Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Propeller Shafts Market reflects a market size of approximately USD ~ billion based on a recent historical assessment supported by industry publications and automotive component trade data. Demand is primarily driven by sustained production of light trucks, SUVs, and heavy commercial vehicles, along with replacement demand in the aftermarket. Growth in logistics, construction activity, and pickup truck sales continues to stimulate demand for durable driveline components across multiple vehicle classes.

Michigan, Ohio, and Indiana remain dominant production hubs due to concentrated automotive OEM manufacturing facilities and a dense supplier ecosystem. These states host major assembly plants and Tier-1 driveline suppliers, ensuring proximity-based procurement advantages and streamlined logistics. Southern states including Texas and Tennessee also contribute significantly owing to expanding vehicle manufacturing investments and strong commercial vehicle demand linked to regional freight and infrastructure development.

Market Segmentation

By Product Type

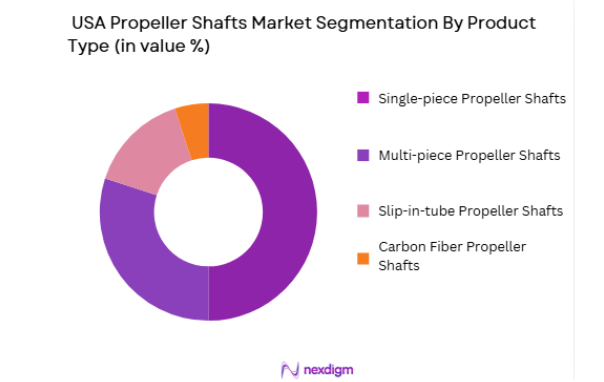

USA Propeller Shafts Market is segmented by product type into single-piece propeller shafts, multi-piece propeller shafts, slip-in-tube propeller shafts, and carbon fiber propeller shafts. Recently, multi-piece propeller shafts have a dominant market share due to factors such as higher application in long-wheelbase vehicles, heavy-duty trucks, and SUVs requiring improved vibration control and torque transmission efficiency. Their ability to reduce noise, vibration, and harshness while supporting higher torque loads makes them suitable for modern commercial vehicles and large passenger vehicles. Increased production of pickup trucks and freight vehicles across the country has reinforced demand for these configurations. Additionally, modular architecture in newer vehicle platforms supports the integration of multi-piece assemblies, strengthening their competitive advantage in OEM supply contracts.

By Vehicle Type

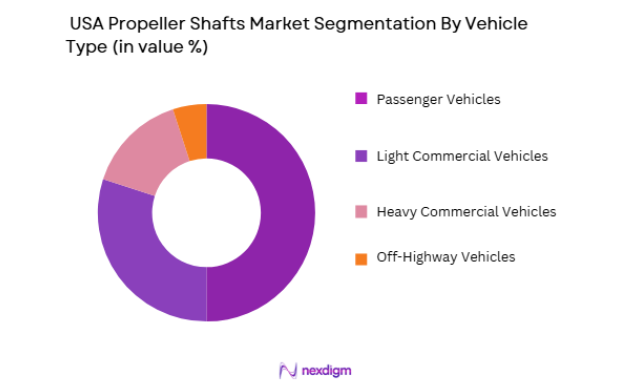

USA Propeller Shafts Market is segmented by vehicle type into passenger vehicles, light commercial vehicles, heavy commercial vehicles, and off-highway vehicles. Recently, light commercial vehicles have a dominant market share due to factors such as strong demand for pickup trucks, delivery vans, and fleet vehicles supporting e-commerce and last-mile logistics expansion. The structural reliance of these vehicles on rear-wheel and all-wheel drive systems significantly increases propeller shaft installation volumes. Fleet renewal cycles and infrastructure-driven freight movement further sustain replacement demand. OEM partnerships with domestic automakers producing high volumes of utility trucks also enhance production stability. Continuous expansion in regional logistics networks and contractor-based vehicle purchases reinforces the leading contribution of this segment to overall market revenue.

Competitive Landscape

The USA propeller shafts market demonstrates moderate consolidation with established Tier-1 automotive component manufacturers maintaining strong OEM contracts and aftermarket networks. Competition is shaped by technological innovation in lightweight materials, precision balancing, and durability performance. Large players leverage vertically integrated manufacturing and long-term supply agreements with domestic automakers, while specialized manufacturers focus on performance and carbon fiber driveline solutions to differentiate their portfolios.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Material Innovation Capability |

| Dana Incorporated | 1904 | Ohio, USA | ~ | ~ | ~ | ~ | ~ |

| American Axle & Manufacturing | 1994 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Meritor Inc. | 1909 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Neapco Holdings | 1921 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| GKN Automotive | 1759 | UK | ~ | ~ | ~ | ~ | ~ |

USA Propeller Shafts Market Analysis

Growth Drivers

Expansion of Light Truck and SUV Production Volumes

The rapid expansion of e-commerce platforms has intensified freight transportation requirements, thereby stimulating procurement of delivery vans and medium-duty commercial vehicles equipped with propeller shaft-driven rear axles. Increased parcel movement volume across urban and suburban distribution corridors requires dependable torque transmission systems capable of handling repetitive stop-and-go duty cycles. Commercial fleet operators prioritize durability and reduced maintenance downtime, which supports investment in advanced driveline systems with improved balancing and corrosion resistance properties. Infrastructure investment programs supporting highway development and warehousing facilities further increase demand for transport vehicles that rely on conventional shaft-driven configurations. Propeller shaft manufacturers benefit from long-term fleet supply contracts and standardized platform production cycles that ensure volume stability. Moreover, modernization of older fleets to meet emission and efficiency regulations encourages replacement of outdated driveline assemblies with lighter and more efficient systems. Technological improvements in shaft balancing, spline design, and universal joint articulation enhance operational reliability under heavy load conditions common in freight distribution networks. Domestic manufacturing incentives and reshoring strategies strengthen local supply chain integration, improving responsiveness to OEM scheduling requirements. As logistics activity continues to expand regionally and nationally, commercial fleet-driven demand acts as a structural growth pillar sustaining propeller shaft market performance.

Infrastructure and Logistics Sector Growth

Infrastructure and Logistics Sector Growth: Federal infrastructure programs and private sector investments in warehousing and logistics expansion significantly contribute to heavy commercial vehicle deployment, directly influencing propeller shaft demand. Increased freight movement volumes documented by the U.S. Department of Transportation require reliable heavy-duty driveline systems capable of operating under sustained torque loads. Commercial trucks, including Class 6 to Class 8 vehicles, depend on durable multi-piece shaft assemblies engineered for high torque transmission and extended service life. Fleet operators prioritize maintenance efficiency and reduced downtime, stimulating procurement of high-quality replacement shafts through authorized service networks. The growth of last-mile delivery and regional distribution centers expands the light commercial vehicle fleet, further reinforcing shaft consumption. Construction equipment utilization linked to highway modernization and urban development projects increases off-highway vehicle demand for specialized driveline components. Domestic manufacturing incentives support localized component production, stabilizing supply chains and encouraging capital investment in shaft balancing technologies. Improved metallurgy and lightweight alloy innovations enable manufacturers to meet efficiency standards without sacrificing load-bearing strength. Collectively, infrastructure expansion and logistics intensification establish sustained revenue potential for propeller shaft producers across multiple vehicle categories.

Market Challenges

Shift Toward Electrification and Alternative Drivetrain Architectures

The accelerating transition toward battery electric vehicles introduces structural uncertainty for conventional propeller shaft demand because many electric platforms adopt integrated e-axle systems that eliminate traditional longitudinal driveline configurations. Electric drivetrains frequently utilize compact motor and reduction gear assemblies directly mounted on axles, reducing reliance on multi-piece shaft systems common in internal combustion vehicles. As automakers increase investment in electric platform development, long-term volume forecasts for conventional shaft assemblies may experience pressure, particularly in passenger vehicle segments. While certain electric trucks and performance vehicles still require propeller shafts, overall design evolution favors simplified architectures with fewer mechanical components. Manufacturers must therefore diversify into hybrid-compatible systems or lightweight carbon composite shafts to remain competitive. Capital investment in retooling facilities and material innovation increases financial strain, particularly for mid-sized suppliers operating on narrower margins. Market participants also face uncertainty in forecasting production mix between internal combustion, hybrid, and electric platforms, complicating inventory planning and capital allocation decisions. Supply chain adaptation for new materials such as advanced composites further adds complexity and cost. Consequently, structural drivetrain evolution represents a persistent strategic challenge requiring continuous technological adaptation and portfolio diversification.

Volatility in Raw Material Prices and Supply Chain Constraints

The propeller shaft manufacturing process relies heavily on high-grade steel, aluminum alloys, and precision-machined components, making the market vulnerable to fluctuations in raw material pricing. Global supply chain disruptions, transportation bottlenecks, and geopolitical tensions can significantly impact material availability and procurement costs. Rising input costs compress supplier margins, especially when long-term OEM contracts restrict immediate price pass-through mechanisms. Additionally, dependence on specialized forging and heat treatment facilities creates production bottlenecks during periods of demand surges or operational disruptions. Inventory management becomes increasingly complex when suppliers must balance cost control with production continuity obligations. Labor shortages in manufacturing-intensive regions further strain output capacity and increase operational expenditures. Smaller manufacturers may struggle to absorb sudden commodity price increases without renegotiating supply agreements, risking competitive disadvantage. Variability in freight costs and international shipping rates also influences component pricing, particularly for imported subassemblies. These cumulative pressures introduce cost instability that complicates long-term investment planning and pricing strategies across the propeller shaft value chain.

Opportunities

Development of Lightweight Carbon Fiber and Aluminum Shaft Solutions

Increasing regulatory emphasis on vehicle efficiency and emission reduction opens substantial opportunity for lightweight propeller shaft innovations that reduce rotational mass and improve fuel economy performance. Carbon fiber composite shafts provide superior strength-to-weight ratios compared to traditional steel alternatives, enabling enhanced torque capacity with reduced vibration characteristics. High-performance passenger vehicles and premium pickup trucks increasingly integrate such solutions to achieve efficiency and drivability improvements. Manufacturers investing in automated composite winding technologies can scale production while maintaining structural precision and durability standards. Aluminum multi-piece shafts also offer significant weight reduction advantages, aligning with automaker lightweighting initiatives across platform redesign programs. Strategic partnerships between OEMs and material science firms accelerate commercialization of next-generation driveline components. Adoption of advanced balancing technologies and corrosion-resistant coatings further differentiates premium offerings in competitive bidding environments. The aftermarket segment also presents opportunity for performance upgrade kits targeting enthusiast and commercial fleet markets seeking durability enhancements. As lightweighting remains central to automotive engineering evolution, suppliers positioned at the forefront of composite and alloy innovation stand to capture premium market segments.

Expansion into Hybrid and All-Wheel Drive Platform Integration

The increasing popularity of hybrid vehicles and all-wheel drive configurations across both passenger and commercial segments provides a complementary growth pathway for propeller shaft manufacturers. Hybrid architectures often retain mechanical driveline components alongside electric assistance systems, preserving demand for high-strength shaft assemblies. All-wheel drive adoption in SUVs and crossover vehicles enhances torque distribution requirements, reinforcing the need for precision-balanced multi-piece shafts. Consumer preference for enhanced traction, towing capability, and performance stability under varying weather conditions sustains AWD penetration across domestic markets. Suppliers that design adaptable shaft systems compatible with modular hybrid platforms can secure long-term OEM contracts. Enhanced electronic integration capabilities that synchronize driveline components with traction control systems create value-added differentiation. Increasing deployment of hybrid pickup trucks and fleet vehicles ensures that electrification does not entirely displace mechanical torque transmission components. As manufacturers pursue transitional drivetrain strategies combining electric and combustion technologies, propeller shaft producers can leverage hybrid integration expertise to sustain revenue continuity while adapting to evolving platform architectures.

Future Outlook

Over the next five years, the USA propeller shafts market is expected to maintain stable growth supported by sustained light truck production, commercial fleet expansion, and infrastructure-driven freight demand. Technological advancements in lightweight materials and NVH optimization will enhance product differentiation and margin potential. Regulatory pressure on fuel efficiency will accelerate aluminum and composite shaft adoption. Hybrid vehicle proliferation and all-wheel drive configurations will continue to sustain mechanical driveline requirements despite gradual electrification trends.

Major Players

- Dana Incorporated

- American Axle & Manufacturing

- Meritor Inc.

- Neapco Holdings

- GKN Automotive

- IFA Rotorion

- JTEKT Corporation

- Hyundai WIA

- Showa Corporation

- Nexteer Automotive

- SKF Group

- Linamar Corporation

- Dorman Products

- AAM Metal Forming

- GMB Corporation

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive OEM manufacturers

- Commercial vehicle manufacturers

- Aftermarket automotive distributors

- Logistics fleet operators

- Automotive component suppliers

- Infrastructure development companies

Research Methodology

Step 1: Identification of Key Variables

Primary variables including production volume, vehicle mix, drivetrain configuration, material innovation, and aftermarket demand were identified. Secondary variables such as regulatory developments and raw material trends were incorporated to ensure comprehensive coverage.

Step 2: Market Analysis and Construction

Quantitative data from automotive trade bodies, industry publications, and financial disclosures were consolidated to construct market valuation models. Segmentation analysis was performed based on product type and vehicle classification.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from OEM procurement, driveline engineering, and fleet management were consulted to validate demand assumptions. Cross-verification ensured alignment between production forecasts and component sourcing volumes.

Step 4: Research Synthesis and Final Output

Data insights were synthesized into structured market analysis covering segmentation, competition, and forward-looking opportunities. Final validation ensured logical consistency, factual accuracy, and relevance to investment and strategic planning stakeholders.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Production of Commercial and Utility Vehicles

Increasing Demand for All Wheel Drive and Four Wheel Drive Systems

Expansion of Logistics and Construction Sectors - Market Challenges

Volatility in Steel and Aluminum Prices

Shift Toward Electric Drivetrains Reducing Traditional Shaft Demand

Stringent Emission and Efficiency Standards - Market Opportunities

Development of Lightweight Carbon Fiber Shafts

Growth in Performance and Motorsport Applications

Expansion of Remanufacturing and Refurbishment Services - Trends

Integration of Advanced Balancing Technologies

Adoption of High Strength Alloy Materials

Growing Preference for Modular Driveline Systems - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Single Piece Propeller Shafts

Multi Piece Propeller Shafts

Slip in Tube Shafts

Constant Velocity Shafts

Lightweight Composite Shafts - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Off Highway Vehicles

Military Vehicles - By Fitment Type (In Value%)

OEM Fitment

Aftermarket Replacement

High Performance Upgrades

Remanufactured Units

Custom Engineered Solutions - By End User Segment (In Value%)

Automotive Manufacturers

Fleet Operators

Defense Contractors

Construction Equipment OEMs

Agricultural Machinery Manufacturers - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier 1 Suppliers

Automotive Aftermarket Distributors

Online B2B Platforms

- Market Share Analysis

- Cross Comparison Parameters (System Configuration, Material Composition, Torque Rating, Vehicle Segment Compatibility, OEM vs Aftermarket Presence, Manufacturing Process Technology, Average Product Lifespan, Pricing Tier Positioning, Distribution Network Strength, R&D Investment Intensity)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Dana Incorporated

American Axle and Manufacturing

Meritor Inc

Neapco Holdings

GKN Automotive

NTN Corporation

JTEKT Corporation

Schaeffler Group

ZF Friedrichshafen AG

Hyundai Wia

Showa Corporation

Yamada Manufacturing

IHS Automotive Driveline

Precision Shaft Technologies

Driveshaft Specialists Inc

- Automotive OEMs focusing on drivetrain efficiency and durability

- Fleet operators prioritizing maintenance cost optimization

- Defense sector demanding high torque and ruggedized solutions

- Aftermarket service providers driving replacement demand

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now