Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Infotainment Chips market current size stands at around USD ~ million, reflecting sustained integration of digital cockpit processors, connectivity chipsets, and audio-visual SoCs across new vehicle platforms. Demand is shaped by the transition toward software-defined vehicles, higher compute requirements for multi-display HMI, and tighter functional safety expectations. Supply chains are increasingly localized through North American assembly and test partnerships, while design-in cycles align with multi-year vehicle platform roadmaps.

Adoption is concentrated in automotive manufacturing hubs across Michigan, California, Texas, and the Southeast, supported by dense clusters of OEM engineering centers, Tier 1 integration facilities, and semiconductor design teams. Strong demand originates from coastal technology ecosystems driving software-defined vehicle development, while Midwest manufacturing capacity anchors hardware integration. Policy support for advanced manufacturing, cybersecurity compliance requirements, and vehicle safety standards reinforce ecosystem maturity and long-term supplier engagement.

Market Segmentation

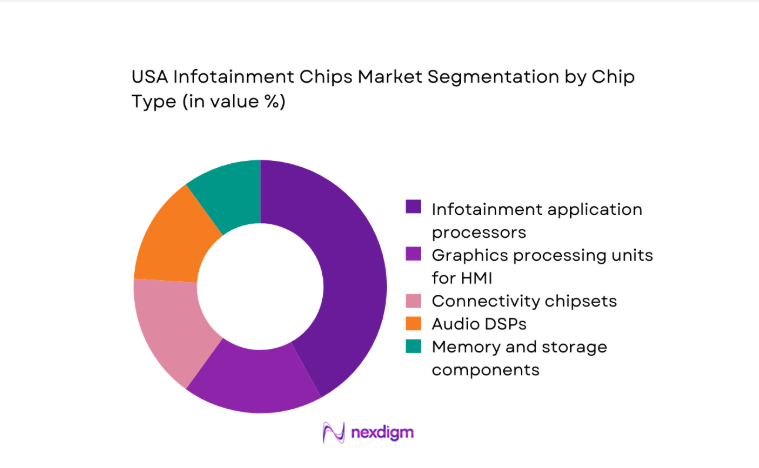

By Chip Type

Infotainment application processors dominate procurement due to their central role in digital cockpit consolidation, enabling multi-display rendering, AI-based voice interfaces, and embedded OS support. OEM platform strategies increasingly favor integrated SoCs that combine CPU, GPU, NPU, and connectivity, reducing wiring complexity and latency across vehicle domains. Memory and storage components maintain steady uptake as infotainment stacks scale in content and over-the-air update capabilities. Audio DSPs retain relevance in premium trims emphasizing immersive sound experiences. Connectivity chipsets gain traction alongside embedded cellular and vehicle-to-cloud integration requirements, reinforcing end-to-end infotainment performance and lifecycle software support.

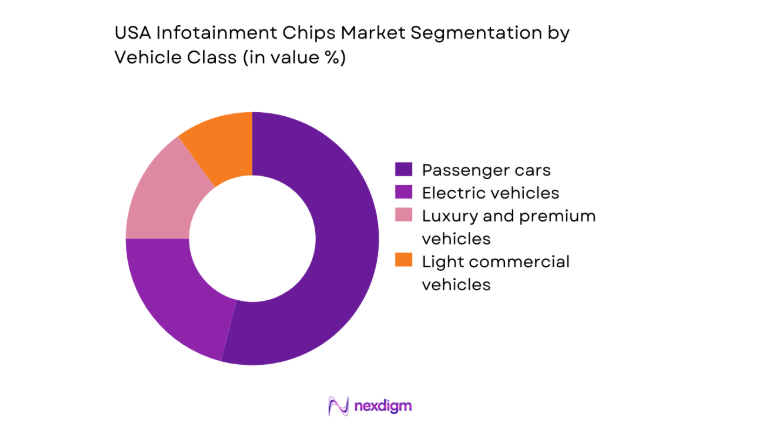

By Vehicle Class

Passenger cars account for the largest share of infotainment chip demand due to higher production volumes and rapid feature adoption across mid-range trims. Electric vehicles demonstrate faster feature density growth, driven by centralized compute architectures and software-centric user experiences. Luxury and premium vehicles sustain early adoption of advanced HMI, multi-screen cockpits, and AI assistants, setting benchmarks that cascade into mass-market platforms. Light commercial vehicles increasingly integrate infotainment for fleet management and driver assistance, supporting connectivity, navigation, and compliance use cases that elevate baseline compute requirements across commercial fleets.

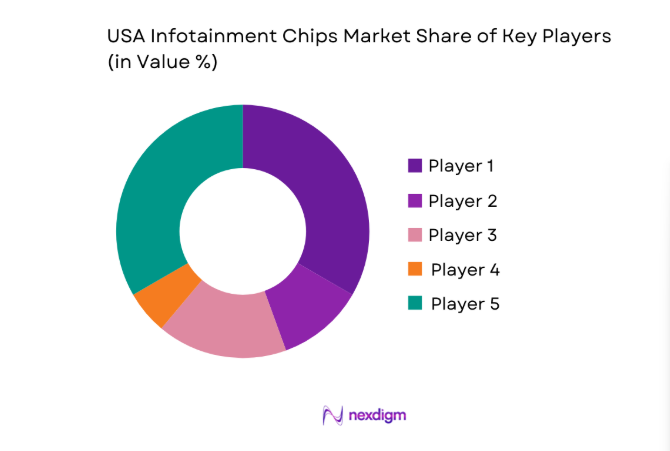

Competitive Landscape

The competitive environment is shaped by deep automotive-grade qualification, long design-in cycles, and close co-development with OEM and Tier 1 partners. Differentiation centers on compute performance, software ecosystem compatibility, power efficiency, and long-term supply assurance aligned with vehicle platform lifecycles.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Qualcomm | 1985 | San Diego, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | Dallas, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| NXP Semiconductors | 2006 | Eindhoven, Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| Renesas Electronics | 2010 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

USA Infotainment Chips Market Analysis

Growth Drivers

Rising consumer demand for connected car features

Consumer expectations for seamless in-vehicle connectivity intensified as 2023 registrations of connected-capable vehicles reached 14,200,000 units across national registrations, supported by 5,600 public charging corridors and 68 certified digital services platforms integrated by OEMs. Smartphone mirroring sessions exceeded 9,800,000 monthly activations in fleet telemetry, while embedded cellular subscriptions expanded across 4,300 dealer networks enabling persistent infotainment services. Federal spectrum allocations in 2024 enabled additional low-latency bands for vehicular connectivity, reinforcing richer streaming use cases. Urban commuting averages of 52 minutes daily increased reliance on navigation, media, and voice assistants, elevating compute requirements within infotainment chip architectures.

Expansion of digital cockpits and multi-display HMI

Multi-display cockpit adoption accelerated as 2024 model platforms integrated up to 3 concurrent displays across 112 vehicle nameplates, driving higher pixel throughput and GPU utilization. OEM platform roadmaps consolidated instrument clusters and center stacks into unified compute domains, reducing discrete controllers from 5 to 2 per vehicle architecture. Federal vehicle safety guidance published in 2023 clarified driver distraction thresholds across 6 interface categories, incentivizing higher frame stability and deterministic latency. Manufacturing plants commissioned 27 new HMI validation rigs to certify display pipelines, while software update cadence averaged 8 releases annually, increasing sustained processing loads on infotainment SoCs.

Challenges

Automotive-grade semiconductor supply constraints

Supply constraints persisted through 2023 as automotive-grade node capacity below 16 nanometers remained allocated across defense, industrial automation, and consumer electronics programs, limiting available wafer starts to 420,000 monthly equivalents for automotive qualification lines. Qualification cycles averaged 18 months, constraining rapid ramp-up for new infotainment SoCs. Logistics disruptions affected 34 port entry points, extending inbound component lead times by 21 days during peak quarters. Regulatory documentation updates across 9 compliance standards required recertification for minor die revisions, slowing deployment of revised chipsets across 64 vehicle programs scheduled for refresh cycles.

Cybersecurity and functional safety compliance costs

Cybersecurity mandates expanded across 2024, introducing 12 additional compliance controls for in-vehicle networks and infotainment gateways, increasing validation workloads across 41 accredited labs. Functional safety certification under automotive standards required 2 parallel safety cases per SoC revision, extending verification timelines by 26 weeks. Incident reporting protocols recorded 1,740 disclosed vehicle software vulnerabilities in 2023, elevating scrutiny on secure boot, hardware roots of trust, and isolation. OEM governance committees mandated quarterly penetration testing cycles across 19 vehicle platforms, intensifying engineering overhead and slowing infotainment chipset design iterations.

Opportunities

5G-enabled infotainment and low-latency streaming

5G network coverage expanded to 315 metropolitan areas by 2024, enabling sustained low-latency media delivery and cloud-assisted rendering for in-vehicle systems. Average round-trip latency measured 18 milliseconds across certified corridors, supporting interactive navigation and real-time content synchronization. Transportation agencies approved 47 connected corridor pilots integrating roadside units with vehicle modems, creating demand for higher-throughput baseband integration within infotainment SoCs. Vehicle firmware stacks incorporated edge offloading across 22 application modules, enabling compute partitioning between cloud nodes and onboard processors. These conditions create platform opportunities for tightly integrated modem-processor architectures optimized for sustained streaming workloads.

AI-driven voice assistants and personalization

In-vehicle voice interaction sessions surpassed 6,900,000 daily activations across registered fleets in 2023, reflecting rising reliance on natural language interfaces for navigation, media, and vehicle controls. On-device inference benchmarks improved as NPUs delivered 24 TOPS class performance within automotive thermal envelopes, enabling offline speech recognition across 14 supported languages. Regulatory accessibility guidelines issued in 2024 emphasized voice-first interaction for visually demanding tasks, accelerating OEM adoption. Driver profiles synchronized across 3 identity layers, supporting personalized HMI layouts. These shifts expand opportunities for infotainment SoCs embedding dedicated AI accelerators and privacy-preserving on-device processing capabilities.

Future Outlook

The market will continue aligning with software-defined vehicle architectures through 2030, emphasizing centralized compute and longer software support lifecycles. Regulatory focus on cybersecurity and safety will shape qualification roadmaps, while connectivity advancements enable richer in-vehicle services. Partnerships across OEMs, Tier 1 integrators, and software platforms will determine platform success and pace of innovation.

Major Players

- Qualcomm

- NVIDIA

- Texas Instruments

- NXP Semiconductors

- Renesas Electronics

- Intel

- MediaTek

- Samsung Electronics

- STMicroelectronics

- Infineon Technologies

- Broadcom

- Marvell Technology

- Microchip Technology

- Analog Devices

- ON Semiconductor

Key Target Audience

- Automotive OEMs and vehicle platform engineering teams

- Tier 1 automotive electronics suppliers

- Semiconductor design and manufacturing firms

- Automotive software platform providers

- Fleet operators and mobility service providers

- Investments and venture capital firms

- Government and regulatory bodies with agency names including the U.S. Department of Transportation and National Highway Traffic Safety Administration

- Automotive aftermarket system integrators

Research Methodology

Step 1: Identification of Key Variables

Core variables were defined across infotainment compute requirements, connectivity integration levels, functional safety compliance, and software platform compatibility. Demand drivers were mapped to vehicle platform refresh cycles and regulatory milestones. Supply-side constraints were linked to node availability and qualification timelines.

Step 2: Market Analysis and Construction

Platform architectures were analyzed across current vehicle programs to construct demand profiles by chip type and vehicle class. Ecosystem dependencies between OEMs and Tier 1 integrators were assessed. Regulatory and infrastructure conditions were incorporated to reflect deployment feasibility.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on centralized compute migration and connectivity adoption were validated through structured consultations with domain engineers and compliance specialists. Architecture trade-offs were stress-tested against certification pathways and software lifecycle requirements.

Step 4: Research Synthesis and Final Output

Findings were synthesized into coherent narratives linking demand drivers, constraints, and opportunity pathways. Scenario framing aligned platform roadmaps with regulatory timelines and infrastructure readiness. Outputs were refined for decision-grade clarity and strategic relevance.

- Executive Summary

- Research Methodology (Market Definitions and infotainment SoC scope alignment, OEM Tier-1 design win tracking, Automotive-grade semiconductor shipment and ASP triangulation, Vehicle platform teardowns and BOM analysis, Dealer and fleet infotainment feature penetration surveys, Regulatory and safety compliance mapping, Channel inventory and lead-time monitoring)

- Definition and Scope

- Market evolution

- In-vehicle usage pathways

- Automotive infotainment ecosystem structure

- OEM–Tier 1–chip vendor supply chain structure

- Regulatory and safety compliance environment

- Growth Drivers

Rising consumer demand for connected car features

Expansion of digital cockpits and multi-display HMI

Increasing penetration of EVs with software-defined architectures

OEM differentiation through advanced infotainment experiences

Growth of in-vehicle apps and cloud-connected services - Challenges

Automotive-grade semiconductor supply constraints

High qualification and long design-in cycles

Cybersecurity and functional safety compliance costs

Rapid technology obsolescence versus vehicle lifecycles

Pricing pressure from OEM procurement practices - Opportunities

5G-enabled infotainment and low-latency streaming

AI-driven voice assistants and personalization

Integration of infotainment with ADAS and vehicle OS platforms

Aftermarket retrofit solutions for legacy fleets

Partnerships with cloud and content service providers - Trends

Migration toward centralized compute architectures

Adoption of Android Automotive and embedded OS platforms

Consolidation of infotainment and digital cockpit SoCs

Over-the-air update enablement

Shift toward software-defined vehicles - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Chip Type (in Value %)

Infotainment application processors

Graphics processing units for HMI

Connectivity chipsets

Audio DSPs

Memory and storage components - By Vehicle Class (in Value %)

Passenger cars

Light commercial vehicles

Electric vehicles

Luxury and premium vehicles - By Connectivity Feature (in Value %)

Embedded cellular (LTE/5G)

Wi-Fi and Bluetooth modules

GNSS positioning

Vehicle-to-cloud telematics interfaces - By Infotainment Function (in Value %)

Digital cockpit and instrument cluster

Central infotainment head unit

Rear-seat entertainment

Voice and AI assistant processing - By Sales Channel (in Value %)

OEM factory fit

Aftermarket upgrades

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Process node capability, Automotive-grade qualification, SoC performance benchmarks, Connectivity integration level, Software and OS support ecosystem, Power efficiency metrics, Design win footprint with OEMs, Pricing and supply reliability)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Qualcomm

NVIDIA

Texas Instruments

NXP Semiconductors

Renesas Electronics

Intel

MediaTek

Samsung Electronics

STMicroelectronics

Infineon Technologies

Broadcom

Marvell Technology

Microchip Technology

Analog Devices

ON Semiconductor

- Demand and utilization drivers

- Procurement and sourcing dynamics

- Buying criteria and vendor selection

- Budget allocation and cost optimization preferences

- Implementation barriers and risk factors

- Post-purchase service and support expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now