Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Switches and Relays market current size stands at around USD ~ million, reflecting steady demand from industrial automation, transportation electrification, power distribution modernization, and building control systems. Market activity is shaped by replacement cycles, safety compliance requirements, and growing system complexity across factories and infrastructure. Procurement patterns emphasize reliability, lifecycle performance, and integration with digital control architectures. Supply dynamics are influenced by domestic manufacturing capacity, qualification cycles for safety-critical components, and multi-tier distribution networks serving OEMs and integrators nationwide.

Demand concentration is strongest across the Midwest and Southeast manufacturing corridors, with additional density in California and Texas driven by technology clusters, energy infrastructure projects, and large-scale logistics hubs. Urban regions with advanced building automation ecosystems show higher adoption of safety-rated switches and smart relays. States with supportive industrial policies and grid modernization programs demonstrate faster uptake, while mature distributor networks and system integrator ecosystems reinforce regional leadership in deployment and service readiness.

Market Segmentation

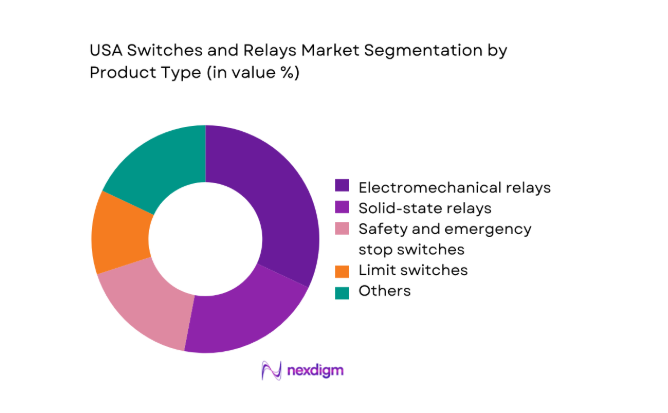

By Product Type

Electromechanical and solid-state relays dominate deployments across industrial control panels, grid protection, and EV charging systems due to proven reliability, broad certification coverage, and compatibility with legacy infrastructure. Limit, safety, and emergency-stop switches show strong penetration in manufacturing cells and logistics automation, driven by compliance mandates and safety audits. Push-button, toggle, and rotary switches maintain relevance in human-machine interfaces for machinery, while hybrid relay designs gain traction in high-cycle applications requiring lower heat dissipation and longer service intervals. Product mix is increasingly shaped by modular panel architectures, OEM standardization efforts, and demand for compact footprints in space-constrained installations.

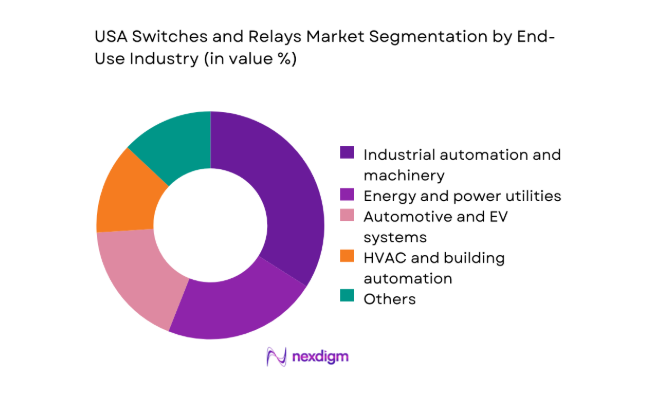

By End-Use Industry

Industrial automation and machinery represent the most dominant end-use due to continuous investments in factory upgrades, robotics integration, and safety retrofits across discrete and process manufacturing. Energy and utilities adoption is driven by substation upgrades, grid automation, and renewable interconnections requiring protection relays and ruggedized switching. Automotive and EV systems show accelerating uptake across battery management, charging infrastructure, and power electronics. HVAC and building automation remain stable contributors as smart building deployments expand. Data centers and telecom facilities increasingly specify high-reliability relays to support power redundancy and uptime requirements across mission-critical environments.

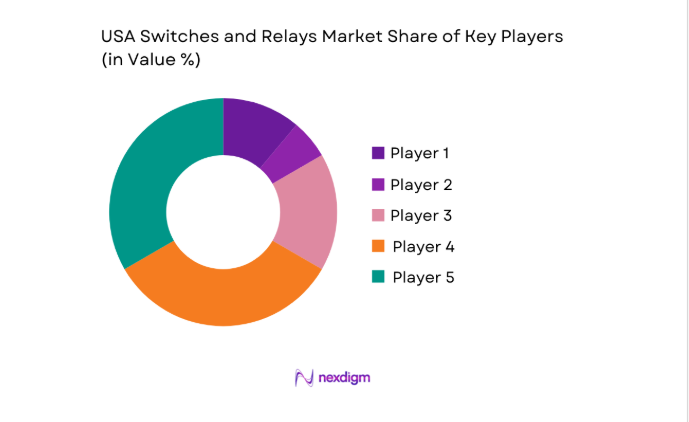

Competitive Landscape

The competitive environment reflects a mix of diversified electrical component manufacturers and specialized switching and relay providers, differentiated by certification coverage, customization capability, delivery performance, and service depth across industrial and infrastructure applications.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Schneider Electric | 1836 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Eaton | 1911 | Ireland | ~ | ~ | ~ | ~ | ~ | ~ |

| ABB | 1883 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

| Siemens | 1847 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Rockwell Automation | 1903 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

USA Switches and Relays Market Analysis

Growth Drivers

Rising automation and smart manufacturing adoption

Manufacturing modernization across the United States is accelerating equipment upgrades within automotive, food processing, and electronics assembly plants. In 2023, the Department of Energy reported 287 advanced manufacturing facilities integrating digital control systems across multiple states. Robotics density expanded across 14 production clusters, while programmable logic controller installations grew by 42000 units supporting safety interlocks and control switching. Federal incentives under infrastructure and manufacturing programs supported 63 regional innovation hubs in 2024, strengthening automation ecosystems. Electrical safety audits conducted by 26 state agencies in 2023 reinforced compliance-driven replacement cycles for safety-rated switches and relays across high-risk industrial environments.

Expansion of EV production and charging infrastructure

Electric vehicle manufacturing scale-up is driving installation of high-reliability switching and protection components across battery assembly, power electronics, and charging networks. In 2024, 17 battery plants were operational across multiple states, with 9 additional facilities under construction. Public charging points exceeded 192000 units, supported by federal and state deployment programs. Grid interconnection approvals for charging corridors were issued across 28 utility service territories, requiring certified relays for protection and load management. Fleet electrification commitments by 12 logistics operators accelerated depot retrofits, increasing demand for industrial-grade switches across power distribution panels.

Challenges

Price volatility of copper, silver alloys, and rare metals

Component manufacturing faces persistent input cost volatility due to fluctuating availability of copper and silver alloys used in contacts and terminals. In 2023, domestic refined copper output declined by 5 units across two major smelting facilities, while silver concentrate imports faced port congestion affecting 11 logistics corridors. Commodity supply constraints forced production rescheduling across 19 component plants, increasing lead-time variability. Industrial users reported 46 contract renegotiations with suppliers due to material volatility during 2024. These disruptions complicate long-term sourcing strategies for OEMs and panel builders, increasing inventory buffers and qualification risks across safety-critical switching components.

Supply chain disruptions and component lead-time variability

Supply chains remain vulnerable to transportation bottlenecks and semiconductor availability affecting hybrid relay production. In 2024, port dwell times across three major West Coast gateways increased by 7 days compared with the prior year. Rail freight capacity constraints affected 23 inland distribution hubs serving industrial corridors. Qualification cycles for safety-rated relays averaged 14 months across regulated installations, delaying substitution options when shortages occur. Inventory shortages affected 31 system integrators supporting utilities and transit agencies, forcing project rescheduling. These constraints elevate working capital needs for distributors and challenge OEM production planning for control panels and electrified systems.

Opportunities

Electrification of transportation fleets and charging networks

Public transit agencies and commercial fleets are accelerating electrification programs, creating sustained demand for high-cycle switching and protection relays within depots and charging corridors. In 2023, 62 transit agencies announced fleet conversion roadmaps covering bus and light-duty vehicles. Depot upgrades across 41 metropolitan areas required certified disconnect switches and fault relays for high-voltage systems. Utility interconnection permits were issued across 29 service regions for depot charging installations in 2024, expanding standardized protection requirements. These deployments favor ruggedized, safety-rated components, enabling suppliers to expand value-added offerings through pre-certified assemblies and integration support for fleet operators nationwide.

Growth in smart buildings and connected HVAC controls

Smart building retrofits across commercial real estate and public infrastructure are increasing adoption of networked relays and safety switches integrated with building management systems. In 2023, 38 municipal retrofit programs targeted energy efficiency upgrades across public facilities. Connected HVAC controller installations reached 74 campuses across healthcare and government buildings in 2024, requiring reliable switching for load management and fault isolation. State energy offices issued 21 building electrification guidelines supporting automation upgrades. These initiatives create demand for compact, low-noise relays and safety switches compatible with digital protocols, enabling suppliers to embed diagnostics and lifecycle monitoring features.

Future Outlook

The market outlook reflects sustained momentum from electrification, automation, and infrastructure modernization initiatives through 2030. Policy support for grid resilience and domestic manufacturing is expected to reinforce replacement demand, while technology shifts toward solid-state and hybrid designs reshape product roadmaps. Regional ecosystems with mature integrator networks are likely to capture earlier adoption of smart control architectures.

Major Players

- Schneider Electric

- Eaton

- ABB

- Siemens

- Rockwell Automation

- Omron

- TE Connectivity

- Panasonic Industry

- Honeywell

- Sensata Technologies

- Fujitsu Components

- Phoenix Contact

- Weidmüller

- Finder Relays

- CIT Relay and Switch

Key Target Audience

- Industrial automation OEMs and panel builders

- Electric vehicle manufacturers and charging infrastructure developers

- Power utilities and grid operators

- Commercial building owners and facility managers

- Data center operators and colocation providers

- Electrical distributors and system integrators

- Investments and venture capital firms

- Government and regulatory bodies with agency names such as the Department of Energy and Federal Energy Regulatory Commission

Research Methodology

Step 1: Identification of Key Variables

Core variables included product certifications, end-use deployment intensity, channel structure, and regional policy drivers influencing adoption. Data points were mapped across industrial, energy, automotive, and building automation use cases. Technical specifications and safety compliance requirements were standardized to ensure consistent comparison across applications.

Step 2: Market Analysis and Construction

Demand patterns were constructed using deployment indicators from infrastructure programs, manufacturing modernization initiatives, and electrification projects. Channel dynamics were assessed across OEM, distributor, and integrator touchpoints. Regional adoption maturity was profiled based on ecosystem readiness and regulatory enforcement intensity.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions on technology shifts and adoption barriers were validated through structured consultations with system integrators, plant engineers, and compliance specialists. Feedback loops refined interpretations of lead-time risks, qualification cycles, and substitution constraints across safety-critical installations.

Step 4: Research Synthesis and Final Output

Findings were synthesized into coherent narratives linking policy drivers, infrastructure investment, and technology transitions. Cross-segment insights were aligned to ensure internal consistency, while scenario implications were stress-tested against regulatory enforcement trends and regional deployment realities.

- Executive Summary

- Research Methodology (Market Definitions and application taxonomy for industrial, automotive, energy, and electronics switching, Primary interviews with OEMs, distributors, and system integrators, Channel checks across electrical wholesalers and e-commerce platforms, Teardown and BOM analysis of end-use equipment, Import-export and tariff analysis for electromechanical components, Regulatory and standards mapping across UL, NEMA, IEEE, SAE)

- Definition and Scope

- Market evolution

- Usage pathways across end-use industries

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising automation and smart manufacturing adoption

Expansion of EV production and charging infrastructure

Grid modernization and renewable energy integration

Data center capacity expansion and power management needs

Retrofit demand for industrial safety and control systems

Reshoring of manufacturing and domestic sourcing incentives - Challenges

Price volatility of copper, silver alloys, and rare metals

Supply chain disruptions and component lead-time variability

Intense price competition from low-cost imports

Qualification cycles and certification costs for safety-critical applications

Technological substitution by semiconductor-based switching

Skilled labor shortages in panel building and maintenance - Opportunities

Electrification of transportation fleets and charging networks

Growth in smart buildings and connected HVAC controls

Upgrades to protection relays in substations and utilities

Customization for harsh environment and safety-rated applications

Aftermarket replacement and retrofit programs

Localization of manufacturing for defense and critical infrastructure - Trends

Shift toward solid-state and hybrid relays for high-cycle applications

Integration of IoT diagnostics and condition monitoring

Miniaturization and higher power density designs

Adoption of safety-rated switches for industrial compliance

Increased use of modular and plug-and-play control architectures

Sustainability-driven material and lifecycle optimization - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Product Type (in Value %)

Electromechanical relays

Solid-state relays

Reed relays

Limit switches

Push-button switches

Toggle and rocker switches

Rotary and selector switches

Safety and emergency stop switches - By Voltage Rating (in Value %)

Low voltage

Medium voltage

High voltage - By Mounting and Form Factor (in Value %)

Panel mount

PCB mount

DIN rail mount

Plug-in and socketed - By End-Use Industry (in Value %)

Industrial automation and machinery

Automotive and EV systems

Energy and power utilities

HVAC and building automation

Consumer electronics and appliances

Telecom and data centers

Railways and transportation - By Distribution Channel (in Value %)

Direct sales to OEMs

Electrical distributors and wholesalers

Online industrial marketplaces

System integrators and panel builders

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product breadth, voltage range coverage, safety certifications, customization capability, delivery lead times, pricing tiers, after-sales support, domestic manufacturing footprint)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Schneider Electric

Eaton

ABB

Siemens

Rockwell Automation

Omron

TE Connectivity

Panasonic Industry

Honeywell

Sensata Technologies

Fujitsu Components

Phoenix Contact

Weidmüller

Finder Relays

CIT Relay and Switch

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now