Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA instrument clusters market is valued at approximately USD ~ billion based on a recent historical assessment, driven by increasing integration of digital cockpit systems across passenger and commercial vehicles. The market expansion is supported by rising production of connected vehicles exceeding USD ~ billion in automotive manufacturing output and strong demand for advanced driver information displays. Federal vehicle safety mandates and growing electric vehicle shipments exceeding USD ~ billion further reinforce adoption of high-resolution and configurable instrument cluster technologies.

Detroit, California, Texas, and the Midwest manufacturing corridor dominate the USA instrument clusters market due to concentration of automotive OEM headquarters, semiconductor supply ecosystems, and vehicle production infrastructure exceeding USD 300 billion in annual output. California leads innovation through electric vehicle production valued above USD 95 billion and software-defined cockpit development hubs, while Michigan remains central to cluster engineering and integration programs. Southern states support large-scale assembly plants and supplier parks enabling cost-efficient instrument cluster deployment across vehicle platforms.

Market Segmentation

By Product Type

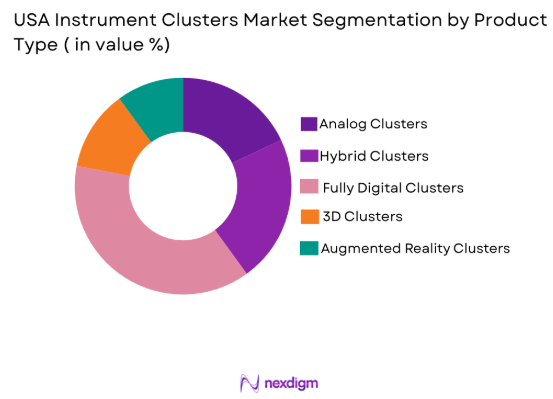

USA instrument clusters market is segmented by product type into analog clusters, hybrid clusters, fully digital clusters, 3D clusters, and augmented reality clusters. Recently, fully digital clusters has a dominant market share due to factors such as consumer demand for customizable displays, OEM transition toward software-defined vehicles, integration with advanced driver assistance systems, and compatibility with electric vehicle architectures. Increasing adoption of large TFT and OLED displays across passenger vehicles and premium commercial vehicles has strengthened production scale and supplier investments supporting digital cluster dominance.

By Platform Type

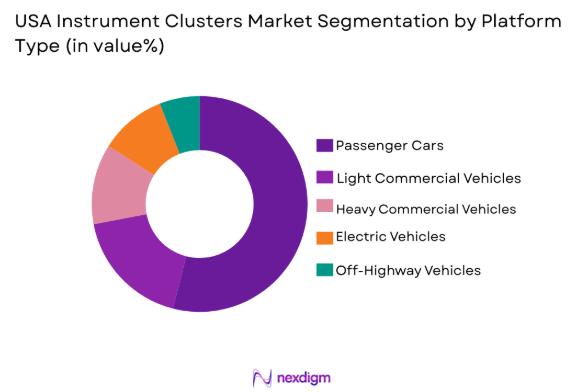

USA instrument clusters market is segmented by platform type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, electric vehicles, and off-highway vehicles. Recently, passenger vehicles has a dominant market share due to factors such as highest production volume, rapid digital cockpit adoption across sedans and SUVs, strong consumer demand for customizable displays, and OEM competition in user interface differentiation. Electrification of passenger vehicles and integration of advanced driver assistance visualization further accelerates deployment of high-resolution and multi-screen instrument clusters across this platform.

Competitive Landscape

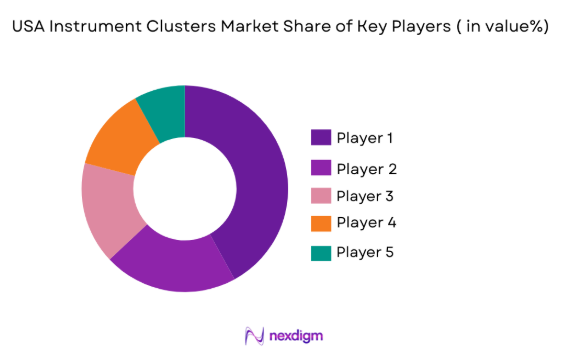

The USA instrument clusters market shows moderate consolidation with automotive electronics suppliers dominating OEM contracts and technology platforms. Major players maintain long-term supply agreements with automotive manufacturers and invest heavily in digital display technologies, software platforms, and cockpit integration capabilities. Competition is shaped by innovation in display resolution, software architecture, and ADAS integration, while scale manufacturing and semiconductor partnerships determine cost competitiveness and market reach across vehicle segments.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Display Technology Specialization |

| Visteon Corporation | 2000 | USA | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Bosch Mobility | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Panasonic Automotive | 1918 | Japan | ~ | ~ | ~ | ~ | ~ |

USA Instrument Clusters Market Analysis

Growth Drivers

Vehicle Digitalization and Software-Defined Cockpit Transformation

The accelerating adoption of advanced instrument clusters across the USA automotive sector as manufacturers shift toward integrated digital interfaces replacing analog gauges. Increasing deployment of connected vehicle platforms requires high-resolution clusters capable of displaying navigation, ADAS alerts, energy management, and driver assistance information in real time across multiple driving modes. Automakers are investing billions of USD in software-centric vehicle architectures that integrate instrument clusters with infotainment and telematics ecosystems, creating unified cockpit experiences. Consumer expectations for personalization, animation, and graphical interfaces have pushed OEMs to replace mechanical clusters with configurable digital displays even in mid-range vehicles. Electric vehicles rely heavily on digital clusters for battery status visualization, range prediction, and energy efficiency indicators, reinforcing demand across EV platforms. Over-the-air update capability in digital clusters allows continuous feature enhancement, extending lifecycle value for manufacturers and users. Regulatory emphasis on driver information clarity and safety warnings further promotes adoption of programmable clusters capable of adaptive display layouts. The convergence of infotainment, ADAS, and cluster computing platforms into centralized cockpit controllers strengthens the role of digital clusters as core human-machine interface components. suppliers are scaling production of large TFT and OLED displays, reducing cost per unit and enabling widespread deployment across vehicle categories. This transformation toward software-defined cockpits positions digital instrument clusters as essential components of next-generation vehicles in the USA market.

Expansion of Electric and Connected Vehicle Production in the USA

The significantly increasing demand for advanced instrument clusters due to the digital information requirements of modern vehicle architectures. Electric vehicle production annually relies on cluster interfaces for energy flow visualization, charging status, regenerative braking feedback, and efficiency analytics unavailable in conventional analog dashboards. Connected vehicles integrate telematics, navigation, and cloud services that require multifunction display interfaces accessible through instrument clusters, expanding their functional scope. Federal incentives and state-level electrification policies have accelerated EV manufacturing capacity across multiple states, increasing installation volumes of digital clusters per vehicle. Autonomous driving development programs also depend on clusters to communicate system status, sensor awareness, and driver takeover alerts, raising technological complexity and value. Commercial fleet electrification programs in logistics and public transport sectors further drive cluster deployment for monitoring vehicle diagnostics and efficiency metrics. Semiconductor and display manufacturing investments in the USA strengthen supply chains for digital cluster components, supporting domestic production scale. Automotive OEM competition in electric vehicle differentiation has shifted focus toward cockpit technology and digital user experience, making clusters central branding elements. Integration of augmented reality navigation and advanced visualization in EVs increases hardware sophistication and revenue per unit for cluster suppliers. The growth trajectory of connected and electric vehicles ensures sustained expansion of the USA instrument clusters market through increased production volumes and technological upgrades.

Market Challenges

High Development Cost and Integration Complexity of Advanced Digital Clusters

presents a major challenge in the USA instrument clusters market due to the extensive hardware, software, and validation requirements associated with modern cockpit systems. Digital clusters require high-performance processors, display panels, graphics engines, and safety-certified operating systems, increasing bill of materials and engineering expenditure compared with analog counterparts. Integration with vehicle networks, ADAS sensors, infotainment platforms, and telematics modules necessitates complex software architectures and long development cycles. Automotive functional safety standards demand rigorous validation, testing, and redundancy mechanisms, significantly raising engineering cost and time to market. Customization requirements across vehicle models force suppliers to design multiple cluster variants, limiting economies of scale and increasing tooling investment. Rapid evolution of display technologies such as OLED and curved panels requires continuous R&D spending to maintain competitiveness. Cybersecurity compliance for connected clusters introduces additional software layers and certification procedures that add to development complexity. Semiconductor shortages and specialized display supply constraints can disrupt production planning and increase component cost volatility. OEM pressure to reduce vehicle cost while enhancing cockpit features compresses supplier margins, challenging profitability. These factors collectively create barriers for new entrants and strain development resources for existing suppliers in the USA instrument clusters ecosystem.

Cybersecurity and Functional Safety Compliance Requirements

pose a critical challenge for the USA instrument clusters market because modern clusters function as connected computing interfaces within vehicle electronic architectures. Digital clusters process sensitive vehicle data, driver inputs, and connectivity signals, making them potential entry points for cyber threats if not secured properly. Regulatory frameworks require compliance with automotive cybersecurity standards and secure software lifecycle management, increasing development cost and certification timelines. Functional safety regulations mandate fail-safe operation of clusters to ensure that driver information remains accurate and visible even during electronic faults. Achieving safety integrity levels requires redundant hardware pathways, watchdog processors, and real-time monitoring software integrated into cluster architecture. Continuous over-the-air updates demand secure communication protocols and authentication mechanisms to prevent malicious interference. OEM liability concerns related to display malfunction or misleading driver information necessitate extensive testing and validation across environmental and operational conditions. Integration of clusters with ADAS and autonomous driving status displays raises safety criticality because incorrect visualization can affect driver decisions. Suppliers must maintain long-term software support and patch management throughout vehicle lifecycles, increasing operational overhead. These stringent cybersecurity and safety requirements significantly increase engineering complexity and cost burden for instrument cluster manufacturers in the USA market.

Opportunities

Integration of Augmented Reality and 3D Visualization in Instrument Clusters

Represents a significant opportunity in the USA instrument clusters market as automotive manufacturers seek immersive driver interfaces that enhance situational awareness and navigation clarity. Augmented reality overlays can display directional cues, hazard alerts, and lane guidance directly within the driver’s line of sight through cluster visualization linked with vehicle sensors and navigation systems. Advances in graphics processors and display optics enable real-time rendering of 3D vehicle surroundings and driving data within digital clusters, increasing perceived value and differentiation. Premium and electric vehicle segments are adopting AR-enabled clusters to support advanced driver assistance and semi-autonomous driving communication requirements. Consumer demand for gaming-like graphical interfaces and interactive cockpit experiences encourages OEM investment in high-performance cluster visualization technologies. Integration with head-up displays and central infotainment screens allows unified AR ecosystems across the cockpit, expanding cluster functionality. Software-defined vehicle architectures enable continuous feature upgrades for AR visualization through updates, extending product lifecycle and revenue potential. Suppliers developing scalable AR cluster platforms can serve multiple vehicle segments, improving production economics. Regulatory emphasis on driver awareness and hazard visualization supports adoption of enhanced display interfaces. The growing convergence of digital entertainment, navigation, and safety visualization positions AR and 3D clusters as next-generation growth avenues in the USA market.

Retrofitting and Aftermarket Upgrades for Digital Instrument Clusters

presents a substantial opportunity in the USA instrument clusters market due to the large installed base of vehicles equipped with analog or basic hybrid dashboards. Vehicle owners increasingly seek digital cockpit upgrades to enhance aesthetics, functionality, and resale value, creating demand for replacement cluster solutions compatible with older vehicle platforms. Fleet operators modernizing vehicles for telematics and efficiency monitoring adopt digital clusters for data visualization and driver interface improvements. Aftermarket suppliers are developing plug-and-play digital cluster kits that integrate with existing vehicle electronics without extensive modification, lowering adoption barriers. Rising availability of software customization and user interface themes increases appeal for personalization in the aftermarket segment. Electric vehicle conversion projects require digital clusters capable of displaying battery and energy metrics absent in legacy dashboards. E-commerce automotive parts platforms expand distribution reach for retrofit clusters across the USA. OEM-approved upgrade programs for premium vehicles create additional channels for digital cluster replacement. Technological advancements reducing display and processor cost enable competitive pricing in the retrofit market. The combination of aesthetic demand, functional upgrades, and aging vehicle fleets establishes retrofitting as a high-growth opportunity within the USA instrument clusters ecosystem.

Future Outlook

The USA instrument clusters market is expected to expand steadily over the next five years driven by increasing digital cockpit adoption across all vehicle segments. Advancements in display technologies, software-defined vehicle architectures, and augmented reality visualization will elevate cluster functionality and value. Electrification and autonomous driving development will further increase demand for advanced driver information interfaces. Regulatory emphasis on safety visualization and cybersecurity will shape technology standards. Growing aftermarket upgrades and retrofit demand will complement OEM installation growth.

Major Player

- Visteon Corporation

- Continental AG

- Denso Corporation

- Bosch Mobility Solutions

- Panasonic Automotive Systems

- AptivPLC

- Magneti Marelli

- Harman International

- Yazaki Corporation

- NipponSeiki

- Valeo SA

- HyundaiMobis

- Alps Alpine

- Garmin Automotive

- Fujitsu Ten

Key Target Audience

- Automotive OEMs

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive electronics suppliers

- Fleet operators

- Vehicle customization companies

- Electric vehicle manufacturers

- Automotive aftermarket distributors

Research Methodology

Step 1: Identification of Key Variables

Key variables including vehicle production, digital cockpit penetration, display technology adoption, and OEM integration strategies were identified. Supply chain factors such as semiconductor availability, display panel manufacturing, and software platform development were also mapped. Regulatory and safety compliance parameters influencing instrument cluster deployment were incorporated.

Step 2: Market Analysis and Construction

The market model was constructed using vehicle production data, cockpit technology penetration rates, and cluster installation value per vehicle. Segment shares were derived from OEM adoption patterns across vehicle types and display technologies. Regional manufacturing and supplier ecosystem data supported market size validation.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions regarding digital cluster penetration, EV adoption impact, and AR integration timelines were validated through consultation with automotive electronics experts and industry specialists. Supplier capability assessments and OEM roadmap analysis confirmed technology trends. Feedback ensured realistic segmentation and competitive positioning.

Step 4: Research Synthesis and Final Output

All validated inputs were synthesized into a structured market framework covering size, segmentation, competition, and growth dynamics. Cross-verification across multiple data points ensured consistency and reliability. Final insights were aligned with automotive digitalization trends and USA manufacturing developments.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising integration of advanced driver assistance and vehicle digitalization

Growing adoption of electric and connected vehicles

Increasing consumer demand for customizable cockpit interfaces

Regulatory push for enhanced driver information visibility

Expansion of autonomous driving display requirements - Market Challenges

High development and integration cost of digital clusters

Complex software validation and cybersecurity requirements

Supply chain constraints in display semiconductors

Compatibility issues across vehicle architectures

Aftermarket standardization limitations - Market Opportunities

Expansion of augmented reality head up integrated clusters

Growth in software defined vehicle cockpit platforms

Retrofitting demand in commercial and fleet vehicles - Trends

Shift toward widescreen and pillar to pillar cockpit displays

Integration of infotainment and cluster interfaces

Increasing use of 3D graphics rendering engines

Personalized driver profiles and UI themes

Over the air updatable cluster software - Government Regulations & Defense Policy

Driver distraction and display visibility standards

Functional safety compliance for automotive electronics

Cybersecurity regulations for connected vehicle systems

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Analog Instrument Clusters

Hybrid Instrument Clusters

Fully Digital Instrument Clusters

3D Instrument Clusters

Augmented Reality Instrument Clusters - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

OffHighway Vehicles - By Fitment Type (In Value%)

OEM Factory Installed

Aftermarket Replacement

Dealer Installed Upgrades

Fleet Retrofit Installations

Performance Custom Installations - By End User Segment (In Value%)

Automotive OEMs

Commercial Fleet Operators

Aftermarket Service Providers

Vehicle Customization Firms

Government and Public Transport Agencies - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier1 Supplier Agreements

Authorized Dealer Networks

Aftermarket Distribution Channels

ECommerce Automotive Platforms - By Material / Technology (in Value %)

TFT LCD Display Technology

OLED Display Technology

LED Backlit Displays

Curved Glass Interfaces

Haptic Feedback Interfaces

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Display Technology, Screen Size Range, Software Platform, Integration Level, Vehicle Segment Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Visteon Corporation

Continental AG

Denso Corporation

Panasonic Automotive Systems

Bosch Mobility Solutions

Aptiv PLC

Magneti Marelli

Harman International

Yazaki Corporation

Nippon Seiki

Valeo SA

Hyundai Mobis

Fujitsu Ten

Alps Alpine

Garmin Automotive

- Automotive OEMs prioritizing digital cockpit differentiation

- Fleet operators adopting digital clusters for telematics integration

- Aftermarket providers targeting cluster upgrades and replacements

- Public transport agencies adopting standardized digital displays

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now