Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Thermal Management Systems market is valued at approximately USD ~ billion based on a recent historical assessment, supported by data from the U.S. Energy Information Administration and Department of Energy industrial efficiency statistics. Growth is driven by expanding electric vehicle production, large-scale data center construction, aerospace electrification programs, and increasing demand for advanced cooling in high-performance electronics. Rising investments in battery manufacturing and semiconductor fabrication facilities further stimulate system integration across automotive and industrial sectors.

The United States dominates the regional landscape, with strong activity concentrated in states such as California, Texas, Michigan, and Arizona due to automotive manufacturing hubs, semiconductor fabrication plants, and hyperscale data center expansion. Major metropolitan clusters including Silicon Valley, Detroit, Dallas–Fort Worth, and Phoenix benefit from advanced R&D ecosystems and infrastructure availability. Federal incentives supporting clean energy manufacturing and domestic chip production strengthen local supply chains and promote large-scale adoption of advanced thermal technologies.

Market Segmentation

By Product Type

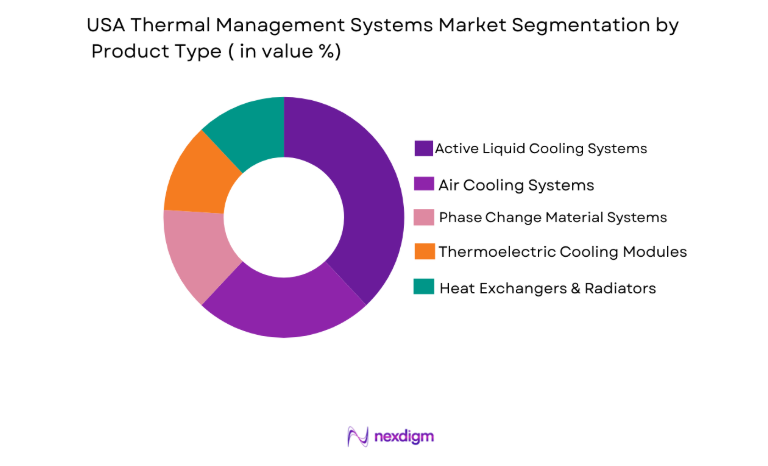

USA Thermal Management Systems market is segmented by product type into Active Liquid Cooling Systems, Air Cooling Systems, Phase Change Material Systems, Thermoelectric Cooling Modules, and Heat Exchangers & Radiators. Recently, Active Liquid Cooling Systems have a dominant market share due to rising adoption in electric vehicles and hyperscale data centers where high heat density requires efficient thermal dissipation. Increased deployment of battery packs and power electronics with higher energy density demands advanced liquid circulation systems. Automotive OEMs prioritize battery safety and performance longevity, driving large-scale procurement. Rapid AI data center expansion also supports large cooling infrastructure installations.

By Platform Type

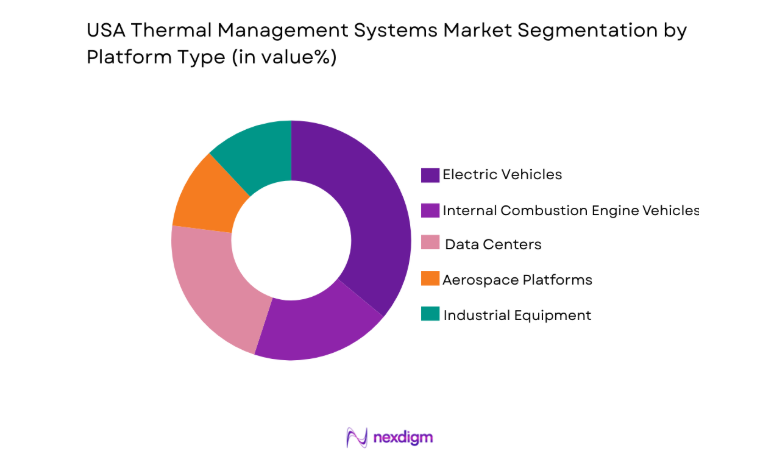

USA Thermal Management Systems market is segmented by platform type into Electric Vehicles, Internal Combustion Engine Vehicles, Data Centers, Aerospace Platforms, and Industrial Equipment. Recently, Electric Vehicles have a dominant market share due to large-scale domestic battery manufacturing, federal clean energy incentives, and rapid consumer adoption of electrified mobility solutions. High-capacity battery packs and power electronics require integrated liquid cooling architectures to ensure thermal stability and safety compliance. Gigafactory expansion across multiple states further strengthens procurement volumes for advanced thermal modules.

Competitive Landscape

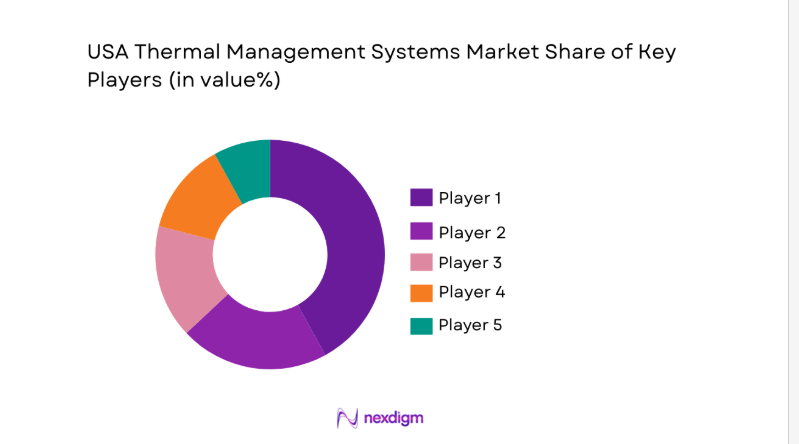

The USA Thermal Management Systems market exhibits moderate consolidation, with established automotive component suppliers and diversified engineering firms controlling a significant portion of revenue. Leading companies focus on vertical integration, R&D investments, and strategic partnerships with EV manufacturers and data center operators. Technological differentiation through advanced materials and liquid cooling innovations influences competitive positioning.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Thermal Efficiency Rating |

| Modine Manufacturing Company | 1916 | USA | ~ | ~ | ~ | ~ | ~ |

| Gentherm Incorporated | 1991 | USA | ~ | ~ | ~ | ~ | ~ |

| Dana Incorporated | 1904 | USA | ~ | ~ | ~ | ~ | ~ |

| Parker Hannifin Corporation | 1917 | USA | ~ | ~ | ~ | ~ | ~ |

| Vertiv Holdings Co | 2016 | USA | ~ | ~ | ~ | ~ | ~ |

USA Thermal Management Systems Market Analysis

Growth Drivers

Electric Vehicle Battery Thermal Regulation Expansion

Rapid electrification of transportation across the United States has significantly increased demand for advanced battery thermal regulation systems, particularly as domestic gigafactories scale production capacity under federal clean energy initiatives. Higher energy density lithium-ion battery packs generate substantial heat loads that require precise thermal control to maintain safety, durability, and performance stability under varying operating conditions. Automotive manufacturers are integrating liquid cooling architectures into battery modules to mitigate thermal runaway risks and enhance fast-charging efficiency. As electric vehicle adoption accelerates, OEMs are prioritizing advanced coolant circulation systems, thermal interface materials, and integrated battery management units that monitor temperature in real time. Federal incentives promoting domestic EV assembly and battery manufacturing are expanding local supply chains, driving procurement of sophisticated cooling modules. Additionally, increasing consumer expectations for longer driving ranges and rapid charging capabilities necessitate improved heat dissipation technologies. Advanced cooling supports battery longevity, thereby reducing warranty costs and enhancing overall vehicle reliability. This systemic shift toward electrified mobility platforms is reinforcing capital investments in thermal management research and manufacturing infrastructure across the automotive sector.

Hyperscale Data Center Infrastructure Growth

The rapid expansion of hyperscale data centers across the United States is driving sustained demand for high-capacity thermal management systems designed to manage intense heat loads from AI processors and high-performance computing clusters. Advanced semiconductor chips deployed in artificial intelligence and cloud computing applications generate concentrated thermal output, necessitating liquid immersion cooling and microchannel heat exchanger technologies. Technology companies are investing heavily in large-scale facilities to support digital transformation, edge computing, and enterprise cloud adoption. Efficient thermal management reduces operational downtime and enhances energy efficiency, directly influencing total cost of ownership for data center operators. Federal semiconductor manufacturing initiatives are further expanding fabrication facilities, which also require precision temperature control systems for cleanroom environments. The integration of renewable energy into data center operations increases the importance of optimized cooling efficiency to maintain sustainability targets. As digital workloads grow in complexity and scale, cooling infrastructure is evolving from traditional air systems toward advanced liquid-based solutions. Continuous technological innovation in server architecture and chip density ensures that thermal management remains a critical enabler of reliable digital infrastructure performance.

Market Challenges

Volatility in Raw Material and Component Supply Chains

The USA Thermal Management Systems market faces persistent challenges related to fluctuating prices and availability of essential raw materials such as copper, aluminum, specialty alloys, and semiconductor-grade components. Global geopolitical tensions and trade disruptions affect supply continuity for critical inputs required in heat exchangers, cooling plates, and thermal interface materials. Manufacturers must manage procurement risks while maintaining cost competitiveness, which can strain margins during periods of commodity price escalation. Advanced cooling systems often rely on precision-engineered components that require specialized fabrication processes, increasing dependency on limited supplier networks. Supply bottlenecks can delay automotive production schedules and large-scale data center installations. Additionally, compliance with domestic sourcing requirements under federal manufacturing policies may restrict access to lower-cost imported materials. These constraints complicate long-term capacity planning for OEMs and system integrators. Sustained volatility increases uncertainty in capital investment decisions and contract negotiations within the value chain.

Integration Complexity in High-Density Electronics Platforms

As electronic devices, electric vehicles, and data center processors become more compact and powerful, integrating effective thermal management systems into constrained design architectures presents significant engineering challenges. Modern battery packs and semiconductor modules operate at high power densities that demand precise and uniform temperature distribution across components. Designing cooling channels, microstructures, and thermal interfaces within limited spatial footprints requires advanced modeling and simulation capabilities. Improper integration can lead to hotspots, reduced performance efficiency, and potential safety hazards, especially in electric mobility applications. OEMs must balance weight, cost, and cooling capacity without compromising product performance. Regulatory standards for safety and environmental compliance add further design constraints. The need for customized cooling solutions for different platforms increases development timelines and R&D expenditure. These complexities create technical barriers that can slow product commercialization and adoption.

Opportunities

Liquid Immersion Cooling Adoption in AI Infrastructure

The rapid expansion of artificial intelligence processing workloads presents a substantial opportunity for liquid immersion cooling technologies within hyperscale and enterprise data centers across the United States. Immersion systems provide superior heat transfer efficiency compared to traditional air-based methods, enabling higher rack densities and reduced energy consumption. As AI accelerators and graphic processing units generate extreme thermal loads, facility operators seek solutions that minimize operational costs while maintaining performance stability. Federal support for domestic semiconductor manufacturing strengthens the ecosystem for advanced cooling integration within fabrication facilities. Sustainability commitments among technology corporations further incentivize adoption of energy-efficient thermal systems. Manufacturers capable of delivering modular, scalable immersion platforms can secure long-term supply contracts. Integration of monitoring sensors and predictive analytics enhances system reliability and creates additional value propositions. This technological shift is expected to redefine cooling architecture standards across high-performance computing environments.

Thermal Management Integration in Renewable Energy Storage Systems

The accelerating deployment of grid-scale battery energy storage systems in the United States creates new demand for specialized thermal management solutions that ensure safe and stable operation under variable load conditions. Renewable energy expansion, particularly solar and wind installations, requires large lithium-ion battery arrays to stabilize power supply and manage intermittency. These storage systems generate heat during charge and discharge cycles, necessitating efficient cooling strategies to prevent degradation and extend service life. Federal infrastructure funding programs encourage domestic manufacturing of energy storage units, increasing procurement of advanced cooling assemblies. Integration of smart thermal monitoring technologies supports predictive maintenance and operational safety. Growing investments in microgrids and distributed energy systems further broaden application scope. Suppliers that develop scalable, cost-effective cooling modules tailored for utility-scale batteries can capture emerging market demand. The intersection of clean energy policy and electrification trends positions thermal management providers for sustained expansion.

Future Outlook

The USA Thermal Management Systems market is expected to experience sustained growth over the next five years, supported by electric mobility expansion, semiconductor manufacturing investments, and hyperscale data center construction. Technological advancements in liquid cooling, microchannel heat exchangers, and smart thermal sensors will redefine efficiency benchmarks. Regulatory emphasis on energy efficiency and domestic manufacturing will further strengthen local supply chains. Demand-side factors including AI infrastructure scaling and renewable energy storage integration will reinforce long-term market momentum.

Major Players

- Modine Manufacturing Company

- Gentherm Incorporated

- Dana Incorporated

- Parker Hannifin Corporation

- Vertiv Holdings Co

- BorgWarner Inc

- Hanon Systems • MAHLE GmbH

- Denso Corporation

- Valeo SA

- Honeywell International Inc

- Johnson Controls International

- Boyd Corporation

- Aavid Thermalloy LLC

- Thermal Management Solutions Group

Key Target Audience

- Automotive manufacturers

- Aerospace and defense contractors

- Data center operators

- Industrial manufacturing companies

- Investments and venture capitalist firms

- Government and regulatory bodies

- Semiconductor manufacturers

- Renewable energy storage developers

Research methodology

Step 1: Identification of Key Variables

Critical demand drivers, regulatory policies, technology adoption rates, and capital expenditure patterns were identified to establish foundational market parameters.

Step 2: Market Analysis and Construction

Quantitative and qualitative data were synthesized from government databases, industry reports, and corporate disclosures to construct market size and segmentation frameworks.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts, engineers, and supply chain specialists were consulted to validate assumptions and refine performance benchmarks across application segments.

Step 4: Research Synthesis and Final Output

Validated insights were consolidated into structured analysis models, ensuring accuracy, logical consistency, and comprehensive coverage of competitive dynamics.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising electric vehicle production and battery thermal regulation requirements

Expansion of hyperscale data centers across major US states

Increased adoption of high performance computing infrastructure

Growth in aerospace electrification initiatives

Stringent energy efficiency standards in industrial operations - Market Challenges

High initial capital investment for advanced cooling systems

Complex integration with next generation battery architectures

Volatility in raw material pricing for copper and specialty alloys

Thermal design constraints in compact electronic devices

Supply chain disruptions affecting semiconductor grade materials - Market Opportunities

Development of liquid cooling solutions for AI driven data centers

Expansion of thermal management in renewable energy storage systems

Integration of smart sensors for predictive thermal monitoring - Trends

Shift toward liquid immersion cooling in large data centers

Growing use of advanced phase change materials in EV batteries

Miniaturization of thermal components for compact electronics

Adoption of sustainable and recyclable thermal materials

Integration of AI enabled thermal control algorithms - Government Regulations & Defense Policy

US Department of Energy efficiency standards for industrial systems

Environmental Protection Agency regulations on refrigerants

Defense electrification initiatives under federal modernization programs - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Active Liquid Cooling Systems

Air Cooling Systems

Phase Change Material Based Systems

Thermoelectric Cooling Modules

Heat Exchanger and Radiator System - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Industrial Equipment

Data Centers and IT Infrastructure - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Retrofits

Modular Add On Units

Embedded PCB Cooling Solutions

Battery Pack Integrated Cooling Assemblies - By EndUser Segment (In Value%)

Automotive Manufacturers

Aerospace and Defense Contractors

Data Center Operators

Industrial Manufacturing Facilities

Consumer Electronics Manufacturers - By Procurement Channel (In Value%)

Direct OEM Contracts

Tier 1 Supplier Agreements

Government Tenders

Distributor and Channel Sales

Online B2B Procurement Platforms - By Material / Technology (in Value %)

Aluminum Based Heat Sinks

Copper Based Cooling Components

Graphene Enhanced Thermal Materials

Advanced Thermal Interface Materials

Microchannel Cooling Technology

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (System Efficiency, Cooling Capacity, Integration Flexibility, Material Innovation, Cost Structure)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Modine Manufacturing Company

Gentherm Incorporated

Dana Incorporated

BorgWarner Inc

Hanon Systems

MAHLE GmbH

Denso Corporation

Valeo SA

Parker Hannifin Corporation

Honeywell International Inc

Johnson Controls International

Vertiv Holdings Co

Boyd Corporation

Aavid Thermalloy LLC

Thermal Management Solutions Group

- Automotive OEMs prioritize battery safety and performance optimization

- Data center operators demand scalable high density cooling infrastructure

- Aerospace manufacturers focus on lightweight and efficient thermal assemblies

- Industrial facilities seek energy efficient process cooling solutions

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now