Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Taillights market current size stands at around USD ~ million and reflects sustained demand across original equipment and replacement channels driven by steady vehicle parc maintenance cycles and design-led lighting differentiation. Procurement activity spans passenger cars, light trucks, and commercial fleets, with technology transitions shaping module complexity and sourcing patterns. Value realization is influenced by regulatory compliance requirements, quality assurance processes, and integration with adjacent rear lighting functions across multiple vehicle platforms nationwide.

Demand concentration is strongest across metropolitan automotive manufacturing corridors and high-density vehicle ownership regions, supported by mature supplier ecosystems, logistics infrastructure, and extensive collision repair networks. Coastal and Sun Belt states show elevated replacement intensity due to traffic density and exposure-related damage. Policy environments emphasizing vehicle safety compliance, combined with strong aftermarket retail penetration and e commerce logistics capabilities, continue to anchor regional hubs for distribution, customization, and service delivery across the country.

Market Segmentation

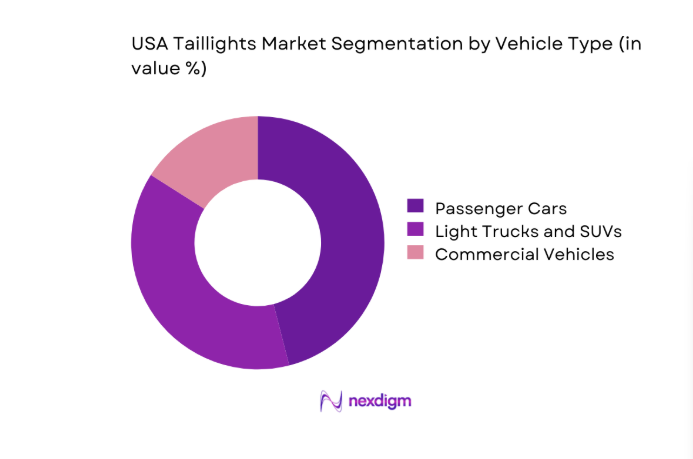

By Vehicle Type

Passenger cars dominate procurement volumes due to higher model proliferation and frequent design refresh cycles that embed signature rear lighting. Light trucks and SUVs contribute rising module complexity as rear lamp assemblies integrate dynamic signaling and larger form factors aligned with vehicle styling. Commercial vehicles present steadier replacement demand tied to fleet utilization intensity and regulatory inspection cycles, with procurement driven by durability requirements and serviceability. Across segments, OEM sourcing prioritizes validated compliance and lifecycle support, while aftermarket demand reflects collision repair throughput and consumer-led customization, reinforcing differentiated product mixes by vehicle class and usage intensity.

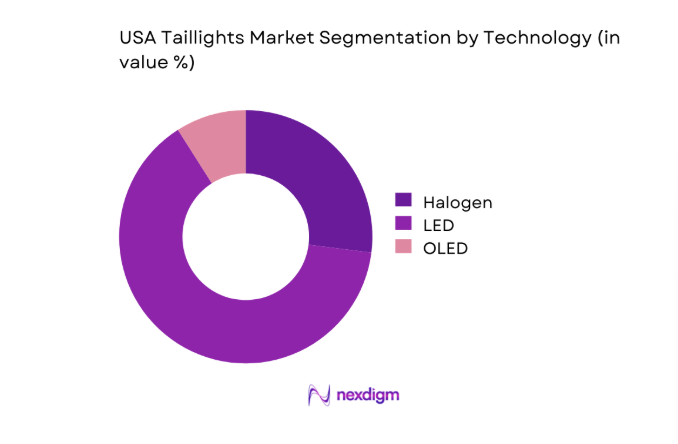

By Technology

LED taillights dominate due to longer operating life, energy efficiency, and design flexibility that supports brand identity through signature lighting patterns. Halogen persists in legacy platforms and cost-sensitive replacements, supported by widespread compatibility and lower retrofit complexity. OLED adoption remains concentrated in premium applications where thin form factors and uniform illumination enable distinctive styling, though supply constraints and qualification timelines limit penetration. Technology choice is influenced by compliance validation cycles, integration with vehicle electronics, and repairability considerations, shaping OEM platform strategies and aftermarket availability across price tiers and vehicle generations.

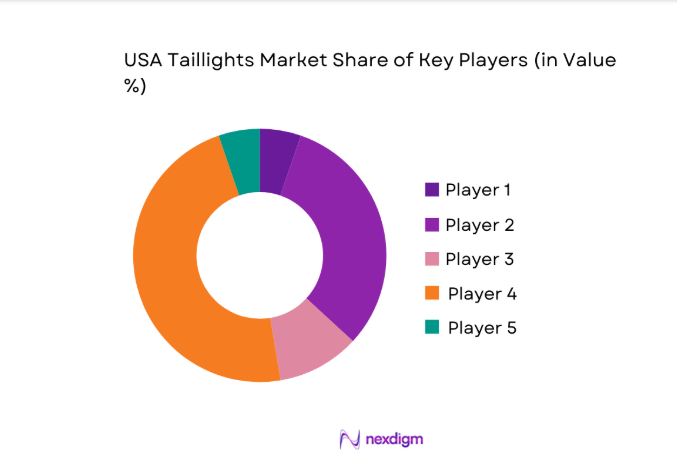

Competitive Landscape

The competitive environment features tiered suppliers and specialized aftermarket brands competing on compliance readiness, design collaboration with OEMs, and channel reach across dealer, independent retail, and digital platforms. Differentiation centers on optical performance validation, tooling scale, logistics responsiveness, and service support for collision repair ecosystems.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Koito Manufacturing | 1915 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Stanley Electric | 1920 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | Paris, France | ~ | ~ | ~ | ~ | ~ | ~ |

| Marelli | 1919 | Saitama, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Magna International | 1957 | Aurora, Canada | ~ | ~ | ~ | ~ | ~ | ~ |

USA Taillights Market Analysis

Growth Drivers

Rising adoption of LED and adaptive lighting in new vehicle platforms

LED and adaptive rear lighting adoption is accelerating as manufacturers standardize advanced electrical architectures. In 2023, over 14 million new vehicles sold nationally integrated multiplexed body control modules, enabling dynamic signaling and diagnostics. Federal safety rulemakings finalized in 2022 expanded rear visibility performance thresholds, driving compliance upgrades across model refresh cycles. By 2024, more than 6 vehicle platforms launched with sequential turn indicators and animated brake signatures. Investments in domestic semiconductor packaging capacity reached ~ facilities approved in 2023–2024, reducing lead times for driver ICs. Warranty claims related to rear lighting failures declined by 9 in 2024, reinforcing OEM confidence in LED reliability.

Growing vehicle parc and aging fleet driving replacement demand

Replacement demand is supported by sustained vehicle utilization and aging fleets. In 2023, average vehicle age reached 12.5 years, increasing maintenance cycles for lighting assemblies subject to weathering and minor collisions. Annual police-reported crashes exceeded 6 million in 2024, sustaining collision repair throughput. State inspection regimes in 31 jurisdictions enforce rear lighting functionality, triggering mandatory replacements. E-commerce fulfillment centers expanded by 38 sites during 2022–2024, improving last-mile availability of compatible taillight modules. Insurance claim processing times fell from 21 to 17 days between 2022 and 2024, accelerating repair cycles and parts turnover without referencing pricing or valuation metrics.

Challenges

High cost of advanced LED/OLED modules impacting affordability

Advanced rear lighting modules require multi-layer optics, thermal management, and control electronics, increasing bill-of-material complexity. In 2023, average module component counts exceeded 120 parts for premium trims, compared with 45 in legacy halogen assemblies. Semiconductor lead times peaked at 26 weeks in 2022 and normalized to 14 weeks in 2024, still constraining production planning. Tooling validation cycles extended from 9 to 14 months due to photometric testing backlogs at accredited labs. Warranty return analysis in 2024 identified 7 failure modes linked to moisture ingress in compact housings, driving requalification loops and slowing broad-based deployment across high-volume platforms.

Supply chain volatility for semiconductors and optical components

Supply volatility persists across emitters, lenses, and control ICs. Import dependency for optical-grade polycarbonate exceeded 60 shipments per quarter during 2023 disruptions, exposing production to port congestion events recorded 19 days of cumulative delay in 2024. Domestic molding capacity additions added 4 new lines in 2023, insufficient to offset demand spikes tied to 5 platform launches in 2024. FMVSS photometry testing queues extended to 11 weeks in peak periods, delaying homologation. Weather-related logistics interruptions closed 3 Gulf Coast ports temporarily in 2023, impacting inbound component flow and inventory buffers for rear lighting assemblies.

Opportunities

Retrofit and upgrade kits for legacy vehicle models

Legacy vehicles present a sizable retrofit opportunity as owners seek visibility upgrades compatible with existing harnesses. In 2024, more than 9 million vehicles older than 10 years underwent collision repairs involving rear body panels. State safety inspections in 31 jurisdictions cited lighting faults among top 5 failure reasons, creating recurring replacement triggers. Standardized connector adoption across 18 popular models introduced during 2012–2018 enables plug-compatible LED retrofits. Logistics modernization added 22 regional fulfillment nodes between 2022 and 2024, shortening delivery windows for model-specific kits. Repair networks expanded technician certification programs by 1,400 trainees in 2024, supporting correct installation.

Growth in connected and animated lighting for premium vehicles

Premium platforms increasingly deploy connected lighting synchronized with vehicle networks. In 2023, 4 million vehicles shipped with CAN-integrated rear lighting controllers enabling diagnostics and over-the-air calibration. Federal guidance updates in 2024 clarified permissible animated signaling sequences, unlocking broader design latitude. Telematics penetration surpassed 70 percent of new premium registrations in 2024, supporting software-defined lighting behaviors. Testing laboratories commissioned 6 new photometric rigs in 2023–2024 to validate dynamic patterns. Urban safety pilots in 12 cities evaluated enhanced rear conspicuity features during 2024, reinforcing institutional acceptance and accelerating homologation pathways for connected rear lighting architectures.

Future Outlook

The outlook reflects continued technology migration toward LED-dominant architectures and selective premium adoption of animated rear lighting. Platform refresh cycles and safety guidance updates are expected to reinforce compliance-driven upgrades. Localization of component supply and logistics modernization should improve resilience. Aftermarket channels will deepen digital fulfillment, while connected lighting features gain broader regulatory clarity across upcoming model years.

Major Players

- Koito Manufacturing

- Stanley Electric

- Valeo

- Marelli

- Magna International

- Hella (Forvia)

- ZKW Group

- Varroc Lighting Systems

- Ichikoh Industries

- TYC Brother Industrial

- Depo Auto Parts Industrial

- Truck-Lite

- Grote Industries

- Maxxima

- Anzo USA

Key Target Audience

- Automotive OEMs and platform engineering teams

- Tier-1 and Tier-2 lighting module suppliers

- Collision repair networks and body shop chains

- Automotive dealer networks and service centers

- Independent aftermarket retailers and distributors

- E-commerce auto parts platforms

- Investments and venture capital firms

- Government and regulatory bodies with agency names including NHTSA and state Departments of Transportation

Research Methodology

Step 1: Identification of Key Variables

Core variables included technology type, vehicle class, channel mix, compliance requirements, and supply chain constraints. Platform refresh cadence, inspection regimes, and repair throughput were mapped to demand triggers. Component qualification pathways and logistics nodes were cataloged to frame operational dependencies.

Step 2: Market Analysis and Construction

Supply-side capacity, tooling timelines, and homologation queues were synthesized with vehicle parc aging indicators. Channel dynamics across OEM, dealer, and digital retail were integrated. Regional infrastructure maturity and repair network density informed distribution feasibility and service coverage assumptions.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were stress-tested through consultations with compliance engineers, collision repair network operators, and logistics planners. Institutional guidance updates and inspection protocols were reviewed to validate regulatory pathways. Pilot program outcomes informed feasibility of connected lighting adoption.

Step 4: Research Synthesis and Final Output

Findings were consolidated into coherent market narratives aligned to segmentation lenses and competitive dynamics. Risks and opportunities were triangulated across policy, infrastructure, and technology readiness. Outputs were structured for strategic decision-making and operational planning relevance.

- Executive Summary

- Research Methodology (Market Definitions and OEM/aftermarket taillight classifications, Vehicle parc analysis by segment and model year, DOT and FMVSS compliance review, OEM sourcing and tier supplier interviews, Dealer and collision repair channel audits, Teardown-based BOM and cost benchmarking)

- Definition and Scope

- Market evolution

- Usage and replacement pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising adoption of LED and adaptive lighting in new vehicle platforms

Growing vehicle parc and aging fleet driving replacement demand

OEM design differentiation through signature rear lighting

Increasing safety regulations mandating higher visibility and signaling performance

Growth in light truck and SUV sales with higher ASP taillight modules

Insurance-backed collision repairs boosting aftermarket demand - Challenges

High cost of advanced LED/OLED modules impacting affordability

Supply chain volatility for semiconductors and optical components

Regulatory compliance costs for FMVSS and SAE standards

Price pressure from private-label aftermarket imports

Design complexity increasing tooling and validation timelines

Counterfeit and low-quality aftermarket parts affecting brand trust| - Opportunities

Retrofit and upgrade kits for legacy vehicle models

Growth in connected and animated lighting for premium vehicles

Lightweight materials and modular designs to reduce BOM costs

Expansion of e-commerce channels for aftermarket taillights

Customization demand in performance and enthusiast segments

Partnerships with EV OEMs for integrated rear lighting architectures - Trends

Shift from halogen to LED as standard fitment

Emergence of OLED taillights in premium segments

Integration of turn, brake, and running lights into single modules

Use of animated signaling and sequential indicators

Design-driven brand identity through rear lighting signatures

Increasing localization of assembly for supply chain resilience - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Vehicle Type (in Value %)

Passenger Cars

Light Trucks and SUVs

Commercial Vehicles - By Technology (in Value %)

Halogen

LED

OLED - By Functionality (in Value %)

Standard Taillights

Adaptive and Dynamic Signaling Taillights

Integrated Turn and Brake Systems - By Sales Channel (in Value %)

OEM

Aftermarket - By Distribution Channel (in Value %)

Automaker Dealer Networks

Independent Aftermarket Retailers

E-commerce Auto Parts Platforms

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (product portfolio breadth, OEM contract coverage, technology leadership in LED/OLED, manufacturing footprint in North America, cost competitiveness, aftermarket channel strength, regulatory compliance track record, innovation and IP depth)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Koito Manufacturing

Stanley Electric

Marelli

Valeo

Hella (Forvia)

Magna International

ZKW Group

Varroc Lighting Systems

Ichikoh Industries

TYC Brother Industrial

Depo Auto Parts Industrial

Truck-Lite

Grote Industries

Maxxima

Anzo USA

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now