Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Pedestrian Detection Systems market reached USD ~ Billion based on a recent historical assessment, supported by data from the National Highway Traffic Safety Administration and industry financial disclosures from leading ADAS suppliers. Growth is driven by increasing integration of advanced driver assistance systems in passenger vehicles, stricter federal safety performance standards, and rising investment in AI-enabled vision processing platforms. Expanding electric vehicle production and higher OEM bundling of collision avoidance technologies further strengthen revenue expansion across domestic automotive manufacturing ecosystems.

Detroit, California, and Texas remain dominant in hubs due to concentrated automotive manufacturing facilities, advanced semiconductor design centers, and established ADAS testing infrastructure. Silicon Valley drives software and AI innovation, while Michigan anchors system integration and large-scale vehicle production. Strong regulatory oversight from federal safety authorities and active state-level transportation safety initiatives reinforce adoption. In addition, collaboration between technology firms and automotive OEMs in these regions accelerates commercialization and deployment of pedestrian detection solutions nationwide.

Market Segmentation

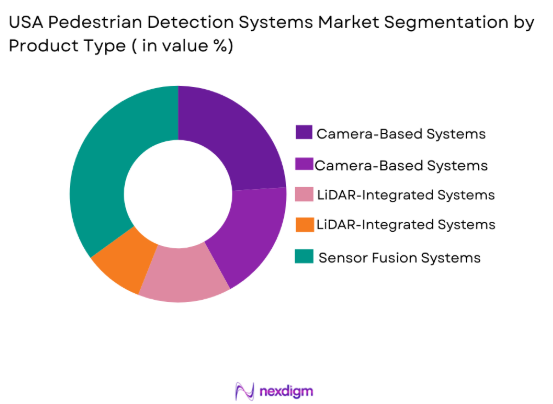

By Product Type

USA Pedestrian Detection Systems market is segmented by product type into Camera-Based Systems, Radar-Assisted Systems, LiDAR-Integrated Systems, Thermal Imaging Systems, and Sensor Fusion Systems. Recently, Sensor Fusion Systems has a dominant market share due to enhanced detection accuracy, improved performance in adverse weather conditions, and superior object classification capabilities compared to single-sensor platforms. OEMs increasingly prioritize multi-sensor architectures to meet federal safety benchmarks and reduce false positives, while insurance incentives and liability mitigation strategies further encourage adoption of advanced integrated solutions across premium and mid-range vehicles.

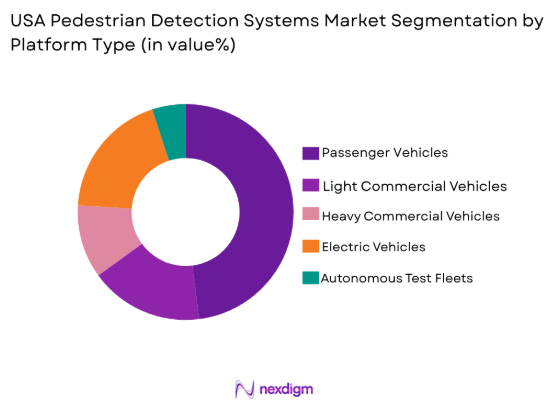

By Platform Type

USA Pedestrian Detection Systems market is segmented by platform type into Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, and Autonomous Test Fleets. Recently, Passenger Vehicles has a dominant market share due to higher production volumes, regulatory safety scoring requirements, and strong consumer demand for advanced safety features. OEM bundling of pedestrian detection with adaptive cruise control and lane assistance systems further strengthens penetration, while financing options and competitive differentiation strategies support broader deployment across compact, mid-size, and SUV segments.

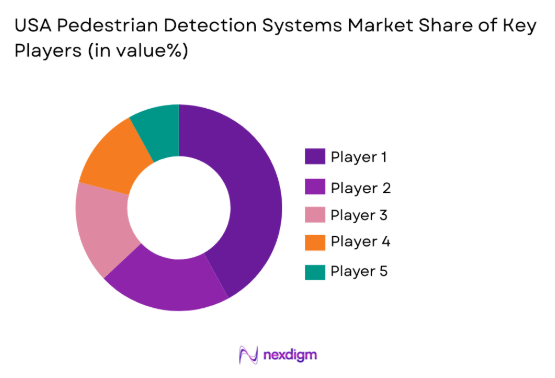

Competitive Landscape

The USA Pedestrian Detection Systems market is moderately consolidated, with automotive suppliers and semiconductor companies controlling a substantial portion of system integration contracts. Strategic partnerships between AI chip manufacturers and automotive OEMs shape competitive intensity, while software-driven differentiation increasingly determines procurement decisions. Market leaders maintain strong distribution networks, patent portfolios, and long-term OEM agreements that reinforce entry barriers for smaller technology firms.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Integration Depth |

| Bosch Mobility Solutions | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ |

| Mobileye Global | 1999 | Israel | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ |

USA Pedestrian Detection Systems Market Analysis

Growth Drivers

Federal Vehicle Safety Mandates and NCAP Integration

Increasing regulatory emphasis on pedestrian protection standards significantly accelerates the adoption of advanced detection technologies across new vehicle platforms in the United States. National safety authorities continuously update crash avoidance assessment frameworks, encouraging manufacturers to integrate pedestrian detection as a core safety feature rather than an optional add-on. Automakers are motivated to achieve higher safety ratings that influence consumer purchasing decisions and insurance underwriting criteria. Integration with broader advanced driver assistance ecosystems further amplifies system value by enabling coordinated braking and steering interventions. The regulatory environment also compels mid-range vehicle manufacturers to incorporate detection features to remain competitive. Insurance providers increasingly recognize advanced pedestrian detection as a risk-reduction mechanism, reinforcing OEM commitments. Federal infrastructure initiatives promoting intelligent transportation systems create a complementary ecosystem that supports vehicle-to-infrastructure interaction. These combined forces sustain continuous investment in sensor accuracy, software refinement, and scalable deployment across domestic automotive production.

Rapid Advancement in AI-Enabled Sensor Fusion Architectures

Continuous innovation in artificial intelligence, edge computing, and high-resolution imaging significantly enhances the operational performance of pedestrian detection systems across varied traffic environments. Advanced neural network models improve object classification accuracy, reducing false positives and enabling reliable detection under low-light and adverse weather conditions. Semiconductor advancements support real-time processing capabilities within compact automotive-grade chipsets, lowering latency and improving response times. Multi-sensor integration combining radar, LiDAR, and camera inputs strengthens redundancy and operational reliability. Automakers increasingly prioritize scalable electronic architectures that accommodate software updates and feature expansions. Strategic collaborations between chip designers and automotive Tier 1 suppliers accelerate commercialization cycles. Cost optimization in semiconductor manufacturing contributes to broader deployment across vehicle categories. This technological acceleration ensures that pedestrian detection evolves from a premium feature into a standardized safety component within mainstream automotive platforms.

Market Challenges

High System Integration and Hardware Costs in Entry-Level Vehicles

The cost of integrating multi-sensor pedestrian detection systems into entry-level vehicles remains a substantial barrier for widespread adoption across all price segments. Advanced radar modules, LiDAR sensors, and AI processing units require significant hardware investment, increasing overall vehicle production costs. Manufacturers must balance safety feature integration with competitive pricing strategies to maintain affordability. Supply chain volatility in semiconductor components further exacerbates cost pressures and production planning complexities. Smaller OEMs face additional challenges in negotiating long-term supplier contracts for high-performance sensors. Calibration and validation processes add engineering expenses that impact profit margins. While premium segments absorb higher technology costs more easily, budget-focused vehicles encounter pricing constraints. This financial pressure limits uniform adoption rates and slows penetration in cost-sensitive consumer categories.

Environmental and Operational Performance Limitations

Pedestrian detection systems must operate reliably across diverse environmental conditions including heavy rain, fog, snow, and low-light scenarios. Sensor accuracy can be compromised by glare, obstructions, or complex urban landscapes with dense pedestrian activity. Thermal variations and physical wear may impact long-term reliability of camera and radar modules. False positive detections can undermine driver confidence and create nuisance braking incidents. Continuous software updates are required to maintain classification accuracy as road scenarios evolve. Integration across different vehicle architectures introduces compatibility challenges that require rigorous testing. Regulatory scrutiny increases as system reliability becomes directly linked to safety performance. These operational limitations necessitate sustained research investment and robust validation protocols, adding complexity to system deployment strategies.

Opportunities

Expansion into Autonomous Delivery and Urban Mobility Platforms

The rapid growth of autonomous delivery vehicles and urban mobility solutions creates a strong opportunity for pedestrian detection technologies to extend beyond conventional passenger vehicles. E-commerce expansion and last-mile logistics demand compact autonomous fleets capable of navigating dense pedestrian environments. Integration of advanced detection systems ensures safe interaction between autonomous platforms and vulnerable road users. Municipal initiatives supporting low-emission and shared mobility services further accelerate adoption of intelligent sensing technologies. Fleet operators prioritize safety compliance to mitigate liability risks and secure regulatory approvals. Edge AI advancements allow cost-effective deployment in smaller autonomous platforms. Collaboration between robotics developers and automotive sensor suppliers fosters specialized detection algorithms. This emerging mobility ecosystem positions pedestrian detection systems as foundational components of next-generation transportation infrastructure.

Integration with Smart City and Vehicle-to-Everything Infrastructure

The development of connected transportation networks provides a significant opportunity for pedestrian detection systems to integrate with broader vehicle-to-everything communication frameworks. Smart traffic signals, connected crosswalks, and roadside sensors enable real-time data exchange that enhances situational awareness. Vehicles equipped with advanced detection systems can receive external alerts regarding pedestrian movement patterns, improving preventive response mechanisms. Federal and state infrastructure investments in intelligent transportation systems support deployment of connected safety ecosystems. Data analytics platforms enable predictive risk modeling based on aggregated mobility data. Automotive OEMs and technology providers collaborate to standardize communication protocols. Enhanced connectivity reduces dependency solely on onboard sensors, strengthening system redundancy. This convergence of automotive safety and digital infrastructure creates a scalable growth pathway for pedestrian detection technologies across urban centers.

Future Outlook

The USA Pedestrian Detection Systems market is expected to witness steady expansion driven by regulatory reinforcement, continuous AI innovation, and increased OEM standardization across vehicle segments. Technological advancements in sensor fusion and edge computing will enhance accuracy and affordability. Infrastructure investments supporting connected mobility will further stimulate integration. Demand from electric vehicles and autonomous mobility platforms is likely to accelerate system deployment across both urban and suburban environments.

Major Players

- Bosch Mobility Solutions

- Continental AG

- AptivPLC

- Mobileye Global

- Magna International

- ZF Friedrichshafen

- Denso Corporation

- Valeo SA

- Autoliv Inc

- Texas Instruments Automotive

- ON Semiconductor

- Hella GmbH

- Visteon Corporation

- Nvidia Automotive

- Analog Devices Automotive Division

Key Target Audience

- Automotive OEMs

- Automotive Suppliers

- Fleet Operators

- Electric Vehicle Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Insurance Providers

- Smart City Infrastructure Developers

Research Methodology

Step 1: Identification of Key Variables

Comprehensive identification of demand-side and supply-side variables influencing the USA Pedestrian Detection Systems market was conducted. Key performance metrics, regulatory influences, pricing structures, and technology integration factors were mapped. Data sources included financial disclosures, federal safety agencies, and automotive production statistics.

Step 2: Market Analysis and Construction

Market size estimation was derived using bottom-up analysis of OEM production volumes and component pricing benchmarks. Cross-validation was performed using supplier revenue disclosures and trade data. Segment-wise distribution was structured based on platform deployment and technology adoption rates.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including automotive engineers, semiconductor specialists, and safety compliance professionals were consulted to validate assumptions. Technical feasibility, regulatory alignment, and deployment scalability were examined. Iterative feedback refined segmentation and competitive positioning analysis.

Step 4: Research Synthesis and Final Output

All validated data points were synthesized into a structured analytical framework. Quantitative modeling and qualitative assessment were integrated to ensure consistency. Final conclusions were reviewed for methodological transparency and analytical coherence.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing Federal Safety Regulations and NCAP Integration

Expansion of Electric Vehicle Production with Embedded ADAS

Rapid Advancement in AI Based Sensor Fusion Architectures - Market Challenges

High Hardware and Integration Costs in Entry Level Vehicles

Environmental Performance Limitations in Adverse Conditions

Semiconductor Supply Chain Volatility - Market Opportunities

Integration with Smart City Infrastructure Networks

Deployment in Autonomous Delivery and Urban Mobility Fleets

Development of Cost Optimized Solid State LiDAR Systems - Trends

Shift Toward Multi Sensor Fusion Architectures

Edge AI Processing for Real Time Object Recognition

Growing OEM Standardization Across Mid Range Vehicles - Government Regulations & Defense Policy

National Highway Traffic Safety Administration Safety Standards

New Car Assessment Program Rating Enhancements

Federal Infrastructure Funding for Intelligent Transportation Systems

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Camera Based Detection Systems

Radar Assisted Detection Systems

LiDAR Enabled Pedestrian Detection Systems

Thermal Imaging Detection Systems

Multi Sensor Fusion Detection Systems - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Autonomous Mobility Platforms - By Fitment Type (In Value%)

OEM Factory Integrated Systems

Aftermarket Retrofit Solutions

Embedded ADAS Modules

Cloud Connected Detection Platforms

Standalone Safety Assist Modules - By End User Segment (In Value%)

Automotive OEMs

Commercial Fleet Operators

Ride Sharing Service Providers

Logistics and Delivery Companies

Municipal Transportation Authorities - By Procurement Channel (In Value%)

Direct OEM Supply Agreements

Tier 1 Supplier Contracts

Fleet Procurement Programs

Government Safety Initiatives

Aftermarket Distribution Networks - By Material / Technology (in Value %)

CMOS Vision Sensors

Millimeter Wave Radar Modules

Solid State LiDAR Sensors

Infrared Thermal Sensors

AI Vision Processing Chipsets

- Market structure and competitive positioning

- Market share snapshot of major players

- Cross Comparison Parameters (Detection Accuracy, Sensor Range, AI Processing Capability, Integration Complexity, Cost Efficiency)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces Analysis

- Key Players

Bosch Mobility Solutions

Continental Automotive Technologies

Aptiv Advanced Safety Systems

Magna Electronics Division

Mobileye Vision Technologies

Denso North America Automotive Systems

Valeo Intelligent Driving Systems

ZF Active Safety Technologies

Autoliv Vehicle Safety Solutions

Hella Electronics Corporation

Visteon Smart Mobility Systems

Nvidia Automotive Platforms

Texas Instruments Automotive Solutions

ON Semiconductor Mobility Division

Analog Devices Automotive Electronics

- Passenger Vehicle OEMs Prioritizing Advanced Safety Differentiation

- Fleet Operators Focusing on Liability Reduction and Insurance Incentives

- Ride Sharing Platforms Integrating Collision Avoidance Technologies

- Municipal Authorities Advancing Vision Zero Safety Initiatives

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now