Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA mobile monitoring devices market is valued at USD ~ billion (prior year) and USD ~ billion (current year), supported by a strong pipeline of medically relevant wearables and a widening set of use cases that blend consumer convenience with clinical monitoring needs. Growth is driven by higher utilization of wearables for cardiometabolic management and remote observation, alongside provider and payer interest in longitudinal data that supports early detection, adherence, and escalation protocols across care settings.

The market is concentrated around innovation and deployment hubs such as San Diego (CGM and digital health device ecosystems), the San Francisco Bay Area (wearable-device product engineering, software platforms, and cardiac monitoring innovators), Boston/Cambridge (medtech R&D and clinical validation density), and Minneapolis–St. Paul (large-scale medical device manufacturing and hospital procurement connectivity). These hubs lead due to proximity to top health systems, regulatory talent, clinical trial networks, and established device supply chains enabling faster commercialization.

Market Segmentation

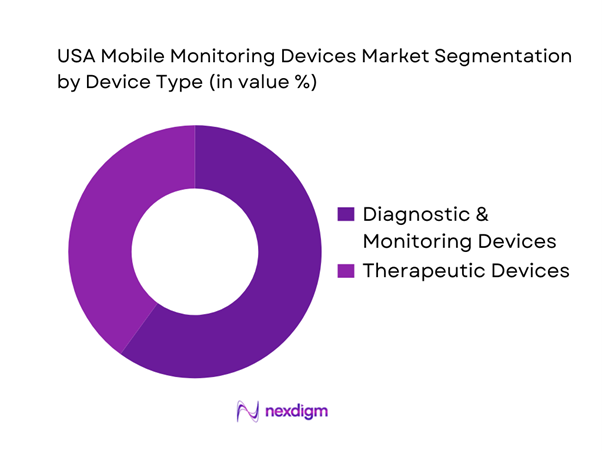

By Device Type

The USA mobile monitoring devices market is segmented by device type into diagnostic & monitoring devices and therapeutic devices. Recently, diagnostic & monitoring devices hold a dominant share because the US market’s primary value creation is still centered on continuous data capture (heart rhythm, glucose, SpO₂, activity/sleep proxies) that can be used to detect deterioration earlier, reduce avoidable utilization, and support structured clinical workflows. These products also scale faster because they are repeatable, non-invasive, and can be deployed broadly across chronic disease cohorts with minimal training. In contrast, therapeutic wearables typically face narrower indications, deeper clinical protocol requirements, and higher friction around outcomes attribution. As monitoring platforms mature (device + app + cloud + clinician dashboard), the monitoring segment also benefits from bundling and subscription models that monetize engagement and longitudinal data utility across multiple use cases rather than a single episode of care.

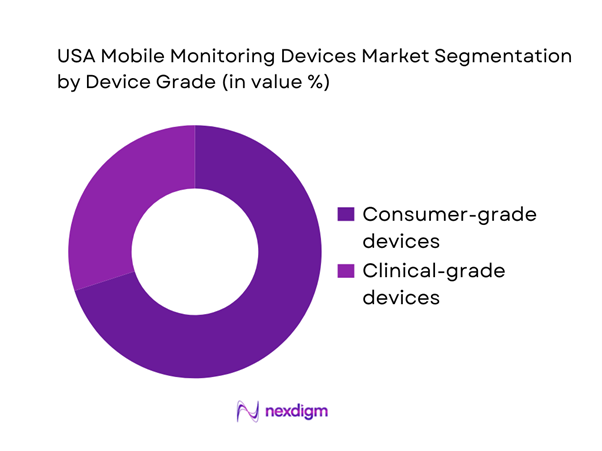

By Device Grade

The market is segmented by device grade into consumer-grade mobile monitoring devices and clinical-grade mobile monitoring devices. Recently, consumer-grade devices dominate because they are distributed at scale through retail and direct-to-consumer channels, have lower onboarding friction, and increasingly include sensor stacks that overlap with medical monitoring needs (heart rhythm features, oxygen saturation, temperature trends, sleep proxies). This segment benefits from large installed bases, frequent device refresh cycles, and engagement-led ecosystems that keep users active within companion apps—creating a larger pool of longitudinal data. Clinical-grade devices remain essential for diagnosis-grade accuracy and specific care pathways, but deployment is limited by procurement cycles, compliance requirements, and workflow constraints (integration, staffing for monitoring, and escalation governance). As consumer devices continue to add clinically relevant capabilities, they are increasingly used as the front door to monitoring—while clinical-grade solutions capture patients when precision, documentation, and high-acuity protocols are required.

Competitive Landscape

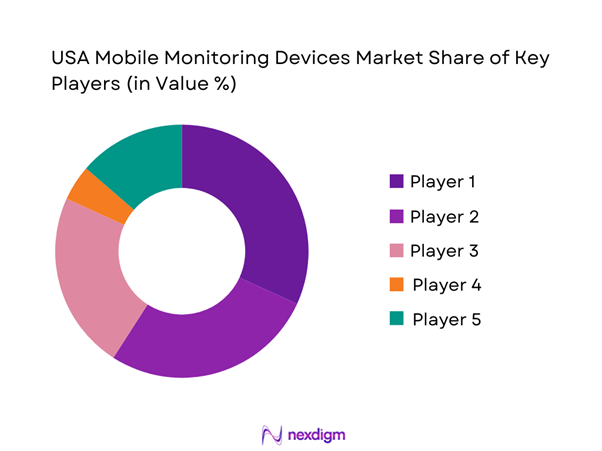

The USA mobile monitoring devices market is dominated by a set of high-influence players spanning CGM leaders, enterprise medical device OEMs, and consumer ecosystem giants. This consolidation reflects the importance of sensor accuracy, regulatory readiness, platform ecosystems, and distribution reach (health system procurement, pharmacy/retail, payer relationships, and DTC). Scale players are advantaged because they can invest in validation, cybersecurity posture, and software analytics while running national distribution and customer support operations.

| Company | Est. Year | Headquarters | Primary Monitoring Focus | Flagship Form Factors | Connectivity Model | Clinical / Regulatory Positioning | Platform & Interoperability Depth | Primary US Channels | Differentiation Lever |

| Dexcom | 1999 | San Diego, CA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Abbott | 1888 | Abbott Park, IL | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Apple | 1976 | Cupertino, CA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| Medtronic | 1949 | Operational HQ: Minneapolis, MN | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

| iRhythm | 2006 | San Francisco, CA | ~ | ~ | ~ | ~ | ~ | ~ | ~ |

USA Mobile Monitoring Devices Market Analysis

Growth Drivers

Expansion of remote patient monitoring programs

Remote patient monitoring (RPM) is scaling in the U.S. because it fits the cost-and-capacity math of caring for a large insured population with limited clinical bandwidth. Medicare’s scale matters: the program’s own reporting shows approximately ~ Medicare beneficiaries in the U.S., which expands the reachable pool for device-enabled monitoring pathways. On the utilization side, federal oversight work found slightly more than ~ Medicare enrollees received RPM and that RPM length-of-service averaged more than ~ months for monitored enrollees—evidence that programs are moving beyond pilots into repeatable care operations. Macro fundamentals reinforce this shift: the U.S. GDP of USD ~ and population of ~ enable sustained payer and provider investment in device-enabled chronic care models that reduce avoidable in-person utilization. As health systems standardize RPM workflows (device onboarding + data review + clinician touchpoints), monitoring devices become embedded in care pathways for hypertension, diabetes-related complications, and post-acute follow-up, raising baseline device throughput and replacement cycles (without needing one-off specialty clinics to drive volume).

Rising chronic disease burden

Mobile monitoring devices (BP cuffs, glucose-linked peripherals, pulse oximeters, ECG patches, multi-parameter wearables) are pulled by the clinical reality that cardiometabolic disease remains a high-frequency, high-cost care driver. Coronary heart disease killed ~ people and the U.S. recorded ~ resident deaths, creating a demand signal for earlier detection, tighter control, and continuous monitoring to prevent deterioration and readmissions. Medicare’s RPM oversight analysis further shows the clinical mix behind monitored care: hypertension is the most common condition, with diabetes-related diagnoses also prominent among monitored enrollees, meaning device categories tied to BP, weight, oxygenation, and glycemic risk sit at the center of deployment. Macro conditions also matter for adoption at scale: U.S. GDP per capita of USD ~ and net migration of ~ support continued expansion of insured and working-age populations that drive outpatient monitoring demand across primary care and specialty networks. Together, these indicators support why providers are operationalizing monitoring-as-standard-care for chronic disease management, as patient volumes and clinical risk loads remain persistently large and well aligned with quantifiable home physiologic signals.

Challenges

Data overload and alert fatigue

Data overload is a real constraint because monitoring scale is now large enough to flood clinical teams unless programs engineer filtering, escalation tiers, and measurement governance. Medicare oversight indicates RPM is not niche: ~ enrollees received RPM and the average monitoring duration exceeded ~ months, which implies sustained streams of readings and alerts that must be reviewed or triaged. Hospital-at-home compounds the load: reporting shows about ~ acute discharges in a measured period and ~ cumulative discharges since inception, with each discharge implying multiple daily vitals and symptom checks that can generate escalations. Macro conditions reinforce why this becomes systemic: the U.S. operates at a national scale of ~ people with an economy of USD ~, so even modest per-patient data volumes quickly become millions of device-days across provider networks. Without governance (frequency protocols, patient-specific thresholds, and staffing models), monitoring teams can be pulled into non-actionable alerts, slowing response for true deterioration events and reducing clinician trust in device data streams.

Interoperability and EHR integration complexity

Integration complexity shows up when device data must be mapped, validated, and written into EHRs in a clinically usable way (flowsheets, problem lists, task queues, and billing documentation). While U.S. hospitals have improved exchange, the broader point for mobile monitoring is that exchange exists does not mean device signals are usable inside the clinician workflow. Hospitals engaged in all four domains of interoperable exchange account for ~, which still leaves a sizable portion of hospitals and clinics with partial capability or inconsistent integration routines, especially for non-EHR-native device feeds. On the RPM side, oversight found approximately ~ of RPM enrollees did not receive all ~ components of RPM, signaling fragmented workflows across setup, data transmission, and clinical management that are often rooted in integration gaps and operational handoffs. Macro conditions keep this challenge high-stakes, as U.S. health systems operate with GDP per capita of USD ~ and total GDP of USD ~, running complex multi-vendor stacks where integration debt becomes expensive and slow to unwind.

Opportunities

AI-assisted clinical triage

The opportunity is to convert raw monitoring streams into prioritized clinical work by using regulated, auditable AI to reduce noise and focus clinician time on deterioration risk. Communications on regulated AI tooling show rapid expansion, with the AI/ML-enabled medical device list including ~ authorized devices, indicating a broad regulatory footprint for AI components embedded into monitoring workflows such as signal interpretation, trend classification, and prioritization. On the demand side, RPM scale provides the throughput AI triage needs to matter operationally, as ~ Medicare enrollees received RPM and average monitoring exceeded ~ months, creating sustained longitudinal datasets where AI can suppress non-actionable variance and elevate true risk. Hospital-at-home adds another high-value zone, with ~ cumulative discharges implying thousands of acute episodes managed remotely where triage speed matters clinically and financially. Macro capacity constraints reinforce the business case, as an economy of USD ~ still faces productivity pressure, making AI-enabled reduction of review burden a credible procurement priority when integrated and clinically governed.

Multi-parameter device convergence

Convergence is a growth opportunity because providers prefer fewer devices with higher clinical yield per patient, reducing logistics, training, and failure points. The RPM ecosystem already trends toward multi-signal care pathways, with monitoring most often used for chronic conditions like hypertension and monitoring durations exceeding ~ months, making single-condition, single-sensor kits less efficient over long enrollment periods. Hospital-at-home further rewards convergence, with ~ cumulative discharges since inception requiring bundles of vital signs and symptom tracking that favor integrated kits rather than separate disconnected devices. Regulatory direction supports convergence, as the AI/ML device list reaching ~ authorized devices signals that software-defined features such as trend detection and risk scoring are becoming part of the device package, enabling one device, many insights positioning. Macro scale makes standardization valuable, as a population of ~ people means even small reductions in device SKUs, returns, and support tickets can translate into large operational savings for national payers and health systems, supporting market pull for converged, enterprise-manageable monitoring portfolios.

Future Outlook

Over the next five to six years, the USA mobile monitoring devices market is expected to accelerate as monitoring shifts from device purchase to continuous programs embedded into home care, chronic disease pathways, and post-acute transitions. The market’s next phase will be shaped by multi-parameter convergence, stronger software-led differentiation, and deeper workflow integration that reduces clinician burden. As platforms mature, procurement will increasingly favor vendors that combine validated sensors, scalable logistics, and interoperable data pipelines.

Major Players

- Philips

- GE HealthCare

- Medtronic

- Baxter

- Masimo

- Nonin Medical

- Dexcom

- Abbott

- ResMed

- iRhythm Technologies

- AliveCor

- Withings Health Solutions

- Omron Healthcare

- Garmin Health

Key Target Audience

- Medical device manufacturers & OEM product strategy teams

- Healthcare providers and IDN procurement leaders

- Remote care / virtual care program operators

- Payers and managed care organizations

- Pharmacy and retail health operators

- Digital health platforms and device-data aggregation providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

We construct a complete ecosystem map of device OEMs, platform vendors, channels, and buyers across the USA mobile monitoring devices market. This is supported by structured desk research from secondary sources and commercial databases, with emphasis on defining measurable variables such as device categories, clinical use cases, and channel mechanics.

Step 2: Market Analysis and Construction

We compile historical market data and validate category boundaries (wearable medical devices vs monitoring systems vs consumer wearables). The build uses triangulation across shipment signals, vendor positioning, and program adoption indicators to ensure category consistency and eliminate double counting.

Step 3: Hypothesis Validation and Expert Consultation

We develop market hypotheses and validate them through expert consultations using computer-assisted interviews with stakeholders across OEMs, provider programs, and channel partners. Inputs focus on commercialization realities such as onboarding friction, returns, usage adherence, and workflow integration patterns.

Step 4: Research Synthesis and Final Output

We synthesize findings into a structured market model and qualitative competitive narrative, reconciling differences between secondary sources and practitioner feedback. Final output prioritizes segment logic, buyer behavior, and program economics, ensuring decision-grade insights for strategy, investment, and go-to-market planning.

- Executive Summary

- Research Methodology (Market definitions and inclusions/exclusions, device taxonomy, abbreviations, data triangulation framework, bottom-up shipment modeling, top-down claims and reimbursement validation, primary interviews with providers payers DME OEMs, channel checks across IDNs retail and e-commerce, regulatory mapping FDA FCC, limitations and assumptions)

- Definition and Scope

- Overview Genesis

- Industry Timeline

- Business Cycle

- Supply Chain and Value Chain Analysis

- Growth Drivers

Expansion of remote patient monitoring programs

Rising chronic disease burden

Hospital-at-home adoption

Digital transformation of clinical workflows - Challenges

Data overload and alert fatigue

Interoperability and EHR integration complexity

Patient adherence and device return rates

Cybersecurity and data privacy risks - Opportunities

AI-assisted clinical triage

Multi-parameter device convergence

Value-based care monitoring programs

Payer-sponsored preventive monitoring - Trends

Shift toward cellular-first monitoring devices

Growth of patch-based cardiology monitoring

Consumer-to-clinical device upgrades - Regulatory & Policy Landscape

- SWOT Analysis

- Stakeholder & Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Average Selling Price, 2019–2024

- By Application (in Value %)

Wearable ECG and cardiac patches

Blood pressure monitors

Pulse oximeters

Continuous glucose monitoring systems

Multi-parameter wearable monitors - By Technology Architecture (in Value %)

Single-parameter monitoring devices

Multi-parameter integrated monitoring devices

Patch-based monitoring platforms

Sensor plus platform bundled architectures

AI-enabled analytics-integrated devices - By Connectivity Type (in Value %)

Bluetooth smartphone-dependent devices

Cellular embedded monitoring devices

Wi-Fi enabled monitoring devices

Gateway or hub-based monitoring kits

Store-and-forward monitoring systems - By End-Use Industry (in Value %)

Hospitals and IDNs

Home healthcare providers

Ambulatory clinics and physician groups

Payers and employer health programs

Retail and consumer health monitoring - By Region (in Value %)

Northeast

Midwest

South

West

- Market share snapshot of major players

- Cross Comparison Parameters (FDA clearance footprint, RPM reimbursement readiness, connectivity architecture, signal quality and clinical performance, interoperability depth, cybersecurity and software update model, deployment and operations capability, commercial model and unit economics)

- SWOT of major players

- Product and SKU benchmarking

- Channel and partnership benchmarking

- Company Profiles

Philips

GE HealthCare

Medtronic

Baxter

Masimo

Nonin Medical

Dexcom

Abbott

ResMed

iRhythm Technologies

VitalConnect

AliveCor

Withings Health Solutions

Omron Healthcare

- Market demand and utilization patterns

- Purchasing power and budget allocations

- Needs desires and pain point analysis

- Decision-making process

- Vendor selection criteria

- Implementation and scale playbook

- By Value, 2025–2030

- By Volume, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now