Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA regenerative braking systems market reached approximately USD ~ billion based on a recent historical assessment, supported by strong electric vehicle and hybrid vehicle production volumes reported by the U.S. Department of Energy and automotive industry associations. Rising battery electric vehicle sales exceeding million units and expanding hybrid penetration have accelerated integration of brake-by-wire and energy recovery systems. Federal incentives, stricter fuel economy regulations, and advancements in silicon carbide power electronics have collectively strengthened domestic system deployment across passenger and commercial platforms.

California, Michigan, Texas, and Ohio dominate the USA regenerative braking systems market due to their concentration of automotive manufacturing facilities, technology research centers, and electric vehicle assembly plants. California benefits from zero-emission vehicle mandates and extensive charging infrastructure, while Michigan and Ohio remain central hubs for suppliers and brake system manufacturing. Texas supports commercial fleet electrification initiatives and electric truck deployment, reinforcing regional leadership in regenerative braking technology adoption and supply chain integration.

Market Segmentation

By Product Type

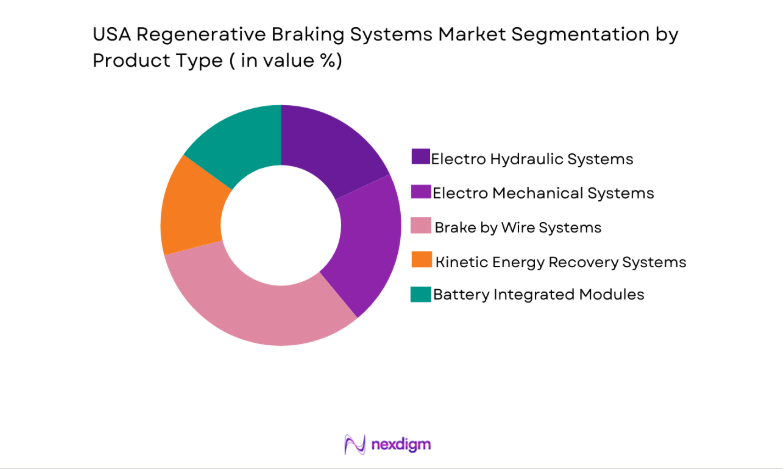

USA Regenerative Braking Systems market is segmented by product type into electro hydraulic systems, electro mechanical systems, brake by wire systems, kinetic energy recovery systems, and battery integrated regenerative modules. Recently, brake by wire systems have a dominant market share due to higher energy recovery efficiency, precise electronic braking control, seamless integration with electric powertrains, improved vehicle stability management, and strong OEM adoption across new electric and hybrid vehicle architectures.

By Platform Type

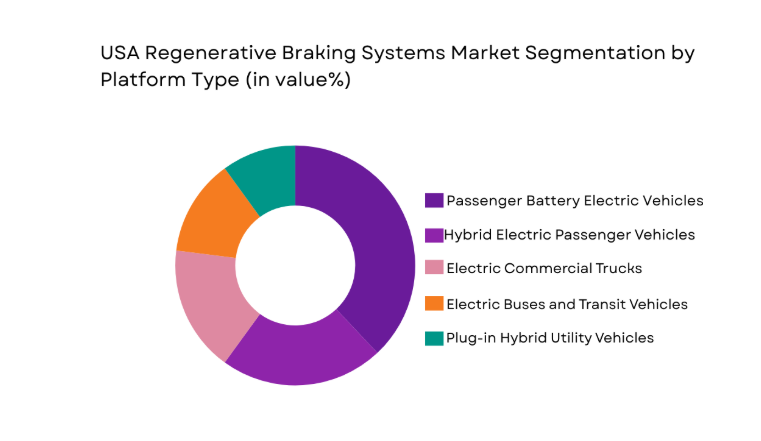

USA Regenerative Braking Systems market is segmented by product type into electro hydraulic regenerative braking systems, electro mechanical regenerative braking systems, brake by wire regenerative systems, kinetic energy recovery systems, and integrated battery coupled regenerative modules. Recently, brake by wire regenerative systems have a dominant market share due to higher energy recovery efficiency, precise electronic braking control, seamless integration with electric powertrains, improved vehicle stability management, and strong OEM adoption across new electric and hybrid vehicle architectures.

Competitive Landscape

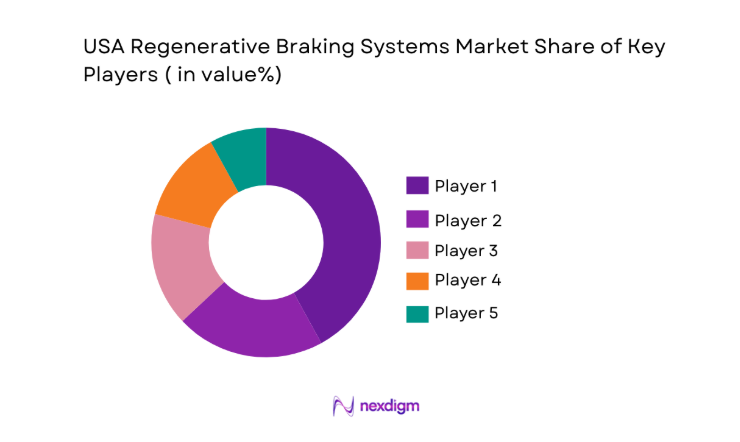

The USA regenerative braking systems market is moderately consolidated, with leading global automotive suppliers controlling significant technological capabilities and long-term OEM contracts. Major players leverage integrated brake-by-wire platforms, silicon carbide power electronics, and strategic partnerships with electric vehicle manufacturers to strengthen their positions. Continuous investments in R&D, vertical integration, and supply chain localization influence competitive intensity and pricing structures across passenger and commercial vehicle segments.

| .

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Partnerships |

| Robert Bosch GmbH | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| BorgWarner Inc | 1928 | USA | ~ | ~ | ~ | ~ | ~ |

USA Regenerative Braking Systems Market Analysis

Growth Drivers

Accelerating Electric Vehicle Production and Federal Incentives

The rapid expansion of electric vehicle manufacturing capacity across multiple states has significantly increased demand for regenerative braking systems as a core component of energy efficiency and range optimization strategies. Federal tax credits, clean transportation grants, and infrastructure funding programs have strengthened EV affordability and stimulated higher consumer adoption, directly influencing regenerative braking integration rates. Automotive OEMs are prioritizing electrified platforms that require advanced brake-by-wire systems capable of maximizing energy recovery and ensuring smooth deceleration control. Rising domestic battery production and localized supply chains have further enabled system standardization across vehicle portfolios. The growing presence of dedicated EV assembly plants has reduced dependence on imported subsystems and encouraged Tier 1 suppliers to expand production capabilities within the United States. Urban fleet electrification initiatives and public transit modernization programs have accelerated deployment of regenerative braking in buses and delivery vehicles. Increasing fuel economy standards have compelled automakers to integrate efficient energy recapture technologies even in hybrid models. Continuous technological innovation in silicon carbide inverters and advanced motor controllers has improved regenerative efficiency and system durability. Consumer awareness regarding energy savings and extended driving range has reinforced manufacturer focus on regenerative braking as a differentiating performance feature.

Advancements in brake by wire and integrated power electronics

The transition from traditional hydraulic braking systems to electronically controlled brake-by-wire architectures has transformed the regenerative braking landscape by enabling seamless blending of mechanical and electrical braking forces. Modern brake-by-wire systems allow precise torque modulation, improving vehicle stability and maximizing kinetic energy recovery during deceleration events. Integration with advanced driver assistance systems has created new performance requirements that favor fully electronic regenerative platforms. Silicon carbide based power electronics enhance conversion efficiency and thermal performance, allowing greater energy recapture under varying driving conditions. OEMs are increasingly adopting scalable modular platforms that integrate braking, motor control, and battery management systems within unified electronic control units. This consolidation reduces vehicle weight and optimizes packaging efficiency in electric and hybrid vehicles. The development of predictive braking algorithms using real time data analytics further improves regeneration accuracy and system responsiveness. Continuous research investments by leading Tier 1 suppliers are reducing system costs while enhancing reliability standards. Strong collaboration between semiconductor manufacturers and automotive OEMs supports innovation in high voltage architectures and next generation energy recovery systems.

Market Challenges

High Integration Costs and Legacy Platform Constraints

The implementation of regenerative braking systems within existing internal combustion engine vehicle platforms presents significant engineering and financial challenges for automakers transitioning toward electrification. Retrofitting legacy architectures with brake-by-wire components requires extensive redesign of control systems, electronic modules, and power distribution networks. High initial capital investment for research, tooling, and validation testing increases overall production costs, especially for smaller manufacturers with limited scale advantages. Supply chain complexity involving semiconductors, sensors, and high voltage components further elevates system expenses. Thermal management requirements and durability testing standards impose additional compliance costs on suppliers. Variability in vehicle weight classes and performance specifications complicates standardization efforts across diverse product portfolios. Economic uncertainty and fluctuating raw material prices can impact procurement strategies and long term investment planning. Dependence on specialized semiconductor technologies exposes manufacturers to supply disruptions and pricing volatility. These integration and cost pressures may delay widespread deployment in certain vehicle categories despite strong regulatory encouragement.

Semiconductor Supply Vulnerabilities and Technological Dependence

Regenerative braking systems rely heavily on advanced semiconductor components, including microcontrollers, power modules, and silicon carbide devices, creating exposure to global supply chain disruptions. Concentration of semiconductor fabrication capacity outside the United States increases vulnerability to geopolitical tensions and trade restrictions. Lead time volatility and allocation challenges can delay vehicle production schedules and hinder timely system integration. Rapid technological evolution in power electronics requires continuous R&D investment to remain competitive, placing financial strain on suppliers. Compatibility issues between new semiconductor platforms and legacy vehicle control systems demand extensive validation processes. Intellectual property concentration among a limited number of global chip manufacturers may restrict design flexibility and bargaining power. Price fluctuations in semiconductor markets can significantly impact overall system cost structures. Limited domestic fabrication capacity for high voltage automotive grade chips further complicates supply resilience strategies. These technological dependencies introduce operational risk and strategic uncertainty across the regenerative braking value chain.

Opportunities

Expansion of Commercial Fleet Electrification Programs

Growing commitments by logistics companies and municipal transit agencies to electrify vehicle fleets present substantial opportunities for regenerative braking system manufacturers. Electrified delivery vans and urban buses operate in stop and go traffic conditions that maximize the efficiency benefits of energy recovery technologies. Federal and state funding programs targeting clean transportation accelerate fleet replacement cycles and encourage adoption of advanced braking architectures. Fleet operators prioritize lower total cost of ownership, and regenerative braking contributes to extended brake life and improved energy efficiency. Partnerships between OEMs and fleet operators enable customized regenerative solutions optimized for commercial duty cycles. Integration of telematics systems allows monitoring of energy recovery performance and predictive maintenance scheduling. Urban sustainability initiatives support large scale procurement of electric buses and trucks, strengthening long term demand visibility. Domestic manufacturing incentives encourage suppliers to localize production facilities, reducing logistics risks. As commercial electrification scales, regenerative braking suppliers can leverage high volume contracts to enhance economies of scale and technological innovation.

Integration with Autonomous and Connected Vehicle Platforms

The evolution of autonomous driving technologies creates significant growth potential for regenerative braking systems integrated with advanced vehicle control architectures. Autonomous vehicles require highly precise braking modulation to ensure passenger safety and optimized route efficiency. Regenerative braking systems equipped with predictive algorithms can anticipate deceleration needs based on sensor data and navigation inputs. Connected vehicle ecosystems enable real time traffic information exchange, enhancing regeneration planning and energy management strategies. Collaboration between software developers and brake system manufacturers fosters development of intelligent energy recovery models. Autonomous commercial fleets operating in urban environments benefit from enhanced braking reliability and reduced mechanical wear. Integration with over the air update capabilities allows continuous performance optimization without hardware replacement. Increased investment in vehicle to infrastructure communication expands opportunities for coordinated braking and energy efficiency improvements. As autonomous and connected technologies mature, regenerative braking systems will become central to integrated vehicle control frameworks and sustainable mobility solutions.

Future Outlook

Over the next five years, the USA regenerative braking systems market is expected to expand steadily due to sustained electric vehicle adoption, stronger domestic semiconductor investments, and increasing commercial fleet electrification. Advancements in silicon carbide technology and integrated brake by wire systems will enhance efficiency and cost competitiveness. Regulatory support for zero emission transportation and infrastructure modernization will reinforce long term demand. Growing collaboration between OEMs, battery manufacturers, and semiconductor firms will further accelerate technological evolution and market penetration.

Major Players

Robert Bosch GmbH

- ZF Friedrichshafen AG

- Continental AG

- Denso Corporation

- BorgWarner Inc

- Aisin Corporation

- Hyundai Mobis

- HitachiAstemoLtd

- Magna International Inc

- Brembo S.p.A.

- Eaton Corporation

- Mando Corporation

- Valeo SA

- Tenneco Inc

- Nissin Kogyo Co Ltd

Key Target Audience

- Automotive OEMs

- Electric vehicle manufacturers

- Commercial fleet operators

- Tier 1 automotive suppliers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Public transportationauthorities

- Semiconductor manufacturers

Research Methodology

Step 1: Identification of Key Variables

Key performance indicators including EV production volumes, hybrid penetration rates, semiconductor supply metrics, and brake system integration levels were identified to define analytical boundaries. Regulatory frameworks and incentive structures were incorporated to refine demand side assessment.

Step 2: Market Analysis and Construction

Primary data from automotive associations and government transportation databases were combined with secondary financial disclosures of major manufacturers to construct the market model. Value chain mapping and cost benchmarking were integrated into the analytical framework.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including automotive engineers and supply chain specialists validated assumptions related to system efficiency, pricing structures, and deployment trends. Feedback loops were incorporated to adjust demand projections and competitive positioning analysis.

Step 4: Research Synthesis and Final Output

Quantitative modeling and qualitative insights were synthesized to generate comprehensive market forecasts and competitive intelligence. Final outputs were structured to provide strategic clarity for stakeholders and decision makers.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising electric vehicle production across major automotive hubs

Federal and state incentives promoting EV adoption

Advancements in battery efficiency improving energy recovery rates

Stricter emission norms driving electrification

Expansion of urban electric bus fleets - Market Challenges

High system integration costs in legacy vehicle platforms

Thermal management complexities in high load applications

Dependence on semiconductor supply chains

Compatibility issues in multi platform deployment

Maintenance complexity in advanced brake by wire systems - Market Opportunities

Integration with autonomous driving systems

Retrofit solutions for commercial fleet electrification

Development of lightweight high efficiency brake materials - Trends

Increasing adoption of brake by wire architecture

Integration of regenerative systems with vehicle energy management software

Shift toward silicon carbide power electronics

Growing collaboration between OEMs and battery manufacturers

Expansion of predictive maintenance analytics - Government Regulations & Defense Policy

Federal fuel economy standards influencing regenerative system adoption

State level zero emission vehicle mandates

Infrastructure grants supporting electric transit modernization - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Electro Hydraulic Regenerative Braking Systems

Electro Mechanical Regenerative Braking Systems

Integrated Brake by Wire Regenerative Systems

Kinetic Energy Recovery Systems

Battery Integrated Regenerative Modules - By Platform Type (In Value%)

Passenger Electric Vehicles

Hybrid Electric Vehicles

Commercial Electric Vehicles

Electric Buses

Plug in Hybrid Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Retrofit Systems

Integrated Powertrain Solutions

Modular Brake Assemblies

High Performance Custom Systems - By EndUser Segment (In Value%)

Passenger Vehicle Manufacturers

Commercial Fleet Operators

Public Transportation Authorities

Logistics and Delivery Companies

Automotive Tier 1 Suppliers - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier 1 Supplier Agreements

Government Fleet Procurement Programs

Private Fleet Tenders

Aftermarket Distribution Networks - By Material / Technology (in Value %)

Silicon Based Power Electronics

Advanced Lithium Ion Battery Integration

Carbon Ceramic Brake Components

Smart Sensor Embedded Systems

AI Enabled Energy Recovery Algorithms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Efficiency, Integration Capability, Thermal Management, Cost Structure, Technology Partnerships)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Robert Bosch GmbH

ZF Friedrichshafen AG

Continental AG

Denso Corporation

Hitachi Astemo Ltd

BorgWarner Inc

Aisin Corporation

Hyundai Mobis

Nissin Kogyo Co Ltd

Brembo S.p.A.

Magna International Inc

Valeo SA

Eaton Corporation

Mando Corporation

Tenneco Inc

- Passenger vehicle OEMs focusing on energy optimization to extend driving range

- Fleet operators adopting regenerative systems to reduce operating costs

- Public transport agencies prioritizing electrified bus integration

- suppliers investing in modular scalable regenerative platforms

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now