Updates Market Outlook 2030") Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Over-the-Air (OTA) Updates market is valued at approximately USD ~ billion in 2024, and this figure reflects the rapid growth seen in the adoption of connected vehicles and the increased demand for real-time software updates, particularly in automotive applications. Driven by the proliferation of connected vehicles, enhanced telematics systems, and consumer demand for continuous product improvements, the OTA market is experiencing accelerated growth. A surge in cloud-based services, technological advancements in wireless communication (such as 5G), and increasing safety and cybersecurity regulations are major contributors to this market’s expansion. Additionally, OEMs’ growing focus on enhancing vehicle performance through continuous software updates is driving the market forward.

The U.S. dominates the OTA updates market due to its robust automotive industry, heavy investment in autonomous vehicles, and widespread use of connected vehicle technology. Major cities like Detroit (the automotive capital) and Silicon Valley play a pivotal role in shaping OTA development through their close ties with OEMs and tech companies. Furthermore, the government’s investment in smart infrastructure and electric vehicle (EV) adoption policies boosts OTA’s growth. Key states such as California, Michigan, and Texas are particularly active in advancing OTA services, where high levels of vehicle connectivity and regulatory incentives enhance adoption.

Market Segmentation

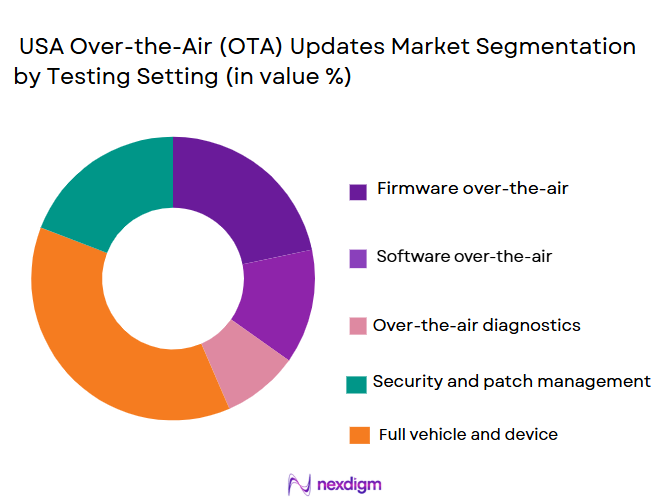

By Testing Setting

The U.S. OTA market is primarily segmented by update technology into software and firmware OTA updates. Software OTA updates include changes to infotainment systems, navigation, and user interfaces, while firmware OTA updates address essential vehicle components like ECUs, powertrains, and safety systems. The dominant sub-segment in 2024 is the firmware OTA updates, largely due to the growing complexity of modern vehicles and the need to keep critical systems up to date for safety, efficiency, and regulatory compliance. With advancements in automotive electronics and increasing vehicle dependency on software-driven components, firmware updates are seen as necessary for ensuring optimal vehicle performance and safety

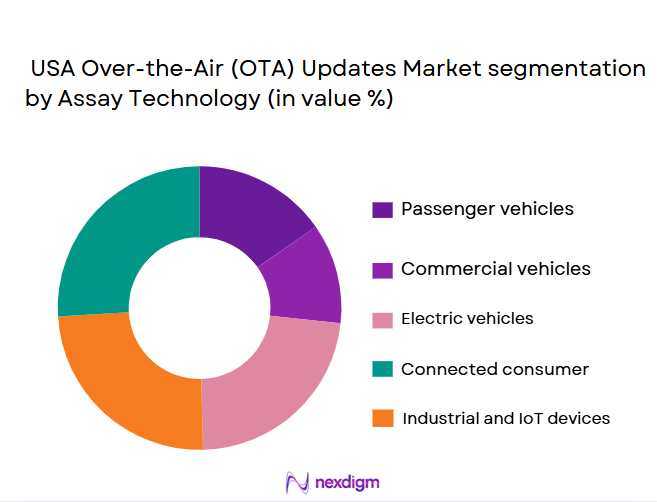

By Assay Technology

The market is also segmented by vehicle type, including passenger vehicles, light commercial vehicles, electric vehicles (EVs), and autonomous vehicles. Electric vehicles are poised to capture the largest share of the OTA market in 2024. As EVs rely heavily on software for battery management, charging optimization, and performance enhancement, OTA updates play a critical role in maintaining these vehicles. Furthermore, EV manufacturers are increasingly implementing OTA technology to update vehicle firmware and enhance driving range and energy efficiency remotely. The rise in EV sales, especially in states like California and New York, is a key factor driving this segment’s dominance in the OTA market.

Competitive Landscape

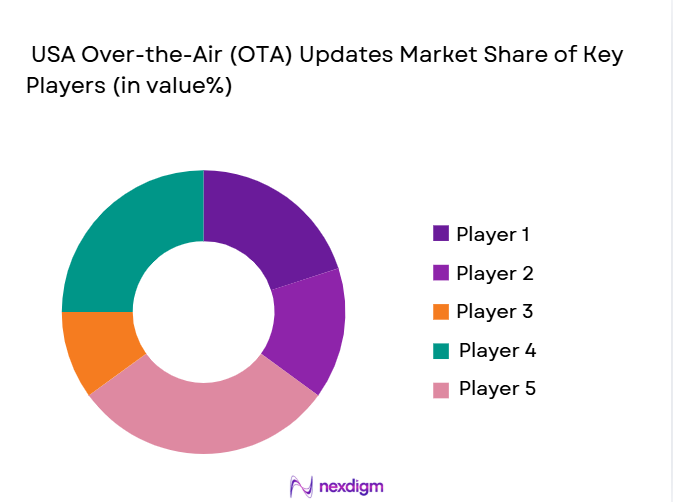

The OTA updates market in the U.S. is competitive, with significant contributions from both established automotive giants and tech-based companies focusing on connected vehicle technology. The major players include both traditional OEMs and specialized tech providers. Notable companies such as Tesla, General Motors, and Ford lead the market, leveraging in-house OTA capabilities for seamless vehicle software updates. On the technology side, companies like Airbiquity and Blackberry QNX are major contributors to OTA software platforms.

| Company | Establishment Year | Headquarters | OTA Technology | Vehicle Connectivity | Cybersecurity Focus | Market Approach | Revenue from OTA |

| Tesla | 2003 | Palo Alto, CA | ~ | ~ | ~ | ~ | ~ |

| General Motors | 1908 | Detroit, MI | ~ | ~ | ~ | ~ | ~ |

| Ford | 1903 | Dearborn, MI | ~ | ~ | ~ | ~ | ~ |

| Airbiquity | 1997 | Seattle, WA | ~ | ~ | ~ | ~ | ~ |

| BlackBerry QNX | 1988 | Ottawa, Canada | ~ | ~ | ~ | ~ | ~ |

USA Over‑the‑Air (OTA) Updates Market Analysis

Growth Drivers

Urbanization

Urbanization in Indonesia has been accelerating rapidly, with over ~% of the population living in urban areas as of 2022, a figure projected to rise to around ~% by 2035. This urban expansion is contributing to higher levels of air pollution due to increased vehicular traffic, industrial emissions, and construction activities. Cities like Jakarta, Surabaya, and Bandung are experiencing deteriorating air quality, leading to increased demand for air quality monitoring systems to manage and mitigate the effects of pollution. The surge in urban population necessitates effective air quality control mechanisms to ensure better public health and compliance with national air quality standards.

Industrialization

Indonesia’s industrial sector continues to expand, contributing significantly to air pollution. The manufacturing industry alone accounted for~ % of the national GDP in 2022. The country’s reliance on coal for energy production further exacerbates pollution levels, particularly in industrial zones like East Java and Sumatra, which are home to many coal-fired power plants. This industrial activity increases the demand for real-time monitoring of air quality to reduce emissions and mitigate environmental harm. The push to improve industrial processes and emissions management is driving investments in air quality monitoring systems.

Challenges

Technical challenges related to the deployment and maintenance of air quality monitoring systems are prevalent across Indonesia. These include the difficulties of installing and operating monitoring equipment in remote areas, where infrastructure is lacking. In many regions, especially rural or remote areas, power outages and unreliable communication networks impede the proper functioning of monitoring stations. Moreover, the need for sophisticated data analysis tools to interpret the results further complicates the widespread use of air quality monitoring technologies in the country.

Lack of Skilled Workforce

Indonesia faces a shortage of skilled professionals in environmental monitoring and data analysis, which poses a challenge for the effective implementation and maintenance of air quality monitoring systems. The country’s educational system has not yet sufficiently addressed the demand for technical expertise in environmental technology. In 2022, the Ministry of Education and Culture identified this gap in its annual report, acknowledging the need for more focused training programs to build a workforce capable of managing and operating air quality monitoring systems, particularly in smaller cities and rural areas.

Opportunities

Technological Advancements

Technological advancements in air quality monitoring systems, particularly the integration of IoT and cloud-based technologies, present significant opportunities for the market in Indonesia. With the increasing affordability of IoT devices, more municipalities are adopting these systems, which offer real-time data transmission, easy maintenance, and cost-effectiveness. Indonesia’s government has expressed interest in expanding IoT-based monitoring infrastructure to enhance air quality management. This technology also allows for remote monitoring and data analysis, making it easier to address air pollution issues in areas that previously lacked monitoring coverage. [Source: Ministry of Environment and Forestry

International Collaborations

Indonesia has been actively engaging in international collaborations to enhance its air quality management capabilities. In partnership with global organizations like the Asian Development Bank (ADB) and the United Nations Environment Programme (UNEP), Indonesia has been implementing projects to strengthen air pollution monitoring and management systems. In 2022, ADB allocated $~ million to support Indonesia’s environmental monitoring programs. These collaborations bring in foreign expertise and funding, helping to accelerate the deployment of advanced air quality monitoring technologies in the country, especially in underserved regions

Future Outlook

Over the next 5 years, the U.S. OTA updates market is projected to experience substantial growth. Factors such as the increasing number of connected vehicles, the rise of EVs, and the adoption of advanced driver-assistance systems (ADAS) are expected to drive demand for OTA technology. Moreover, with the expansion of 5G connectivity, OTA updates will become faster and more reliable, allowing for more frequent and diverse updates. Additionally, stricter regulatory frameworks related to vehicle safety, security, and emissions will necessitate regular software updates, further boosting the market.

Major Players in the Market

- Tesla

- General Motors

- Ford

- Airbiquity

- BlackBerry QNX

- Aptiv

- Continental AG

- Harman International

- Qualcomm

- NXP Semiconductors

- Intel Corporation

- Verizon Communications

- Bosch Mobility

- Daimler AG

- Waymo (Alphabet Inc.)

Key Target Audience

- Automotive OEMs

- Tier-1 Suppliers in Automotive Electronics

- Telecommunications Companies (Verizon, AT&T)

- Electric Vehicle Manufacturers

- Software and Telematics Service Providers

- Investments and Venture Capitalist Firms

- Government and Regulatory Bodies

- Fleet Management Companies

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves identifying the key variables influencing the U.S. OTA Updates market. This process is conducted through desk research utilizing secondary databases, industry reports, and relevant market data from OEMs, software vendors, and regulatory bodies.

Step 2: Market Analysis and Construction

This step includes analyzing historical data of vehicle production, OTA adoption rates, and consumer preferences. The focus is on understanding how OEMs and Tier-1 suppliers integrate OTA into their vehicle models and services, and assessing revenue generation through OTA updates.

Step 3: Hypothesis Validation and Expert Consultation

In this phase, market hypotheses are validated through interviews with industry experts from major companies, including OEMs, software developers, and regulatory authorities. This consultation helps in gaining insights on technological developments and customer preferences.

Step 4: Research Synthesis and Final Output

The final phase synthesizes data gathered through interviews and desk research. Direct interactions with manufacturers and OTA service providers ensure the final output is accurate and validated. This approach guarantees that the research findings reflect current market realities and future potential.

- Executive Summary

- USA Over-the-Air (OTA) Updates Market Research Methodology

Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rapid growth of connected and software-defined vehicles

Rising demand for remote feature updates and diagnostics

Increasing cybersecurity and compliance requirements - Market Challenges

Data security and privacy risks

Complex integration with legacy hardware systems

High dependency on network reliability and bandwidth - Market Opportunities

Expansion of OTA solutions in electric and autonomous vehicles

Monetization through feature-on-demand and subscription models

Adoption of OTA updates in non-automotive IoT ecosystems - Trends

Shift toward full lifecycle OTA management platforms

Integration of AI for predictive updates and diagnostics

Increased focus on secure and encrypted update delivery

- By Market Value 2019–2024

- By Installed Units 2019–2024

- By Average System Price 2019–2024

- By System Complexity Tier 2019–2024

- By System Type (In Value%)

Firmware over-the-air updates

Software over-the-air updates

Over-the-air diagnostics systems

Security and patch management OTA systems

Full vehicle and device OTA platforms - By Platform Type (In Value%)

Passenger vehicles

Commercial vehicles

Electric vehicles

Connected consumer electronics

Industrial and IoT devices - By Fitment Type (In Value%)

Embedded OEM-installed OTA systems

Cloud-based OTA management platforms

Hybrid edge-cloud OTA solutions

Aftermarket OTA enablement systems

Standalone OTA software platforms - By EndUser Segment (In Value%)

Automotive OEMs

Tier I automotive suppliers

Fleet operators and mobility providers

Consumer electronics manufacturers

Industrial and enterprise IoT operators - By Procurement Channel (In Value%)

Direct OEM contracts

Software licensing agreements

Cloud service subscriptions

System integrator partnerships

Enterprise-level procurement contracts

- Market Share Analysis

- Cross Comparison Parameters

(Update reliability, Cybersecurity capability, Platform scalability, Integration flexibility, Pricing model) - SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bosch

Continental

Harman International

Aptiv

BlackBerry QNX

Airbiquity

Wind River

Red Hat

Cisco Systems

Qualcomm

Siemens

PTC

IBM

Microsoft

Amazon Web Services

- OEMs leverage OTA to reduce recall and service costs

- Fleet operators prioritize uptime and remote diagnostics

- Electronics manufacturers use OTA for rapid feature deployment

- Enterprises focus on security patching and compliance

- Forecast Market Value 2025–2030

- Forecast Installed Units 2025–2030

- Price Forecast by System Tier 2025–2030

- Future Demand by Platform 2025–2030

Updates Market Outlook 2030")

Updates Market Outlook 2030")

Updates Market Outlook 2030")

Updates Market Outlook 2030")

Updates Market Outlook 2030") Request a Sample

Request a Sample Updates Market Outlook 2030") Ask for Customization

Ask for Customization Updates Market Outlook 2030") Get a Quote

Get a Quote Updates Market Outlook 2030") Enquire Now

Enquire Now Updates Market Outlook 2030")