Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA seatbelts market is closely aligned with the broader automotive safety systems industry, which according to data published by the National Highway Traffic Safety Administration and the U.S. Department of Commerce contributes several billion ~ USD annually through OEM integration and aftermarket replacement demand. Based on a recent historical assessment, U.S. motor vehicle manufacturing output exceeded USD ~ billion, directly influencing restraint system procurement and compliance-driven installations across passenger and commercial vehicles.

Dominance within the USA seatbelts market is concentrated in automotive manufacturing hubs such as Michigan, Ohio, and Tennessee, where large-scale vehicle assembly plants operate. Michigan remains central due to Detroit’s legacy OEM ecosystem, supported by advanced safety engineering clusters and supplier networks. Southern states including Alabama and Kentucky also exhibit strong presence because of foreign OEM investments, integrated supply chains, and proximity to logistics corridors that facilitate large-scale seatbelt module distribution.

Market segmentation

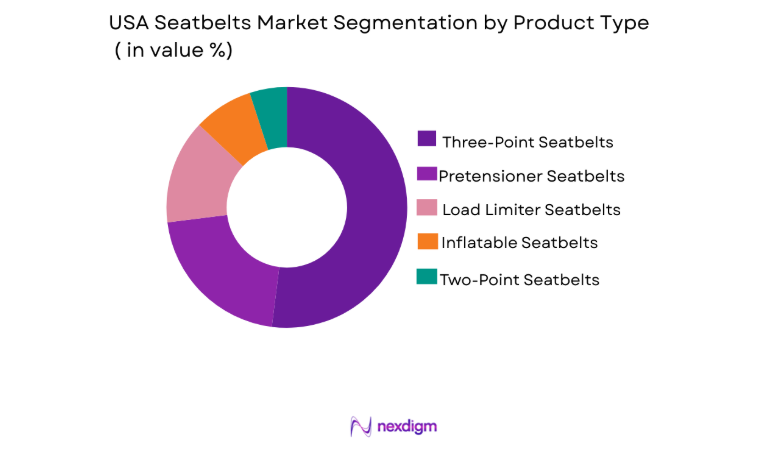

Product Type

USA Seatbelts market is segmented by product type into Three-Point Seatbelts, Two-Point Seatbelts, Pretensioner Seatbelts, Load Limiter Seatbelts, and Inflatable Seatbelts. Recently, Three-Point Seatbelts has a dominant market share due to factors such as regulatory mandates, universal OEM integration, infrastructure compatibility, and consumer safety preference reinforced by federal compliance requirements and crash-test standards that prioritize torso and pelvic restraint efficiency across passenger vehicles and light trucks nationwide.

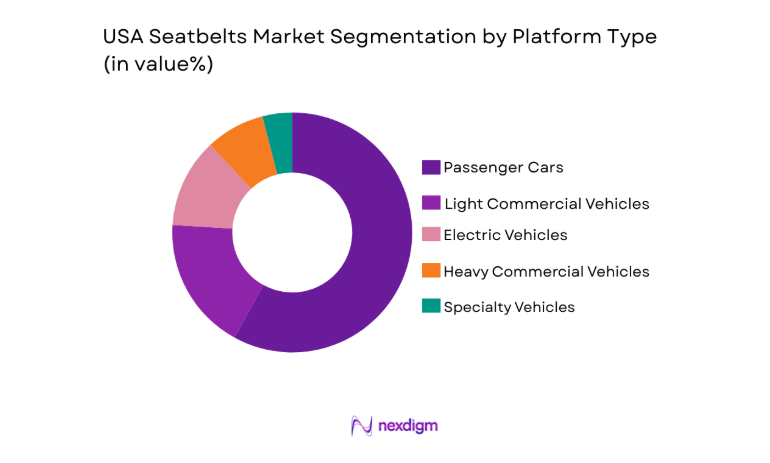

By Platform Type

USA Seatbelts market is segmented by platform type into Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Electric Vehicles, and Specialty Vehicles. Recently, Passenger Cars has a dominant market share due to factors such as higher vehicle production volumes, consistent consumer demand, established manufacturing infrastructure, and mandatory safety integration across all seating positions, resulting in greater procurement volumes compared to commercial and niche vehicle platforms.

Competitive Landscape

The USA seatbelts market exhibits moderate consolidation with a limited number of Tier-1 safety system manufacturers supplying major OEMs under long-term contracts. Technological integration, regulatory compliance capabilities, and global manufacturing footprints provide competitive advantage. Leading players emphasize pretensioner integration, lightweight materials, and advanced load-limiting mechanisms to align with evolving safety protocols.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Safety Integration Capability |

| Autoliv Inc. | 1953 | Stockholm, Sweden | ~ | ~ | ~ | ~ | ~ |

| ZF Friedrichshafen AG | 1915 | Friedrichshafen, Germany | ~ | ~ | ~ | ~ | ~ |

| Joyson Safety Systems | 2018 | Auburn Hills, USA | ~ | ~ | ~ | ~ | ~ |

| Tokai Rika Co., Ltd. | 1948 | Aichi, Japan | ~ | ~ | ~ | ~ | ~ |

| Hyundai Mobis | 1977 | Seoul, South Korea | ~ | ~ | ~ | ~ | ~ |

USA Seatbelts Market Analysis

Growth Drivers

Federal Safety Compliance and Regulatory Enforcement

The USA seatbelts market continues to expand due to strict enforcement of federal motor vehicle safety standards that mandate seatbelt installation across all seating positions in passenger vehicles and most commercial platforms. Regulatory oversight administered by national safety authorities requires OEMs to integrate compliant restraint systems during production, thereby ensuring sustained procurement demand from automotive manufacturers. Crash test protocols and compliance audits further compel automakers to adopt advanced pretensioner and load-limiting technologies to meet evolving performance benchmarks. Continuous updates in safety assessment programs incentivize innovation and push suppliers to enhance reliability and structural durability of restraint mechanisms. Enforcement of occupant protection rules also stimulates aftermarket replacement demand due to inspection requirements following vehicle collisions. Insurance providers frequently mandate seatbelt functionality verification during claim processing, indirectly strengthening service market demand. Public awareness campaigns reinforcing occupant safety benefits contribute to high usage rates, which in turn support regulatory continuity. Combined, regulatory enforcement, compliance-driven manufacturing, and institutional monitoring create a structured demand environment that stabilizes long-term procurement cycles within the USA seatbelts market.

Rising Vehicle Production and Electrification Trends

Sustained vehicle production volumes in the United States directly influence the USA seatbelts market as every new vehicle requires integrated restraint systems for all passenger positions. Growth in electric vehicle assembly plants adds incremental demand because EV platforms maintain equivalent or enhanced safety architecture standards compared to internal combustion vehicles. Investment inflows into automotive manufacturing facilities across southern and midwestern states strengthen supply chain resilience and component sourcing requirements. Electrification also encourages modular platform designs, enabling manufacturers to integrate advanced seatbelt sensors compatible with airbag control units and occupant detection systems. Consumer preference for technologically advanced vehicles reinforces demand for enhanced pretensioner and load-limiting features. Automotive exports contribute additional production stability, indirectly benefiting restraint system suppliers. Strategic partnerships between OEMs and Tier-1 safety manufacturers enable volume-based procurement agreements that secure long-term contracts. Overall vehicle manufacturing scale combined with electrification momentum generates consistent and diversified demand streams for the USA seatbelts market.

Market Challenges

Cost Pressures and Raw Material Volatility

The USA seatbelts market faces persistent cost challenges arising from volatility in raw materials such as high-strength polyester webbing fibers and precision metal components used in retractors and buckles. Fluctuations in steel and synthetic fiber pricing can significantly affect manufacturing margins, particularly for suppliers operating under long-term fixed contracts with automotive OEMs. Global supply chain disruptions periodically increase logistics expenses, leading to procurement uncertainty and extended lead times. Manufacturers must balance compliance with safety standards while controlling per-unit production costs to remain competitive in bidding cycles. Currency fluctuations affecting imported components further intensify financial risk exposure. Additionally, energy costs associated with high-volume manufacturing processes can influence operational expenditure. OEMs frequently demand cost optimization without compromising quality, placing pricing pressure on seatbelt suppliers. This combination of input volatility and procurement negotiation dynamics constrains profitability within the USA seatbelts market.

Technological Integration Complexity with Advanced Safety Systems

Increasing integration of electronic control units and advanced driver assistance systems introduces complexity into seatbelt module design and compatibility testing. Modern vehicles require seamless synchronization between airbags, crash sensors, and seatbelt pretensioners, demanding extensive validation procedures. Engineering redesigns are often necessary when OEM platforms undergo structural changes, increasing development timelines. Compliance testing for crash performance must be conducted across multiple configurations, elevating research and certification costs. Any malfunction risks costly recalls, creating reputational and financial exposure for suppliers. Cyber-physical integration in newer vehicles also necessitates robust communication protocols between restraint modules and onboard systems. Smaller manufacturers may struggle to match the R&D investments required for advanced integration capabilities. These technological and compliance complexities present operational and financial challenges for the USA seatbelts market.

Opportunities

Adoption of Smart and Sensor-Enabled Seatbelt Technologies

The USA seatbelts market presents significant opportunity through integration of smart sensors capable of monitoring occupant positioning, belt tension, and real-time crash data. Automotive manufacturers increasingly seek advanced restraint solutions that enhance coordination with airbag deployment systems and active safety technologies. Sensor-enabled modules can provide diagnostic feedback, supporting predictive maintenance and reducing liability exposure. Integration of weight-detection and occupancy sensors improves passenger-specific safety calibration. Growing interest in connected vehicle ecosystems encourages suppliers to embed communication features within restraint systems. Collaboration between electronics manufacturers and traditional seatbelt suppliers can foster innovation. OEM differentiation strategies based on enhanced safety features create additional procurement potential. These advancements support value-added product development within the USA seatbelts market.

Expansion of Electric and Autonomous Vehicle Platforms

The structural redesign of vehicle interiors in electric and emerging autonomous platforms opens avenues for innovative restraint configurations tailored to flexible seating arrangements. Rotational seats and reconfigurable cabin layouts necessitate adaptable seatbelt anchoring mechanisms and advanced load distribution technologies. Suppliers capable of engineering modular restraint systems compatible with diverse cabin geometries can secure long-term OEM partnerships. Autonomous driving progression may require new safety certification frameworks, creating opportunities for next-generation belt technologies. Increased investment in EV production facilities strengthens localized sourcing requirements. Integration with advanced crash sensing algorithms can differentiate product offerings. As manufacturers compete on safety and comfort innovation, adaptive seatbelt systems represent a scalable growth opportunity within the USA seatbelts market.

Future Outlook

Over the next five years, the USA seatbelts market is expected to experience stable expansion driven by regulatory reinforcement, steady vehicle production, and technological innovation. Electrification trends and evolving crash performance benchmarks will encourage advanced pretensioner and sensor integration. Regulatory authorities are likely to maintain stringent occupant protection requirements, sustaining OEM demand. Increased emphasis on smart safety ecosystems will further strengthen product development and procurement cycles.

Major Players

- Autoliv Inc

- ZF Friedrichshafen AG

- Joyson Safety Systems

- Tokai Rika Co., Ltd.

- Hyundai Mobis

- Takata Corporation

- Ashimori Industry Co., Ltd.

- Far Europe Holding Limited

- Iron Force Industrial Co., Ltd.

- Seatbelt Solutions LLC

- GWR Safety Systems

- APV Safety Products

- Beam’s Seatbelts

- Seatbelt Planet

- Key Safety Systems

Key Target Audience

- Automotive OEM Manufacturers

- Automotive Component Suppliers

- Electric Vehicle Manufacturers

- Commercial Vehicle Manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Automotive Aftermarket Distributors

- Automotive Safety Technology Developers

Research Methodology

Step 1: Identification of Key Variables

Primary variables such as vehicle production output, regulatory compliance mandates, and safety integration requirements were identified. Secondary variables including raw material pricing and OEM procurement trends were also assessed.

Step 2: Market Analysis and Construction

Production data, automotive revenue statistics, and supplier financial disclosures were synthesized to construct market estimations and structural segmentation models.

Step 3: Hypothesis Validation and Expert Consultation

Industry specialists including automotive safety engineers and procurement analysts were consulted to validate demand assumptions and technology integration trends.

Step 4: Research Synthesis and Final Output

Quantitative findings and qualitative insights were consolidated into a structured report framework ensuring alignment with compliance standards and industry benchmarks.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Stringent federal vehicle safety mandates

Increasing vehicle production volumes across passenger and commercial segments

Rising consumer awareness regarding occupant safety - Market Challenges

Price pressure from OEM procurement cycles

Volatility in raw material costs for webbing and metal components

Integration complexity with advanced restraint systems - Market Opportunities

Adoption of smart seatbelt reminder and monitoring systems

Expansion in electric and autonomous vehicle platforms

Retrofit demand in aging vehicle fleets - Trends

Integration of seatbelts with airbag deployment algorithms

Use of lightweight materials to improve fuel efficiency

Incorporation of occupant detection sensors

Growth of modular restraint system architectures

Development of enhanced child safety restraint compatibility - Government Regulations & Defense Policy

Federal Motor Vehicle Safety Standards compliance requirements

National Highway Traffic Safety Administration enforcement initiatives

Crashworthiness and occupant protection policy updates - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Three-Point Seatbelt Systems

Two-Point Lap Belt Systems

Four-Point Harness Systems

Five-Point Harness Systems

Active and Pretensioner-Integrated Seatbelts - By Platform Type (In Value%)

Passenger Vehicles

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Off-Highway Vehicles - By Fitment Type (In Value%)

OEM Factory Installed Systems

Aftermarket Replacement Systems

Retrofit Safety Upgrades

Integrated Seatbelt-Airbag Modules

Child Restraint Compatible Systems - By EndUser Segment (In Value%)

Automotive OEMs

Fleet Operators

Public Transportation Authorities

Defense and Specialized Vehicle Operators

Individual Vehicle Owner - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier-1 Supplier Agreements

Government Safety Tenders

Authorized Automotive Distributors

Online Automotive Parts Platforms - By Material / Technology (in Value %)

Polyester Webbing Systems

Load Limiter Technology

Pretensioner Mechanisms

Smart Sensor-Integrated Seatbelts

High-Strength Steel Buckle Assemblies

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Product Portfolio Breadth, Technology Integration Level, Manufacturing Capacity, OEM Partnership Strength, Pricing Strategy, Aftermarket Presence, R&D Investment, Geographic Footprint)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Autoliv Inc

ZF Friedrichshafen AG

Joyson Safety Systems

Hyundai Mobis Co Ltd

Tokai Rika Co Ltd

Ashimori Industry Co Ltd

GWR Safety Systems

Far Europe Inc

Seatbelt Solutions LLC

Beam’s Seatbelts

APV Safety Products

Indiana Mills and Manufacturing Inc

Safety Belt Services Inc

TRW Automotive Holdings Corp

Ningbo Joyson Electronic Corp

- Automotive OEMs prioritize compliance with evolving safety standards

- Fleet operators emphasize durability and lifecycle cost efficiency

- Public transportation agencies focus on passenger safety mandates

- Defense and specialty vehicle operators require reinforced restraint systems

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030**

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now