Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Vehicle Connectivity Solutions market is valued at approximately USD ~ billion based on a recent historical assessment, driven by increasing integration of connected technologies in passenger and commercial vehicles. Growth is fueled by rising adoption of telematics, infotainment systems, and vehicle-to-everything communication platforms, supported by advancements in 5G infrastructure and software-defined vehicle architectures. Automotive OEMs are heavily investing in connectivity solutions to enhance safety, real-time diagnostics, and user experience, strengthening overall market expansion.

The United States remains the dominant region, with cities such as Detroit, San Francisco, and Austin leading due to strong automotive manufacturing, advanced technology ecosystems, and high digital infrastructure penetration. California stands out for its innovation in autonomous and connected vehicle technologies, while Michigan benefits from established automotive OEM presence. Texas is emerging as a connectivity hub due to investments in smart mobility and telecom infrastructure, enabling large-scale deployment of vehicle connectivity solutions.

Market Segmentation

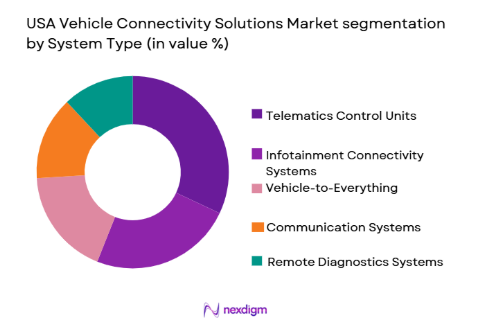

By System Type

USA Vehicle Connectivity Solutions market is segmented by product type into telematics control units, infotainment connectivity systems, vehicle-to-everything communication systems, remote diagnostics systems, and over-the-air update platforms. Recently, telematics control units have a dominant market share due to strong integration across OEM platforms, regulatory mandates for vehicle safety, and widespread adoption in fleet management. These systems enable real-time data exchange, predictive maintenance, and driver behavior monitoring, making them essential for both commercial and passenger vehicles, thereby strengthening their market dominance.

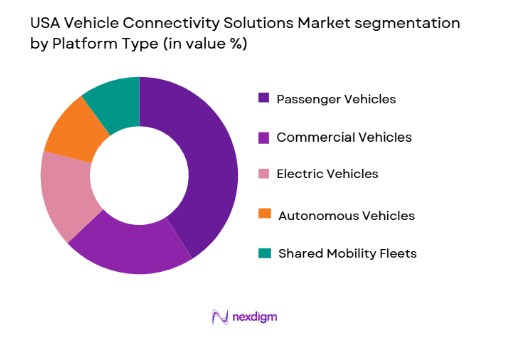

By Platform Type

USA Vehicle Connectivity Solutions market is segmented by product type into passenger vehicles, commercial vehicles, electric vehicles, autonomous vehicles, and shared mobility fleets. Recently, passenger vehicles have a dominant market share due to higher production volumes, increasing consumer demand for advanced infotainment and connectivity features, and rapid integration of smart technologies by OEMs. Growing consumer preference for enhanced driving experience and safety features further strengthens the dominance of passenger vehicle connectivity solutions across urban and suburban mobility landscapes.

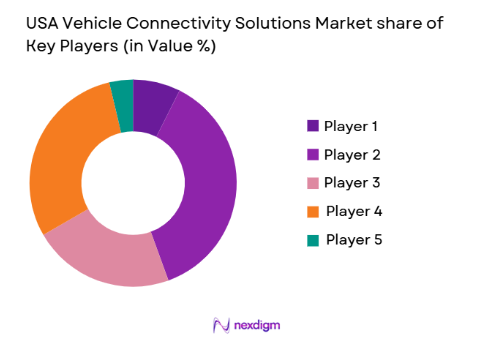

Competitive Landscape

The USA Vehicle Connectivity Solutions market is moderately consolidated, with major players leveraging strong technological capabilities, strategic partnerships, and integrated solutions to strengthen their market positions. Leading companies focus on innovations in 5G connectivity, AI-driven analytics, and cloud-based platforms to enhance vehicle communication ecosystems. Increasing collaboration between telecom providers and automotive OEMs is intensifying competition while accelerating technological advancements and expanding market reach.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Connectivity Capability |

| Harman International | 1980 | USA | ~ | ~ | ~ | ~ | ~ |

| Bosch Mobility Solutions | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Continental AG | 1871 | Germany | ~ | ~ | ~ | ~ | ~ |

| Qualcomm Technologies | 1985 | USA | ~ | ~ | ~ | ~ | ~ |

| Visteon Corporation | 2000 | USA | ~ | ~ | ~ | ~ | ~ |

USA Vehicle Connectivity Solutions Market Analysis

Growth Drivers

Advanced 5G and IoT Infrastructure Integration in Automotive Ecosystems:

The rapid deployment of 5G networks and IoT infrastructure is significantly driving the USA Vehicle Connectivity Solutions market by enabling high-speed data transmission and real-time communication between vehicles and external systems. Automotive manufacturers are increasingly embedding connectivity modules that leverage 5G capabilities to enhance navigation, infotainment, and safety features. This integration allows seamless communication across multiple platforms, including cloud-based services and edge computing systems. The increasing demand for real-time diagnostics and predictive maintenance is further accelerating the adoption of connected technologies. Fleet operators are leveraging these advancements to optimize logistics, reduce downtime, and improve operational efficiency. Additionally, government initiatives supporting smart transportation infrastructure are contributing to the expansion of connectivity solutions. The development of vehicle-to-everything communication systems is enhancing road safety and traffic management. Consumer demand for personalized driving experiences is also encouraging OEMs to adopt advanced connectivity solutions. These combined factors are establishing 5G and IoT integration as a fundamental growth driver in the market.

Rising Demand for Software Defined Vehicles and Connected Services:

The transition toward software defined vehicles is a major growth driver for the USA Vehicle Connectivity Solutions market as automotive systems increasingly rely on software updates and digital services. Manufacturers are integrating advanced connectivity platforms that enable over-the-air updates, enhancing vehicle performance and reducing the need for physical servicing. This shift is enabling continuous improvement of vehicle functionalities, including navigation, infotainment, and safety systems. Consumers are showing growing interest in subscription-based services such as remote diagnostics, navigation upgrades, and entertainment features. The increasing adoption of electric and autonomous vehicles is also contributing to the demand for advanced connectivity solutions. Automotive companies are focusing on building integrated ecosystems that combine hardware and software capabilities. Partnerships between technology firms and automotive OEMs are accelerating innovation in this space. The ability to collect and analyze vehicle data in real time is improving decision-making and operational efficiency. These developments are driving the widespread adoption of connected vehicle technologies across the market.

Market Challenges

Cybersecurity Risks and Data Privacy Concerns in Connected Vehicles:

The increasing connectivity of vehicles exposes them to cybersecurity threats, making data protection a critical challenge in the USA Vehicle Connectivity Solutions market. Connected vehicles generate large volumes of data, including sensitive information related to location, driver behavior, and vehicle performance. This data is vulnerable to cyberattacks, which can compromise safety and privacy. Automotive manufacturers are required to invest heavily in cybersecurity frameworks to protect connected systems. The complexity of integrating secure communication protocols across multiple platforms adds to the challenge. Regulatory requirements for data protection are becoming more stringent, increasing compliance costs for companies. Consumers are also becoming more aware of privacy risks, influencing their purchasing decisions. Ensuring secure over-the-air updates and preventing unauthorized access to vehicle systems remains a key concern. Collaboration between technology providers and automotive companies is necessary to address these issues. Despite advancements, maintaining robust cybersecurity remains a persistent challenge in the market.

High Cost of Integration and Infrastructure Development:

The implementation of advanced vehicle connectivity solutions involves significant costs related to hardware, software, and infrastructure development. Automotive manufacturers must invest in sophisticated communication modules, sensors, and cloud-based platforms to enable seamless connectivity. The cost of integrating these technologies into vehicles is high, particularly for entry-level models. Telecom infrastructure upgrades, including 5G network deployment, further increase overall investment requirements. Smaller manufacturers and suppliers face challenges in adopting these technologies due to limited financial resources. Additionally, the complexity of integrating multiple systems across different platforms increases development costs. Maintenance and continuous software updates add to the operational expenses. The need for skilled workforce and technical expertise further raises costs. These financial barriers can limit market penetration and slow down the adoption of connectivity solutions, especially among cost-sensitive segments.

Opportunities

Expansion of Smart City and Vehicle-to-Everything Communication Ecosystems:

The development of smart cities presents significant opportunities for the USA Vehicle Connectivity Solutions market by enabling integration of connected vehicles with urban infrastructure. Governments are investing in intelligent transportation systems that rely on vehicle-to-everything communication technologies to improve traffic management and reduce congestion. Connected vehicles can interact with traffic signals, road infrastructure, and other vehicles to enhance safety and efficiency. This integration supports real-time data exchange, enabling better decision-making and improved mobility services. Automotive companies are exploring partnerships with city planners and technology providers to develop advanced connectivity solutions. The increasing adoption of autonomous vehicles further enhances the need for robust communication systems. Smart parking solutions and intelligent routing systems are also contributing to market growth. These developments are creating new revenue streams for connectivity solution providers. As urbanization continues to increase, the demand for connected mobility solutions is expected to expand significantly.

Growth of Subscription Based Connected Vehicle Services:

The emergence of subscription-based models is creating new growth opportunities in the USA Vehicle Connectivity Solutions market by enabling continuous revenue generation for automotive companies. Consumers are increasingly willing to pay for value-added services such as navigation updates, remote diagnostics, and entertainment features. This shift is encouraging manufacturers to develop integrated digital ecosystems that offer personalized services. The ability to update vehicle functionalities through over-the-air platforms enhances customer satisfaction and retention. Automotive companies are leveraging data analytics to provide tailored services based on user preferences. Partnerships with telecom and technology firms are facilitating the development of scalable subscription platforms. The growing demand for digital services is transforming traditional business models in the automotive industry. This trend is also enabling manufacturers to differentiate their offerings in a competitive market. As connectivity becomes a standard feature, subscription-based services are expected to drive long-term market growth.

Future Outlook

The USA Vehicle Connectivity Solutions market is expected to witness steady expansion driven by advancements in 5G networks, AI-based analytics, and cloud integration. Increasing adoption of software-defined vehicles and connected ecosystems will enhance real-time communication capabilities. Regulatory support for vehicle safety and smart transportation infrastructure will further accelerate growth. Demand from electric and autonomous vehicle segments is anticipated to strengthen the market. Continuous innovation and partnerships between automotive and technology firms will shape future market dynamics.

Major Players

- Harman International

- Bosch Mobility Solutions

- Continental AG

- Qualcomm Technologies

- Visteon Corporation

- Panasonic Automotive Systems

- Valeo Group

- NXP Semiconductors

- Ericsson Automotive

- Cisco Systems Automotive

- Verizon Connect

- AT&T Connected Car

- TomTom Automotive

- Sierra Wireless

- Denso Corporation

Key Target Audience

- Automotive OEMs

- Fleet management companies

- Electric vehicle manufacturers

- Autonomous vehicle developers

- Telecom service providers

- Cloud and data platform providers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables such as connectivity adoption rates, vehicle production, telecom infrastructure, and regulatory frameworks are identified. These variables form the foundation for analyzing market dynamics and technological advancements.

Step 2: Market Analysis and Construction

Extensive secondary and primary research is conducted to assess market trends, segment performance, and competitive landscape. Data is structured into models to estimate market size and segmentation.

Step 3: Hypothesis Validation and Expert Consultation

Findings are validated through industry expert interviews and cross-verification with multiple data sources. Assumptions are refined to ensure accuracy and reliability of insights.

Step 4: Research Synthesis and Final Output

All validated data is synthesized into a structured report highlighting key trends, opportunities, and challenges. Final outputs are aligned with market realities and strategic insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising adoption of connected car ecosystems across passenger and commercial vehicles

Expansion of 5G infrastructure enabling high speed vehicle communication

Increasing demand for real time vehicle diagnostics and predictive maintenance

Growth in electric and autonomous vehicle integration requiring advanced connectivity

Government mandates supporting vehicle safety and telematics integration - Market Challenges

Data privacy and cybersecurity risks associated with connected vehicles

High integration costs for advanced connectivity systems in vehicles

Interoperability challenges across multiple platforms and communication standards

Limited infrastructure readiness in rural and remote regions

Complex regulatory compliance requirements across states and federal agencies - Market Opportunities

Expansion of vehicle to everything communication for smart city integration

Growth in subscription based connected vehicle services

Increasing partnerships between automotive and technology companies - Trends

Integration of AI driven predictive analytics in vehicle connectivity platforms

Shift towards software defined vehicles with continuous updates

Adoption of cloud native architectures for real time data processing

Increased focus on cybersecurity frameworks in automotive systems

Emergence of digital cockpit and immersive infotainment systems - Government Regulations & Defense Policy

Federal mandates on vehicle safety and telematics standards

Data protection regulations governing connected vehicle ecosystems

Incentives for deployment of smart transportation infrastructure - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Telematics Control Units

Infotainment Connectivity Systems

Vehicle-to-Everything Communication Systems

Remote Diagnostics and Monitoring Systems

Over-the-Air Update Platforms - By Platform Type (In Value%)

Passenger Vehicles

Commercial Vehicles

Electric Vehicles

Autonomous Vehicles

Shared Mobility Fleets - By Fitment Type (In Value%)

OEM Integrated Solutions

Aftermarket Plug-in Devices

Embedded Connectivity Modules

Smartphone Integrated Systems

Cloud-linked Hybrid Systems - By EndUser Segment (In Value%)

Automotive OEMs

Fleet Operators

Individual Vehicle Owners

Mobility Service Providers

Insurance and Telematics Firms - By Procurement Channel (In Value%)

Direct OEM Contracts

Technology Vendor Partnerships

Aftermarket Retail Distribution

Online Platform Sales

Fleet Procurement Agreements - By Material / Technology (in Value %)

5G Connectivity Modules

Edge Computing Platforms

AI-enabled Analytics Systems

Cloud-based Data Management Solutions

Cybersecurity and Encryption Technologies

- Market structure and competitive positioning

- Market share snapshot of major players

- CrossComparison Parameters (Product Portfolio, Connectivity Technology, Integration Capability, Pricing Strategy, Geographic Presence, Partnerships, Innovation Pipeline, Data Security Features, Cloud Integration, Customer Base)

- SWOT Analysis of Key Players

- Pricing & Procurement Analysis

- Key Players

Harman International

Bosch Mobility Solutions

Continental AG

Denso Corporation

Qualcomm Technologies

Visteon Corporation

Panasonic Automotive Systems

Valeo Group

NXP Semiconductors

Ericsson Automotive

Cisco Systems Automotive

Verizon Connect

AT&T Connected Car

TomTom Automotive

Sierra Wireless

- Automotive OEMs focusing on integrated connectivity as a core vehicle feature

- Fleet operators leveraging connectivity for operational efficiency and cost reduction

- Mobility service providers adopting real time tracking and user experience enhancements

- Insurance firms utilizing telematics data for usage based insurance models

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now