Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on data published by the National Highway Traffic Safety Administration and the U.S. Department of Transportation, the USA Lane Departure Warning Systems market reached approximately USD ~ billion, driven by regulatory encouragement for advanced driver assistance systems and increasing OEM integration across passenger vehicles. Growing vehicle production volumes and consumer prioritization of safety technologies have strengthened installation rates. Continuous advancements in camera sensors, radar fusion modules, and onboard processing capabilities further support revenue expansion across domestic automotive manufacturing clusters.

Detroit, Michigan and the broader Midwest automotive corridor dominate system development due to concentrated OEM headquarters and supplier facilities. California contributes significantly through semiconductor design, AI algorithm development, and electric vehicle manufacturing ecosystems centered in Silicon Valley and Los Angeles. Southern states including Tennessee and Alabama remain important because of large-scale vehicle assembly plants. Strong federal safety compliance frameworks and infrastructure modernization initiatives further reinforce national demand concentration.

Market Segmentation

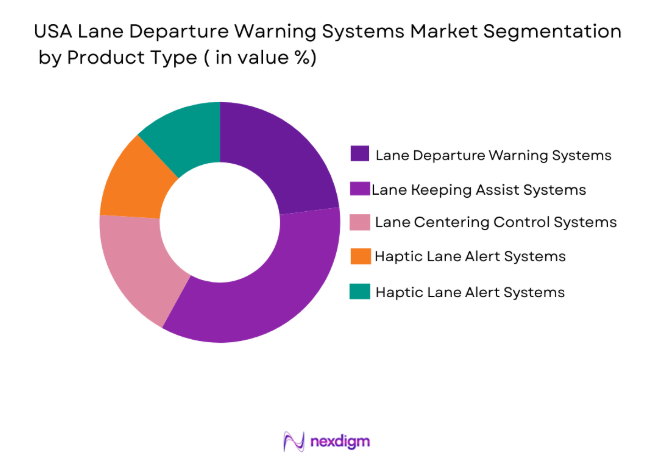

By Product Type

USA Lane Departure Warning Systems market is segmented by product type into Lane Departure Warning Systems, Lane Keeping Assist Systems, Lane Centering Control Systems, Haptic Lane Alert Systems, and Vision-Based Lane Monitoring Systems. Recently, Lane Keeping Assist Systems have a dominant market share due to their active steering correction capability, higher integration with adaptive cruise control, broader deployment across passenger vehicle segments, improved driver confidence in semi-autonomous assistance, and increasing OEM standardization within advanced driver assistance system packages.

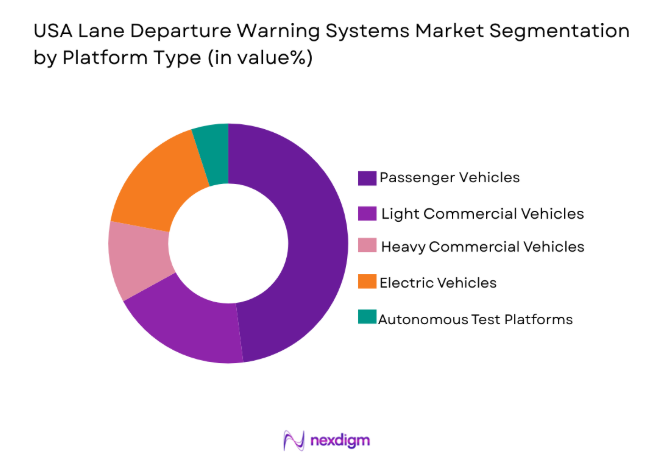

By Platform Type

USA Lane Departure Warning Systems market is segmented by platform type into Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Autonomous Test Vehicles, and Electric Vehicles. Recently, Passenger Vehicles has a dominant market share due to high vehicle ownership, mandatory safety feature integration, and increasing consumer awareness regarding driver assistance technologies. Automakers increasingly include lane departure warning systems as standard features within mid range and premium passenger cars. Integration with broader ADAS packages such as lane keeping assistance and adaptive cruise control further strengthens adoption across passenger vehicle segments.

Competitive Landscape

The USA Lane Departure Warning Systems market is moderately consolidated, with global automotive suppliers controlling a significant portion of OEM contracts. Market leadership is influenced by proprietary sensor technologies, long-term partnerships with vehicle manufacturers, and strong R&D investments in AI-driven perception systems. Strategic acquisitions and software integration capabilities continue to shape competitive positioning across the value chain.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | ADAS Integration Capability |

| Robert Bosch GmbH | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

USA Lane Departure Warning Systems Market Analysis

Growth Drivers

Expansion of Federal Vehicle Safety Standards Mandating Advanced Driver Assistance Integration:

The strengthening of federal safety frameworks in the United States has significantly accelerated adoption of lane departure warning systems across new vehicle platforms. Regulatory encouragement from national highway safety authorities has pushed automakers to integrate advanced driver assistance technologies as standard or bundled features rather than optional upgrades. This regulatory direction has reduced variability in installation rates and encouraged large-scale procurement agreements between OEMs and suppliers. Insurance industry data highlighting accident reduction benefits has further incentivized manufacturers to prioritize active safety systems. Growing litigation and liability risks associated with driver distraction have encouraged companies to embed corrective steering and lane monitoring functions within vehicle architectures. Fleet operators seeking compliance with safety performance benchmarks are increasingly standardizing vehicles equipped with lane support technologies. Continuous harmonization between federal standards and state-level road safety programs has strengthened long-term demand visibility. As regulatory clarity improves, supplier investment in research and localized production facilities has increased substantially.

Rising Consumer Demand for Semi-Autonomous Driving Capabilities:

Consumer perception of vehicle safety has evolved toward expectation of intelligent intervention rather than passive alerts, encouraging broader deployment of lane keeping technologies. Buyers in mid and premium vehicle categories increasingly associate lane departure correction with modern mobility standards. Automotive manufacturers respond by integrating sensor fusion systems that combine cameras, radar, and onboard processors to deliver smoother steering control. Electric vehicle growth has further amplified demand for software-driven driver assistance features. Technology-savvy customers actively compare ADAS capabilities during purchase decisions, strengthening competitive pressure among OEMs. Ride-sharing and subscription vehicle services prioritize advanced safety packages to enhance brand credibility. Continuous marketing of semi-autonomous features reinforces awareness of lane monitoring solutions. Improvements in system accuracy and reduced false alerts contribute to greater user acceptance.

Market Challenges

High System Calibration and Integration Costs Across Vehicle Platforms:

Lane departure warning systems require precise camera alignment, radar synchronization, and software calibration to function accurately across diverse vehicle models. Integration complexity increases when adapting systems to existing mechanical steering architectures. Smaller OEMs face financial pressure due to elevated sensor procurement and validation costs. Continuous software updates demand cybersecurity safeguards and technical expertise. Supply chain volatility affecting semiconductor availability adds additional cost uncertainty. Aftermarket retrofitting remains technically challenging and labor-intensive. Weather sensitivity can impact performance reliability, requiring additional sensor enhancements. Warranty liabilities associated with malfunctioning systems can raise operational expenses.

Performance Limitations in Adverse Weather and Road Conditions:

Lane detection algorithms rely heavily on clear road markings and camera visibility, which can deteriorate under snow, heavy rain, or faded paint conditions. Sensor obstruction reduces detection accuracy and may trigger inconsistent alerts. Rural infrastructure gaps create variability in system effectiveness. False positives can reduce driver trust and encourage manual override. System overreliance may cause complacency among drivers. Continuous testing across diverse environments requires substantial R&D spending. Infrastructure modernization disparities between states limit uniform adoption performance. Technology refinement cycles remain ongoing to address environmental limitations.

Opportunities

Integration with Autonomous Driving Software Ecosystems:

The convergence of lane departure systems with higher-level autonomous driving platforms presents significant technological and commercial expansion potential. As vehicle manufacturers advance toward Level 2 and Level 3 autonomy, lane centering and monitoring functionalities become foundational components of broader control architectures. Software-defined vehicle platforms enable over-the-air upgrades, enhancing lifecycle value of installed systems. Partnerships between automotive OEMs and semiconductor firms foster scalable perception modules. Increased electric vehicle penetration encourages unified software stacks integrating safety and autonomy features. Federal research initiatives supporting smart mobility accelerate innovation funding. Data collection from connected vehicles improves algorithm training and predictive accuracy. Collaborative industry standards for automated steering interfaces create interoperability advantages.

Commercial Fleet Safety Modernization Programs:

Logistics companies and public transportation agencies increasingly prioritize accident prevention technologies to reduce operational risk exposure. Fleet operators benefit from telematics integration that combines lane monitoring data with driver behavior analytics. Insurance premium reductions for safety-compliant fleets provide measurable financial incentives. Government transportation grants encourage modernization of public service vehicles. Standardization of ADAS packages within procurement contracts improves scalability. Predictive maintenance insights derived from sensor systems enhance vehicle uptime. Expansion of e-commerce distribution networks raises the need for safe long-distance driving support. Long-term fleet replacement cycles ensure sustained procurement of lane departure technologies.

Future Outlook

Over the next five years, the USA Lane Departure Warning Systems market is expected to experience steady expansion supported by regulatory reinforcement and technological convergence with semi-autonomous platforms. Advancements in AI-based perception and sensor fusion will improve system reliability across diverse road conditions. Federal safety mandates and infrastructure modernization initiatives will strengthen adoption. Increasing integration within electric and connected vehicles will further elevate long-term demand momentum.

Major Players

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Valeo SA

- ZF Friedrichshafen AG

- Mobileye Global Inc. • Autoliv Inc.

- Hyundai Mobis

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Panasonic Automotive Systems

- HitachiAstemoLtd.

- HELLA GmbH & Co. KGaA

Key Target Audience

- Automotive OEMs

- Automotive Suppliers

- Electric Vehicle Manufacturers

- Commercial Fleet Operators

- Insurance Companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Semiconductor Manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key performance indicators, regulatory variables, OEM production volumes, and technology adoption metrics were identified through structured secondary research. Industry databases, transportation authority publications, and company disclosures were analyzed to define baseline parameters.

Step 2: Market Analysis and Construction

Quantitative modeling incorporated vehicle production data, ADAS penetration rates, and supplier revenue disclosures. Demand-side drivers and cost structures were mapped to construct segmented market estimates.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through consultations with automotive engineers, ADAS product managers, and supply chain specialists. Comparative benchmarking ensured consistency across segment-level assumptions.

Step 4: Research Synthesis and Final Output

All quantitative and qualitative insights were synthesized into a structured framework aligning regulatory, technological, and competitive dimensions. Final outputs were cross-verified for logical coherence and data accuracy.

- Executive Summary

- Research Methodology

(Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing federal road safety mandates and NCAP performance requirements

Rising integration of ADAS in mid-segment vehicles

Growing consumer awareness regarding accident prevention technologies

Technological advancements in camera resolution and sensor fusion

Expansion of electric and connected vehicle production - Market Challenges

High calibration and maintenance costs

False alert limitations in adverse weather conditions

Complex integration with legacy vehicle architectures

Cybersecurity vulnerabilities in connected ADAS platforms

Pricing pressure from cost-sensitive vehicle segments - Market Opportunities

Adoption of AI-enabled predictive lane analytics

Expansion in commercial fleet safety modernization

Integration with autonomous driving software ecosystems - Trends

Transition toward software-defined ADAS architectures

Sensor fusion combining radar and vision systems

Edge computing for real-time lane detection

Over-the-air update capabilities for system improvement

Increased collaboration between semiconductor and OEM players - Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standards alignment with ADAS requirements

New Car Assessment Program safety rating incentives

State-level road infrastructure digitization initiatives - SWOT Analysis

Stakeholder and Ecosystem Analysis - Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Lane Departure Warning

Lane Keeping Assist

Lane Centering Control

Haptic Steering Feedback Systems

Vision-Based Alert Systems - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Autonomous Test Platforms - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Retrofit Kits

Embedded ADAS Modules

Software-Defined Upgradable Systems

Fleet-Specific Installations - By EndUser Segment (In Value%)

Private Vehicle Owners

Commercial Fleet Operators

Logistics and Transportation Companies

Ride-Sharing Operators

Government Transportation Agencies - By Procurement Channel (In Value%)

Direct OEM Procurement

Supplier Contracts

Authorized Dealership Networks

Aftermarket Distributors

Fleet Procurement Agreements - By Material / Technology (in Value %)

Mono Camera Systems

Stereo Vision Systems

Radar Assisted Vision Systems

LiDAR Integrated Systems

AI-Based Image Processing Platforms

- Market structure and competitive positioning

Market share snapshot of major players

CrossComparison Parameters (Technology Integration Depth, Sensor Type Portfolio, OEM Partnerships, Software Capability, Pricing Strategy, Aftermarket Presence, R&D Intensity, Production Capacity) - SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Robert Bosch GmbH

Continental AG

Denso Corporation

Aptiv PLC

ZF Friedrichshafen AG

Magna International Inc.

Valeo SA

Mobileye Global Inc.

Autoliv Inc.

Hyundai Mobis

Texas Instruments Incorporated

NXP Semiconductors N.V.

Panasonic Automotive Systems

Hitachi Astemo Ltd.

HELLA GmbH & Co. KGaA

- Commercial fleets prioritizing accident liability reduction

- Private consumers valuing enhanced vehicle safety features

- Ride-sharing platforms adopting advanced safety packages

- Government agencies investing in public transport modernization

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now