Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA HVAC Systems market reached approximately USD ~ billion based on a recent historical assessment, driven by strong residential replacement demand, commercial building upgrades, and large-scale electrification of heating technologies. Federal efficiency standards and incentives accelerated adoption of heat pumps and high-efficiency air conditioning units, while growth in data centers and healthcare facilities expanded demand for precision climate control systems. Supply chain normalization supported installation volumes across residential and commercial construction activity nationwide.

Dominance in the USA HVAC Systems market is concentrated in states such as Texas, California, Florida, and New York due to large building stock, extreme climate conditions, and high construction spending. Major metropolitan regions including Houston, Los Angeles, Miami, and New York City lead installations because of dense residential and commercial infrastructure requiring year-round climate control. Strong regulatory enforcement of energy codes and electrification mandates in coastal states further strengthens regional HVAC equipment demand.

Market Segmentation

By Product Type

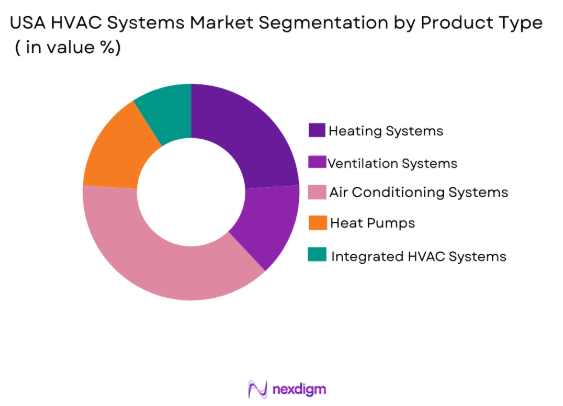

USA HVAC Systems market is segmented by product type into heating systems, ventilation systems, air conditioning systems, heat pumps, and integrated HVAC systems. Recently, air conditioning systems has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Extensive cooling requirements across hot and humid states, widespread installed base in residential and commercial buildings, and replacement cycles driven by efficiency upgrades sustain strong sales volumes. Established distribution networks and contractor familiarity further reinforce air conditioning system dominance across new construction and retrofit projects.

By Platform Type

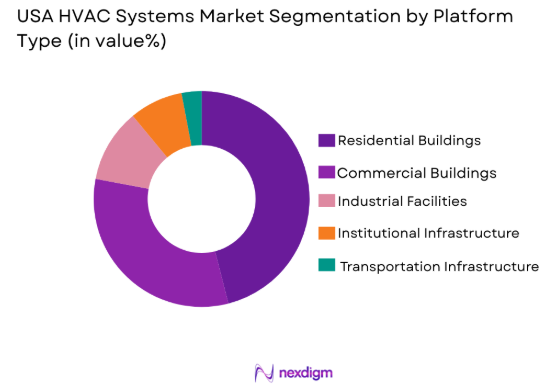

USA HVAC Systems market is segmented by platform type into residential buildings, commercial buildings, industrial facilities, institutional infrastructure, and transportation infrastructure. Recently, residential buildings has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Large housing stock, high replacement frequency of home HVAC units, and strong single-family construction activity drive equipment demand. Consumer comfort expectations and energy efficiency incentives accelerate adoption of modern systems, ensuring residential segment leadership across national HVAC installations.

Competitive Landscape

The USA HVAC Systems market is moderately consolidated, with major multinational manufacturers controlling technology innovation, distribution networks, and brand recognition across residential and commercial segments. Leading firms maintain competitive advantage through vertically integrated manufacturing, contractor partnerships, and advanced heat pump and smart control technologies. Regional OEMs and private-label brands compete in price-sensitive residential markets, while large players dominate commercial and institutional HVAC projects requiring engineering capability and service networks.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Heat Pump Portfolio Strength |

| Carrier Global Corporation | 1915 | USA | ~ | ~ | ~ | ~ | ~ |

| Trane Technologies plc | 1913 | Ireland/USA | ~ | ~ | ~ | ~ | ~ |

| Daikin Industries Ltd | 1924 | Japan | ~ | ~ | ~ | ~ | ~ |

| Lennox International Inc | 1895 | USA | ~ | ~ | ~ | ~ | ~ |

| Johnson Controls International | 1885 | Ireland/USA | ~ | ~ | ~ | ~ | ~ |

USA HVAC Systems Market Analysis

Growth Drivers

Energy Efficiency Regulations and Electrification Policies

Federal appliance efficiency standards and state-level building energy codes have significantly accelerated the transition toward high-efficiency HVAC systems and electric heat pumps across the USA HVAC Systems market. Regulatory frameworks increasingly restrict low-efficiency equipment while incentivizing adoption of advanced air conditioning and heating technologies that reduce energy consumption and carbon emissions in residential and commercial buildings. Electrification mandates in several states encourage replacement of fossil-fuel heating systems with electric heat pumps, expanding equipment demand across retrofit and new construction segments. Financial incentives including tax credits, rebates, and utility programs reduce upfront costs and stimulate consumer adoption of high-efficiency HVAC units, particularly in residential markets. Commercial building owners respond to decarbonization targets and ESG commitments by upgrading HVAC infrastructure to energy-efficient and low-emission technologies. Data centers and institutional facilities adopt precision cooling systems meeting stringent efficiency and reliability requirements. Manufacturers expand product portfolios aligned with regulatory thresholds, strengthening innovation and market competition. Compliance enforcement ensures consistent replacement cycles and technology upgrades nationwide. These policy-driven factors collectively sustain long-term growth momentum in the USA HVAC Systems market.

Rising Construction and Building Retrofit Activity

Expanding residential construction, commercial real estate development, and renovation of aging building stock are major structural drivers of HVAC equipment demand across the USA HVAC Systems market. Housing growth in high-population states and suburban expansion increases installation of central air conditioning and heating systems in new homes. Commercial office, retail, healthcare, and hospitality infrastructure projects require large-scale HVAC installations with advanced ventilation and climate control capabilities. Aging HVAC equipment in existing buildings generates strong replacement demand as systems reach end-of-life or fail to meet updated efficiency standards. Retrofit programs targeting energy savings and indoor air quality improvements further stimulate equipment upgrades in schools, hospitals, and government facilities. Urban redevelopment and mixed-use construction increase demand for centralized and packaged HVAC solutions. Industrial facility expansion and warehouse construction linked to e-commerce logistics also contribute to climate control equipment adoption. Contractors and distributors benefit from consistent project pipelines across regions. Building modernization initiatives sustain long-term HVAC replacement cycles nationwide.

Market Challenges

High Installation and Lifecycle Costs of Advanced HVAC Systems

Advanced HVAC technologies including heat pumps, variable refrigerant flow systems, and smart climate control platforms involve high equipment and installation costs that can limit adoption across price-sensitive residential and small commercial segments in the USA HVAC Systems market. Upfront capital expenditure for high-efficiency systems remains significantly higher than conventional HVAC equipment, discouraging replacement despite long-term energy savings. Complex installation requirements and specialized labor increase total project cost, particularly in retrofit applications within existing buildings. Maintenance and servicing expenses for advanced HVAC technologies can also exceed those of traditional systems, influencing lifecycle cost considerations. Limited contractor expertise in emerging technologies such as VRF or cold-climate heat pumps creates additional installation risk and cost variability. Financing barriers and homeowner budget constraints reduce adoption rates in certain regions. Small businesses face capital limitations for HVAC modernization projects. Economic uncertainty and interest rate fluctuations further constrain investment decisions. These cost-related factors collectively slow penetration of advanced HVAC systems despite regulatory and efficiency incentives.

Skilled Workforce Shortage in HVAC Installation and Service

The USA HVAC Systems market faces a persistent shortage of trained technicians capable of installing, commissioning, and servicing modern HVAC equipment, particularly advanced heat pumps and digitally integrated systems. Aging workforce demographics and insufficient vocational training pipelines reduce availability of qualified labor across regions. Increasing complexity of HVAC technologies requires specialized certification and technical expertise, extending training time and limiting workforce scalability. Contractor capacity constraints delay installation projects and maintenance services, affecting equipment adoption and customer satisfaction. Labor shortages also elevate installation costs, further increasing total system ownership expense for end users. Seasonal demand peaks during extreme weather exacerbate service backlogs and workforce strain. Manufacturers and distributors depend on contractor networks whose limited capacity restricts market expansion. Training initiatives and apprenticeship programs have yet to meet industry demand. Workforce constraints remain a structural barrier to HVAC system deployment nationwide.

Opportunities

Heat Pump Adoption in Cold-Climate Regions: Heat Pump Adoption in Cold-Climate Regions

Advances in cold-climate heat pump technology present a major growth opportunity for the USA HVAC Systems market as electrification policies expand beyond traditionally warm states into northern regions. Modern variable-speed compressors and improved refrigerants enable efficient heating performance at low outdoor temperatures, making heat pumps viable replacements for gas furnaces in colder climates. Federal incentives and state electrification programs promote adoption of heat pumps for residential and commercial heating decarbonization. Replacement of aging furnace systems in northern housing stock creates a large addressable retrofit market. Utilities support electrification through rebates and grid modernization investments. Manufacturers expand cold-climate product lines targeting northern states. Contractor training programs increase installation capability for advanced heat pumps. Consumer awareness of energy savings and emissions reduction continues to grow. These factors collectively position cold-climate heat pumps as a transformative opportunity in HVAC electrification.

Integration of HVAC with Smart Building and IoT Platforms

Digitalization of building infrastructure creates significant opportunity for HVAC manufacturers and service providers in the USA HVAC Systems market through integration with smart controls, sensors, and building management systems. Connected HVAC equipment enables real-time monitoring, predictive maintenance, and energy optimization across residential and commercial environments. Smart thermostats and cloud-based HVAC analytics improve system efficiency and occupant comfort while reducing operational costs. Commercial building owners adopt integrated HVAC platforms to meet energy performance and sustainability targets. Data-driven HVAC operation enhances demand response participation and grid efficiency. Manufacturers develop IoT-enabled equipment and service ecosystems generating recurring revenue streams. Facility managers leverage analytics to optimize ventilation and indoor air quality. Integration with broader smart building infrastructure strengthens value proposition of advanced HVAC systems. Digital HVAC ecosystems represent a major long-term growth pathway.

Future Outlook

The USA HVAC Systems market is expected to maintain steady growth driven by electrification of heating, expansion of high-efficiency cooling technologies, and increasing regulatory pressure on building energy performance. Heat pump adoption will accelerate across residential and commercial retrofits, while smart HVAC integration will reshape system design and operation. Federal incentives and state energy codes will continue supporting upgrades of aging building HVAC infrastructure. Demand from data centers, healthcare facilities, and climate-controlled logistics will further strengthen advanced HVAC deployment nationwide.

Major Players

- Carrier Global Corporation

- Trane Technologies plc

- Daikin Industries Ltd

- Lennox International Inc

- Johnson Controls International

- Rheem Manufacturing Company

- Mitsubishi Electric Corporation

- BoschThermotechnology Corp

- Goodman Manufacturing Company

- AAON Inc

- Nortek Global HVAC LLC

- Modine Manufacturing Company

- Emerson Electric Co

- Ingersoll Rand Inc

- GreeElectric Appliances Inc

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- HVAC equipment manufacturers

- Building developers and contractors

- Commercial real estate owners

- Industrial facility operators

- Facility management companies

- Energy service companies

Research Methodology

Step 1: Identification of Key Variables

Key market variables including HVAC system types, building platforms, regulatory drivers, and technology adoption factors were identified through secondary industry literature and policy databases. Demand indicators such as construction activity, retrofit rates, and electrification incentives were mapped to quantify HVAC installation drivers across segments.

Step 2: Market Analysis and Construction

Market size estimation combined equipment shipment data, construction statistics, and replacement cycle modeling across residential and commercial buildings. Segmentation shares were derived using industry sales distribution, contractor insights, and product mix analysis across HVAC technologies.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary market assumptions were validated through consultations with HVAC manufacturers, distributors, and installation contractors to confirm adoption trends, pricing ranges, and regional demand patterns. Regulatory and technology forecasts were cross-checked with policy experts and industry analysts.

Step 4: Research Synthesis and Final Output

Validated datasets and expert insights were synthesized into final market estimates, segmentation structures, and competitive analysis. Forecast modeling incorporated regulatory trajectories, technology penetration curves, and construction outlook to produce coherent market projections.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Stringent building energy efficiency standards and decarbonization mandates

Rising construction of residential and commercial infrastructure

Electrification of heating through heat pump adoption

Growing demand for indoor air quality and ventilation upgrades

Expansion of data centers and climate-controlled industrial facilities - Market Challenges

High upfront cost of advanced HVAC and heat pump systems

Skilled workforce shortages in HVAC installation and servicing

Supply chain volatility in compressors and electronic components

Energy price fluctuations impacting operating cost perceptions

Complex retrofitting in aging building stock

- Market Opportunities

Large-scale electrification of heating in cold-climate regions

Integration of HVAC with smart building management platforms

Federal and state incentives for high-efficiency HVAC upgrades

- Trends

Rapid penetration of variable refrigerant flow systems

Shift toward low-GWP refrigerants and refrigerant transition

Adoption of connected and sensor-based HVAC controls

Growth of packaged rooftop units with high efficiency ratings

Hybrid HVAC systems combining heat pumps and furnaces - Government Regulations & Defense Policy

Federal minimum energy performance standards for HVAC equipment

State-level building energy codes and electrification mandates

Refrigerant phase-down regulations under environmental policy

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Heating Systems

Ventilation Systems

Air Conditioning Systems

Integrated HVAC Systems

Air Purification and Filtration Systems - By Platform Type (In Value%)

Residential Buildings

Commercial Buildings

Industrial Facilities

Institutional Infrastructure

Transportation and Mobility Infrastructure - By Fitment Type (In Value%)

New Installation Systems

Retrofit and Replacement Systems

Modular HVAC Units

Packaged HVAC Systems

Centralized HVAC Plants

- By End User Segment (In Value%)

Homeowners and Residential Developers

Commercial Real Estate Owners

Industrial Manufacturing Operators

Healthcare and Institutional Facilities

Government and Public Infrastructure Authorities - By Procurement Channel (In Value%)

Direct OEM Procurement

HVAC Contractors and Installers

Engineering Procurement Construction Firms

Facility Management Providers

Distribution and Wholesale Networks - By Material / Technology (in Value %)

Variable Refrigerant Flow Technology

Inverter and Smart Compressor Technology

Advanced Heat Pump Technology

Energy Recovery Ventilation Technology

Smart Thermostat and IoT Control Systems

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (System Efficiency Rating, Product Portfolio Breadth, Heat Pump Capability, Smart Control Integration, Distribution Network Strength)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Carrier Global Corporation

Trane Technologies plc

Johnson Controls International plc

Daikin Industries Ltd

Lennox International Inc

Rheem Manufacturing Company

Nortek Global HVAC LLC

Mitsubishi Electric Corporation

Bosch Thermotechnology Corp

Goodman Manufacturing Company

AAON Inc

Modine Manufacturing Company

Emerson Electric Co

Ingersoll Rand Inc

Gree Electric Appliances Inc

- Residential sector prioritizing energy efficiency and electrified heating

- Commercial buildings demanding smart climate control and IAQ compliance

- Industrial facilities requiring process cooling and ventilation reliability

- Public infrastructure upgrading HVAC for decarbonization targets

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now