Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Lithium-Ion Batteries Market is valued at USD ~ billion based on a recent historical assessment derived from U.S. Department of Energy manufacturing statistics and corporate financial disclosures. Growth is driven by expanding electric vehicle production, rising grid-scale energy storage deployments, and federal manufacturing incentives under the Inflation Reduction Act. Accelerated gigafactory construction across multiple states further strengthens domestic supply capacity and supports increasing battery demand across automotive and stationary applications.

California, Texas, Michigan, Ohio, and Georgia dominate the USA Lithium-Ion Batteries Market due to large-scale electric vehicle manufacturing, established automotive ecosystems, and multi-billion-dollar battery plant investments. Michigan and Ohio benefit from legacy automotive infrastructure transitioning toward electrification, while Texas and Georgia attract new gigafactory projects supported by state-level incentives and logistics advantages. California leads in EV adoption and energy storage installations, reinforcing regional battery demand concentration.

Market Segmentation

By Product Type

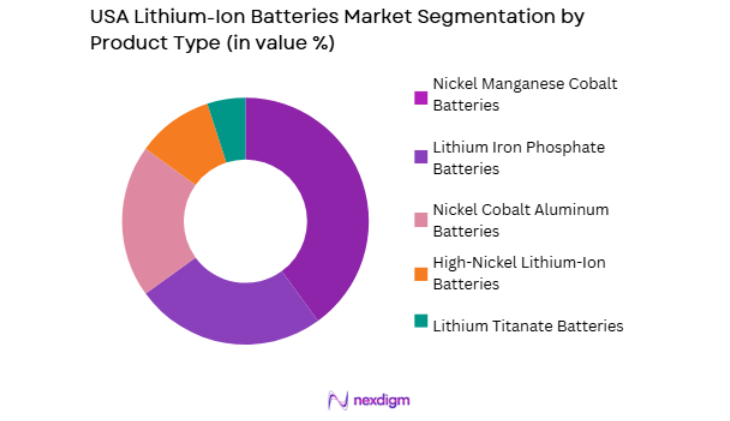

USA Lithium-Ion Batteries Market is segmented by product type into Nickel Manganese Cobalt Batteries, Lithium Iron Phosphate Batteries, Nickel Cobalt Aluminum Batteries, Lithium Titanate Batteries, and High-Nickel Lithium-Ion Batteries. Recently, Nickel Manganese Cobalt Batteries has a dominant market share due to high energy density, strong compatibility with long-range electric vehicles, and widespread OEM adoption. Major automakers prioritize NMC chemistry for its balanced performance in power output, safety, and lifecycle durability. Established supplier networks and manufacturing scalability support consistent deployment across passenger and commercial electric vehicles. Federal incentives promoting domestic battery production have further reinforced large-scale NMC cell manufacturing investments. Continuous improvements in cathode formulations and thermal management systems enhance reliability and cost efficiency, sustaining the segment’s leadership in the overall lithium-ion landscape.

By Platform Type

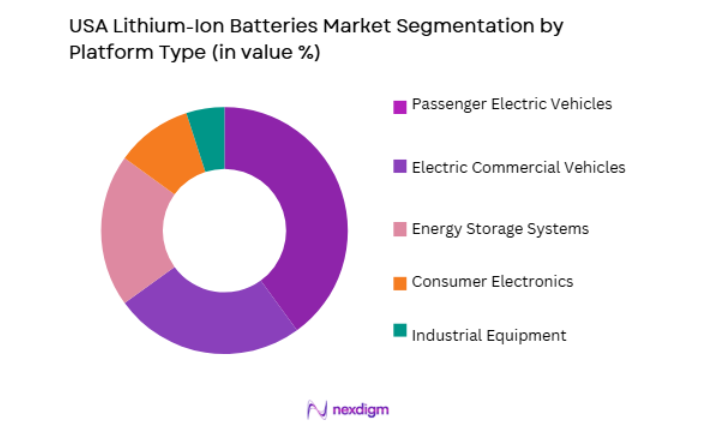

USA Lithium-Ion Batteries Market is segmented by platform type into Passenger Electric Vehicles, Electric Commercial Vehicles, Energy Storage Systems, Consumer Electronics, and Industrial Equipment. Recently, Passenger Electric Vehicles has a dominant market share due to rapid model expansion, growing consumer demand, and increasing driving range expectations. Automotive OEMs deploy high-capacity battery packs to meet performance benchmarks and regulatory emission targets. Federal tax credits and infrastructure expansion contribute to higher EV registrations, directly stimulating lithium-ion battery demand. Passenger EV platforms account for larger cumulative installed battery capacity compared to other segments. Additionally, premium electric SUVs and pickup trucks require larger pack sizes, increasing total revenue concentration within this platform segment.

Competitive Landscape

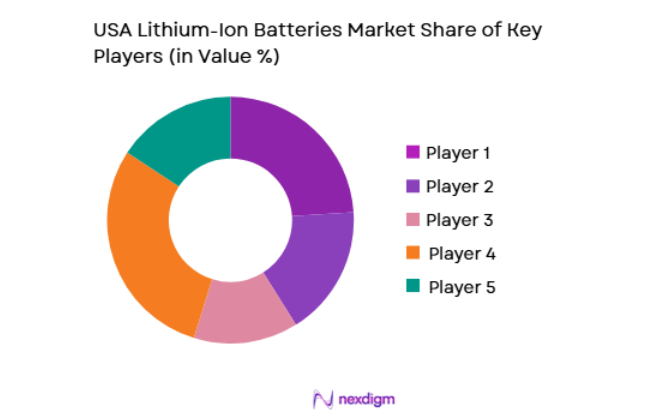

The USA Lithium-Ion Batteries Market is characterized by strategic joint ventures, vertical integration between automakers and cell manufacturers, and large-scale domestic production expansion. Leading companies focus on advanced chemistries, localized mineral sourcing, and proprietary battery management systems to strengthen competitive positioning. High capital intensity and technology specialization create substantial entry barriers, reinforcing the dominance of established manufacturers.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Domestic Manufacturing Footprint |

| Tesla | 2003 | Texas | ~ | ~ | ~ | ~ | ~ |

| Panasonic Energy | 1918 | Nevada | ~ | ~ | ~ | ~ | ~ |

| LG Energy Solution | 2020 | Michigan | ~ | ~ | ~ | ~ | ~ |

| SK On | 2021 | Georgia | ~ | ~ | ~ | ~ | ~ |

| Samsung SDI | 1970 | South Korea | ~ | ~ | ~ | ~ | ~ |

USA Lithium-Ion Batteries Market Analysis

Growth Drivers

Federal Incentives and Domestic Manufacturing Expansion

The Inflation Reduction Act has introduced production-linked tax credits for battery cell and module manufacturing, significantly reducing effective production costs for domestic facilities. These incentives encourage automakers and battery producers to establish localized gigafactories to qualify for financial benefits tied to domestic content thresholds. As a result, multi-billion-dollar investments have been announced across several states, increasing annual gigawatt-hour capacity and strengthening supply chain resilience. Localization reduces dependence on imported cells and improves long-term price stability for automotive OEMs. State-level incentives complement federal measures, creating competitive industrial clusters that attract additional capital inflows. Domestic production also supports workforce development and strengthens vertical integration between automakers and suppliers. This policy-driven expansion directly increases lithium-ion output volumes and stimulates innovation in cell design and manufacturing automation. Sustained regulatory backing enhances investor confidence and reinforces long-term market stability.

Electrification of Transportation and Grid Storage Integration

Rapid growth in electric vehicle adoption is significantly increasing lithium-ion battery demand across passenger, commercial, and fleet segments. Automotive manufacturers continue to launch new electric SUVs, trucks, and performance vehicles requiring large-capacity battery packs, expanding cumulative deployment volume. Charging infrastructure expansion reduces range anxiety and supports consumer adoption. Fleet electrification initiatives in logistics and municipal services further amplify battery consumption. Simultaneously, utility companies deploy lithium-ion systems for grid-scale energy storage to balance renewable power variability. Solar and wind integration projects increasingly rely on battery storage to stabilize output and improve grid reliability. Technological improvements in battery management systems enhance safety and lifecycle durability, strengthening end-user confidence. The combined growth of transportation electrification and stationary energy storage establishes a diversified demand base, reinforcing sustained lithium-ion market expansion.

Market Challenges

Critical Mineral Supply Volatility and Import Dependence

The USA Lithium-Ion Batteries Market remains exposed to fluctuations in lithium, nickel, and cobalt supply chains, which directly influence production costs and margin stability. Concentration of mineral extraction and refining outside domestic borders introduces geopolitical risk and trade uncertainties. Price volatility complicates long-term procurement planning and increases financial exposure for manufacturers. Domestic mining projects face environmental permitting delays, limiting near-term supply diversification. Recycling infrastructure is expanding but remains insufficient to offset primary mineral demand at current scale. Manufacturers must secure long-term supply contracts to mitigate risks, reducing procurement flexibility. Transportation and logistics disruptions can further affect material availability. These structural challenges create cost unpredictability and strategic vulnerability across the value chain.

High Capital Expenditure and Technological Transition Uncertainty

Establishing advanced lithium-ion gigafactories requires substantial capital investment in automation systems, cleanroom facilities, and quality control infrastructure. Rapid evolution of battery chemistries increases the risk of technology obsolescence before capital recovery is achieved. Companies must simultaneously invest in research for next-generation chemistries such as solid-state systems while maintaining existing production lines. Skilled workforce shortages in battery engineering and manufacturing further elevate operational complexity. Equipment calibration and safety compliance standards require continuous updates, adding to operational costs. Production ramp-up delays may impact supply agreements with automotive OEMs. Cybersecurity risks associated with advanced manufacturing automation also require mitigation investments. These financial and technological pressures increase competitive intensity and raise barriers for new entrants.

Opportunities

Commercialization of Solid-State and High-Energy-Density Chemistries

Transitioning toward solid-state battery architectures presents significant opportunities to enhance energy density, safety, and charging performance. Solid electrolytes reduce flammability risk and enable compact battery pack designs suitable for long-range electric vehicles. Federal research funding and venture capital investments are accelerating pilot production programs across the United States. Early commercialization in premium EV segments may validate performance advantages before mass-market scaling. Intellectual property development in advanced chemistries strengthens domestic technological leadership. Improved cycle life and faster charging capabilities enhance consumer value propositions. Collaboration between automakers and technology startups accelerates innovation cycles. Successful deployment of next-generation chemistries could redefine competitive dynamics within the lithium-ion ecosystem.

Expansion of Battery Recycling and Second-Life Applications

Increasing volumes of end-of-life EV batteries create opportunities for large-scale recycling facilities capable of recovering lithium, cobalt, and nickel. Advanced hydrometallurgical processes improve material recovery rates and reduce environmental impact. Closed-loop supply agreements between automakers and recyclers enhance mineral security and sustainability compliance. Second-life battery applications in stationary energy storage systems extend asset utilization beyond automotive use. Utility operators adopt repurposed battery modules for renewable integration and grid balancing. Federal incentives supporting circular economy initiatives further stimulate recycling infrastructure development. Reduced reliance on imported raw materials strengthens domestic supply chains. These recycling and second-life ecosystems present long-term economic and environmental benefits for industry participants.

Future Outlook

The USA Lithium-Ion Batteries Market is projected to expand steadily over the next five years, supported by sustained EV adoption and continued gigafactory capacity expansion. Advancements in high-energy-density chemistries and recycling technologies will enhance efficiency and sustainability. Regulatory incentives and localization strategies are expected to maintain strong capital inflows. Diversification across automotive and stationary energy storage applications will reinforce long-term demand stability.

Major Players

- Tesla

- Panasonic Energy

- LG Energy Solution

- SK On

- Samsung SDI

- CATL North America

- Envision AESC

- General Motors

- Ford Motor Company

- Quantum Scape

- Solid Power

- Microvast

- Sila Nanotechnologies

- FREYR Battery

- Northvolt

Key Target Audience

- Automotive OEMs

- Battery Cell Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Fleet Operators

- Utility and Grid Operators

- Raw Material Suppliers

- Energy Storage Integrators

Research Methodology

Step 1: Identification of Key Variables

Key demand and supply variables including EV sales, gigawatt-hour production capacity, mineral sourcing, and policy incentives were identified. Quantitative indicators such as installed battery capacity and average pack cost were mapped to structural growth trends.

Step 2: Market Analysis and Construction

Primary interviews with industry participants were combined with secondary data from federal agencies and corporate financial reports. Market sizing integrated revenue benchmarking and capacity analysis for validation.

Step 3: Hypothesis Validation and Expert Consultation

Findings were validated through expert consultations with battery engineers, automotive strategists, and policy specialists. Cross-verification ensured alignment with investment and regulatory developments.

Step 4: Research Synthesis and Final Output

All data streams were consolidated into structured insights supported by financial modeling and comparative evaluation. The final output integrates quantitative evidence with strategic interpretation for decision-making support.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid electrification of transportation sector

Expansion of domestic gigafactory production capacity

Federal incentives promoting battery localization - Market Challenges

Volatility in lithium and nickel raw material pricing

High capital intensity of battery manufacturing facilities

Recycling infrastructure scalability constraints - Market Opportunities

Commercialization of next-generation high energy density chemistries

Growth of stationary energy storage integration

Expansion of domestic mineral processing capabilities - Trends

Shift toward high-nickel and LFP chemistries

Integration of advanced battery management systems

Strategic vertical integration between OEMs and cell manufacturers - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Nickel Manganese Cobalt Batteries

Lithium Iron Phosphate Batteries

Nickel Cobalt Aluminum Batteries

Lithium Titanate Batteries

High-Nickel Lithium-Ion Batteries - By Platform Type (In Value%)

Passenger Electric Vehicles

Electric Commercial Vehicles

Energy Storage Systems

Consumer Electronics

Industrial Equipment - By Fitment Type (In Value%)

OEM Integration

Aftermarket Replacement

Modular Battery Packs

Integrated Battery Systems

Swappable Battery Systems - By EndUser Segment (In Value%)

Automotive OEMs

Utility and Grid Operators

Electronics Manufacturers

Fleet Operators

Industrial Enterprises - By Procurement Channel (In Value%)

Long-Term Supply Agreements

Direct OEM Contracts

Government Procurement Programs

- Market Share Analysis

- Cross Comparison Parameters (Cost per kWh, Charging Speed Capability, Cycle Life Performance, Raw Material Sourcing Strategy, Manufacturing Capacity, Recycling Integration, Technology Maturity, Safety Certification Standards, Supply Chain Localization, Strategic Partnerships, R&D Investment Intensity, Gigafactory Footprint)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Tesla

Panasonic Energy

LG Energy Solution

SK On

Samsung SDI

CATL North America

Envision AESC

General Motors

Ford Motor Company

Quantum Scape Solid Power

Microvast

Sila Nanotechnologies

FREYR Battery

Northvolt

- Automotive OEMs accelerating EV production requiring large battery volumes

- Utility operators deploying lithium-ion storage for grid stability

- Electronics manufacturers integrating compact high-density cells

- Fleet operators transitioning to electric commercial vehicles

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now