Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA semiconductor manufacturing market is expected to witness significant growth, with a market size based on a recent historical assessment estimated to be worth billions of USD. The market is primarily driven by increased demand for semiconductors across key industries such as consumer electronics, automotive, telecommunications, and industrial automation. The continuous advancements in semiconductor technologies, including the development of smaller, more efficient chips, alongside the government’s support for domestic production, have contributed to the growth of the market. These factors, along with supply chain diversification efforts, are expected to sustain the market’s momentum in the coming years.

The United States remains a dominant force in the semiconductor manufacturing market, owing to its advanced technological capabilities and strong industrial infrastructure. Major semiconductor hubs, such as Silicon Valley in California, continue to foster innovation, drawing global investment and talent. The government’s strategic initiatives, such as the CHIPS Act, are designed to enhance the country’s semiconductor manufacturing capabilities, reducing dependency on foreign supply chains. Furthermore, leading semiconductor companies based in the US maintain a competitive edge through continuous innovation, research, and development.

Market Segmentation

By Product Type

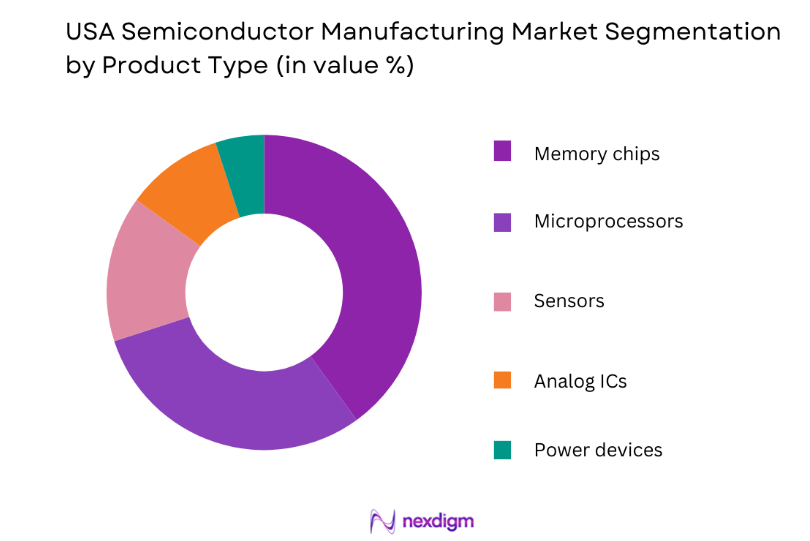

The USA semiconductor manufacturing market is segmented by product type into memory chips, microprocessors, sensors, analog ICs, and power devices. Recently, memory chips have held a dominant market share due to their widespread use in mobile devices, data centers, and consumer electronics. The increasing demand for cloud computing, storage solutions, and high-performance computing has further fueled the need for memory chips. As technology evolves and applications such as artificial intelligence (AI) and the Internet of Things (IoT) proliferate, memory chips continue to be crucial for processing large data volumes efficiently, driving their dominance in the market.

By Application

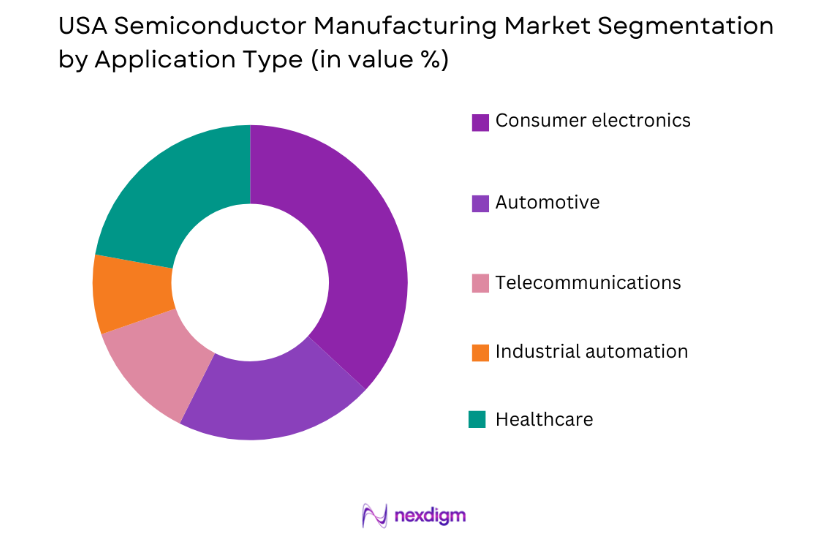

The USA semiconductor manufacturing market is segmented by application into consumer electronics, automotive, telecommunications, industrial automation, and healthcare. Recently, the consumer electronics segment has dominated the market share due to the widespread demand for advanced semiconductors in smartphones, laptops, and other personal electronic devices. The continuous innovations in mobile technology, such as 5G-enabled smartphones and advanced processing capabilities, have significantly increased the demand for high-performance semiconductors. The growing need for smaller, faster, and more energy-efficient chips in consumer electronics is driving this segment’s market dominance, as it aligns with consumer expectations for more powerful devices with longer battery life.

Competitive Landscape

The USA semiconductor manufacturing market is highly competitive, marked by the presence of established industry leaders as well as emerging players investing in next-generation technologies. Major players dominate the market through economies of scale, continuous innovation, and significant R&D expenditures. Consolidation within the market is also notable, with larger companies acquiring smaller firms to strengthen their technology portfolios and expand their market reach. This intense competition encourages ongoing advancements and helps maintain the USA’s competitive edge in semiconductor manufacturing.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Technology Innovation Index |

| Intel | 1968 | Santa Clara | ~ | ~ | ~ | ~ | ~ |

| NVIDIA | 1993 | Santa Clara | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | Dallas | ~ | ~ | ~ | ~ | ~ |

| Micron | 1978 | Boise | ~ | ~ | ~ | ~ | ~ |

| Qualcomm | 1985 | San Diego | ~ | ~ | ~ | ~ | ~ |

USA Semiconductor Manufacturing Market Analysis

Growth Drivers

Technological Advancements in Semiconductor Design

Technological advancements in semiconductor design are one of the primary drivers of growth in the USA semiconductor manufacturing market. The increasing demand for high-performance computing, cloud storage, and AI applications has pushed the need for smaller, faster, and more efficient semiconductors. Innovations such as the development of FinFET (Fin Field-Effect Transistor) technology and 7nm/5nm node chips have significantly improved the performance and power efficiency of semiconductors. These advancements enable companies to meet the needs of modern computing, including real-time processing for autonomous vehicles, smart devices, and data analytics. The continuous progress in semiconductor design ensures that US-based manufacturers remain competitive in the global market, driving the demand for advanced chips. Additionally, innovations in semiconductor materials, such as the use of silicon carbide (SiC) and gallium nitride (GaN), are enhancing semiconductor performance in power applications, further supporting market growth.

Government Initiatives and Investments in Domestic Manufacturing

Government initiatives and investments aimed at boosting domestic semiconductor manufacturing are another key driver of the USA market’s growth. In response to the growing dependency on foreign semiconductor suppliers and disruptions to global supply chains, the US government has introduced policies like the CHIPS Act, which provides substantial funding to support domestic semiconductor research, development, and manufacturing. These initiatives not only aim to reduce the nation’s reliance on overseas suppliers but also seek to maintain the USA’s technological leadership. As a result, the market is witnessing an increase in domestic semiconductor production, with major players expanding their manufacturing capacity within the country. The long-term vision of these government policies is to create a more resilient and self-sufficient semiconductor ecosystem, which will further fuel demand for locally manufactured semiconductors across various industries.

Market Challenges

Supply Chain Disruptions and Dependence on Global Suppliers

One of the significant challenges faced by the USA semiconductor manufacturing market is the ongoing supply chain disruptions and dependence on global suppliers for critical raw materials and components. While semiconductor fabrication in the US has increased, the supply chain remains vulnerable to fluctuations in global material availability, such as rare earth elements and silicon wafers. Recent disruptions, such as those caused by the COVID-19 pandemic and geopolitical tensions, have shown how susceptible the semiconductor supply chain is to external factors. These challenges can lead to delays in production and increased costs for manufacturers, thereby hindering market growth. Although efforts are underway to diversify supply chains, it remains a major hurdle for the industry.

High Capital Investment and Operating Costs

Another challenge for the USA semiconductor manufacturing market is the high capital investment and operating costs associated with building and maintaining semiconductor fabrication facilities (fabs). Semiconductor manufacturing requires cutting-edge technologies, state-of-the-art equipment, and highly specialized facilities, all of which are costly to establish and operate. The high initial investment required to construct a semiconductor fab, combined with the ongoing costs of R&D, materials, and labor, creates a barrier to entry for smaller companies. Additionally, the rapid pace of technological innovation means that existing fabs require frequent upgrades to stay competitive, further increasing operational costs. These high costs can limit the ability of companies to scale production quickly and reduce margins, particularly for newer or smaller manufacturers attempting to enter the market.

Opportunities

Growth in Artificial Intelligence and Machine Learning Applications

The USA semiconductor manufacturing market is presented with a significant opportunity due to the growing demand for semiconductors used in artificial intelligence (AI) and machine learning (ML) applications. As AI and ML continue to evolve, they require powerful, energy-efficient semiconductors capable of handling complex computations. The rise of AI-based technologies in sectors such as healthcare, automotive, and finance is driving the need for specialized semiconductors such as graphics processing units (GPUs), application-specific integrated circuits (ASICs), and system-on-chips (SoCs). As a global leader in AI innovation, the US semiconductor industry is well-positioned to meet the increasing demand for high-performance chips needed to power these applications. Companies like NVIDIA, Intel, and Qualcomm are leading the charge by developing chips specifically designed for AI workloads, which are becoming increasingly critical in a range of industries. The continued growth of AI technology presents substantial opportunities for semiconductor manufacturers to expand their market presence and capitalize on this demand.

Expansion of 5G Networks

The global rollout of 5G networks presents another lucrative opportunity for the USA semiconductor manufacturing market. The deployment of 5G infrastructure requires advanced semiconductors capable of supporting the high-speed, low-latency communication demanded by 5G networks. This includes semiconductors used in base stations, network equipment, and 5G-enabled devices, which are vital for the successful implementation of 5G technology. The United States, with its leadership in both 5G technology and semiconductor manufacturing, is well-positioned to benefit from the expanding demand for 5G chips. US-based companies such as Qualcomm and Intel are actively involved in the development of semiconductors tailored for 5G applications, offering significant growth potential in both domestic and international markets. As 5G networks continue to expand, the demand for semiconductors that support these networks will only increase, creating long-term growth prospects for the semiconductor manufacturing sector.

Future Outlook

The future outlook for the USA semiconductor manufacturing market remains highly positive, driven by technological advancements and increasing demand from industries such as AI, 5G, and automotive. With strong government support and continued investments in research and development, the market is poised to experience steady growth over the next five years. The expansion of semiconductor production capacity, coupled with the rise of new applications in emerging technologies, will provide ample opportunities for companies in the sector. As the demand for advanced chips intensifies, the USA is expected to maintain its leadership position in semiconductor manufacturing, ensuring a resilient and self-sufficient industry.

Major Players

- Intel

- NVIDIA

- Texas Instruments

- Micron

- Qualcomm

- AMD

- Broadcom

- ON Semiconductor

- Analog Devices

- GlobalFoundries

- TSMC

- Applied Materials

- ASML

- Skyworks Solutions

- Marvell Technology

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor manufacturers

- Technology companies

- Telecommunications firms

- Automotive manufacturers

- AI and machine learning firms

Research Methodology

Step 1: Identification of Key Variables

Key variables affecting market dynamics, including technological advancements, government policies, and demand patterns, were identified to shape the research framework.

Step 2: Market Analysis and Construction

A comprehensive analysis of market trends, technological shifts, and consumer demands was conducted using data from trusted sources, including industry reports and government publications.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through consultations with industry experts and stakeholders, ensuring the accuracy of predictions and analysis.

Step 4: Research Synthesis and Final Output

The collected data was synthesized into a final report, providing actionable insights and strategic recommendations for market participants to capitalize on emerging opportunities.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Growth Drivers

Expansion of Electronics Manufacturing and Export Activities

Government Incentives for Domestic Semiconductor Production

Increasing Demand for Semiconductor Chips in AI, 5G, and IoT Applications - Market Challenges

High Capital Requirements for Semiconductor Fabrication Facilities

Supply Chain Dependencies and Global Semiconductor Shortages

Integration Complexities with Legacy Manufacturing Systems - Market Opportunities

Development of Semiconductor Packaging and Testing Hubs in the USA

Strategic Partnerships with Leading Global Semiconductor Foundries

Increasing Demand for High-Performance Chips in Consumer Electronics Manufacturing - Trends

Advancements in Semiconductor Packaging Technologies

Increased Demand for Advanced Chips Supporting Artificial Intelligence and Autonomous Vehicles - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Semiconductor Wafer Fabrication Systems

Semiconductor Assembly and Packaging Systems

Semiconductor Testing Systems

Semiconductor Manufacturing Equipment

Semiconductor Materials and Specialty Chemicals - By Platform Type (In Value%)

Consumer Electronics Manufacturing

Automotive Electronics Manufacturing

Telecommunications Infrastructure Manufacturing

Industrial Electronics Manufacturing - By Fitment Type (In Value%)

Front End Semiconductor Fabrication

Back End Assembly and Packaging

Integrated Semiconductor Manufacturing Facilities

Outsourced Semiconductor Manufacturing Services - By End User Segment (In Value%)

Electronics and Consumer Device Manufacturers

Telecommunications Infrastructure Providers

Automotive and Industrial Electronics Manufacturers

- Market Share Analysis

- Cross Comparison Parameters (Technology Node Capability, Fabrication Capacity, Packaging Technology, Equipment Integration, Supply Chain Partnerships, Pricing Structure, Innovation Capability)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Intel Corporation

Taiwan Semiconductor Manufacturing Company

Samsung Electronics

GlobalFoundries

United Microelectronics Corporation

STMicroelectronics

Infineon Technologies

Texas Instruments

Amkor Technology

ASE Technology Holding

Applied Materials

ASML Holding

KLA Corporation

Lam Research

Foxconn Technology Group

- Electronics Manufacturers Increasing Demand for Integrated Circuit Production

- Telecommunications Companies Expanding Semiconductor Usage for Network Infrastructure

- Automotive Electronics Producers Requiring Semiconductor Components for Smart Vehicles

- Industrial Equipment Manufacturers Utilizing Semiconductor Devices in Automation Systems

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now