breach and enforcement signals have become impossible for buyers to ignore: reporting on the U.S. healthcare cyber environment notes ~ incidents in a recent year affecting nearly ~ individuals—scale that hardens consumer skepticism and forces employers and payers to demand stronger vendor risk controls. Regulators reinforce this posture through ongoing work on consumer privacy and health data practices, including formal updates on privacy and data security activity—raising the baseline expectation for consent, data minimization, and truthful claims around health data use. Macro conditions matter because higher system spend increases scrutiny: national health expenditure totals (USD ~) mean more stakeholders and more data flows, expanding the attack surface and reputational risk when incidents occur. In this environment, “trust deficit” is not abstract—it shows up in employer security questionnaires, payer vendor audits, app-store review dynamics, and user hesitation to connect wearables or EHR data. Health apps that cannot clearly explain data flows (what is collected, why, retention period, and third-party sharing) face higher churn and weaker enterprise distribution. Conversely, vendors that implement strict governance (privacy impact assessments, encryption, incident response, limited sharing, and transparent user controls) are better positioned to win contracts where employers and payers fear downstream liability and reputational damage.

Data Privacy and Security Scrutiny

Privacy scrutiny is tightening because U.S. health apps sit at the intersection of consumer protection, health regulation, and cybersecurity expectations, and the “surface area” is expanding with connectivity. The FCC reports ~ total fixed and mobile internet connections and ~ mobile connections—scale that increases the volume of app sessions, API calls, and personal data transfers that must be secured. Enforcement visibility has increased through dedicated guidance on health privacy and the Health Breach Notification Rule—signaling that non-HIPAA consumer health data can still trigger regulatory exposure when mishandled. Meanwhile, security expectations are being productized through cybersecurity labeling programs for consumer IoT products, including recognizable labels and registries—important because health-adjacent wearables and connected devices increasingly feed health apps. Macro pressure compounds scrutiny: with GDP at USD ~ and broad healthcare spending at multi-trillion scale, policymakers and large buyers prioritize systemic risk reduction—pushing app vendors toward stronger controls (SBOM discipline, vulnerability management, MFA, audit trails, and least-privilege data access). For market participants, this scrutiny raises compliance cost and slows go-to-market unless “security by design” is built in. It also shifts competitive advantage toward vendors that can pass enterprise security reviews, support formal BAAs or DPAs where applicable, and provide defensible evidence of controls rather than marketing claims.

Opportunities

EHR-Embedded Health Apps

A major U.S. growth opportunity is embedding health apps inside EHR workflows and patient access channels, because interoperability is turning “apps” into a front-end layer for scheduling, results review, care plans, and longitudinal coaching. The Medicare ecosystem provides an adoption runway through accountable-care scale: the Shared Savings Program listed ~ ACOs serving ~ assigned beneficiaries, and these organizations have strong incentives to use app-enabled patient engagement to reduce leakage and improve quality performance. Policy infrastructure is also advancing through formal rulemaking tied to trusted exchange governance and participation pathways, supporting broader exchange that can make EHR-connected apps more practical across networks. The spend environment supports buyer willingness: national health expenditures of USD ~ mean even incremental improvements in care coordination can justify scaled app deployments when embedded into clinical workflow rather than left as optional downloads. Macro indicators add support—U.S. GDP at USD ~ implies continued investment capacity for health systems and payers to modernize patient engagement stacks. Commercially, the embedded opportunity favors vendors with strong API integration, identity management, evidence governance, and the ability to operate inside provider security and compliance environments. It also shifts competition away from app-store marketing toward partnerships with EHR vendors, provider networks, ACOs, and payers that want a measurable pathway from digital engagement to claims and utilization outcomes.

AI Triage and Care Navigation

AI triage and care navigation is a high-potential opportunity because U.S. healthcare is expensive and fragmented, and routing people to the right setting is a direct lever against avoidable utilization. The national cost base is clear in official accounting—USD ~ in hospital expenditures and USD ~ in physician and clinical services—so navigation tools that reduce unnecessary emergency or out-of-network care have strong economic logic. The connectivity foundation is equally large: ~ mobile connections enable always-available symptom intake, appointment finding, and benefits-aware care routing in real time. The regulatory landscape is also maturing toward transparency for AI-enabled tools, with maintained lists identifying authorized AI-enabled devices—important because triage engines increasingly overlap with regulated decision-support in higher-risk use cases. Macro indicators reinforce sustained demand: U.S. GDP totals USD ~ while CPI change ~ pressures employers and payers to adopt tools that can reduce friction and steer members toward cost-effective options. Practically, the opportunity is to build “claims-aware” navigation (in-network, deductible-aware), integrate with appointment availability, and connect to telehealth or escalation pathways—while meeting privacy, safety, and fairness requirements that enterprise buyers now treat as non-negotiable.

Future Outlook

Over the next several years, the USA health apps market is expected to expand as medical-grade app experiences move deeper into routine care delivery and as payers and employers intensify focus on cost containment, virtual-first access, and longitudinal condition management. AI-enabled triage, personalization, and automation will accelerate product differentiation, while privacy and interoperability requirements will shape go-to-market strategies. The market’s growth trajectory is supported by a forecast CAGR of ~ for the ~–~ period.

Major Players

- Apple

- Teladoc Health

- Amwell

- Headspace Health

- Calm

- Talkspace

- BetterHelp

- Omada Health

- Noom

- MyFitnessPal

- Fitbit

- Abbott

- Johnson & Johnson Services

Key Target Audience

- Investments and venture capitalist firms

- Health insurers and payers

- Self-insured employers and employer benefits managers

- Hospital systems and Integrated Delivery Networks

- Primary care and specialty provider groups and MSOs

- Pharma and life sciences companies

- Device OEMs and wearable manufacturers

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

We build a U.S.-specific ecosystem map covering platforms, digital health operators, payers, providers, employers, and device OEMs. Desk research is conducted across credible secondary sources, app intelligence datasets, and market trackers to define revenue pools, buying centers, and compliance factors.

Step 2: Market Analysis and Construction

Historical market sizing is constructed using reported market totals and validated demand-side indicators (consumer spend behavior, enterprise adoption patterns, and care delivery digitization). We align category boundaries (medical vs fitness apps) and reconcile overlaps with telehealth and RPM-linked app revenues.

Step 3: Hypothesis Validation and Expert Consultation

We validate assumptions through structured expert calls with product leaders, payer and employer benefits teams, clinicians, and app growth specialists. Insights focus on ARPU drivers, churn dynamics, reimbursement linkage, and enterprise procurement criteria.

Step 4: Research Synthesis and Final Output

Findings are synthesized using triangulation (top-down market totals plus bottom-up company and program signals). Outputs are stress-tested for consistency across segments, platforms, and buyer channels, then finalized with clear definitions, limitations, and decision-useful benchmarks.

- Executive Summary

- Research Methodology (Market Definitions and Inclusion/Exclusion, App Taxonomy Framework, Assumptions and Limitations, Data Triangulation Logic, Bottom-Up Sizing Using App Store and Public Financials, Top-Down Sizing Using Digital Health Spend Proxies, Primary Interview Coverage with Payers Providers Employers Developers, Validation and Error Checks, Abbreviations)

- Definition and Scope

- Market Genesis and Evolution

- Business Cycle and Seasonality

- Ecosystem Mapping

- Value Chain and Data Flow

- Growth Drivers

Employer Benefit Digitization

Payer Preventive Health Push

Rising Mental Health Demand

Wearable Device Penetration

AI-Based Coaching Adoption - Challenges

Consumer Trust Deficit

Data Privacy and Security Scrutiny

High User Churn

Category Saturation - Opportunities

EHR-Embedded Health Apps

AI Triage and Care Navigation

Women’s Health Care Journeys

GLP-1 Companion Ecosystems

Medicaid-Adjacent Digital Health Programs - Trends

Outcomes-Based Contracting

Hybrid Virtual and In-Person Care Models

On-Device AI Personalization

Community and Group Coaching Models

Deep Clinical Workflow Integration - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Downloads and Installs, 2019–2024

- By Active Users, 2019–2024

- By Subscription versus B2B Contract Revenue, 2019–2024

- By Average Revenue per User, 2019–2024

- By Clinical and Use-Case Category (in Value %)

Mental Health

Fitness and Nutrition

Women’s Health

Chronic Condition Management

Medication Adherence - By Buyer and Revenue Model (in Value %)

B2C Subscription

Freemium with In-App Purchases

Advertising and Data Monetization

Employer-Sponsored

Payer-Sponsored - By User Cohort (in Value %)

Healthy Lifestyle Users

At-Risk Users

Diagnosed Chronic Users

Post-Acute and Recovery Users

Caregivers - By Delivery Modality (in Value %)

Self-Guided

Coach-Led

Clinician-Led

Hybrid Care Team

Community-Based - By Platform and Device Pairing (in Value %)

iOS

Android

Cross-Platform

Smartphone-Only

Wearable-Linked - By Integration Level (in Value %)

Standalone

Claims and Eligibility Linked

EHR Connected

Remote Patient Monitoring Workflow Connected

eRx and Lab Connected - By Regulatory Classification (in Value %)

General Wellness Apps

HIPAA-Adjacent Consumer Apps

FDA-Regulated Software Functions

Digital Therapeutics Programs - By Acquisition Channel (in Value %)

App Store Search

Paid User Acquisition

Influencer and Affiliate Marketing

Employer Benefits Marketplaces

Health Plan Portals

- Market Share Assessment

Competitive Positioning Matrix - Cross Comparison Parameters (MAU and DAU Scale and Growth Velocity, Monetization Mix, Retention and Churn Controls, Clinical Evidence and Outcomes Reporting Depth, Regulatory Readiness and Compliance Exposure, Interoperability and EHR Integration Depth, Employer and Payer Contract Footprint, AI Personalization Stack and Governance)

- SWOT Analysis of Major Players

- Detailed Profiles of Major Companies

MyFitnessPal

Headspace

Calm

Noom

Omada Health

Teladoc Health

Amwell

Talkspace

BetterHelp

Fitbit

Apple Health

Google Fit

Flo Health

K Health

- Consumer Adoption and Willingness to Pay

- Employer Procurement and ROI Expectations

- Payer Contracting and Cost Offset Logic

- Provider Workflow and Referral Dynamics

- Pharmacy and Device OEM Distribution Roles

- By Value, 2025–2030

- By Downloads and Installs, 2025–2030

- By Active Users, 2025–2030

- By Subscription versus B2B Contract Revenue, 2025–2030

- By Average Revenue per User, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now