Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Night Vision Systems market is valued at USD ~ billion based on a recent historical assessment derived from U.S. Department of Defense procurement disclosures and company financial reports of leading defense electronics manufacturers. Demand is primarily driven by modernization programs focused on soldier lethality and situational awareness, expansion of homeland security surveillance capabilities, and increased procurement of advanced imaging systems for tactical operations. Continuous upgrades in image intensification and thermal imaging technologies further stimulate replacement cycles and system integration initiatives across federal agencies.

Washington D.C., Arlington, and Huntsville dominate the USA Night Vision Systems market due to their proximity to defense command centers, federal procurement agencies, and major prime contractors. California and Texas also play critical roles, supported by advanced optics manufacturing clusters and defense technology innovation hubs. These regions benefit from sustained federal budget allocations, established supply chain ecosystems, and strong collaboration between military end users and technology developers, reinforcing their operational and procurement leadership within the national market.

Market Segmentation

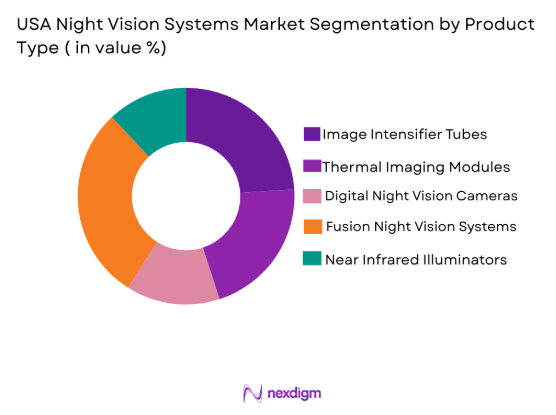

By Product Type

USA Night Vision Systems market is segmented by product type into Image Intensifier Tubes, Thermal Imaging Modules, Digital Night Vision Cameras, Fusion Night Vision Systems, and Near Infrared Illuminators. Recently, Fusion Night Vision Systems has a dominant market share due to enhanced operational capability combining thermal detection with image intensification clarity, improved target recognition in complex environments, strong adoption in military modernization programs, broader compatibility with vehicle and helmet mounted platforms, and sustained federal procurement focus on advanced battlefield visualization technologies.

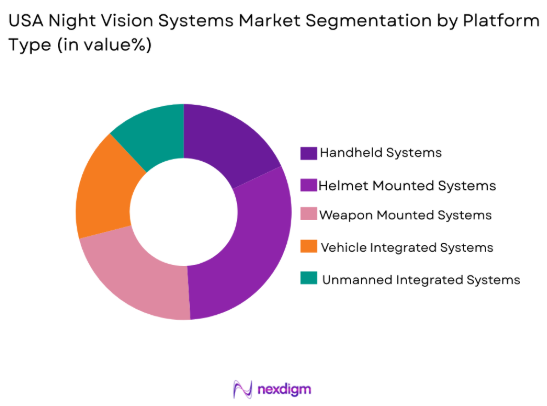

By Platform Type

USA Night Vision Systems market is segmented by platform type into Handheld Systems, Helmet Mounted Systems, Weapon Mounted Systems, Vehicle Integrated Systems, and Unmanned Platform Integrated Systems. Recently, Helmet Mounted Systems has a dominant market share due to rising demand for hands free tactical operations, enhanced soldier mobility requirements, integration with augmented reality overlays, compatibility with advanced combat helmets, and sustained Department of Defense procurement initiatives prioritizing wearable situational awareness technologies.

Competitive Landscape

The USA Night Vision Systems market is moderately consolidated, characterized by strong presence of defense primes and specialized electro optics manufacturers with long term federal contracts. Major players influence pricing, innovation cycles, and procurement standards through vertically integrated supply chains and proprietary imaging technologies. Competitive advantage is largely determined by resolution performance, sensor integration capabilities, ruggedization standards, and compliance with federal export controls.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Primary Defense Contract Exposure |

| L3Harris Technologies | 2019 | Florida, USA | ~ | ~ | ~ | ~ | ~ |

| Elbit Systems of America | 1990 | Texas, USA | ~ | ~ | ~ | ~ | ~ |

| BAE Systems Inc | 1999 | Virginia, USA | ~ | ~ | ~ | ~ | ~ |

| Leonardo DRS | 1968 | Virginia, USA | ~ | ~ | ~ | ~ | ~ |

| Teledyne Technologies | 1960 | California, USA | ~ | ~ | ~ | ~ | ~ |

USA Night Vision Systems market Market Analysis

Growth Drivers

Defense Modernization Programs Focused on Enhanced Soldier Lethality and Situational Awareness

The significantly driving the USA Night Vision Systems market as federal defense budgets prioritize advanced optical technologies for ground forces, special operations units, and tactical law enforcement agencies. The integration of fusion night vision systems into next generation combat helmets and weapon platforms has accelerated procurement cycles, with defense agencies allocating substantial funding toward advanced electro optics procurement contracts. These modernization initiatives emphasize improved detection range, high resolution imaging clarity, and seamless integration with command and control systems, thereby increasing average system value and technological sophistication. Government funded research partnerships with private manufacturers further stimulate innovation pipelines, resulting in rapid development of lightweight, energy efficient, and digitally enhanced systems tailored for modern warfare environments. Increased geopolitical uncertainties and border surveillance requirements contribute to expanded acquisition programs that strengthen long term demand stability. Replacement of legacy image intensifier tubes with white phosphor and multi spectral fusion systems further expands upgrade cycles, encouraging recurring procurement activities. As defense agencies aim to enhance operational readiness and nighttime mission effectiveness, night vision systems are becoming standard issue equipment across multiple operational tiers. The emphasis on interoperability between night vision devices and communication networks reinforces system integration investments and supports sustained revenue growth for established manufacturers.

Expansion of Homeland Security and Border Surveillance Investments

An acting as a major growth catalyst for the USA Night Vision Systems market as federal and state agencies allocate higher budgets toward advanced surveillance and reconnaissance infrastructure. Increasing emphasis on perimeter security, coastal monitoring, and cross border threat detection has led to the procurement of thermal imaging and digital night vision solutions integrated into fixed and mobile surveillance units. These investments support enhanced situational awareness capabilities in low light and adverse weather conditions, strengthening operational effectiveness for border patrol and homeland security personnel. Deployment of vehicle integrated and unmanned platform compatible night vision technologies enables real time intelligence gathering across expansive terrains, thereby expanding application diversity beyond traditional military use. Public safety initiatives targeting critical infrastructure protection further contribute to demand for high performance imaging modules capable of long range detection. Collaboration between defense contractors and security agencies fosters customization of systems tailored to domestic surveillance requirements, reinforcing sustained procurement pipelines. Funding allocations from federal security programs create predictable revenue streams that stabilize manufacturer investments in research and development. As surveillance mandates evolve with technological advancements, adoption of AI enabled night vision analytics enhances threat identification efficiency and strengthens long term market expansion prospects.

Market Challenges

Strict Export Control Regulations and Compliance Constraints Under Federal Defense Laws

present a significant challenge for the USA Night Vision Systems market as manufacturers must adhere to International Traffic in Arms Regulations and related compliance frameworks governing sensitive optical technologies. These regulatory obligations restrict cross border sales, limit international expansion opportunities, and increase administrative overhead for defense contractors engaged in global distribution. Licensing procedures for advanced image intensification and thermal imaging modules can extend procurement timelines and introduce uncertainties in international contract negotiations. Compliance costs associated with documentation, audit requirements, and cybersecurity safeguards add financial burden to small and medium sized manufacturers seeking entry into defense supply chains. Restrictions on technology transfer also constrain collaborative research initiatives with foreign partners, potentially limiting innovation scalability. Complex classification standards for multi spectral and fusion systems require rigorous review processes before approval, delaying revenue realization from export markets. Heightened scrutiny of defense electronics exports can lead to contractual risks if compliance standards are not meticulously maintained. These regulatory complexities collectively increase operational risk and restrict the pace at which companies can diversify revenue streams beyond domestic federal procurement.

High Research and Development Expenditure with Rapid Technological Obsolescence

creates structural pressure within the USA Night Vision Systems market as manufacturers must continuously invest in next generation imaging solutions to maintain competitive positioning. Advanced electro optical engineering demands significant capital allocation toward semiconductor fabrication, sensor miniaturization, and integration of digital processing capabilities. As technological cycles shorten, newly developed systems risk becoming outdated within a few procurement cycles due to advancements in sensor resolution, power efficiency, and multi spectral capabilities. This dynamic necessitates continuous reinvestment in innovation, increasing financial exposure for companies dependent on long term defense contracts. Development of ruggedized systems capable of operating in extreme environments requires extensive testing and certification processes, adding to cost burdens and elongating commercialization timelines. Smaller suppliers may face barriers in sustaining innovation pipelines without consistent federal contract support. Additionally, procurement agencies often require backward compatibility and system interoperability, complicating design transitions between legacy and advanced platforms. The necessity to balance performance improvements with affordability constraints further compresses profit margins, intensifying competitive pressure among established manufacturers.

Opportunities

Integration of Artificial Intelligence and Data Analytics into Advanced Night Vision Platforms

presents a significant opportunity for the USA Night Vision Systems market as defense and security agencies increasingly demand intelligent threat recognition capabilities beyond conventional imaging performance. AI driven target detection algorithms enhance situational awareness by automatically identifying potential threats within low visibility environments, thereby reducing operator fatigue and improving response efficiency. Incorporation of machine learning models into digital night vision cameras enables continuous performance optimization through adaptive image processing techniques. This technological advancement creates new revenue streams for manufacturers capable of offering software driven enhancements layered onto existing hardware platforms. Federal agencies seeking real time battlefield intelligence integration are more likely to invest in network enabled night vision solutions capable of transmitting analyzed data across secure communication channels. The convergence of optical hardware and intelligent analytics strengthens product differentiation and encourages long term service contracts for software upgrades and system maintenance. Manufacturers that successfully integrate AI capabilities can leverage recurring revenue models through data support and algorithm refinement services. As modernization roadmaps increasingly emphasize digital transformation across defense infrastructure, intelligent night vision platforms are positioned to capture expanded procurement budgets and strengthen long term growth trajectories.

Expansion into Commercial and Critical Infrastructure Security Applications

Represents a growing opportunity for the USA Night Vision Systems market as non military sectors adopt advanced imaging technologies for asset protection and surveillance enhancement. Energy facilities, transportation hubs, and industrial complexes are increasingly investing in thermal and digital night vision systems to improve perimeter monitoring and risk mitigation capabilities. Rising awareness of infrastructure vulnerability to unauthorized access and sabotage is driving procurement of high resolution imaging devices capable of long range detection in low light environments. Commercial security providers are integrating vehicle mounted and fixed surveillance night vision modules into their service portfolios, broadening end user diversification for manufacturers. Adoption of cost optimized digital night vision cameras tailored for industrial use expands addressable market size beyond traditional defense procurement channels. Partnerships between electro optical manufacturers and commercial security integrators enable scalable deployment across metropolitan and rural installations. As critical infrastructure modernization initiatives continue to receive federal and private investment, demand for reliable and durable night vision systems is expected to increase. This diversification reduces dependency on exclusive defense contracts and supports more stable revenue distribution across multiple industry verticals.

Future Outlook

The USA Night Vision Systems market is expected to demonstrate steady expansion over the next five years supported by continued defense modernization funding and integration of advanced imaging technologies. Increasing adoption of fusion and AI enabled platforms will strengthen technological differentiation. Regulatory alignment and procurement stability are likely to sustain long term demand. Expanding applications in homeland security and commercial surveillance will further diversify revenue streams.

Major Players

- L3Harris Technologies

- Elbit Systems of America

- BAE Systems Inc

- Leonardo DRS

- Teledyne Technologies

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- Thales Defense and Security Inc

- Sierra Nevada Corporation

- General Dynamics Mission Systems

- FLIR Systems Inc

- Hensoldt USA

- ATN Corporation

- Photonis Defense

- Armasight Inc

Key Target Audience

- Defense Equipment Manufacturers

- Homeland Security Agencies

- Border Protection Authorities

- Military Procurement Departments

- Private Security Firms

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense Electronics Distributors

Research Methodology

Step 1: Identification of Key Variables

Key variables including defense procurement budgets, technology adoption rates, system pricing benchmarks, and regulatory frameworks were identified through structured secondary research and review of federal procurement data. These variables established the analytical foundation for quantitative and qualitative assessment of the USA Night Vision Systems market.

Step 2: Market Analysis and Construction

Comprehensive analysis was conducted using company financial disclosures, government contract announcements, and defense spending reports to construct market size and segmentation estimates. Cross validation with industry experts ensured consistency and reliability of calculated values.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary findings were validated through consultations with defense technology specialists, procurement officers, and supply chain stakeholders to refine assumptions and confirm demand drivers. Feedback loops enhanced analytical precision and minimized estimation bias.

Step 4: Research Synthesis and Final Output

All validated data points were synthesized into a structured analytical framework integrating quantitative metrics and qualitative insights. Final output was prepared following standardized reporting protocols ensuring transparency, accuracy, and relevance.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising defense modernization budgets focused on soldier survivability and situational awareness

Increasing border surveillance and homeland security deployments

Technological advancements in lightweight and high resolution imaging modules

Growing integration of night vision in unmanned ground and aerial systems

Expansion of commercial hunting and wildlife monitoring applications - Market Challenges

High acquisition and lifecycle maintenance costs

Export control restrictions under ITAR and related compliance regimes

Rapid technological obsolescence cycles

Power consumption and battery life constraints in portable devices

Supply chain dependence on specialized semiconductor materials - Market Opportunities

Development of compact fusion systems combining thermal and image intensification

Expansion of night vision integration in autonomous security platforms

Increasing adoption in critical infrastructure protection and industrial monitoring - Trends

Shift toward white phosphor tubes for enhanced contrast and reduced eye strain

Miniaturization of components for helmet mounted and wearable formats

Rising demand for network enabled and data integrated night vision systems

Integration of artificial intelligence for target detection and recognition

Growth in multi spectral imaging capabilities for complex terrains - Government Regulations & Defense Policy

Compliance with International Traffic in Arms Regulations for controlled technologies

Department of Defense modernization roadmaps prioritizing advanced optics

Federal procurement standards emphasizing cybersecurity and interoperability|

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Image Intensifier Based Night Vision Devices

Thermal Imaging Night Vision Systems

Digital Night Vision Systems

Fusion Night Vision Systems

Near Infrared Illuminated Systems - By Platform Type (In Value%)

Handheld and Portable Devices

Helmet Mounted Systems

Weapon Mounted Systems

Vehicle Integrated Systems

Unmanned Platform Integrated Systems - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Retrofit Solutions

Modular Plug and Play Units

Embedded Platform Solutions

Clip On Attachment Systems - By End User Segment (In Value%)

Military and Defense Forces

Homeland Security Agencies

Law Enforcement Departments

Border Protection Units

Commercial and Civilian Users - By Procurement Channel (In Value%)

Direct Government Contracts

Defense Procurement Programs

GSA Schedule Procurement

Private Security Procurement

Authorized Defense Distributors - By Material / Technology (in Value %)

Gallium Arsenide Photocathode Technology

Microbolometer Thermal Sensors

CMOS Based Digital Sensors

White Phosphor Imaging Tubes

Multi Spectral Sensor Fusion Modules

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Technology Type, Resolution Performance, Detection Range, Platform Compatibility, Power Efficiency, System Weight, Integration Capability, Price Tier, Aftermarket Support)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

L3Harris Technologies

Elbit Systems of America

BAE Systems Inc

Raytheon Technologies Corporation

FLIR Systems Inc

Leonardo DRS

Northrop Grumman Corporation

Teledyne Technologies Incorporated

General Dynamics Mission Systems

Hensoldt USA

Sierra Nevada Corporation

ATN Corporation

Armasight Inc

Photonis Defense

Thales Defense and Security Inc

- Military users prioritize ruggedized and high-performance systems for combat readiness

- Homeland security agencies focus on border and coastal surveillance enhancement

- Law enforcement departments adopt compact and vehicle mounted units for tactical operations

- Commercial users emphasize affordability and ease of deployment for recreational and industrial use

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now