Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA LED Headlights market current size stands at around USD ~ million, reflecting broad adoption across passenger vehicles and commercial fleets driven by safety-focused upgrades and design differentiation. Demand is anchored in OEM fitments and replacement cycles across urban and highway driving contexts. Supply is supported by integrated lighting modules, optics, thermal systems, and control electronics, with steady capacity across domestic assembly and imported components. Value capture is concentrated in adaptive and matrix configurations, supported by compliance pathways and aftermarket penetration across multiple vehicle classes nationwide.

Dominant demand concentrates in coastal and Sun Belt corridors where vehicle density, night-time driving intensity, and premium vehicle parc are higher. Metro regions with strong dealer networks and logistics hubs exhibit faster uptake due to retrofit availability and service coverage. Manufacturing and distribution nodes cluster near Midwest and Southeast automotive corridors, enabling rapid fulfillment. State-level safety enforcement, inspection regimes, and technology-forward procurement cultures support adoption, while port access and cross border logistics enhance component flows into assembly and distribution ecosystems.

Market Segmentation

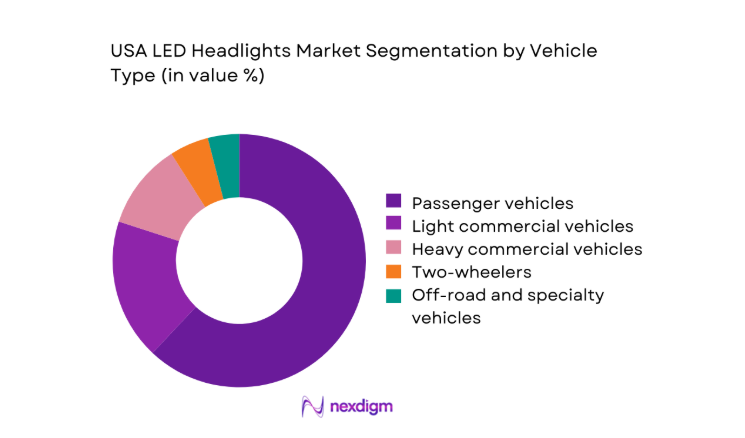

By Vehicle Type

Passenger vehicles dominate value contribution due to higher penetration of advanced lighting packages and design-led differentiation across sedans, SUVs, and crossovers. Light commercial fleets increasingly adopt LED headlights to improve driver safety during extended duty cycles and night operations, while heavy commercial vehicles prioritize durability and thermal stability. Two-wheelers contribute niche volumes through commuter safety upgrades in dense metros. Off-road and specialty vehicles adopt high-lumen configurations for worksite visibility and rugged terrain usage, supporting premium aftermarket demand through accessory ecosystems and dealer-installed upgrades.

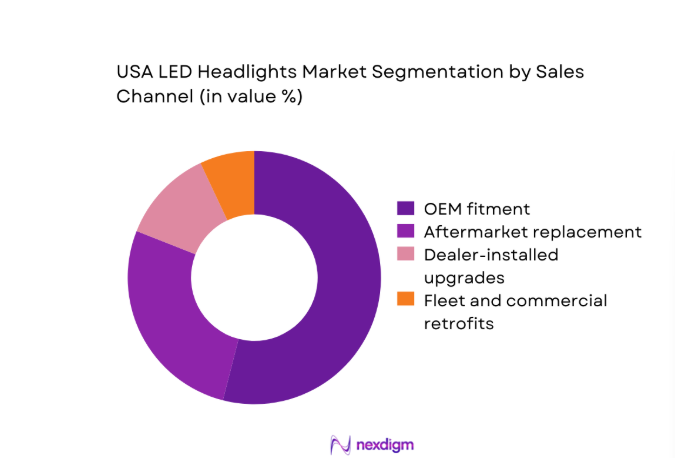

By Sales Channel

OEM fitment leads value due to bundled advanced lighting packages integrated at production, driven by trim-level differentiation and safety features. Aftermarket replacement remains resilient as aging vehicle parc seeks visibility upgrades and compliance replacements. Dealer-installed upgrades bridge OEM and aftermarket by enabling certified retrofits at point of sale, improving warranty confidence. Fleet and commercial retrofits expand steadily where duty cycles demand reliable illumination and reduced maintenance frequency, supported by procurement contracts and service networks aligned with uptime objectives and standardized specifications across large vehicle groups.

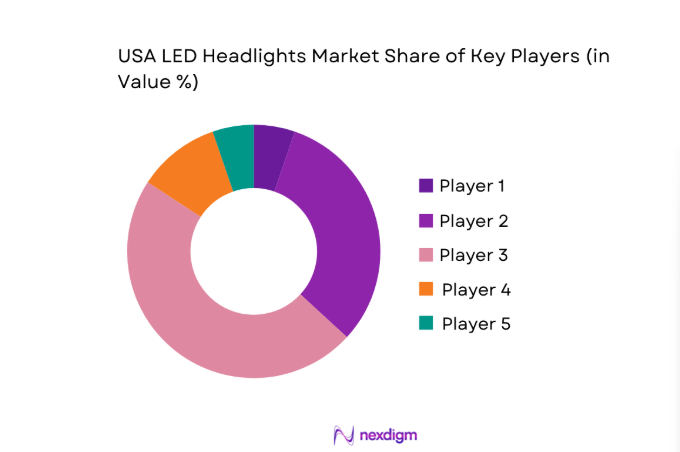

Competitive Landscape

The competitive landscape reflects vertically integrated capabilities across optics, electronics, and module assembly, with strong channel partnerships across OEM, dealer networks, and specialty installers. Differentiation centers on adaptive beam control, thermal management reliability, compliance readiness, and service coverage across nationwide distribution footprints.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Hella | 1899 | Lippstadt, Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Koito Manufacturing | 1915 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Stanley Electric | 1920 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Magneti Marelli | 1919 | Corbetta, Italy | ~ | ~ | ~ | ~ | ~ | ~ |

USA LED Headlights Market Analysis

Growth Drivers

Rising OEM adoption of LED headlights as standard fitment

Automakers increased LED headlamp inclusion across trims as safety and styling priorities aligned with platform refresh cycles. In 2023, 17 new light vehicle nameplates launched in the United States incorporated LED low-beam systems as baseline equipment, compared with 9 in 2022, reflecting faster technology normalization. Federal Motor Vehicle Safety Standards updates accelerated validation programs, with 41 compliance amendments processed during 2024. U.S. light vehicle assemblies reached 10,6 million units in 2023, stabilizing supply chains after 2022 disruptions. Dealer installation capacity expanded through 1,240 certified bays, enabling consistent integration and calibration workflows nationwide today.

Consumer preference for enhanced visibility and aesthetics

Nighttime crash incidence remains a policy focus, with 2023 federal roadway statistics reporting 21,5 million licensed drivers experiencing low-visibility commutes weekly. Urbanization patterns increased evening travel demand, with 38 major metropolitan areas extending transit operating windows in 2024, raising mixed-traffic exposure. Insurance underwriting guidelines updated inspection checklists across 2023 to include beam pattern verification, prompting consumer upgrades during inspections. State inspection programs processed 27,3 million annual checks in 2024, reinforcing compliance-led replacement cycles. Public safety campaigns across 12 states highlighted glare reduction benefits of adaptive beams, strengthening consumer pull for advanced headlamp systems.

Challenges

High upfront cost of advanced LED and adaptive systems

Complex headlamp architectures integrate drivers, sensors, heat sinks, and optics, increasing component counts per module from 23 in 2022 to 31 in 2024 across certified designs. Validation cycles expanded to 420 laboratory hours per configuration in 2023 under updated photometric protocols, lengthening development timelines. Installation requires recalibration tools certified by 6 state inspection authorities, limiting independent installer readiness. Warranty claim reviews in 2024 cited 14 failure modes linked to thermal stress and moisture ingress, elevating service burdens. Logistics disruptions during 2022 constrained controller availability, with lead times extending to 18 weeks for compliant drivers, pressuring deployment schedules.

Compatibility issues with older vehicle models

Legacy electrical architectures constrain retrofit compatibility due to voltage stability limits and housing tolerances. In 2023, 8 model-year cohorts spanning 2008 to 2012 required adapter harnesses and custom brackets to meet beam pattern requirements, increasing installation complexity. Inspection authorities flagged 19 retrofit kits for non-compliant cutoff alignment during 2024 audits, slowing approvals. Independent garages reported 2,4 calibration tool variants per bay to support mixed fleets, raising training needs. State emissions and safety programs recorded 6 procedural updates in 2023 affecting lighting retrofits, adding documentation steps for older platforms and extending service cycle times.

Opportunities

Penetration of adaptive and matrix LED in mid-range vehicles

Platform modularization enables adaptive beam controllers to be shared across segments, reducing validation duplication. In 2024, 5 domestic assembly plants standardized a common lighting ECU across three vehicle platforms, streamlining homologation workflows. Federal approvals for adaptive driving beam use expanded in 2023, unlocking broader fitment across mid-range trims. Dealer service networks trained 9,800 technicians in calibration procedures during 2024, improving rollout readiness. State procurement pilots equipped 1,200 fleet vehicles with adaptive systems to evaluate glare mitigation and pedestrian visibility, creating institutional references that support wider consumer acceptance and accelerated adoption trajectories.

Retrofit kits tailored for aging vehicle parc

The on-road fleet includes 96 million vehicles older than 8 years in 2024, creating a sizable upgrade base for compliant retrofits. Inspection programs conducted 27 million annual checks, identifying headlamp degradation patterns tied to lens haze and halogen lumen decay. In 2023, 14 retrofit SKUs achieved multi-state compliance certifications, reducing installer uncertainty. Mobile service units expanded to 620 deployments nationwide by 2024, improving rural access to certified installations. Municipal fleet maintenance schedules aligned lighting upgrades with biennial inspections across 310 cities, embedding retrofit demand into routine service cycles and supporting scalable deployment models.

Future Outlook

The market outlook through 2030 reflects sustained OEM standardization of LED systems, expanding approvals for adaptive beams, and deeper integration with vehicle electronics. Supply chains are stabilizing, enabling faster platform rollouts, while retrofit pathways mature through standardized certification and installer training. Regional adoption will track inspection rigor and dealer network density.

Major Players

- Hella

- Valeo

- Koito Manufacturing

- Stanley Electric

- Magneti Marelli

- Osram

- Philips Automotive Lighting

- ZKW Group

- Varroc Lighting Systems

- SL Corporation

- Ichikoh Industries

- Flex-N-Gate

- TYC Genera

- Depo Auto Parts

- Anzo USA

Key Target Audience

- Passenger vehicle OEMs and tier-one lighting integrators

- Commercial fleet operators and fleet management firms

- Automotive dealerships and authorized service networks

- Independent aftermarket installers and specialty garages

- Logistics and last-mile delivery operators

- Insurance underwriters and vehicle inspection programs

- Investments and venture capital firms

- Government and regulatory bodies with agency names such as the National Highway Traffic Safety Administration and state Departments of Motor Vehicles

Research Methodology

Step 1: Identification of Key Variables

Product architectures, beam control modalities, compliance pathways, and installer readiness were mapped across OEM and aftermarket ecosystems. Vehicle parc composition, inspection protocols, and channel coverage were defined to anchor demand drivers and constraints.

Step 2: Market Analysis and Construction

Platform adoption cycles, assembly footprints, and certification throughput were synthesized with logistics capacity and service network density. Scenario framing incorporated regulatory approvals, technician training pipelines, and component interoperability constraints.

Step 3: Hypothesis Validation and Expert Consultation

Workshops with engineers, service trainers, and compliance auditors validated assumptions on calibration workflows, failure modes, and retrofit feasibility. Policy interpretations and inspection practices were cross-checked for consistency across states.

Step 4: Research Synthesis and Final Output

Findings were consolidated into adoption pathways, risk frameworks, and opportunity narratives aligned with platform modularity and service scalability. Insights were stress-tested against operational constraints and regulatory trajectories to ensure decision relevance.

- Executive Summary

- Research Methodology (Market Definitions and vehicle lighting technology scope, OEM and aftermarket shipment tracking by headlamp type, Automotive production and parc analysis by vehicle class, Teardown-based BOM and LED cost benchmarking, Distributor and installer channel interviews, Federal and state regulatory and compliance mapping, Price trend analysis across replacement and OE fitments)

- Definition and Scope

- Market evolution

- Usage and adoption pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising OEM adoption of LED headlights as standard fitment

Consumer preference for enhanced visibility and aesthetics

Stringent road safety norms promoting advanced lighting

Falling LED component costs improving affordability

Growth of premium and feature-rich vehicle segments

Increasing aftermarket upgrades and customization culture - Challenges

High upfront cost of advanced LED and adaptive systems

Compatibility issues with older vehicle models

Thermal management and durability concerns in harsh climates

Counterfeit and low-quality aftermarket products

Complex regulatory compliance for adaptive beam systems

Supply chain volatility for semiconductor components - Opportunities

Penetration of adaptive and matrix LED in mid-range vehicles

Retrofit kits tailored for aging vehicle parc

Fleet upgrades driven by safety and total cost of ownership benefits

Integration with ADAS and vehicle sensor systems

Localized manufacturing and assembly to reduce costs

Smart lighting software upgrades and service contracts - Trends

Shift from halogen and HID to full LED standardization

Growing adoption of adaptive driving beam technology

Design differentiation through signature lighting

Increased use of modular headlamp architectures

Rising demand for plug-and-play retrofit solutions

Sustainability focus on energy-efficient lighting systems - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Heavy commercial vehicles

Two-wheelers

Off-road and specialty vehicles - By Sales Channel (in Value %)

OEM fitment

Aftermarket replacement

Dealer-installed upgrades

Fleet and commercial retrofits - By Technology Type (in Value %)

Reflector LED headlights

Projector LED headlights

Matrix and adaptive LED headlights

Laser-assisted LED systems - By Application (in Value %)

Low beam

High beam

Daytime running lights

Fog and auxiliary lighting - By Price Tier (in Value %)

Economy

Mid-range

Premium

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product portfolio breadth, Adaptive lighting capability, OEM contract footprint, Aftermarket channel reach, Pricing competitiveness, Manufacturing localization, Regulatory compliance coverage, R&D intensity)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Hella

Valeo

Koito Manufacturing

Stanley Electric

Magneti Marelli

Osram

Philips Automotive Lighting

ZKW Group

Varroc Lighting Systems

SL Corporation

Ichikoh Industries

Flex-N-Gate

TYC Genera

Depo Auto Parts

Anzo USA

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now