Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Sun Visors market current size stands at around USD ~ million, reflecting steady demand driven by ongoing vehicle production cycles, interior feature standardization, and replacement needs across aging fleets. Demand is supported by continuous OEM integration of comfort and safety components, broad aftermarket availability, and recurring wear-related replacement cycles. The market benefits from stable supplier networks, diversified material sourcing, and consistent procurement by vehicle manufacturers and service networks nationwide.

Demand concentration is strongest across automotive manufacturing clusters and high vehicle density corridors, including the Midwest production belt, Southern assembly hubs, and coastal metropolitan regions. These areas combine mature supplier ecosystems, dense dealer and service networks, logistics connectivity, and skilled labor pools. Policy alignment around vehicle safety features, interior compliance standards, and sustainability-driven material shifts further supports adoption, while regional customization preferences influence feature configurations and trim choices.

Market Segmentation

By Vehicle Type

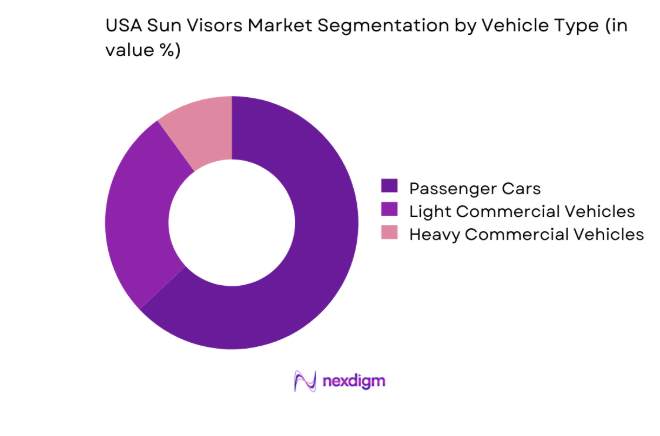

Passenger vehicles dominate demand due to higher production volumes, broader model diversity, and frequent refresh cycles of interior components. Sun visors are standard-fit across sedans, SUVs, and crossovers, with feature differentiation such as illuminated mirrors and extendable panels more prevalent in mid and premium trims. Light commercial vehicles contribute consistent replacement demand driven by high utilization in logistics and services. Heavy commercial vehicles show lower penetration but stable baseline demand linked to regulatory safety compliance and fleet maintenance practices. The dominance of passenger vehicles is reinforced by stronger aftermarket replacement cycles tied to consumer customization and wear-driven upgrades.

By Sales Channel

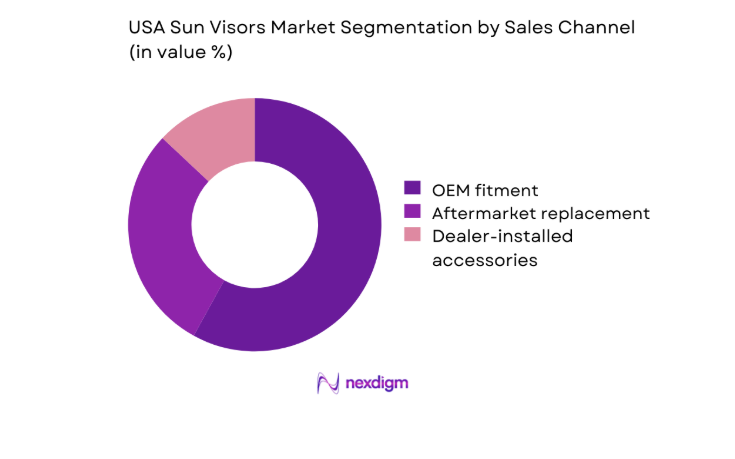

OEM fitment leads the market due to standardized integration of sun visors across vehicle platforms and the inclusion of feature upgrades during model refreshes. OEM sourcing benefits from long-term supply agreements, quality certifications, and synchronized production planning. The aftermarket remains resilient, supported by replacement cycles in older vehicles and consumer demand for customization, particularly for illuminated and premium-trim visors. Dealer-installed accessories bridge OEM and aftermarket dynamics, capturing buyers seeking upgrades at point of sale. Channel dominance reflects strong OEM influence on specifications and volumes, while the aftermarket benefits from fleet wear-and-tear and personalization trends.

Competitive Landscape

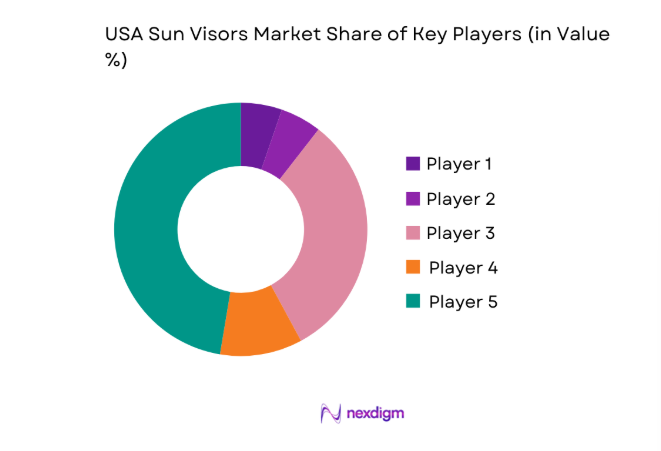

The competitive landscape is characterized by vertically integrated interior component suppliers with strong OEM relationships and specialized manufacturing capabilities. Competition is driven by design integration with vehicle interiors, supply reliability, material innovation, and compliance readiness. Scale, geographic manufacturing footprint, and ability to align with platform refresh cycles shape positioning across OEM and aftermarket channels.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Adient plc | 1883 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Lear Corporation | 1917 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Canada | ~ | ~ | ~ | ~ | ~ | ~ |

| Yanfeng Automotive Interiors | 2010 | China | ~ | ~ | ~ | ~ | ~ | ~ |

| Toyota Boshoku Corporation | 1918 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

USA Sun Visors Market Analysis

Growth Drivers

Rising vehicle production and parc in the US

Vehicle assembly volumes across the United States reached 10.6 million units in 2023, supported by 3 major manufacturing corridors in the Midwest, South, and Southwest. New model introductions exceeded 120 nameplates across passenger and light commercial categories during 2024, expanding interior component demand. The national vehicle parc surpassed 286 million registered vehicles, with average vehicle age at 12.6 years, sustaining replacement cycles for interior fittings. Logistics throughput across 48 continental states strengthened parts distribution. Federal transportation infrastructure programs allocated 110 billion toward mobility corridors, indirectly supporting production continuity, assembly plant modernization, and steady component sourcing across 2022–2025 periods nationwide.

Increasing integration of comfort and convenience features in interiors

Interior feature integration expanded across 2022–2025 as 42 vehicle platforms introduced upgraded cabin packages including illuminated mirrors and extendable visor formats. Manufacturing plants implemented 19 new interior module assembly lines to accommodate feature bundling. Consumer preference shifts toward enhanced cabin ergonomics aligned with 2.5 million premium-trim unit deliveries during 2024. Advanced cockpit integration programs across 6 major automotive clusters emphasized modular interior architectures. Federal safety standards updates across 14 categories encouraged standardized interior fitments. Rising commute times averaging 54 minutes daily in metropolitan regions increased demand for comfort-oriented features, reinforcing OEM prioritization of interior convenience components.

Challenges

Price pressure from OEM cost optimization programs

OEM procurement teams enforced cost reduction targets averaging 4 annually across tiered supplier contracts during 2022–2024. Supplier consolidation reduced approved vendor lists from 12 to 7 across multiple interior modules, intensifying competition. Manufacturing input volatility affected plastics, foams, and trims across 18 material categories. Production line takt time reductions of 9 required component suppliers to compress lead times while maintaining quality compliance. Freight variability across 5 logistics corridors increased operational complexity. Workforce shortages across 23 assembly plants limited flexible shift coverage, constraining capacity utilization and elevating compliance risks within tightly managed procurement frameworks.

Limited product differentiation in entry-level segments

Entry-level vehicle trims across 28 high-volume models standardized interior specifications, limiting feature variance for sun visors. Platform sharing across 14 vehicle architectures constrained design customization. Engineering change approvals averaged 210 days, slowing differentiation cycles. Interior bill-of-material constraints capped component variation across 6 material options. Dealer feedback across 1,400 outlets highlighted low consumer willingness to pay for incremental visor upgrades in base trims. Regulatory uniformity across 9 safety compliance checkpoints further narrowed scope for differentiation. High production cadence across 3 shifts prioritized standardized parts to minimize retooling frequency and changeover complexity.

Opportunities

Integration of smart features such as ambient lighting and sensors

Smart interior integration programs expanded across 2023–2025 with 17 cockpit electronics platforms supporting ambient lighting modules. Cabin sensor deployments across 9 driver monitoring architectures created pathways for integrated visor-mounted lighting cues. Semiconductor supply stabilization increased chip availability by 38 units per vehicle for interior electronics packages. Urban vehicle registrations across 25 metropolitan regions favored tech-enabled trims. Federal safety pilot programs across 4 states evaluated in-cabin alerting enhancements, supporting feature experimentation. Software-defined vehicle rollouts across 11 platforms enabled modular integration of lighting control interfaces, creating scope for differentiated visor feature sets aligned with digital cockpit ecosystems.

Rising demand for premium interior trims in SUVs and trucks

SUV and light truck deliveries reached 8.1 million units in 2024, driven by consumer preference for higher seating positions and utility. Premium trim penetration expanded across 22 high-volume SUV models, with interior upgrade packages bundled into factory options. Manufacturing retooling investments across 9 assembly plants supported premium material integration. Dealer customization programs across 1,200 outlets emphasized interior personalization for high-margin trims. Urban-to-suburban migration across 14 regions increased demand for larger vehicles with enhanced cabin comfort. Fleet replacement cycles across 6 commercial categories also adopted upgraded interior specifications to improve driver retention.

Future Outlook

The market outlook through 2030 reflects steady integration of interior comfort features aligned with platform refresh cycles and digital cockpit evolution. Regulatory alignment on safety and material sustainability will shape design choices. Regional manufacturing hubs are expected to deepen localization strategies. Aftermarket customization will expand alongside aging vehicle fleets. Collaboration across interior ecosystems will influence innovation pace.

Major Players

- Adient plc

- Lear Corporation

- Magna International

- Yanfeng Automotive Interiors

- Toyota Boshoku Corporation

- Grupo Antolin

- TS Tech Co., Ltd.

- Hyundai Mobis

- International Automotive Components

- CIE Automotive

- Ficosa International

- Motherson Group

- Gentex Corporation

- Faurecia SE

- IAC Group

Key Target Audience

- Passenger vehicle OEMs and assembly plants

- Tier-1 automotive interior component suppliers

- Automotive aftermarket distributors and retailers

- Fleet operators and commercial vehicle managers

- Dealer networks and accessory installation partners

- Investments and venture capital firms

- Government and regulatory bodies with agency names

- Automotive logistics and distribution service providers

Research Methodology

Step 1: Identification of Key Variables

Core demand drivers, vehicle platform cycles, interior feature adoption pathways, regulatory checkpoints, and channel dynamics were mapped across OEM and aftermarket contexts. Material flows, assembly dependencies, and logistics touchpoints were defined to frame variable interactions within the interior components ecosystem.

Step 2: Market Analysis and Construction

Production corridors, supplier footprints, platform refresh schedules, and channel structures were analyzed to construct demand linkages. Scenario frameworks captured technology integration pathways, manufacturing capacity constraints, and regional ecosystem maturity across multiple operational environments.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses were refined through structured consultations with interior engineering specialists, manufacturing operations leaders, procurement managers, and distribution channel operators. Cross-validation focused on feasibility of feature integration, compliance readiness, and scalability across production cycles.

Step 4: Research Synthesis and Final Output

Insights were synthesized into coherent narratives linking demand drivers, operational constraints, and opportunity pathways. The final output aligned ecosystem dynamics with strategic implications for stakeholders across OEM, supplier, and aftermarket interfaces.

- Executive Summary

- Research Methodology (Market Definitions and OEM vs aftermarket sun visor classification, Primary interviews with Tier-1 suppliers and automotive interior OEMs, Vehicle parc analysis by segment and production volumes, Dealer and distributor channel pricing audits, Consumer preference surveys on features and materials, Regulatory and safety standard mapping, Teardown cost analysis of visor assemblies)

- Definition and Scope

- Market evolution

- Usage and safety functionality pathways

- Automotive interior ecosystem structure

- Supply chain and distribution channels

- Regulatory and safety environment

- Growth Drivers

Rising vehicle production and parc in the US

Increasing integration of comfort and convenience features in interiors

Growing consumer preference for illuminated and vanity mirror visors

OEM focus on lightweight interior components for fuel efficiency

Customization trends in premium and luxury vehicle segments

Expanding replacement demand in aging vehicle fleet - Challenges

Price pressure from OEM cost optimization programs

Limited product differentiation in entry-level segments

Fluctuations in raw material prices for plastics and trims

Supply chain disruptions affecting automotive interior components

Aftermarket competition from low-cost imports

Design constraints linked to evolving vehicle interior architectures - Opportunities

Integration of smart features such as ambient lighting and sensors

Rising demand for premium interior trims in SUVs and trucks

Electrification-driven interior redesign opportunities

Growth in customized and branded interior accessories

Partnerships with OEMs for next-generation cockpit platforms

Sustainable materials adoption for eco-friendly interiors - Trends

Shift toward lightweight and recyclable visor materials

Increasing adoption of illuminated and dual-panel visors

Premiumization of interior components in mass-market vehicles

Design harmonization with digital cockpit and ADAS layouts

Growth of modular visor assemblies for platform sharing

Rising aftermarket personalization for interior accessories - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Vehicle Type (in Value %)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles - By Propulsion Type (in Value %)

Internal Combustion Engine Vehicles

Hybrid Electric Vehicles

Battery Electric Vehicles - By Sun Visor Type (in Value %)

Conventional sun visors

Illuminated sun visors

Vanity mirror sun visors

Extendable and sliding sun visors - By Material Type (in Value %)

Fabric-covered visors

Leatherette and premium trim visors

Molded plastic visors

Composite and lightweight material visors - By Sales Channel (in Value %)

OEM fitment

Aftermarket replacement

Dealer-installed accessories

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product portfolio breadth, OEM supply footprint, material and design innovation capability, manufacturing scale and localization, cost competitiveness, aftermarket distribution reach, regulatory compliance track record, customization and premium offering depth)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Adient plc

Faurecia SE

Grupo Antolin

Lear Corporation

Yanfeng Automotive Interiors

Magna International

IAC Group

Toyota Boshoku Corporation

TS Tech Co., Ltd.

CIE Automotive

International Automotive Components

Motherson Group

Ficosa International

Hyundai Mobis

Gentex Corporation

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now