Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Seat Frames market reached approximately USD ~ billion based on a recent historical assessment, supported by domestic automotive production data and component shipment statistics published by the U.S. Bureau of Economic Analysis and the Federal Reserve’s industrial output records. Demand is primarily driven by strong SUV and pickup truck assembly volumes, increasing integration of power-adjustable seating systems, and adoption of advanced high-strength steel structures for enhanced crash performance and lightweight optimization across passenger and commercial vehicles.

Detroit, Michigan remains a central hub due to concentration of major OEM headquarters and suppliers, while Ohio and Tennessee host extensive automotive manufacturing clusters supported by advanced metal fabrication facilities. Southern states such as Alabama and Kentucky contribute significantly because of expanding vehicle assembly plants and integrated supply chains. These regions dominate due to established logistics networks, skilled labor availability, and proximity to high-volume vehicle production platforms requiring consistent seat frame procurement.

Market Segmentation

By Product Type

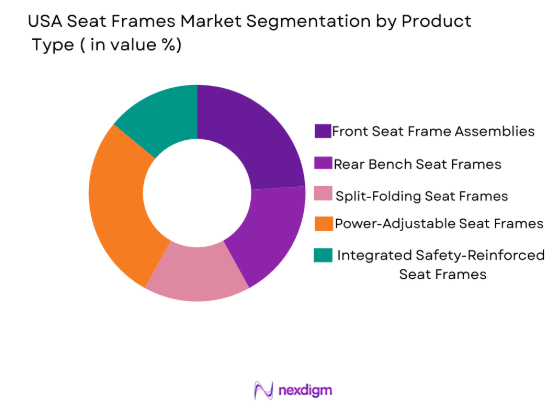

USA Seat Frames market is segmented by product type into front seat frame assemblies, rear bench seat frames, split-folding seat frames, power-adjustable seat frames, and integrated safety-reinforced seat frames. Recently, power-adjustable seat frames has a dominant market share due to factors such as rising consumer preference for comfort features, increasing OEM bundling of electronic seat controls in mid-range vehicles, broader adoption of memory seating functions in SUVs and pickup trucks, and higher structural complexity compared to manual frame systems, which increases average component value and production demand across domestic manufacturing facilities.

By Platform Type

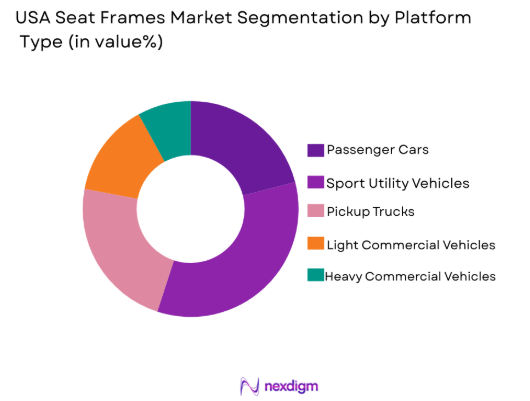

USA Seat Frames market is segmented by platform type into passenger cars, sport utility vehicles, pickup trucks, light commercial vehicles, and heavy commercial vehicles. Recently, sport utility vehicles has a dominant market share due to factors such as sustained consumer demand for larger vehicle formats, higher seat structural complexity in multi-row configurations, increased integration of premium seating technologies, and strong domestic production volumes concentrated in SUV assembly plants across the Midwest and Southern United States, which elevates component procurement requirements for reinforced and modular seat frame structures.

Competitive Landscape

The USA Seat Frames market is moderately consolidated, with major Tier-1 automotive seating manufacturers maintaining long-term OEM supply contracts and vertically integrated production facilities. Competitive positioning is influenced by manufacturing automation capabilities, lightweight material expertise, engineering customization, and geographic proximity to vehicle assembly plants. Strategic partnerships and multi-year procurement agreements strengthen the influence of established players while smaller specialized fabricators focus on niche or aftermarket segments.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Manufacturing Footprint |

| Adient plc | 2016 | Plymouth, USA | ~ | ~ | ~ | ~ | ~ |

| Lear Corporation | 1917 | Michigan, USA | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Ontario, Canada | ~ | ~ | ~ | ~ | ~ |

| Faurecia Seating | 1997 | Nanterre, France | ~ | ~ | ~ | ~ | ~ |

| Toyota Boshoku | 1918 | Aichi, Japan | ~ | ~ | ~ | ~ | ~ |

USA Seat Frames Market Analysis

Growth Drivers

Rising SUV and Pickup Production Volumes Across Domestic Assembly Plants

The significantly stimulate structural seat frame demand because these vehicle categories require reinforced multi-row seat assemblies, enhanced load-bearing capacity, and advanced adjustability mechanisms that increase per-unit component value. Strong consumer preference for larger vehicles has encouraged OEMs to expand SUV manufacturing lines in Michigan, Tennessee, Kentucky, and Alabama, thereby increasing procurement contracts for seat frame integrators located within close geographic proximity. Higher ride height configurations and expanded interior cabin dimensions require more complex seat frame geometries, cross-member reinforcements, and optimized welding structures to ensure safety compliance. Electrification trends further amplify SUV production because many new electric models are launched in crossover and utility body formats, increasing demand for lightweight yet rigid seat frame materials. Integration of advanced driver assistance systems and airbag mounting points into seat structures adds engineering complexity that benefits specialized frame manufacturers. Increased disposable income levels and preference for comfort-oriented vehicles support the adoption of power-adjustable seating systems with integrated structural rails and motor housings. OEM strategies focused on platform standardization across SUV families also drive higher production scale of compatible seat frame modules. As domestic assembly capacity expands to meet sustained demand, seat frame suppliers experience higher order volumes and multi-year supply agreements. These combined production and design factors establish sustained structural demand momentum within the USA Seat Frames market.

Integration of Advanced High-Strength Steel and Lightweight Materials in Vehicle Interiors

Accelerates demand for technologically upgraded seat frame systems because automakers seek to reduce overall vehicle mass while maintaining crash integrity and structural durability. Advanced high-strength steel grades allow thinner gauge designs without compromising performance, enabling manufacturers to lower weight while meeting Federal Motor Vehicle Safety Standards. Lightweight optimization is particularly critical for electric vehicles where structural efficiency directly influences driving range and battery performance, increasing the strategic importance of optimized seat frame assemblies. Material innovation also enables modular seat architectures that support flexible interior configurations and foldable seating systems. The use of aluminum alloys and hybrid composite reinforcements supports corrosion resistance and long-term durability in commercial fleets operating under intensive utilization conditions. Automated robotic welding and laser cutting technologies enhance precision in high-strength material fabrication, reducing production defects and ensuring dimensional consistency. OEMs increasingly collaborate with Tier-1 suppliers during early vehicle design stages to integrate lightweight structural concepts, strengthening supplier influence in long-term contracts. Rising regulatory focus on fuel efficiency and emission reduction indirectly reinforces lightweight adoption across interior structural components. Continuous material engineering advancements therefore create a strong and sustained growth trajectory for the USA Seat Frames market.

Market Challenges

Volatility in Steel and Aluminum Raw Material Pricing

presents a substantial challenge for seat frame manufacturers because structural components rely heavily on high-strength metal inputs whose costs fluctuate in response to global trade policies, tariff adjustments, and supply chain disruptions. Sudden increases in steel pricing directly compress supplier margins, particularly when long-term OEM contracts limit the ability to immediately pass cost increases downstream. Domestic sourcing policies and import duties can create short-term supply constraints, forcing manufacturers to diversify procurement channels at potentially higher prices. Inventory management becomes more complex as companies attempt to hedge against unpredictable raw material cycles while maintaining just-in-time delivery commitments to automotive assembly plants. Fluctuations in commodity markets also complicate long-term pricing negotiations with OEM clients that demand cost transparency and predictable supply structures. Smaller fabricators with limited purchasing power face greater exposure to pricing instability compared to globally diversified Tier-1 suppliers. Capital planning for expansion projects becomes more cautious when material costs remain uncertain, slowing investment in new fabrication lines. Additionally, shifts in aluminum demand from other industries such as aerospace and construction intensify competition for supply. These combined financial and operational pressures constrain profitability within the USA Seat Frames market.

High Capital Investment Requirements for Automated Manufacturing Infrastructure

create entry barriers and financial strain because advanced seat frame production increasingly depends on robotic welding cells, hydroforming systems, precision stamping presses, and laser cutting technologies. Establishing or upgrading fabrication facilities demands significant upfront expenditure in equipment, plant layout redesign, and workforce training, which may extend return-on-investment timelines. OEM clients require strict quality assurance and traceability standards, compelling suppliers to invest in digital monitoring systems and advanced inspection technologies. Smaller regional manufacturers may struggle to secure financing for automation upgrades, limiting their competitiveness against global Tier-1 players with diversified capital access. Continuous technological advancement means that equipment purchased today may require modernization within a few years to remain compatible with evolving vehicle architectures. Energy consumption and maintenance costs associated with automated machinery further increase operational expenditure. Workforce upskilling is necessary to operate and maintain high-tech fabrication systems, adding training expenses and potential productivity gaps during transition phases. Regulatory compliance related to workplace safety and environmental standards also adds to infrastructure investment requirements. Collectively, these financial burdens pose structural challenges for sustained expansion within the USA Seat Frames market.

Opportunities

Expansion of Modular Seat Frame Architectures for Electric Vehicle Platforms

presents a significant opportunity because EV manufacturers increasingly require flexible interior layouts that maximize cabin space while accommodating battery pack positioning beneath the floor structure. Modular seat frames allow standardized mounting points, interchangeable components, and scalable designs adaptable across multiple EV models, reducing development cycles and manufacturing complexity. As automakers launch new electric SUVs and crossovers, suppliers capable of delivering lightweight yet structurally optimized modules gain competitive advantage. Integration of sensor mounts and smart seating electronics within modular frames further enhances value creation opportunities. EV-specific structural considerations such as lower center of gravity and altered crash dynamics require redesigned reinforcement strategies, encouraging innovation in frame engineering. Domestic EV production incentives and plant expansions across southern and midwestern states strengthen long-term procurement prospects for specialized suppliers. Collaboration between seat frame manufacturers and battery platform engineers fosters cross-disciplinary innovation that enhances structural compatibility. Modular systems also simplify aftermarket replacement and maintenance processes. This convergence of electrification and modular design evolution offers sustained growth potential within the USA Seat Frames market.

Adoption of Hybrid Composite Reinforced Structural Solutions

offers transformative opportunity because combining advanced high-strength steel with composite reinforcements can significantly reduce component weight while preserving rigidity and crash safety performance. Composite materials enable innovative geometries that traditional metal stamping cannot achieve, allowing optimized stress distribution and enhanced structural efficiency. As regulatory focus on fuel economy and emissions persists, automakers prioritize lightweight interior components to achieve broader efficiency targets. Hybrid structures also provide improved corrosion resistance, extending product lifecycle particularly in commercial fleet applications exposed to harsh operating environments. Technological advances in composite bonding and multi-material joining processes make large-scale production increasingly feasible. Investment in research and development partnerships between material science firms and automotive suppliers accelerates commercialization of these advanced systems. Enhanced aesthetic flexibility and noise vibration reduction properties add further design advantages. Early adopters of hybrid structural technologies can secure long-term OEM contracts by offering differentiated performance benefits. These innovation-driven developments create substantial opportunity within the USA Seat Frames market.

Future Outlook

The USA Seat Frames market is expected to witness steady expansion over the next five years supported by sustained SUV and electric vehicle production growth. Technological advancement in lightweight materials and modular seat architectures will redefine structural engineering standards. Regulatory emphasis on safety compliance and fuel efficiency will further accelerate innovation in frame design. Demand-side factors such as consumer preference for comfort, powered seating, and multi-row vehicle configurations will continue strengthening procurement volumes across domestic manufacturing clusters.

Major Players

- Adient plc

- Lear Corporation

- Magna International

- Faurecia Seating

- Toyota Boshoku Corporation

- TS Tech Co. Ltd.

- NHK Spring Co. Ltd.

- Brose Fahrzeugteile GmbH

- Aisin Corporation

- Martinrea International

- Grupo Antolin

- Inteva Products

- Shiloh Industries

- Tower International

- Guelph Manufacturing Group

Key Target Players

- Automotive OEM Manufacturers

- Tier-1 Automotive Seating Suppliers

- Electric Vehicle Manufacturers

- Commercial Fleet Operators

- Automotive Component Distributors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Aftermarket Retailers

Research Methodology

Step 1: Identification of Key Variables

Primary variables including production volumes, raw material pricing, platform demand, and regulatory compliance metrics were identified to establish the analytical foundation of the USA Seat Frames market assessment.

Step 2: Market Analysis and Construction

Quantitative and qualitative datasets from federal economic records, automotive production statistics, and supplier disclosures were synthesized to construct market value and segmentation frameworks.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts across manufacturing, supply chain, and automotive engineering domains were consulted to validate structural assumptions and ensure alignment with current procurement dynamics.

Step 4: Research Synthesis and Final Output

Validated findings were consolidated into structured analytical outputs incorporating segmentation tables, competitive mapping, and forward-looking strategic evaluation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Expansion of SUV and pickup truck production

Increasing adoption of lightweight materials in vehicle structures

Growing demand for powered and adjustable seating systems

Rising electric vehicle manufacturing capacity

Integration of enhanced crash safety reinforcement designs - Market Challenges

Volatility in steel and aluminum pricing

High capital investment in automated fabrication lines

Supply chain disruptions affecting raw materials

Stringent safety compliance testing requirements

Margin pressure from OEM cost reduction initiatives - Market Opportunities

Development of modular seat frame platforms for EV architectures

Adoption of hybrid composite structural components

Expansion of domestic reshoring initiatives for automotive components - Trends

Increased use of advanced high-strength steel grades

Integration of smart seating mechanisms with sensor mounting points

Shift toward modular seat assemblies for platform standardization

Automation in robotic welding and laser cutting processes

Growth in lightweight structural optimization for EV range improvement - Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standards compliance

Trade policies influencing domestic steel sourcing

Incentives supporting domestic automotive manufacturing expansion

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Front Seat Frame Structures

Rear Bench Seat Frames

Split-Folding Seat Frame Assemblies

Recliner Integrated Frames

Power Adjustable Seat Frame Systems - By Platform Type (In Value%)

Passenger Cars

Sport Utility Vehicles

Pickup Trucks

Light Commercial Vehicles

Heavy Commercial Vehicles - By Fitment Type (In Value%)

OEM Factory Fitment

Aftermarket Replacement

Retrofit Upgrade Systems

Fleet Fitment Programs

Custom Performance Installations - By End User Segment (In Value%)

Automotive OEM Manufacturers

Commercial Fleet Operators

Electric Vehicle Manufacturers

Automotive Aftermarket Retailers

Specialty Vehicle Builders - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier-1 Seat System Integrators

Long-Term Supply Agreements

Spot Purchase Contracts

Aftermarket Distribution Networks - By Material / Technology (in Value %)

High-Strength Steel Frames

Advanced High-Strength Steel Assemblies

Aluminum Alloy Structures

Magnesium Lightweight Frames

Hybrid Composite Reinforced Frames

- Market structure and competitive positioning

- The market is moderately consolidated with global seating system suppliers and specialized frame manufacturers competing on cost efficiency, engineering capability, and supply reliability.

- Market share snapshot of major players

Large integrated seating suppliers maintain strong OEM relationships supported by regional manufacturing footprints. - Cross Comparison Parameters (Manufacturing Capacity, Material Expertise, OEM Partnerships, Automation Level, R&D Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Porter’s Five Forces

- Key Players

Adient plc

Lear Corporation

Magna International Inc.

Faurecia Seating

Toyota Boshoku Corporation

TS Tech Co. Ltd.

Brose Fahrzeugteile GmbH

NHK Spring Co. Ltd.

Aisin Corporation

Guelph Manufacturing Group

Martinrea International Inc.

Tower International Inc.

Shiloh Industries Inc.

Inteva Products LLC

Grupo Antolin

- OEMs prioritize lightweight structural integrity to meet fuel efficiency and EV performance targets

- Fleet operators demand durable and cost-efficient seat frame assemblies for high utilization vehicles

- Electric vehicle manufacturers require optimized structural designs compatible with battery floor architecture

- Aftermarket retailers focus on replacement demand driven by wear and collision repair cycles

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now