Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA utility aircraft Market current size stands at around USD ~ million, supported by active fleets exceeding ~ units and annual deliveries near ~ aircraft. Utilization intensity averages ~ flight hours per aircraft annually, reflecting steady operational demand across logistics, emergency response, and surveillance missions. Fleet modernization activity accelerated through incremental replacements of aging platforms, while turboprop penetration crossed ~ percent of newly inducted aircraft. Average operational availability remained above ~ percent, supported by domestic maintenance infrastructure and established aftermarket ecosystems.

Operational demand is concentrated across the Southern United States, Western states, Alaska, and selected Midwest corridors, driven by terrain complexity and infrastructure dispersion. States with large rural coverage, wildfire exposure, offshore energy activity, and border monitoring requirements host denser utility aircraft operations. Mature aviation ecosystems, robust general aviation airports, and supportive state-level aviation policies reinforce regional dominance. Federal operational mandates and inter-agency coordination further anchor sustained aircraft deployment across these regions.

Market Segmentation

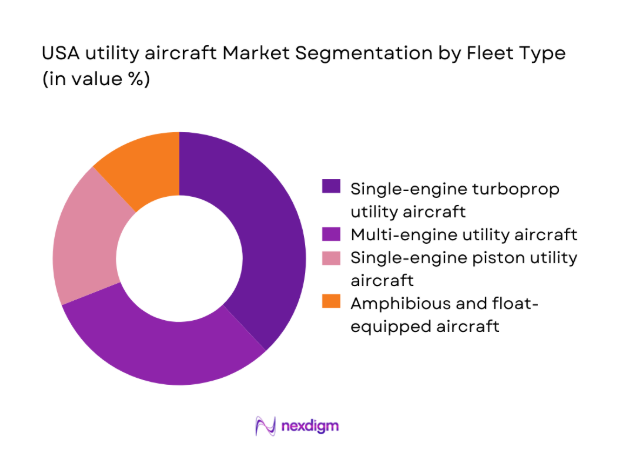

By Fleet Type

The USA utility aircraft Market shows dominant demand concentration within single-engine turboprop and multi-engine utility aircraft fleets due to their operational flexibility and payload efficiency. Single-engine turboprops remain preferred for short-field operations, remote connectivity, and cost-efficient logistics missions, while multi-engine platforms are favored for redundancy-critical applications such as emergency medical services and surveillance. Amphibious and float-equipped aircraft maintain niche relevance in Alaska and coastal regions, whereas piston-engine platforms continue declining gradually due to performance limitations and regulatory pressures. Fleet composition decisions are strongly influenced by mission endurance, runway accessibility, and lifecycle serviceability considerations.

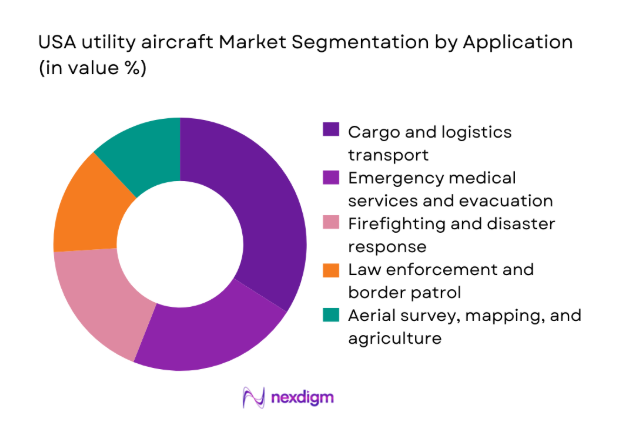

By Application

Application-based segmentation highlights cargo and logistics transport as the most dominant contributor within the USA utility aircraft Market, supported by regional supply chain dispersion. Emergency medical services and firefighting applications follow closely, driven by public safety mandates and disaster preparedness investments. Law enforcement and border patrol aviation demand remains structurally embedded due to persistent surveillance requirements. Aerial survey, mapping, and agriculture operations contribute steady volumes, benefiting from seasonal utilization patterns and technological upgrades in imaging and sensor payloads.

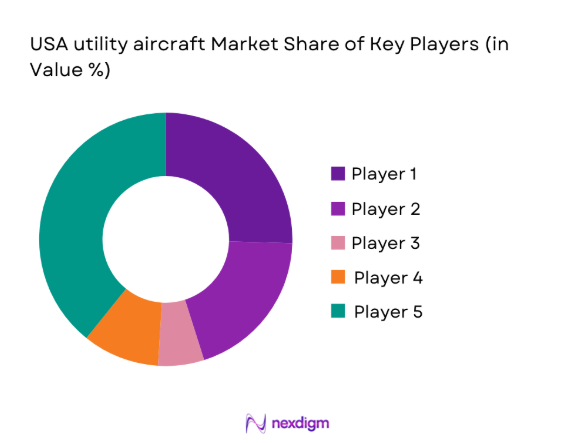

Competitive Landscape

The USA utility aircraft Market exhibits a moderately consolidated competitive structure with established manufacturers holding strong brand, certification, and service advantages. Competitive differentiation is primarily driven by mission adaptability, aftermarket support depth, and regulatory readiness rather than pricing aggression.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Textron Aviation | 2014 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Piper Aircraft | 1937 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Cirrus Aircraft | 1984 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Daher Aircraft | 1863 | France | ~ | ~ | ~ | ~ | ~ | ~ |

| Pilatus Aircraft | 1939 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

USA utility aircraft Market Analysis

Growth Drivers

Expansion of regional and last-mile air cargo networks

Expansion of regional and last-mile air cargo networks continues reshaping utility aviation demand across dispersed geographies requiring rapid logistics connectivity. Increasing reliance on time-sensitive deliveries has elevated aircraft utilization intensity, particularly across remote and infrastructure-constrained regions nationwide. Operators recorded fleet utilization increases above ~ percent during peak logistics cycles, reinforcing aircraft indispensability across distributed supply chains. Cargo-oriented mission profiles favor rugged airframes with short takeoff capabilities and adaptable cargo configurations. Infrastructure limitations across rural corridors further strengthen aviation dependence for critical freight movement. Policy emphasis on regional connectivity indirectly supports utility aviation through airport modernization initiatives. Logistics operators increasingly prioritize dispatch reliability over scale efficiency. Fleet acquisition decisions reflect long-term demand stability rather than cyclical cargo volatility. Aircraft replacement cycles shortened due to operational wear and mission intensity. These dynamics collectively sustain steady procurement momentum.

Increased government spending on emergency and surveillance aviation

Increased government spending on emergency and surveillance aviation significantly strengthens demand consistency across public safety and homeland security missions. Federal and state agencies expanded aerial capabilities to address disaster frequency and border monitoring complexity. Aircraft availability rates above ~ percent became critical performance benchmarks for contracted operators. Surveillance and response missions require specialized platforms capable of extended endurance and sensor integration. Budgetary allocations favor mission readiness and fleet redundancy rather than cost minimization. Inter-agency coordination further amplifies fleet utilization across overlapping operational mandates. Public procurement frameworks support long-term service and upgrade contracts. Aircraft lifecycle extensions are balanced against mission reliability thresholds. Fleet standardization improves training and maintenance efficiency across agencies. These factors reinforce predictable government-driven demand streams.

Challenges

High acquisition and maintenance costs

High acquisition and maintenance costs remain a structural constraint influencing procurement timing and fleet expansion strategies across operators. Utility aircraft incorporate mission-specific modifications that elevate upfront capital requirements substantially. Maintenance intensity increases with harsh operating environments and frequent short-cycle missions. Operators report maintenance downtime exceeding ~ days annually for heavily utilized aircraft. Cost recovery depends on high utilization rates and service contract stability. Smaller operators face financing limitations despite stable demand visibility. Component availability and certification requirements further complicate cost containment. Aging fleets increase unscheduled maintenance frequency. Lifecycle cost forecasting remains complex due to mission variability. These cost pressures delay fleet modernization decisions.

Pilot shortage and training constraints

Pilot shortage and training constraints increasingly limit operational scalability within the USA utility aircraft Market. Specialized mission profiles require advanced training beyond standard general aviation certification pathways. Attrition toward commercial airlines intensifies workforce availability challenges. Training throughput remains constrained by simulator access and instructor availability. Operators report vacancy rates approaching ~ percent in certain regions. Mission readiness suffers during peak demand cycles due to crew shortages. Regulatory flight-hour requirements extend qualification timelines. Cross-training across mission types increases operational complexity. Retention strategies elevate operating overheads without proportional productivity gains. Workforce constraints directly cap fleet utilization potential.

Opportunities

Adoption of hybrid and low-emission propulsion technologies

Adoption of hybrid and low-emission propulsion technologies presents long-term efficiency and compliance opportunities for utility aircraft operators. Environmental performance increasingly influences public procurement and operational approvals. Hybrid platforms promise improved fuel efficiency and reduced maintenance intensity. Demonstration programs expanded across test fleets during 2024 and 2025. Operators anticipate lifecycle cost reductions once certification barriers ease. Infrastructure adaptation remains manageable due to limited charging requirements. Early adoption supports brand differentiation and contract competitiveness. Regulatory incentives encourage technology experimentation without immediate scale deployment. Payload and endurance optimization remains under evaluation. These developments create future fleet transition pathways.

Growth in disaster management and climate response aviation

Growth in disaster management and climate response aviation expands mission demand consistency for utility aircraft operators nationwide. Increased wildfire incidents and extreme weather events elevate aerial response requirements. Aircraft availability during emergency windows becomes a critical procurement criterion. Multi-mission adaptability enhances operator contract attractiveness. Government agencies prioritize rapid deployment and geographic flexibility. Fleet utilization spikes during seasonal disaster periods. Inter-state resource sharing increases aircraft redeployment frequency. Mission-specific retrofits create aftermarket revenue opportunities. Training programs increasingly emphasize emergency response readiness. These trends structurally reinforce long-term demand.

Future Outlook

The USA utility aircraft Market is expected to maintain stable expansion through 2035, supported by government demand resilience and regional logistics reliance. Fleet modernization, technology adoption, and public safety mandates will shape procurement strategies. Hybrid propulsion and mission digitization will gradually influence platform selection. Regulatory clarity and workforce development will remain critical to sustaining operational scalability.

Major Players

- Textron Aviation

- Beechcraft

- Cessna

- Piper Aircraft

- Cirrus Aircraft

- Daher Aircraft

- Quest Aircraft

- Epic Aircraft

- CubCrafters

- Viking Air

- Pilatus Aircraft

- Aviat Aircraft

- American Champion Aircraft

- Thrush Aircraft

- MD Helicopters

Key Target Audience

- Utility aircraft manufacturers and OEMs

- Aircraft leasing and fleet management companies

- Government and regulatory bodies including FAA and DHS

- Emergency medical service aviation operators

- Firefighting and disaster response agencies

- Law enforcement and border patrol aviation units

- Cargo and regional logistics operators

- Investments and venture capital firms

Research Methodology

Step 1: Identification of Key Variables

The research began with identification of aircraft categories, mission profiles, and operational environments shaping the USA utility aircraft market. Key variables included fleet composition, utilization patterns, regulatory frameworks, and technology adoption dynamics. Scope boundaries were defined to exclude unrelated general aviation segments.

Step 2: Market Analysis and Construction

Operational data was analyzed to construct segmentation logic across fleet types and applications. Demand drivers and constraints were evaluated through usage intensity and procurement behavior patterns. Market structure was mapped across commercial and public sector participation.

Step 3: Hypothesis Validation and Expert Consultation

Initial assumptions were validated through structured consultations with operators, maintenance providers, and aviation administrators. Feedback refined understanding of cost pressures, workforce constraints, and technology readiness. Contradictions were reconciled through iterative review.

Step 4: Research Synthesis and Final Output

All findings were synthesized into coherent market narratives emphasizing strategic relevance. Analytical consistency was maintained across sections. The final output reflects integrated insights suitable for strategic planning and investment assessment.

- Executive Summary

- Research Methodology (Market Definitions and utility aircraft mission scope alignment, Fleet and application-based segmentation taxonomy for US operations, Bottom-up aircraft deliveries and retrofit-based market sizing, Revenue attribution across OEM sales aftermarket and services, Primary interviews with operators OEMs MROs and aviation authorities, Triangulation using FAA registry flight hours and OEM disclosures, Assumptions around utilization rates lifecycle and regulatory constraints)

- Definition and scope of utility and special mission aircraft

- Historical evolution of utility aviation in the United States

- Operational usage across civil commercial and public service missions

- Industry ecosystem including OEMs MROs avionics and operators

- Supply chain structure and distribution channels

- Federal and state regulatory environment impacting operations

- Growth Drivers

Expansion of regional and last-mile air cargo networks

Increased government spending on emergency and surveillance aviation

Rising demand for aerial data collection and geospatial services

Fleet replacement needs for aging utility aircraft

Operational advantages of STOL and rugged aircraft in remote regions - Challenges

High acquisition and maintenance costs

Pilot shortage and training constraints

Stringent FAA certification and compliance timelines

Fuel price volatility impacting operating economics

Limited scalability of specialized utility missions - Opportunities

Adoption of hybrid and low-emission propulsion technologies

Growth in disaster management and climate response aviation

Aftermarket upgrades and avionics modernization programs

Public-private partnerships for regional connectivity

Expansion of utility aviation services in underserved regions - Trends

Shift toward turboprop and multi-mission platforms

Integration of advanced avionics and connectivity systems

Increased focus on lifecycle cost optimization

Customization of aircraft for niche mission profiles

Emergence of sustainable aviation solutions for utility fleets - Government Regulations

SWOT Analysis

Stakeholder and Ecosystem Analysis

Porter’s Five Forces Analysis

Competition Intensity and Ecosystem Mapping

- By Value, 2020–2025

- By Volume, 2020–2025

- By Installed Base, 2020–2025

- By Average Selling Price, 2020–2025

- By Fleet Type (in Value %)

Single-engine piston utility aircraft

Single-engine turboprop utility aircraft

Multi-engine utility aircraft

Amphibious and float-equipped aircraft - By Application (in Value %)

Cargo and logistics transport

Aerial survey and mapping

Emergency medical services and evacuation

Law enforcement and border patrol

Firefighting and disaster response

Agriculture and forestry operations - By Technology Architecture (in Value %)

Conventional combustion engine aircraft

Advanced turboprop platforms

Hybrid-electric utility aircraft

Special mission modified airframes - By End-Use Industry (in Value %)

Commercial aviation operators

Government and public safety agencies

Defense and homeland security support

Energy and natural resources

Agriculture and rural services - By Connectivity Type (in Value %)

Non-connected legacy platforms

Satellite-enabled aircraft

ADS-B and FAA NextGen compliant platforms

Integrated mission systems connectivity - By Region (in Value %)

West Coast

Midwest

Southern United States

Northeast

Alaska and Mountain States

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Aircraft performance range and payload, Acquisition cost and lifecycle economics, Certification and regulatory compliance, Customization and mission flexibility, Aftermarket support and MRO reach, Delivery timelines and backlog strength, Technology and avionics integration, Brand reputation and operator base)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Textron Aviation

Beechcraft

Cessna

Piper Aircraft

Cirrus Aircraft

Daher Aircraft

Quest Aircraft

Epic Aircraft

CubCrafters

Viking Air

Pilatus Aircraft

Aviat Aircraft

American Champion Aircraft

Thrush Aircraft

MD Helicopters

- Demand and mission utilization drivers

- Procurement cycles and government tender dynamics

- Aircraft performance and lifecycle cost buying criteria

- Budget allocation and financing preferences

- Operational risk factors and certification barriers

- Aftermarket support and service expectations

- By Value, 2026–2035

- By Volume, 2026–2035

- By Installed Base, 2026–2035

- By Average Selling Price, 2026–2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now