Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA Home Finance Market reflects outstanding residential mortgage debt of approximately USD ~ trillion, as reported by the Federal Reserve’s Financial Accounts of the United States. The market is driven by strong household formation, refinancing activity, government-backed mortgage programs, and deep secondary markets supported by Fannie Mae and Freddie Mac, which provide liquidity and stability to primary lenders across fixed-rate and adjustable-rate mortgage structures.

California, Texas, Florida, and New York remain dominant housing finance markets due to high property values, population concentration, and elevated transaction volumes. Metropolitan regions such as Los Angeles, Houston, Miami, and New York City generate significant mortgage origination activity driven by employment growth and urban demand. Strong capital market infrastructure and nationwide digital lending platforms reinforce liquidity, while federal housing agencies sustain affordability and credit accessibility nationwide.

Market Segmentation

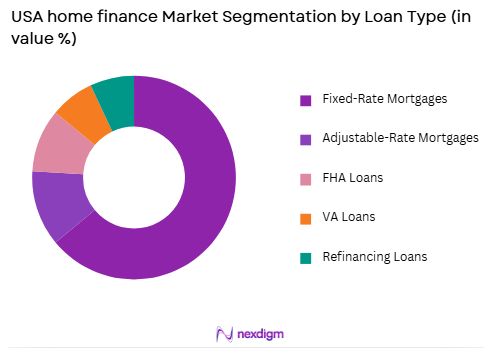

By Loan Type

USA Home Finance Market market is segmented by loan type into Fixed-Rate Mortgages, Adjustable-Rate Mortgages, FHA Loans, VA Loans, and Refinancing Loans. Recently, Fixed-Rate Mortgages have a dominant market share due to factors such as borrower preference for long-term payment stability, strong securitization support through government-sponsored enterprises, predictable amortization schedules, and widespread lender offerings supported by deep secondary mortgage markets and investor demand for mortgage-backed securities.

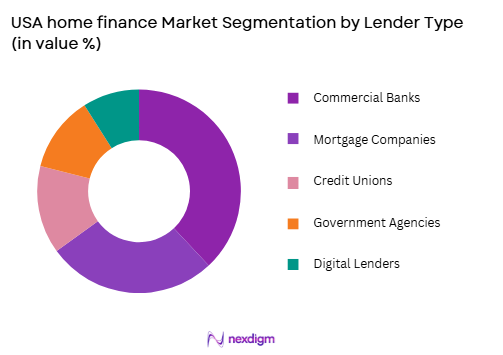

By Lender Type

USA Home Finance Market market is segmented by lender type into Commercial Banks, Mortgage Companies, Credit Unions, Government Agencies, and Digital Lenders. Recently, Commercial Banks have a dominant market share due to factors such as nationwide branch networks, diversified funding sources, established underwriting infrastructure, strong balance sheets, and integration with capital markets that enable large-scale mortgage origination and servicing capabilities across diverse borrower segments.

Competitive Landscape

The USA Home Finance Market demonstrates high institutional participation with strong influence from commercial banks, specialized mortgage lenders, and government-sponsored enterprises. Consolidation has occurred through acquisitions of regional lenders and digital mortgage platforms. Major players compete on interest rates, servicing efficiency, digital application processes, and securitization capacity. Liquidity support from federal housing institutions ensures stability, while private mortgage companies leverage fintech integration for competitive differentiation.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Mortgage Servicing Portfolio (USD) |

| JPMorgan Chase | 1799 | New York, USA | ~ | ~ | ~ | ~ | ~ |

| Bank of America | 1904 | North Carolina, USA | ~ | ~ | ~ | ~ | ~ |

| Wells Fargo | 1852 | California, USA | ~ | ~ | ~ | ~ | ~ |

| Rocket Mortgage | 1985 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| United Wholesale Mortgage | 1986 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

USA Home Finance Market Analysis

Growth Drivers

Government-Backed Mortgage Liquidity and Secondary Market Depth

The structured involvement of government-sponsored enterprises and federal housing agencies provides foundational liquidity to the USA Home Finance Market, enabling lenders to originate mortgages at scale while transferring credit risk through securitization channels. Institutions such as Fannie Mae and Freddie Mac purchase conforming loans, creating a liquid secondary market that supports stable mortgage rates and broad credit availability. The availability of mortgage-backed securities attracts institutional investors seeking stable fixed-income instruments. Federal Housing Administration and Veterans Affairs programs expand credit access to first-time and eligible borrowers. This liquidity infrastructure lowers funding costs for primary lenders and enhances market stability during cyclical fluctuations. The presence of standardized underwriting criteria ensures transparency and consistency across loan origination practices. Strong capital market integration allows mortgage risk distribution across global investors. Policy-driven affordability programs further sustain borrower participation. Servicing platforms ensure structured repayment management across long tenures. Collectively, this government-backed framework strengthens resilience and supports continuous credit flow within the housing finance ecosystem.

Demographic Growth and Residential Property Demand Expansion

Population growth, urban migration patterns, and household formation trends continue to sustain long-term demand for residential housing finance across the United States. Expanding suburban development and metropolitan housing demand increase mortgage origination volumes in high-growth states. Employment growth in technology, healthcare, and services sectors supports borrower income stability and creditworthiness. Millennials transitioning into peak homebuying years contribute significantly to purchase mortgage demand. Refinancing cycles also respond to interest rate movements and home equity accumulation. Rising home equity levels provide opportunities for cash-out refinancing products. Institutional investors’ participation in residential real estate supports transaction liquidity. Construction activity and housing supply dynamics influence financing volumes across regional markets. Digital mortgage applications streamline borrower onboarding and approval timelines. These demographic and structural drivers collectively reinforce sustained expansion in mortgage credit demand nationwide.

Market Challenges

Interest Rate Volatility and Affordability Pressures

Fluctuations in benchmark interest rates directly influence mortgage pricing, borrower qualification thresholds, and refinancing incentives within the USA Home Finance Market. Rising rates increase monthly payment obligations and reduce purchasing power for prospective homebuyers. Elevated home prices in metropolitan regions intensify affordability constraints, particularly for first-time buyers. Lenders must adjust underwriting models to account for debt-to-income sensitivity. Volatile refinancing activity affects origination revenue stability for lenders. Adjustable-rate mortgage products may expose borrowers to payment uncertainty. Investor demand for mortgage-backed securities may shift under changing yield environments. Regional disparities in housing affordability create uneven loan growth patterns. Credit risk assessment becomes more complex during economic slowdowns. These macroeconomic pressures can dampen origination volumes and margin expansion opportunities.

Regulatory Compliance and Capital Adequacy Requirements

The USA Home Finance Market operates within a highly regulated framework involving federal and state supervisory authorities overseeing lending practices and consumer protection standards. Basel III capital requirements influence balance sheet allocation and risk-weighted asset management. Detailed disclosure requirements increase administrative costs for lenders. Servicing standards mandate strict borrower communication protocols. Data privacy and cybersecurity compliance demand continuous system upgrades. Anti-discrimination and fair lending regulations require ongoing monitoring and reporting. Smaller lenders may face disproportionate compliance cost burdens. Stress testing frameworks evaluate resilience under adverse housing scenarios. Documentation requirements extend approval timelines. These regulatory obligations raise operational costs while reinforcing systemic stability.

Opportunities

Expansion of Digital Mortgage Platforms and Automated Underwriting Systems

The integration of digital platforms across mortgage origination and servicing processes presents significant scalability and efficiency opportunities within the USA Home Finance Market. Automated underwriting systems reduce processing time and manual documentation requirements. Online application portals enhance borrower convenience and improve approval transparency. Artificial intelligence-based credit scoring models refine risk assessment precision. Electronic closing processes reduce transaction friction. Data analytics enable personalized mortgage product recommendations. Cloud-based infrastructure improves operational scalability. Cybersecurity enhancements strengthen consumer trust in digital channels. Partnerships between traditional banks and fintech firms accelerate innovation cycles. Cost efficiencies derived from automation support competitive interest pricing strategies. These technological advancements create long-term structural growth potential in mortgage origination and servicing.

Growth in Green and Energy-Efficient Housing Finance Programs

Increasing policy emphasis on sustainability and energy efficiency creates opportunities for specialized mortgage products supporting environmentally responsible housing investments. Green mortgage programs offer preferential terms for energy-efficient construction and renovation. Federal incentives encourage adoption of renewable energy systems within residential properties. Lenders can structure sustainability-linked mortgage products aligned with environmental standards. Investors demonstrate rising interest in green mortgage-backed securities. Energy-efficient housing enhances long-term property value resilience. Digital energy performance certification systems facilitate verification processes. Public-private partnerships expand access to climate-aligned housing finance. Borrower awareness of sustainability benefits supports product uptake. This alignment between housing finance and environmental policy objectives presents a scalable opportunity for long-term market expansion.

Future Outlook

Over the next five years, the USA Home Finance Market is expected to maintain structural resilience supported by government-backed securitization frameworks and steady housing demand. Digital mortgage platforms will continue to enhance operational efficiency and borrower accessibility. Green housing initiatives are likely to gain further institutional backing. Interest rate cycles and regulatory oversight will shape origination volumes, while demographic trends sustain long-term credit demand across metropolitan and suburban regions.

Major Players

- JPMorgan Chase

- Bank of America

- Wells Fargo

- Rocket Mortgage

- United Wholesale Mortgage

- CitiMortgage

- PNC Bank

- Truist Financial

- U.S. Bank

- Flagstar Bank

- LoanDepot

- Guild Mortgage

- Navy Federal Credit Union

- Freedom Mortgage

- Mr. Cooper

Key Target Audience

- Commercial banks

- Mortgage lenders

- Housing finance companies

- Credit unions

- Institutional investors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Real estate developers

Research Methodology

Step 1: Identification of Key Variables

Key variables including outstanding mortgage debt, lender categories, loan structures, securitization volumes, and regulatory parameters were identified through Federal Reserve publications and housing finance disclosures. Macroeconomic and demographic housing indicators were integrated into the analytical scope.

Step 2: Market Analysis and Construction

Market sizing was constructed using official mortgage debt statistics and financial institution reports. Segmentation was developed by mapping loan types and lender structures within the U.S. housing finance ecosystem.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultations with mortgage analysts, banking professionals, and regulatory experts. Cross-verification ensured consistency with publicly disclosed servicing portfolios and federal supervisory data.

Step 4: Research Synthesis and Final Output

Quantitative data and qualitative insights were consolidated into a structured analytical framework. Final outputs were reviewed for factual accuracy, regulatory alignment, and logical coherence prior to publication.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Housing Market Demand and Demographic Expansion

Digital Mortgage Origination and Automation

Government Backed Loan Programs Supporting Homeownership - Market Challenges

Interest Rate Volatility and Affordability Constraints

Stringent Underwriting Standards

Housing Supply Shortages in Key Urban Areas - Market Opportunities

Expansion of Green and Energy Efficient Mortgage Products

AI Driven Credit Assessment and Risk Analytics

Growth in Non Bank Digital Mortgage Lenders - Trends

End to End Digital Mortgage Processing

Rising Popularity of Hybrid Adjustable Rate Products - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Fixed Rate Mortgage Loans

Adjustable Rate Mortgage Loans

FHA and VA Loans

Home Equity Lines of Credit

Jumbo Mortgage Loans - By Platform Type (In Value%)

Traditional Bank Lending

Credit Union Lending

Non Bank Mortgage Lenders

Online Mortgage Platforms

Mortgage Broker Networks - By Fitment Type (In Value%)

Purchase Financing

Refinancing Solutions

Cash Out Refinancing

Home Improvement Financing - By End User Segment (In Value%)

First Time Home Buyers

Repeat Home Buyers

Real Estate Investors

Self Employed Borrowers

- Market Share Analysis

- Cross Comparison Parameters (Processing Turnaround Time, Digital Application and eClosing Capability, Prepayment Penalty Terms, Government Loan Eligibility, Credit Score Requirements, Origination Fees and Closing Costs, Customer Service Channels)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Wells Fargo Home Mortgage

Rocket Mortgage

Bank of America Home Loans

Chase Home Lending

U S Bank Home Mortgage

PNC Bank Mortgage

CitiMortgage

loanDepot

Guild Mortgage

Freedom Mortgage

Caliber Home Loans

Flagstar Bank

Guaranteed Rate

Mr Cooper Group

AmeriHome Mortgage

- Increased Demand for Flexible Loan Tenures

- Preference for Online Pre Approval and Instant Rate Quotes

- Growing Use of Home Equity for Debt Consolidation

- Higher Credit Scrutiny for Self Employed Applicants

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now