Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA On-Board Chargers market is valued at approximately USD ~ based on a recent historical assessment derived from electric vehicle production volumes reported by the U.S. Energy Information Administration and power electronics revenue disclosures from major automotive component suppliers. Market growth is driven by increasing electric vehicle manufacturing, higher onboard charging power requirements, and integration of bidirectional charging capability across passenger and commercial vehicle platforms, alongside OEM electrification strategies and expanding EV model portfolios nationwide.

California, Michigan, Texas, and Tennessee dominate the USA On-Board Chargers market due to concentration of electric vehicle manufacturing plants, automotive powertrain engineering centers, and supplier production facilities. These states benefit from established automotive supply chains, EV assembly investments, and strong OEM–supplier collaboration in electrified drivetrain development. Proximity to semiconductor and power electronics manufacturing hubs further strengthens regional leadership, while policy incentives and workforce specialization sustain advanced charger integration across leading vehicle production clusters.

Market Segmentation

By Product Type

USA On-Board Chargers market is segmented by product type into Single-phase On-board Chargers, Three-phase On-board Chargers, Bidirectional On-board Chargers, Integrated Drive Chargers, and High-power On-board Chargers. Recently, Three-phase On-board Chargers has a dominant market share due to factors such as compatibility with higher-capacity battery packs, faster AC charging performance, and adoption across mid- to high-range electric vehicles. Automotive manufacturers increasingly standardize three-phase architectures to reduce charging time without requiring external DC fast charging, improving daily usability for consumers. Higher voltage and current handling capability supports larger battery capacities common in modern EV platforms, strengthening OEM preference. Suppliers have optimized three-phase charger designs for efficiency, thermal stability, and packaging integration within vehicle platforms, improving cost-effectiveness at scale. Expanding residential and workplace three-phase AC infrastructure in commercial and fleet environments further reinforces demand.

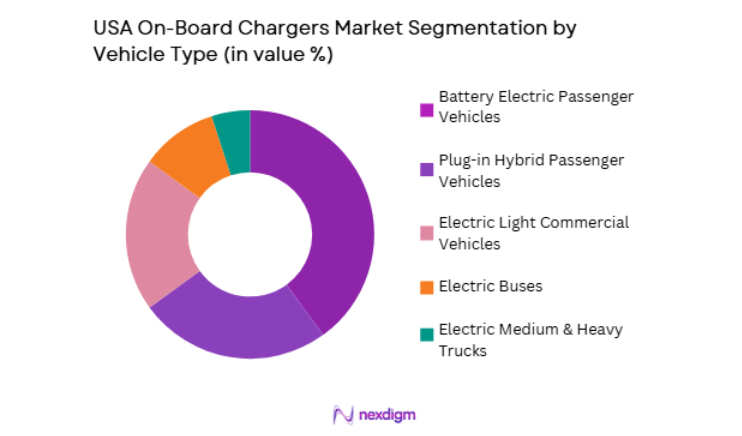

By Vehicle Type

USA On-Board Chargers market is segmented by vehicle type into Battery Electric Passenger Vehicles, Plug-in Hybrid Passenger Vehicles, Electric Light Commercial Vehicles, Electric Buses, and Electric Medium & Heavy Trucks. Recently, Battery Electric Passenger Vehicles has a dominant market share due to factors such as higher production volumes, widespread electrification strategies among automotive OEMs, and consumer shift toward fully electric mobility. Passenger EV platforms require onboard chargers across all vehicle units, creating the largest cumulative demand compared to commercial segments. Automakers prioritize efficient onboard charging to support residential and workplace AC charging convenience, reinforcing integration across passenger models. Expanding model availability and declining battery costs increase passenger EV adoption, proportionally raising onboard charger installation volumes. Government incentives and emissions regulations accelerate passenger EV sales, strengthening segment dominance. Component suppliers scale production for passenger platforms, achieving cost advantages and technology standardization.

Competitive Landscape

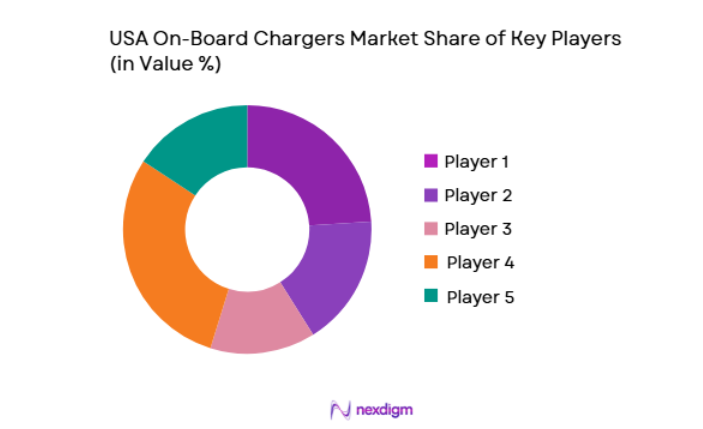

The USA On-Board Chargers market is moderately consolidated, dominated by automotive power electronics suppliers and semiconductor-integrated drivetrain companies supplying onboard charging systems to electric vehicle manufacturers. Leading firms leverage economies of scale, advanced semiconductor integration, and long-term OEM supply contracts to maintain competitive positioning. Strategic partnerships between automakers and Tier-1 suppliers influence platform integration decisions, while technology differentiation in efficiency, power density, and bidirectional capability shapes supplier competitiveness across global EV programs.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Bidirectional Capability |

| BorgWarner | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | France | ~ | ~ | ~ | ~ | ~ |

| Delta Electronics | 1971 | Taiwan | ~ | ~ | ~ | ~ | ~ |

| Denso | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| LG Magna e-Powertrain | 2021 | South Korea | ~ | ~ | ~ | ~ | ~ |

USA On-Board Chargers Market Analysis

Growth Drivers

Rising Electric Vehicle Production and Platform Electrification

The rapid expansion of electric vehicle production across passenger and commercial segments is a fundamental growth driver for the USA On-Board Chargers market, directly increasing demand for onboard charging systems integrated into every electric vehicle platform. Automotive manufacturers are accelerating electrification strategies to comply with emissions regulations and corporate sustainability targets, expanding electric model portfolios across multiple vehicle classes. Each new electric vehicle requires an onboard charger to convert grid AC power to battery-compatible DC, ensuring universal baseline demand proportional to vehicle production volumes. Higher battery capacities and longer driving range expectations necessitate increased onboard charging power, encouraging adoption of three-phase and high-power architectures. OEMs standardize onboard charger designs across global platforms to optimize manufacturing efficiency and reduce component costs. Strategic investments in EV-dedicated manufacturing plants and scalable powertrain architectures further amplify charger integration rates. Declining battery costs and growing consumer acceptance of electric mobility expand market penetration, sustaining charger demand growth. As electrification transitions from niche to mainstream automotive production, onboard chargers remain essential hardware embedded across all vehicle categories.

Advancement of Bidirectional Charging and Vehicle-to-Grid Integration

Technological advancement toward bidirectional charging capability is a major growth driver in the USA On-Board Chargers market, enabling electric vehicles to function as distributed energy resources within power systems. Bidirectional onboard chargers allow vehicles to discharge stored energy back to homes, buildings, or electrical grids, creating additional value streams beyond mobility. Utilities and energy regulators increasingly support vehicle-to-grid integration to stabilize renewable-dominant power networks and manage peak demand fluctuations. Automotive OEMs integrate bidirectional capability to differentiate electric vehicles through energy resilience and backup power functionality. Fleet operators and commercial users adopt bidirectional charging to optimize energy costs and participate in demand response programs. Semiconductor and power electronics advancements improve efficiency and thermal performance of bidirectional charger architectures, making them viable at scale. Energy market participation opportunities encourage partnerships between automakers, utilities, and energy service providers.

Market Challenges

Thermal Management and Power Density Constraints in Vehicle Integration

Thermal management and packaging limitations present significant challenges for the USA On-Board Chargers market, particularly as charging power levels increase and vehicle architectures become more compact. Onboard chargers must dissipate heat generated by power conversion electronics within confined vehicle spaces while maintaining reliability and safety standards. Higher power density requirements complicate cooling design and component placement, increasing engineering complexity and cost. Automotive OEMs demand lightweight and compact chargers to preserve vehicle efficiency and packaging flexibility, constraining design margins. Elevated operating temperatures reduce semiconductor lifespan and conversion efficiency, requiring advanced thermal materials and cooling strategies. Integration with other power electronics systems such as inverters and DC-DC converters intensifies thermal load concentration. Meeting automotive durability standards across extreme environmental conditions further complicates thermal design.

Semiconductor Cost Volatility and Supply Chain Dependence

The USA On-Board Chargers market faces persistent challenges from semiconductor cost fluctuations and supply chain concentration affecting power electronics manufacturing. Onboard chargers rely heavily on power semiconductors such as silicon carbide and IGBT devices, whose prices are influenced by global demand cycles and production capacity constraints. Automotive electrification growth competes with renewable energy and industrial sectors for semiconductor supply, creating procurement risks. Component shortages or price increases directly impact onboard charger manufacturing costs and OEM sourcing strategies. Limited supplier concentration in advanced automotive-grade semiconductors increases dependency risks for charger manufacturers. Supply chain disruptions, geopolitical tensions, and trade restrictions further exacerbate procurement uncertainty. OEMs seek cost reductions in electrified powertrains, pressuring suppliers despite volatile component pricing.

Opportunities

Expansion of High-Voltage 800V Vehicle Architectures

The transition toward high-voltage 800-volt electric vehicle architectures represents a significant opportunity for the USA On-Board Chargers market by enabling faster charging capability and improved drivetrain efficiency. High-voltage systems reduce current requirements for equivalent power transfer, lowering thermal losses and allowing lighter wiring and components. Onboard chargers compatible with 800-volt platforms support higher AC charging power levels, enhancing vehicle charging convenience without reliance on DC fast chargers. Premium and performance EV segments are leading adoption of high-voltage architectures, creating early market demand for advanced onboard chargers. Suppliers developing scalable high-voltage charger platforms gain competitive advantage across next-generation EV programs. Increased energy efficiency from high-voltage charging reduces energy loss and operating cost for users. Automotive manufacturers seek differentiation through faster home and workplace charging capability enabled by advanced onboard chargers.

Integration of Onboard Chargers with Power Electronics and Drive Systems

The integration of onboard chargers with traction inverters and DC-DC converters into unified power electronics modules presents a major opportunity for the USA On-Board Chargers market to enhance efficiency, cost reduction, and system optimization. Integrated drive charger architectures combine multiple power conversion functions within a single housing, reducing component count and wiring complexity. Automotive OEMs adopt integrated power electronics platforms to improve packaging efficiency and manufacturing scalability across EV platforms. Shared cooling and control systems within integrated modules reduce overall system weight and cost. Suppliers capable of delivering integrated power electronics solutions strengthen strategic partnerships with vehicle manufacturers. Integration improves electrical efficiency by minimizing conversion stages and losses. Simplified assembly and modular architectures support scalable EV production and platform standardization.

Future Outlook

The USA On-Board Chargers market is expected to grow steadily over the next five years, supported by rising electric vehicle production, high-voltage charging architectures, and bidirectional energy integration. Advancements in semiconductor materials and power density will improve charger efficiency and compactness. Regulatory support for vehicle-to-grid functionality and electrification mandates will further drive adoption. Increasing integration of onboard chargers with power electronics platforms will reshape technology development and supplier competition across EV manufacturing ecosystems.

Major Players

- BorgWarner

- Valeo

- Delta Electronics

- Denso

- LG Magna e-Powertrain

- ZF Friedrichshafen

- Hitachi Astemo

- Marelli

- Panasonic Automotive

- Lear Corporation

- Infineon Technologies

- STMicroelectronics

- onsemi

- Texas Instruments

- Nidec

Key Target Audience

- Automotive OEM Manufacturers

- Electric Vehicle Platform Developers

- Power Electronics Suppliers

- Commercial Vehicle Manufacturers

- Fleet Electrification Integrators

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Component Distributors

Research Methodology

Step 1: Identification of Key Variables

Key variables including EV production volumes, onboard charger power ratings, semiconductor adoption, OEM sourcing patterns, and electrification policies were identified through industry databases, government EV statistics, and supplier financial reports to define market scale and segmentation.

Step 2: Market Analysis and Construction

Market structure was constructed by mapping charger technologies, vehicle categories, supplier roles, and manufacturing integration levels. Historical production data and component revenue disclosures were synthesized to estimate market size and segment shares.

Step 3: Hypothesis Validation and Expert Consultation

Preliminary assumptions were validated through consultations with automotive power electronics engineers, EV platform specialists, and supplier strategy teams. Expert feedback refined technology adoption trends and competitive positioning across onboard charger architectures.

Step 4: Research Synthesis and Final Output

Validated datasets and insights were integrated into a unified analytical framework to generate segmentation, competitive landscape, and forecast outlook. Cross-checks ensured consistency between production volumes, supplier revenues, and technology deployment trends.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Electric Vehicle Production Volumes

Shift Toward Bidirectional Charging Architectures

Integration of Power Electronics Platforms - Market Challenges

Thermal Management and Packaging Constraints

Cost Pressure from Semiconductor Components

Voltage Standard Fragmentation - Market Opportunities

Vehicle-to-Grid and Vehicle-to-Home Integration

High-voltage 800V Charging Architectures

Commercial Vehicle Electrification Platforms - Trends

Adoption of Silicon Carbide Power Devices

Integrated Drive Charger Development

Higher Power Density Designs - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Single-phase On-board Chargers

Three-phase On-board Chargers

Bidirectional On-board Chargers

Integrated Drive Charger Units

High-power On-board Chargers - By Platform Type (In Value%)

Battery Electric Passenger Vehicles

Plug-in Hybrid Passenger Vehicles

Electric Light Commercial Vehicles

Electric Buses

Electric Medium & Heavy Trucks - By Fitment Type (In Value%)

Embedded OEM-installed Chargers

Modular Replaceable Chargers

Integrated Power Electronics Modules

Dual-charger Parallel Systems

Compact High-density Chargers - By EndUser Segment (In Value%)

Passenger Vehicle Manufacturers

Commercial Vehicle OEMs

Electric Bus Manufacturers

Fleet Integrators

Aftermarket Powertrain Integrators - By Procurement Channel (In Value%)

Direct OEM Sourcing

Tier-1 Power Electronics Suppliers

Strategic Technology Partnerships

- Market Share Analysis

- Cross Comparison Parameters (Charging Power Rating, Voltage Architecture Compatibility, Efficiency Level, Power Density, Bidirectional Capability, Thermal Management Method, Semiconductor Technology, Integration Level, OEM Platform Compatibility, Weight & Form Factor, Cooling Interface, Functional Safety Compliance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

BorgWarner

Valeo

Delta Electronics

STMicroelectronics

Infineon Technologies

Onsemi

Texas Instruments

Nidec

Hitachi Astemo

Denso

Lear Corporation

LG Magna e-Powertrain

ZF Friedrichshafen

Marelli

Panasonic Automotive

- Passenger EV OEMs demand higher efficiency onboard charging

- Commercial vehicle OEMs require high-power durable chargers

- Bus manufacturers prioritize depot charging compatibility

- Fleet integrators seek bidirectional energy management capability

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now