Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Prognostic Biomarkers market is valued at approximately USD ~ billion, driven by the increasing prevalence of chronic diseases and the growing focus on personalized medicine. Advanced diagnostic techniques, including genetic sequencing, proteomics, and liquid biopsy, have propelled the demand for prognostic biomarkers. Technological innovations in these fields have enhanced early disease detection and personalized treatment options, contributing to the market’s expansion. Additionally, significant healthcare investments and government support for biomarker research are anticipated to sustain growth in the coming years.

Dominant regions such as California, New York, and Massachusetts lead the market due to their well-established healthcare infrastructures, presence of major research institutions, and thriving biotechnology sectors. These areas benefit from high levels of healthcare spending, numerous academic collaborations, and a strong presence of pharmaceutical companies, all of which foster innovation in prognostic biomarker development. Additionally, their proximity to cutting-edge technology hubs accelerates the adoption of advanced diagnostic tools, further cementing their dominance in the market.

Market Segmentation

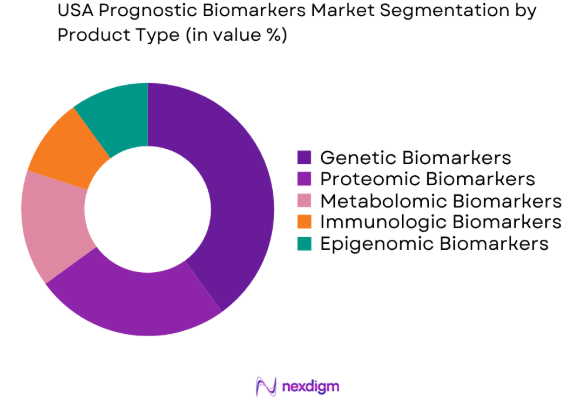

By Product Type

The USA Prognostic Biomarkers market is segmented by product type into genetic biomarkers, proteomic biomarkers, metabolomic biomarkers, immunologic biomarkers, and epigenomic biomarkers. Recently, genetic biomarkers have gained dominance due to the increasing focus on genomics in personalized medicine. Advances in genetic sequencing technologies and the increasing adoption of genetic testing for early disease detection, particularly in oncology, are significant factors driving this sub-segment’s growth. The ability to use genetic biomarkers for precision medicine, especially in cancer diagnostics, has propelled their widespread use in clinical applications.

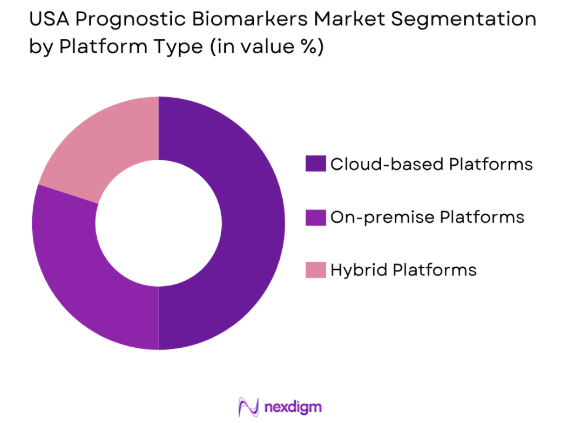

By Platform Type

The USA Prognostic Biomarkers market is segmented by platform type into cloud-based platforms, on-premise platforms, and hybrid platforms. Cloud-based platforms dominate the market due to their flexibility, scalability, and cost-efficiency, making them highly attractive to businesses of all sizes. The rise in remote work and the increasing need for data storage and processing power have contributed significantly to the growth of cloud-based platforms. Additionally, advancements in cloud security and the integration of AI tools for better data management are propelling the demand for cloud-based solutions.

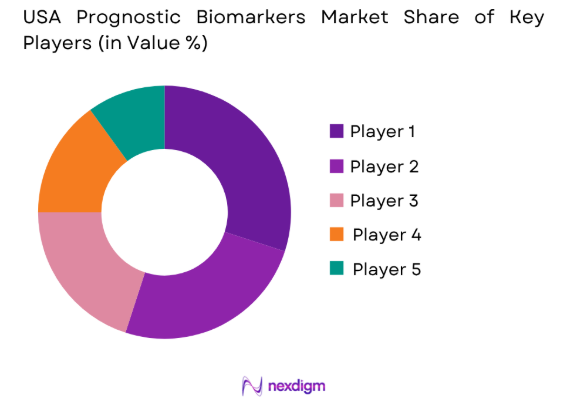

Competitive Landscape

The USA Prognostic Biomarkers market is highly competitive, with several leading diagnostic companies and biotech firms pushing the boundaries of innovation. Large established players, as well as emerging biotech startups, are focusing on advancements in AI, genomics, and proteomics to stay competitive. The market is consolidating as companies engage in mergers, acquisitions, and strategic partnerships to strengthen their product portfolios and expand into new markets. These collaborations foster greater access to cutting-edge technologies and facilitate the development of new biomarkers for early disease detection.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Additional Parameter |

| Thermo Fisher Scientific | 1956 | Waltham, Massachusetts | ~ | ~ | ~ | ~ | ~ |

| Abbott Laboratories | 1888 | Chicago, Illinois | ~ | ~ | ~ | ~ | ~ |

| Roche Diagnostics | 1896 | Basel, Switzerland | ~ | ~ | ~ | ~ | ~ |

| Illumina Inc. | 1998 | San Diego, California | ~ | ~ | ~ | ~ | ~ |

| Qiagen | 1984 | Hilden, Germany | ~ | ~ | ~ | ~ | ~ |

USA Prognostic Biomarkers Market Analysis

Growth Drivers

Technological Advancements in Diagnostic Tools

Advancements in diagnostic technologies are driving growth in the USA Prognostic Biomarkers market. Innovations like next-generation sequencing (NGS), liquid biopsy, and AI-powered diagnostics have transformed disease detection, enabling earlier and more accurate diagnoses. These technologies also allow for personalized treatments based on genetic profiles. AI integration enhances diagnostic accuracy and efficiency, improving early disease detection. As healthcare providers increasingly adopt these solutions, the market is set to grow, with new uses in oncology, cardiology, and neurology. The reduction in diagnostic time and costs makes these technologies more accessible, expanding the reach of prognostic biomarkers to a broader population and fueling market demand.

Increasing Demand for Personalized Medicine

The shift towards personalized medicine is a significant driver of the USA Prognostic Biomarkers market. By understanding a patient’s genetic makeup, personalized medicine tailors treatments to improve outcomes and minimize side effects. The use of biomarkers, especially in oncology, helps identify targeted therapies and guide individualized treatments. As more patients seek personalized care, the demand for biomarkers that can accurately assess disease risk, predict treatment responses, and track progression grows. This trend toward patient-centric care models emphasizes the role of biomarkers in improving outcomes, further driving the market’s growth. As a result, personalized medicine powered by biomarkers is central to the future of healthcare.

Market Challenges

High Cost of Diagnostic Technologies

A major challenge in the USA Prognostic Biomarkers market is the high cost of diagnostic technologies. While advancements in genomics and proteomics have led to accurate diagnostic tools, their premium price can be prohibitive, especially for smaller healthcare providers and diagnostic centers. The costs associated with sequencing technologies, liquid biopsy tests, and other advanced systems limit access, particularly in underserved regions. Additionally, the ongoing expense of maintaining and upgrading diagnostic equipment adds to the financial burden. Overcoming these cost barriers is essential to ensure that the benefits of prognostic biomarkers reach a wider population and are not restricted by economic limitations.

Regulatory and Reimbursement Barriers

The regulatory landscape for prognostic biomarkers and diagnostic systems remains complex and challenging. The approval process for new diagnostic tests and biomarkers is stringent, requiring substantial clinical data to demonstrate their efficacy and safety. These lengthy and expensive regulatory processes can delay the market entry of new technologies, limiting innovation. Additionally, reimbursement policies for diagnostic tests are often inconsistent and unclear, which can affect the affordability and accessibility of biomarker-based diagnostics. Healthcare providers may face challenges in obtaining reimbursement for new diagnostic tests, especially if they are considered experimental or unproven. Overcoming regulatory hurdles and securing appropriate reimbursement will be critical for the widespread adoption and market growth of prognostic biomarkers.

Opportunities

Expansion of Research Partnerships in Biomarker Discovery

A key opportunity in the USA Prognostic Biomarkers market lies in expanding research partnerships to discover and validate new biomarkers. Collaborations between pharmaceutical companies, biotech firms, and academic institutions are speeding up the identification of novel biomarkers for various diseases, such as cancer, cardiovascular conditions, and neurological disorders. These partnerships facilitate the sharing of resources, expertise, and clinical data, enhancing the efficiency of biomarker discovery. With the growing demand for personalized medicine, there is a rising need for biomarkers that can accurately predict disease risk and monitor treatment effectiveness. Expanding these research collaborations will drive the development of innovative diagnostic solutions, fueling market growth.

Integration of Artificial Intelligence in Diagnostic Platforms

The integration of artificial intelligence (AI) into diagnostic platforms presents a major opportunity for growth in the USA Prognostic Biomarkers market. AI can enhance the analysis of biomarker data by identifying complex patterns and correlations that would be difficult for human clinicians to detect. AI-driven algorithms can analyze large datasets from genetic tests, medical records, and imaging systems to provide more accurate and timely diagnoses. This technology also allows for the development of predictive models that can guide treatment decisions and improve patient outcomes. As AI continues to advance, its integration into biomarker diagnostic platforms will become increasingly important, offering opportunities for companies that are at the forefront of this technological revolution.

Future Outlook

The USA Prognostic Biomarkers market is expected to experience continued growth over the next five years, driven by ongoing advancements in molecular diagnostics, artificial intelligence, and personalized medicine. With the increasing demand for early disease detection and personalized treatment, the adoption of innovative biomarker-based diagnostic tools will continue to expand. Additionally, regulatory support and increasing investment in biomarker research are expected to further stimulate market growth. The next few years will see continued innovation in genetic testing, liquid biopsy technologies, and AI integration, all of which will contribute to the market’s long-term success.

Major Players

- ThermoFisher Scientific

- Abbott Laboratories

- Roche Diagnostics

- Illumina Inc.

- Qiagen

- PerkinElmer

- Danaher Corporation

- Bio-Rad Laboratories

- Siemens Healthineers

- Sysmex Corporation

- Hologic Inc.

- Beckman Coulter

- Agilent Technologies

- Becton Dickinson

- Exact Sciences

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Pharmaceutical companies

- Diagnostic laboratories

- Healthcare providers

- Biotechnology companies

- Medical device manufacturers

- Research institutions

Research Methodology

Step 1: Identification of Key Variables

Key variables affecting the prognostic biomarkers market are identified, including technological advancements, demand patterns, and regulatory factors.

Step 2: Market Analysis and Construction

Comprehensive analysis of the market is conducted, leveraging primary and secondary data to understand market trends, growth drivers, and segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Consultations with industry experts are conducted to validate hypotheses and ensure the accuracy of market assumptions and findings.

Step 4: Research Synthesis and Final Output

Final research outputs are synthesized, providing a comprehensive report with actionable insights and strategic recommendations.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increased Healthcare Spending

Technological Advancements in Diagnostic Tools

Rising Demand for Personalized Medicine - Market Challenges

High Cost of Diagnostic Equipment

Regulatory Barriers

Limited Awareness in Emerging Markets - Market Opportunities

Expansion of Research Partnerships

Integration of AI in Biomarker Discovery

Growing Demand in Precision Medicine - Trends

Shift Towards Non-invasive Diagnostic Techniques

Increased Adoption of Biomarkers in Cancer Treatment

Rising Popularity of Liquid Biopsy - Government Regulations

- SWOT Analysis of Key Competitors

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Genetic Biomarkers

Proteomic Biomarkers

Metabolomic Biomarkers

Immunologic Biomarkers

Epigenomic Biomarkers - By Platform Type (In Value%)

Laboratory-Based Platforms

Point-of-Care Testing Platforms

Mobile Testing Platforms

Hospital Testing Platforms

Wearable Diagnostic Platforms - By Fitment Type (In Value%)

In-house Solutions

Outsourced Solutions

Mobile Solutions

Cloud-based Solutions

Integrated Systems - By End User Segment (In Value%)

Hospitals

Clinics

Research Institutes

Pharmaceutical Companies

Diagnostic Laboratories - By Procurement Channel (In Value%)

Direct Procurement

Government Tenders

Private Sector Procurement

Online Bidding Platforms

Third-party Distributors

- Market Share Analysis

- Cross Comparison Parameters (System Type, Platform Type, Procurement Channel, End User Segment, Fitment Type, Market Reach, Technology Focus, Revenue, Product Portfolio, Geographic Coverage)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Thermo Fisher Scientific

Abbott Laboratories

Roche Diagnostics

Siemens Healthineers

GE Healthcare

Bio-Rad Laboratories

Illumina Inc.

Qiagen

Agilent Technologies

PerkinElmer

Sysmex Corporation

Hologic Inc.

Danaher Corporation

Becton Dickinson

Exact Sciences

- Hospitals’ Growing Demand for Diagnostic Tools

- Pharmaceutical Companies’ Interest in Biomarker Research

- Clinics Seeking Cost-effective Solutions

- Research Institutions’ Focus on Early Disease Detection

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now