Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Solid-State Batteries Market is valued at USD ~ billion based on a recent historical assessment derived from U.S. Department of Energy funding allocations, pilot production disclosures, and publicly reported revenues of leading solid-state developers. Market growth is driven by accelerating research investments, strategic partnerships between automotive OEMs and battery startups, and federal incentives promoting advanced battery innovation. Expanding pilot manufacturing lines and prototype deployments further contribute to early-stage revenue expansion.

California, Michigan, Colorado, and Massachusetts dominate the USA Solid-State Batteries Market due to strong innovation ecosystems, venture capital concentration, and proximity to automotive R&D centers. California leads in startup formation and venture-backed battery technology firms, while Michigan benefits from established automotive engineering infrastructure transitioning toward next-generation battery platforms. Colorado and Massachusetts host advanced materials research institutions and federally supported battery research programs, reinforcing technological development and commercialization efforts.

Market Segmentation

By Product Type

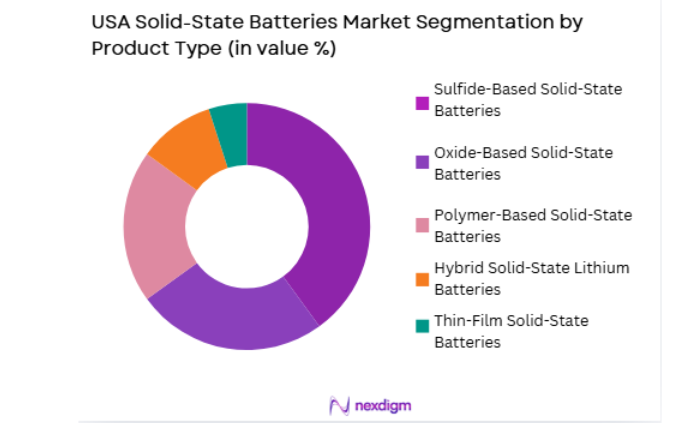

USA Solid-State Batteries Market is segmented by product type into Sulfide-Based Solid-State Batteries, Oxide-Based Solid-State Batteries, Polymer-Based Solid-State Batteries, Thin-Film Solid-State Batteries, and Hybrid Solid-State Lithium Batteries. Recently, Sulfide-Based Solid-State Batteries has a dominant market share due to superior ionic conductivity, compatibility with high-energy-density lithium metal anodes, and strong industry research focus. Automotive OEM collaborations with technology startups have accelerated sulfide electrolyte pilot-scale production. The chemistry enables improved energy density and faster charging performance compared to oxide and polymer alternatives. Investment in scalable sulfide processing techniques further strengthens its leadership. Additionally, sulfide systems demonstrate competitive performance benchmarks for electric vehicle applications, driving stronger commercial interest relative to other emerging solid-state chemistries.

By Platform Type

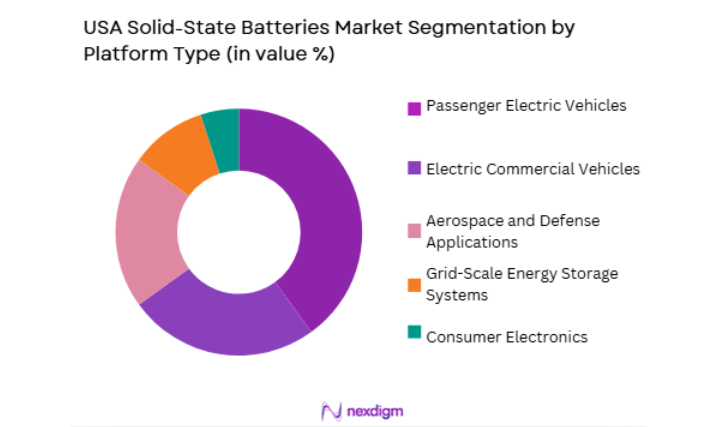

USA Solid-State Batteries Market market is segmented by platform type into Passenger Electric Vehicles, Electric Commercial Vehicles, Aerospace and Defense Applications, Grid-Scale Energy Storage Systems, and Consumer Electronics. Recently, Passenger Electric Vehicles has a dominant market share due to automakers’ pursuit of longer driving ranges, enhanced safety profiles, and competitive differentiation through advanced battery technology. Leading OEMs are integrating solid-state prototypes into premium EV platforms to validate energy density improvements. Federal R&D funding and joint development agreements support pilot deployment in automotive applications. Passenger EV platforms offer the largest commercialization opportunity in terms of unit volumes and revenue concentration. Consequently, automotive integration remains the primary focus of solid-state battery development strategies.

Competitive Landscape

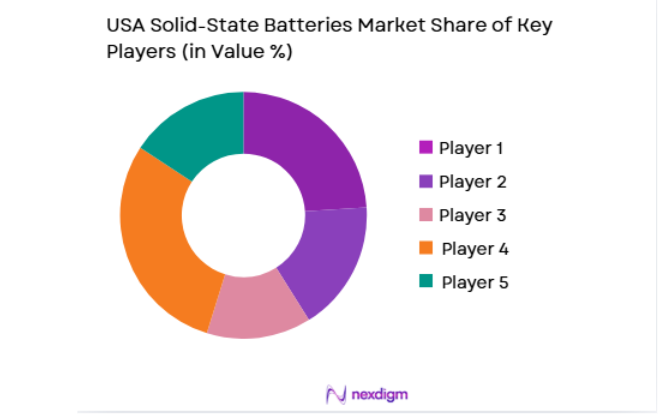

The USA Solid-State Batteries Market is characterized by high R&D intensity, startup-driven innovation, and strategic partnerships with established automotive OEMs. Competition centers on intellectual property portfolios, pilot-scale manufacturing readiness, and electrolyte chemistry performance. Market consolidation is emerging through equity investments, joint ventures, and long-term development agreements aimed at accelerating commercialization timelines.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Pilot Manufacturing Capacity |

| QuantumScape | 2010 | California | ~ | ~ | ~ | ~ | ~ |

| Solid Power | 2012 | Colorado | ~ | ~ | ~ | ~ | ~ |

| Factorial Energy | 2016 | Massachusetts | ~ | ~ | ~ | ~ | ~ |

| SES AI Corporation | 2012 | Massachusetts | ~ | ~ | ~ | ~ | ~ |

| Toyota Motor North America | 1957 | Texas | ~ | ~ | ~ | ~ | ~ |

USA Solid-State Batteries Market Analysis

Growth Drivers

Electrification Demand for Higher Energy Density and Safety

The rapid expansion of electric vehicle adoption across the United States is creating strong demand for next-generation battery systems capable of delivering longer driving ranges and enhanced safety profiles. Solid-state batteries offer higher energy density compared to conventional lithium-ion cells by enabling lithium metal anodes and compact electrolyte structures. Automotive manufacturers seek differentiation through improved performance benchmarks, making solid-state integration a strategic priority. Enhanced thermal stability reduces fire risks and improves regulatory compliance, strengthening consumer confidence in advanced battery systems. Federal fuel economy and emissions standards further push OEMs to adopt technologies that enhance vehicle efficiency. Joint development agreements between automakers and solid-state startups accelerate commercialization timelines. Pilot-scale deployments in premium EV segments validate performance capabilities and attract additional investment. As competition intensifies in the EV market, advanced battery technology becomes a central differentiator driving sustained demand growth for solid-state platforms.

Research Funding and Strategic Investment Ecosystem Expansion

The U.S. Department of Energy and other federal agencies have allocated substantial funding to accelerate advanced battery research and domestic manufacturing capacity. Grants and public-private partnerships reduce financial risk for early-stage solid-state developers pursuing pilot production facilities. Venture capital firms and strategic automotive investors provide additional funding streams, enabling rapid scaling of prototype lines. Innovation clusters in states such as California and Massachusetts benefit from strong academic research ecosystems and skilled workforce availability. Intellectual property development is strengthened through university-industry collaborations supported by federal programs. These financial and institutional mechanisms collectively reduce commercialization barriers. As funding pipelines expand, more companies enter the development landscape, fostering competitive innovation. Sustained investment inflows create long-term structural support for solid-state battery commercialization across automotive, defense, and grid applications.

Market Challenges

Manufacturing Scalability and Process Complexity Constraints

Solid-state battery production involves advanced materials engineering, precise electrolyte deposition, and high-purity manufacturing environments that significantly increase operational complexity. Scaling from laboratory prototypes to gigafactory-level production presents substantial technical challenges. Sulfide electrolytes require controlled atmospheric conditions to prevent degradation, increasing infrastructure costs. Production yield optimization remains a barrier, affecting cost competitiveness compared to conventional lithium-ion technologies. Equipment customization for solid electrolyte integration further raises capital expenditure requirements. Workforce specialization in materials science and advanced manufacturing processes is limited, creating talent shortages. Delays in scaling pilot lines to commercial output levels may affect contractual commitments with automotive OEMs. These manufacturing complexities restrict rapid deployment and contribute to elevated per-unit production costs.

High Commercialization Risk and Competitive Pressure from Lithium-Ion Advancements

Conventional lithium-ion technology continues to improve in energy density, cost efficiency, and safety performance, narrowing the performance gap with emerging solid-state systems. Manufacturers investing heavily in solid-state R&D face uncertainty regarding large-scale commercialization timelines. Automotive OEMs may delay full integration until reliability and lifecycle benchmarks are fully validated. The absence of standardized manufacturing frameworks increases regulatory approval complexity. Capital-intensive pilot plants must achieve technological breakthroughs before scaling decisions are justified. Additionally, supply chain development for specialized solid electrolytes remains underdeveloped. Competitive advancements in lithium iron phosphate and high-nickel chemistries create alternative pathways for OEM performance improvements. This competitive environment increases risk exposure for companies prioritizing solid-state commercialization.

Opportunities

Premium Electric Vehicle Segment Commercialization and Early Adoption

Solid-state batteries present a strong opportunity within the premium electric vehicle segment, where consumers prioritize range, performance, and technological differentiation. Higher manufacturing costs can be absorbed more effectively in luxury vehicle categories, enabling early-stage commercialization. Automotive brands seek competitive advantages by integrating cutting-edge battery systems into flagship models. Successful premium deployment establishes proof of concept and accelerates brand positioning as innovation leaders. Positive performance data from high-end vehicles can encourage broader market adoption. Regulatory incentives supporting domestic advanced battery production further enhance investment attractiveness. Collaborative development programs between startups and established OEMs reduce commercialization risk. Premium EV integration thus represents a strategic entry pathway for large-scale solid-state adoption.

Defense, Aerospace, and Grid Storage Diversification

Solid-state batteries offer enhanced safety and energy density characteristics suitable for aerospace and defense applications requiring secure and lightweight power systems. Military programs prioritize resilient energy storage solutions with reduced flammability risks. Aerospace manufacturers benefit from compact, high-energy storage systems for electric propulsion research. Grid storage applications seeking improved cycle life and safety features present additional commercialization avenues. Federal contracts and government-backed innovation programs support early adoption in these specialized sectors. Diversifying beyond automotive applications reduces dependency on a single demand channel. Successful deployment in defense and aerospace contexts enhances credibility and technical validation. Cross-sector integration strengthens revenue stability and accelerates broader commercialization momentum.

Future Outlook

The USA Solid-State Batteries Market is expected to expand steadily over the next five years as pilot production scales and commercialization milestones are achieved. Continued federal research support and venture investment will accelerate technology maturation. Automotive OEM collaborations are likely to intensify as performance benchmarks improve. Diversification into defense and grid storage applications will further strengthen long-term growth potential.

Major Players

- Quantum Scape

- Solid Power

- Factorial Energy

- SES AI Corporation

- Toyota Motor North America

- Samsung SDI

- LG Energy Solution

- Panasonic Energy

- ProLogium Technology

- Blue Solutions

- Ionic Materials

- Ilika

- Enovix Corporation

- Sila Nanotechnologies

- SK On

Key Target Audience

- Automotive OEMs

- Battery Technology Developers

- Investments and venture capitalist firms

- Government and regulatory bodies

- Defense Contractors

- Aerospace Manufacturers

- Utility and Grid Operators

- Raw Material Suppliers

Research Methodology

Step 1: Identification of Key Variables

Key variables including R&D funding levels, pilot production capacity, joint development agreements, and projected automotive integration were identified. Quantitative and qualitative indicators were mapped to commercialization readiness benchmarks.

Step 2: Market Analysis and Construction

Primary interviews with battery developers and OEM representatives were combined with secondary data from federal agencies and financial disclosures. Market valuation incorporated pilot revenue estimates and investment flows.

Step 3: Hypothesis Validation and Expert Consultation

Technology feasibility, scalability timelines, and demand forecasts were validated through consultation with materials scientists and automotive strategists. Cross-verification ensured consistency with policy and investment trends.

Step 4: Research Synthesis and Final Output

All findings were consolidated into structured market insights supported by financial modeling and scenario evaluation. The final output integrates technological assessment with strategic growth analysis.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising demand for higher energy density EV batteries

Federal R&D funding for advanced battery technologies

Strategic partnerships between automakers and startups - Market Challenges

High manufacturing complexity and scalability barriers

Elevated production costs compared to lithium-ion systems

Limited commercial-scale deployment infrastructure - Market Opportunities

Commercialization of solid electrolyte technologies

Expansion into aerospace and defense energy systems

Integration with next-generation fast-charging architectures - Trends

Shift toward sulfide-based solid electrolytes

Increased pilot-scale manufacturing investments

Focus on enhanced safety and thermal stability - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Polymer-Based Solid-State Batteries

Sulfide-Based Solid-State Batteries

Oxide-Based Solid-State Batteries

Thin-Film Solid-State Batteries

Hybrid Solid-State Lithium Batteries - By Platform Type (In Value%)

Passenger Electric Vehicles

Electric Commercial Vehicles

Grid-Scale Energy Storage Systems

Consumer Electronics

Aerospace and Defense Applications - By Fitment Type (In Value%)

OEM Integrated Battery Systems

Modular Battery Packs

Prototype and Pilot Installations

Aftermarket Replacement Units

Integrated Powertrain Solutions - By End User Segment (In Value%)

Automotive OEMs

Battery Technology Developers

Defense and Aerospace Contractors

Utility and Grid Operators

Electronics Manufacturers - By Procurement Channel (In Value%)

Strategic Joint Development Agreements

Long-Term OEM Contracts

Government Research Grants

- Market Share Analysis

- Cross Comparison Parameters (Cost per kWh, Charging Speed Capability, R&D Investment Intensity, Strategic Partnerships, Intellectual Property Portfolio, Pilot Production Capacity, System Type, Energy Density, Solid Electrolyte Composition, Manufacturing Scalability, Safety Performance, Cycle Life)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Quantum Scape

Solid Power

Toyota Motor North America

Samsung SDI

LG Energy Solution

Panasonic Energy

ProLogium Technology

Factorial Energy

SES AI Corporation

Blue Solutions

Ionic Materials

Ilika

Enovix Corporation

Sila Nanotechnologies

SK On

- Automotive OEMs investing in next-generation battery platforms

- Defense contractors exploring secure and high-density energy storage

- Utility operators evaluating pilot solid-state storage systems

- Technology startups driving innovation through venture funding

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now