Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Interior Lighting market is valued at approximately USD ~ billion, driven by extensive adoption of LED-based ambient and architectural lighting across automotive, residential, and commercial interiors. Growth is supported by increasing vehicle interior illumination integration, rising smart home lighting installations, and renovation of commercial building lighting systems. Regulatory efficiency standards and declining LED costs are accelerating replacement of legacy interior fixtures, while premium interior design trends are expanding demand for customizable and integrated lighting environments across multiple applications.

Major demand concentration exists in California, Texas, New York, and Florida due to high construction spending, strong automotive ownership, and advanced smart home adoption across metropolitan regions. These states host large residential renovation markets, commercial real estate development, and automotive manufacturing ecosystems that sustain interior lighting deployment. Urban luxury housing and hospitality infrastructure expansion further increase adoption of ambient and decorative lighting systems, reinforcing regional dominance in advanced interior illumination technologies.

Market Segmentation

By Product Type

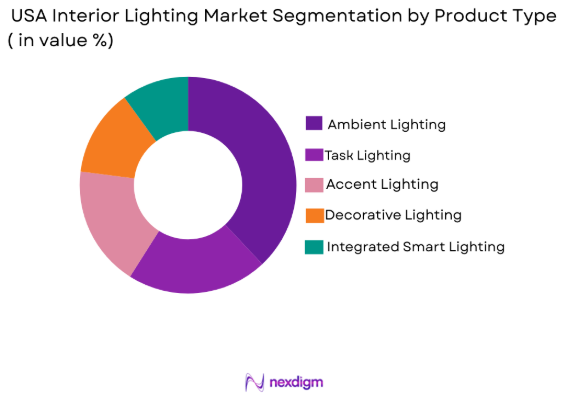

USA Interior Lighting market is segmented by product type into ambient lighting, task lighting, accent lighting, decorative lighting, and integrated smart lighting. Recently, ambient lighting has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Ambient lighting dominates because it forms the foundational illumination layer across automotive cabins, homes, and commercial interiors, enabling uniform light distribution and comfort visibility. Integration with LED strips, diffused panels, and color-tunable modules supports personalization trends in vehicles and smart homes. Large-scale architectural applications including ceilings, panels, and concealed coves rely heavily on ambient systems, expanding installed base. OEM vehicle manufacturers increasingly integrate ambient light bands and dashboard illumination as standard features, strengthening demand stability. Energy efficiency compliance also favors ambient LED retrofits across commercial buildings and hospitality interiors, further consolidating its leading position.

By Platform Type

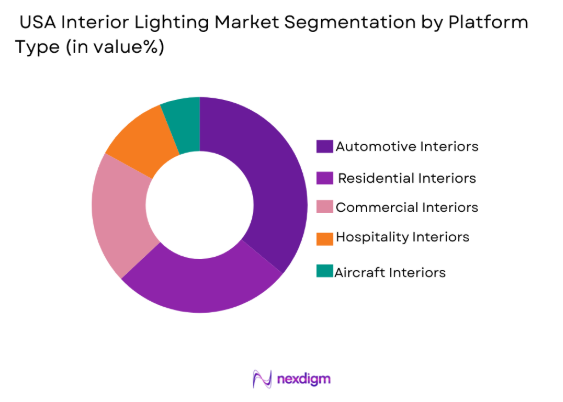

USA Interior Lighting market is segmented by platform type into automotive interiors, residential interiors, commercial interiors, hospitality interiors, and aircraft interiors. Recently, automotive interiors has a dominant market share due to factors such as demand patterns, brand presence, infrastructure availability, or consumer preference. Automotive interiors lead because interior lighting has become a key differentiation element in vehicle design, particularly in premium and electric vehicles emphasizing cabin ambiance and user experience. OEM integration of multi-zone ambient lighting, dynamic color transitions, and illuminated panels is expanding across mid-range models, increasing volume deployment. Regulatory focus on energy-efficient automotive electronics favors LED interior modules, accelerating adoption. The shift toward connected cabins and digital dashboards requires integrated illumination interfaces for controls and displays. High vehicle production volumes combined with lifecycle upgrades and aftermarket customization demand reinforce automotive platform dominance.

Competitive Landscape

The USA Interior Lighting market shows moderate consolidation with multinational lighting manufacturers and automotive component suppliers controlling technology-intensive segments such as LED modules, optical diffusion systems, and smart lighting electronics. Major players leverage vertical integration across LEDs, drivers, and control software to maintain cost efficiency and innovation leadership. Automotive OEM partnerships and architectural lighting projects create long-term supply relationships, while regional specialists compete in decorative and retrofit segments through design customization and niche applications.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Application Integration |

| Signify | 1891 | Netherlands | ~ | ~ | ~ | ~ | ~ |

| Acuity Brands | 1892 | USA | ~ | ~ | ~ | ~ | ~ |

| OSRAM | 1919 | Germany | ~ | ~ | ~ | ~ | ~ |

| HELLA | 1899 | Germany | ~ | ~ | ~ | ~ | ~ |

| GE Lighting | 1911 | USA | ~ | ~ | ~ | ~ | ~ |

USA Interior Lighting Market Analysis

Growth Drivers

Expansion of Human-Centric and Ambient Interior Lighting in Automotive and Smart Buildings

The USA Interior Lighting market is strongly driven by the accelerating shift toward human-centric lighting concepts that optimize comfort, mood, and circadian alignment across automotive cabins and built environments, encouraging adoption of tunable ambient illumination systems across residential, commercial, and mobility platforms. Automotive manufacturers are integrating multi-color ambient strips, illuminated surfaces, and adaptive brightness controls as standard interior features to enhance user experience and brand differentiation, which substantially increases per-vehicle lighting content and system complexity. Parallel growth in smart homes and connected buildings is promoting integrated lighting ecosystems where interior illumination interacts with occupancy sensors, daylight harvesting systems, and digital control networks, reinforcing demand for intelligent ambient fixtures. Interior designers and architects are prioritizing concealed and layered lighting architectures that rely heavily on diffused LED panels, coves, and indirect luminaires, expanding installed ambient lighting volumes across renovation and new construction projects. Energy efficiency regulations and building codes are simultaneously accelerating replacement of legacy incandescent and fluorescent interior fixtures with LED-based ambient solutions, ensuring long-term retrofit demand stability. Consumer preference for personalization through adjustable color temperature and intensity further strengthens adoption of dynamic interior lighting platforms across homes and vehicles. Technology advances in miniaturized LEDs, flexible light guides, and optical diffusion materials are enabling seamless integration of lighting into surfaces, panels, and furniture, expanding application scope. These combined technological, regulatory, and design shifts are sustaining structural growth momentum in interior lighting adoption across multiple end-use sectors.

Integration of LED and Smart Control Electronics Across Interior Illumination Systems

The widespread integration of solid-state LED technology with embedded control electronics is significantly propelling the USA Interior Lighting market by improving efficiency, durability, and functional versatility of interior lighting solutions across automotive, residential, and commercial applications. LED-based interior luminaires offer superior energy performance, long operational life, and compact form factors, enabling designers to implement thin, lightweight, and customizable lighting elements across dashboards, ceilings, cabinetry, and architectural features. Smart drivers, wireless connectivity modules, and programmable controllers are transforming lighting fixtures into interactive systems capable of adaptive brightness, color tuning, and automated scheduling, increasing functional value beyond basic illumination. Automotive interiors are particularly benefiting from digitally controlled lighting zones synchronized with infotainment and user interfaces, enhancing cabin ambiance and perceived quality. Commercial buildings are adopting networked interior lighting for energy management and occupancy-based automation, supporting sustainability targets and operational efficiency. Residential consumers are increasingly installing app-controlled interior lighting integrated with voice assistants and home automation ecosystems, accelerating smart lighting penetration. Manufacturing scale economies and declining LED component costs are improving affordability and encouraging large-scale deployment across retrofit and new installations. Continuous innovation in optical efficiency and thermal management is further improving performance reliability, reinforcing long-term adoption across interior lighting platforms.

Market Challenges

High Integration and Design Complexity in Advanced Interior Lighting Systems

The USA Interior Lighting market faces significant challenges arising from the growing complexity of integrating advanced lighting modules into diverse interior platforms such as vehicles, buildings, and aircraft cabins, which increases engineering requirements, development timelines, and production costs for manufacturers and system integrators. Automotive ambient lighting systems require precise optical diffusion, uniform brightness distribution, and seamless integration with interior materials such as plastics, leather, and composites, creating design constraints that demand specialized tooling and engineering expertise. Smart building lighting installations must coordinate luminaires, sensors, controllers, and network infrastructure, increasing system architecture complexity and installation skill requirements. Variations in interior geometry, mounting conditions, and environmental factors complicate standardization of lighting components, limiting scalability across projects and platforms. Reliability expectations for automotive and aerospace interiors impose strict durability, vibration resistance, and thermal stability requirements, further elevating design and testing complexity. Integration with digital control networks and user interfaces introduces software dependencies that require ongoing updates and cybersecurity considerations, adding lifecycle management burdens. Supply chains must accommodate diverse optical components, drivers, housings, and electronics, increasing procurement and manufacturing coordination challenges. These multidimensional integration requirements raise overall system costs and technical barriers, slowing adoption among cost-sensitive applications and smaller manufacturers.

Cost Sensitivity and Retrofit Barriers in Residential and Commercial Interior Lighting Upgrades

Despite technological advantages of modern interior lighting systems, the USA Interior Lighting market encounters resistance from price-sensitive segments where upfront costs and installation complexity hinder widespread adoption of advanced LED and smart lighting upgrades across existing residential and commercial buildings. Many legacy structures require electrical modifications, mounting adaptations, and control wiring to accommodate new interior luminaires, increasing project expenses and disruption during renovation. Commercial property owners often prioritize essential infrastructure upgrades over aesthetic or ambient lighting enhancements, delaying modernization investments. Small businesses and households may perceive limited immediate financial return from interior lighting upgrades beyond basic illumination, reducing willingness to invest in premium systems. Fragmented building ownership and tenant-landlord cost allocation issues further complicate retrofit decision-making in multi-tenant properties. Skilled installation requirements for integrated lighting controls and automation systems increase labor costs and limit contractor availability in certain regions. Product diversity and compatibility concerns between fixtures, drivers, and control protocols create uncertainty for buyers evaluating upgrade options. Economic fluctuations affecting construction and renovation spending can quickly reduce demand for discretionary interior lighting improvements. These financial and practical barriers collectively constrain retrofit penetration rates and slow expansion in non-premium interior lighting segments.

Opportunities

Expansion of Interior Lighting in Electric and Autonomous Vehicle Cabin Architectures

The transition toward electric and autonomous vehicles presents substantial opportunity for the USA Interior Lighting market as cabin environments evolve into multifunctional living and working spaces requiring sophisticated ambient illumination, user interaction lighting, and adaptive mood environments beyond conventional automotive lighting roles. Electric vehicle platforms prioritize minimalist dashboards, panoramic interiors, and flat floors that increase visible lighting surfaces and enable continuous light bands, illuminated panels, and customizable zones throughout the cabin. Autonomous driving concepts anticipate occupants engaging in relaxation, entertainment, or productivity activities, creating demand for circadian lighting, reading illumination, and ambient scene control similar to residential interiors. Manufacturers are exploring interactive lighting interfaces that communicate vehicle status, navigation cues, and safety alerts through color and motion patterns embedded in interior surfaces. Lightweight LED modules and flexible light guides support integration into seats, doors, ceilings, and consoles without adding significant mass or power consumption. Premium vehicle differentiation strategies increasingly rely on immersive interior ambiance, encouraging broader adoption across mid-range segments. Collaboration between automotive OEMs and lighting technology providers is accelerating innovation in optical materials and control software tailored for vehicle cabins. As electric and autonomous vehicle penetration expands, interior lighting content per vehicle is expected to rise substantially, creating sustained long-term demand growth.

Growth of Human-Centric and Wellness-Oriented Lighting in Residential and Hospitality Interiors

Increasing awareness of the physiological and psychological effects of lighting on human health and wellbeing is generating new opportunity for the USA Interior Lighting market through adoption of human-centric lighting systems in homes, hotels, healthcare facilities, and workplaces designed to support circadian rhythms, relaxation, and productivity. Tunable white and color-adjustable interior luminaires allow dynamic adjustment of light intensity and spectrum throughout the day to align with natural biological cycles, improving occupant comfort and sleep patterns. Hospitality and wellness-focused residential developments are incorporating layered ambient lighting, indirect illumination, and customizable scenes to create immersive interior environments that enhance guest experience and perceived luxury. Healthcare and senior living facilities are implementing therapeutic lighting strategies to support patient recovery and cognitive health, expanding specialized interior lighting demand. Integration with smart home and building automation platforms enables personalized lighting schedules and responsive environmental control, increasing consumer engagement. Interior designers and architects are emphasizing concealed and architectural lighting techniques that rely on advanced diffused LED systems, expanding product adoption. Regulatory emphasis on energy efficiency aligns with LED-based human-centric lighting solutions, supporting sustainability goals. These health-driven design trends are broadening interior lighting applications beyond aesthetics toward functional wellness infrastructure.

Future Outlook

The USA Interior Lighting market is expected to advance steadily over the next five years as LED efficiency improvements, smart control integration, and human-centric design principles reshape interior illumination across vehicles and buildings. Growth will be supported by electric vehicle cabin innovation, smart home adoption, and renovation of aging building infrastructure. Regulatory energy standards will continue accelerating LED retrofit demand. Increasing emphasis on wellness-oriented lighting and immersive interior experiences will further expand premium and intelligent interior lighting deployments.

Major Players

- Signify

- Acuity Brands

- OSRAM

- HELLA

- GE Lighting

- Stanley Electric

- Koito Manufacturing

- Valeo

- Nichia

- Cree Lighting

- Hubbell Lighting

- Panasonic Lighting

- Lutron Electronics

- Zumtobel Group

- Legrand

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive OEM interior design teams

- Residential lighting manufacturers

- Commercial building developers

- Smart home technology providers

- Hospitality infrastructure operators

- Architectural lighting designers

Research Methodology

Step 1: Identification of Key Variables

Core market variables including interior lighting technologies, platform adoption patterns, integration levels, regulatory influences, and end-use demand drivers were identified through industry databases, standards documentation, and sector-specific literature. Product architecture and platform segmentation frameworks were established to structure analysis.

Step 2: Market Analysis and Construction

Segmental demand patterns and technology penetration trends were analyzed across automotive, residential, and commercial interiors using manufacturer disclosures, construction activity indicators, and vehicle production data. Competitive positioning and value chain dynamics were mapped to construct market structure.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings regarding dominant segments, growth drivers, and technology transitions were validated through consultations with lighting engineers, automotive interior designers, and building lighting specialists. Feedback refined adoption assumptions and integration challenges.

Step 4: Research Synthesis and Final Output

Validated insights were synthesized into segment narratives, competitive assessment, and strategic outlook for the USA Interior Lighting market. Qualitative and structural conclusions were consolidated into a coherent market intelligence framework supporting strategic decision-making.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Integration of Ambient Lighting in Automotive Cabins

Expansion of Smart and Connected Interior Lighting in Buildings

Energy Efficiency Regulations Accelerating LED Interior Adoption

Growth in Premium Residential and Hospitality Interior Design

Advancements in Flexible and Miniaturized LED Technologies - Market Challenges

High Integration Complexity in Automotive Interior Lighting Systems

Cost Sensitivity in Residential Lighting Retrofit Projects

Compatibility Issues Across Smart Lighting Protocols

Thermal and Durability Constraints in Compact Fixtures

Supply Chain Dependence on Semiconductor Components - Market Opportunities

Interior Lighting Expansion in Electric and Autonomous Vehicles

Human Centric Lighting Adoption in Wellness Architecture

Growth of Smart Home Integrated Interior Illumination - Trends

Multi Color Ambient Lighting in Vehicle Interiors

Tunable White Lighting in Residential Spaces

Architectural Concealed Linear Lighting Growth

App Controlled Interior Lighting Ecosystems

Integration of Lighting with Interior Materials - Government Regulations & Defense Policy

Building Energy Efficiency Lighting Standards

Automotive Interior Illumination Safety Regulations

LED Efficiency and Environmental Compliance Policies

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Ambient Interior Lighting Systems

Task and Functional Interior Lighting

Accent and Decorative Interior Lighting

Adaptive and Dynamic Lighting Systems

Integrated Smart Interior Lighting Systems - By Platform Type (In Value%)

Automotive Interior Lighting Platforms

Residential Interior Lighting Platforms

Commercial Building Interior Lighting

Hospitality Interior Lighting Environments

Aerospace Cabin Interior Lighting - By Fitment Type (In Value%)

OEM Integrated Interior Lighting

Aftermarket Retrofit Lighting Kits

Modular Plug and Play Lighting

Embedded Architectural Lighting

Surface Mounted Interior Lighting - By End User Segment (In Value%)

Automotive Manufacturers

Residential Property Owners

Commercial Real Estate Developers

Hospitality and Leisure Operators

Aerospace Cabin Integrators - By Procurement Channel (In Value%)

Direct OEM Procurement

Lighting Distributors and Wholesalers

Online Lighting Retail Platforms

Project Based Contract Procurement

Aftermarket Accessory Retailers - By Material / Technology (in Value %)

LED Strip and Linear Lighting

LED Panel and Diffused Modules

Fiber Optic Interior Lighting

OLED Interior Lighting Panels

Smart Connected Lighting Electronics

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Technology Integration Level, Platform Coverage, OEM Partnerships, Smart Lighting Capability, Product Portfolio Depth, Manufacturing Scale, Design Customization Capability, Geographic Presence)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Signify

Acuity Brands

OSRAM

HELLA

Stanley Electric

Koito Manufacturing

Valeo

Nichia

Cree Lighting

Hubbell Lighting

Panasonic Lighting

Lutron Electronics

Zumtobel Group

Legrand

Current Lighting

- Automotive OEMs Increasing Cabin Lighting Content

- Residential Consumers Adopting Smart Interior Lighting

- Commercial Developers Prioritizing Energy Efficient Interiors

- Hospitality Sector Investing in Experiential Lighting Design

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now