Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Vehicle Networking Systems market current size stands at around USD ~ million, reflecting sustained demand for in-vehicle communication architectures that connect sensors, ECUs, gateways, and software stacks across multiple domains. The market is shaped by increasing electronic content per vehicle, rising integration of advanced driver assistance functions, and the shift toward zonal and centralized compute architectures. OEM programs and Tier suppliers prioritize robust networking backbones to enable diagnostics, cybersecurity controls, and over-the-air software updates across diverse vehicle platforms nationwide.

Demand concentration is strongest across automotive manufacturing and technology clusters in Michigan, California, Texas, Ohio, and the Southeast, where OEM assembly plants, Tier supplier engineering centers, and software development hubs coexist. These regions benefit from dense logistics corridors, mature testing infrastructure, and proximity to semiconductor design ecosystems. State-level incentives for advanced manufacturing, connected mobility pilots, and cybersecurity compliance readiness further strengthen ecosystem maturity and accelerate adoption across passenger, commercial, and fleet vehicle segments.

Market Segmentation

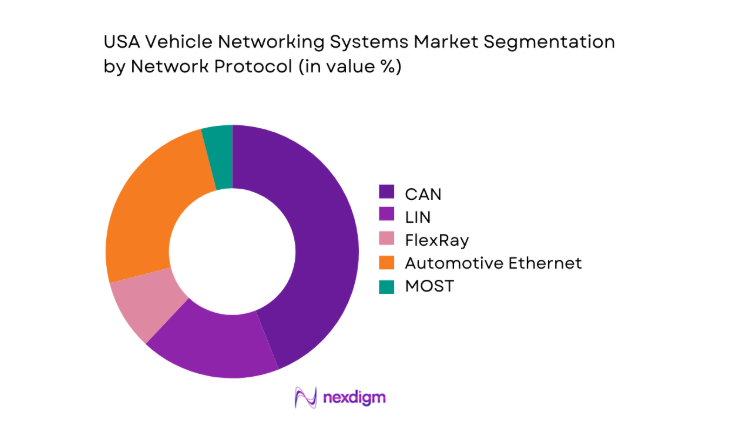

By Network Protocol

Adoption is dominated by legacy protocols transitioning toward high-speed backbones as vehicle architectures evolve. CAN and LIN remain embedded across body electronics and low-speed domains due to reliability and cost efficiency, while FlexRay persists in safety-critical control networks. Automotive Ethernet is rapidly penetrating ADAS, infotainment, and centralized compute backbones, driven by bandwidth needs and software-defined vehicle roadmaps. OEMs increasingly deploy hybrid protocol stacks to manage interoperability across generations of platforms, balancing deterministic control requirements with scalable data transport for sensor fusion, diagnostics, and OTA updates. Standardization initiatives and cybersecurity hardening further shape protocol selection across new model programs.

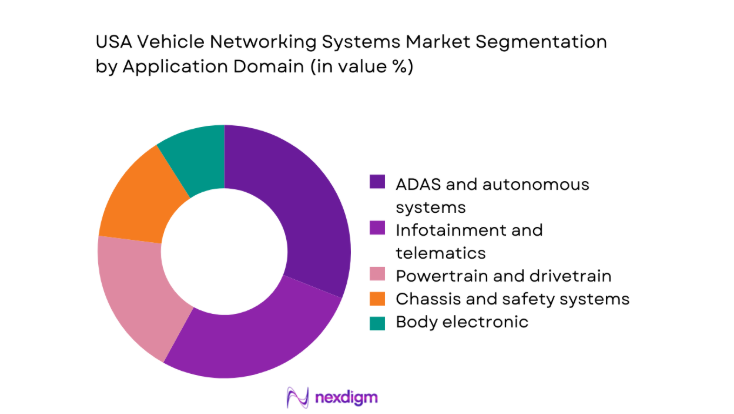

By Application Domain

Network deployment is concentrated in ADAS and infotainment domains, reflecting rising sensor counts, camera integration, and data-heavy user interfaces. Powertrain and chassis networks remain critical for real-time control and safety functions, while body electronics sustain large installed bases across lighting, access, and comfort features. Telematics integration expands across fleet and consumer vehicles to support remote diagnostics, compliance reporting, and OTA updates. OEMs increasingly converge application domains through centralized gateways, enabling cross-domain data sharing, cybersecurity enforcement, and software lifecycle management aligned with software-defined vehicle strategies.

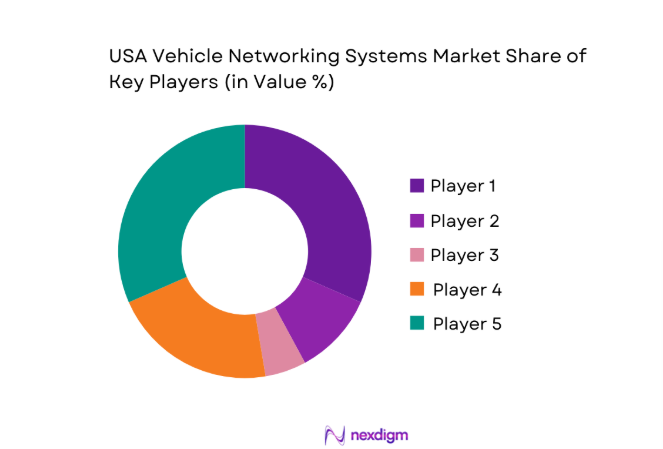

Competitive Landscape

The competitive landscape reflects a mix of semiconductor vendors, automotive electronics specialists, and system integrators supporting OEM networking architectures. Differentiation centers on protocol breadth, automotive Ethernet maturity, cybersecurity readiness, and software toolchain integration to support zonal architectures and OTA operations.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| NXP Semiconductors | 2006 | Netherlands | ~ | ~ | ~ | ~ | ~ | ~ |

| Infineon Technologies | 1999 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

| Texas Instruments | 1930 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Renesas Electronics | 2010 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| STMicroelectronics | 1987 | Switzerland | ~ | ~ | ~ | ~ | ~ | ~ |

USA Vehicle Networking Systems Market Analysis

Growth Drivers

Rising ADAS content and sensor fusion requirements

ADAS deployment accelerated as federal safety guidance expanded lane-keeping, automatic emergency braking, and blind-spot monitoring across new vehicle programs. Camera counts per vehicle increased from 3 in 2022 to 6 in 2024, while radar modules rose from 2 to 4 over the same period. Highway pilot corridors expanded testing mileage from 1200000 to 2100000 route-miles. State transportation agencies increased connected corridor endpoints from 46 to 71. These changes elevated bandwidth and determinism needs across in-vehicle backbones, driving adoption of higher-speed networking and gateway consolidation. OEM validation cycles shortened from 36 to 28 months, intensifying integration demand across ECUs and software stacks nationwide.

Transition toward software-defined vehicles

OEM platform roadmaps prioritized centralized compute and OTA updates, increasing in-vehicle network complexity. Vehicles capable of OTA updates rose from 3800000 units in 2022 to 6200000 units in 2024 across U.S. deliveries. Software update events per vehicle increased from 2 to 6 annually, requiring resilient networking paths and cybersecurity segmentation. Zonal architecture pilots expanded from 4 programs in 2022 to 11 in 2024, reducing wiring mass and enabling scalable feature deployment. Federal cybersecurity guidance prompted compliance audits across 27 state fleets. These shifts elevated demand for deterministic Ethernet, secure gateways, and lifecycle management across vehicle platforms and supplier ecosystems.

Challenges

Complex integration across legacy and new protocols

Mixed protocol stacks persist across body, powertrain, and ADAS domains, complicating interoperability. Vehicles integrating three or more protocols rose from 58 percent of new platforms in 2022 to 71 percent in 2024. Gateway firmware interfaces increased from 12 to 19 per platform, expanding validation scope. Field incidents linked to protocol translation faults grew from 430 to 690 reported cases across fleet service networks. Engineering change requests per program increased from 140 to 210, extending integration timelines. Toolchain fragmentation across 9 major interface standards constrained debugging efficiency and raised system complexity for OEMs and Tier suppliers.

Cybersecurity vulnerabilities across in-vehicle networks

Connected vehicle exposure increased as telematics nodes per vehicle rose from 1 to 3 between 2022 and 2024. Reported vulnerability disclosures affecting in-vehicle networks grew from 38 to 92 advisories across coordinated disclosure programs. Federal agencies expanded penetration testing mandates across 14 to 26 public fleet programs, elevating compliance burdens. Security patch deployment windows narrowed from 120 to 45 days, pressuring OTA reliability. Encryption overhead increased processor utilization by 18 points on legacy ECUs, constraining performance headroom. These factors complicate secure integration while sustaining deterministic latency across safety-critical domains nationwide.

Opportunities

Migration to zonal architectures reducing wiring complexity

Zonal pilots demonstrated wiring length reductions from 3500 to 2100 meters per vehicle, lowering mass and assembly complexity. Assembly time per vehicle declined from 18 to 12 labor-hours in pilot plants during 2023 to 2024. Gateway consolidation reduced ECU counts from 110 to 65 per platform, simplifying diagnostics and service workflows. Warranty claims tied to harness faults decreased from 7.4 to 4.1 incidents per 1000 vehicles in pilot fleets. These operational improvements create incentives for broader rollout across new platforms, supporting scalable networking backbones and standardized interfaces across U.S. manufacturing footprints.

High-speed Ethernet adoption for autonomous compute domains

Compute nodes supporting sensor fusion expanded from 2 to 5 per vehicle between 2022 and 2024 in pilot autonomous stacks. Aggregate data throughput requirements increased from 1.5 to 6.2 gigabits per second across ADAS domains, exceeding legacy bus limits. Test track deployments expanded from 9 to 17 facilities supporting multi-gigabit validation. Development toolchains supporting time-sensitive networking rose from 6 to 14 certified environments. These trends position Ethernet backbones as core enablers for scalable autonomy features, reducing integration friction and enabling future software feature deployment across U.S. vehicle programs.

Future Outlook

The market will continue shifting toward zonal architectures and high-speed backbones as software-defined vehicle strategies mature. Regulatory emphasis on cybersecurity and OTA resilience will shape network design choices. OEM platform consolidation will accelerate standardization, while fleet digitization sustains demand across commercial segments. Supply chain localization and validation capacity will influence deployment cadence through the outlook period.

Major Players

- NXP Semiconductors

- Infineon Technologies

- Texas Instruments

- Renesas Electronics

- STMicroelectronics

- Qualcomm Technologies

- Broadcom

- Marvell Technology

- Analog Devices

- Microchip Technology

- Bosch Mobility

- Continental

- ZF Friedrichshafen

- Aptiv

- Denso

Key Target Audience

- Automotive OEM engineering and platform teams

- Tier 1 automotive electronics suppliers

- Fleet operators and telematics service providers

- Automotive software platform vendors

- Semiconductor and connectivity component manufacturers

- System integrators and vehicle architecture consultants

- Investments and venture capital firms

- Government and regulatory bodies with agency names including NHTSA and DOT

Research Methodology

Step 1: Identification of Key Variables

Key variables included network protocols, ECU and gateway density, zonal architecture adoption, OTA readiness, cybersecurity compliance, and validation cycles across passenger and commercial vehicles. Vehicle program roadmaps and regulatory requirements informed variable prioritization.

Step 2: Market Analysis and Construction

Program-level adoption patterns, platform transitions, and integration complexity were mapped across OEMs and supplier tiers. Architecture shifts and protocol migration pathways were synthesized to construct adoption scenarios and operational constraints.

Step 3: Hypothesis Validation and Expert Consultation

Engineering leads, cybersecurity specialists, and fleet technology managers validated assumptions on bandwidth needs, gateway consolidation, and compliance readiness. Field feedback refined integration risk assessments and deployment feasibility.

Step 4: Research Synthesis and Final Output

Insights were consolidated into a cohesive narrative linking architecture transitions to operational outcomes. The synthesis emphasized interoperability, security, and scalability implications across U.S. vehicle programs.

- Executive Summary

- Research Methodology (Market Definitions and in-vehicle networking architectures, OEM and Tier-1 supplier shipment tracking, Telematics and connected vehicle platform audits, CAN LIN FlexRay Ethernet penetration modeling, Federal safety and cybersecurity regulation mapping, Primary interviews with automotive electronics engineers, Fleet operator and aftermarket installer surveys)

- Definition and Scope

- Market evolution

- Usage pathways across passenger and commercial vehicles

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising ADAS content and sensor fusion requirements

Transition toward software-defined vehicles

Growth of connected car and telematics deployments

Electrification and increasing ECU density

Regulatory push for safety and diagnostics interoperability

OEM demand for zonal and centralized architectures - Challenges

Complex integration across legacy and new protocols

Cybersecurity vulnerabilities across in-vehicle networks

Cost pressures on wiring harness and gateway redesign

Interoperability issues across multi-vendor ECUs

Supply chain disruptions for semiconductors and connectors

Qualification and validation complexity for automotive Ethernet - Opportunities

Migration to zonal architectures reducing wiring complexity

High-speed Ethernet adoption for autonomous compute domains

Over-the-air update enablement via robust networking backbones

Fleet digitization driving demand for telematics gateways

Aftermarket connectivity upgrades for legacy vehicles

Standardization of time-sensitive networking for real-time control - Trends

Shift from CAN/FlexRay to Automotive Ethernet backbones

Adoption of zonal architectures and centralized compute

Integration of TSN for deterministic networking

Increased use of gateway domain controllers

Software-defined networking within vehicles

Enhanced in-vehicle cybersecurity frameworks - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Shipment Volume, 2019–2024

- By Active Systems, 2019–2024

- By Average Selling Price, 2019–2024

- By Network Protocol (in Value %)

CAN

LIN

FlexRay

Automotive Ethernet

MOST - By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Medium and heavy commercial vehicles

Off-highway vehicles - By Application Domain (in Value %)

Powertrain and drivetrain

ADAS and autonomous systems

Infotainment and telematics

Body electronics

Chassis and safety systems - By Component Type (in Value %)

Network controllers and transceivers

ECUs and gateways

Cabling and connectors

Software stacks and middleware - By Sales Channel (in Value %)

OEM integration

Tier-1 supply to OEMs

Aftermarket retrofits

Fleet and telematics service providers

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (protocol portfolio breadth, automotive Ethernet maturity, OEM program wins, ASIL compliance depth, cybersecurity capabilities, manufacturing footprint in the USA, cost competitiveness, software toolchain integration)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

NXP Semiconductors

Infineon Technologies

Texas Instruments

Analog Devices

Microchip Technology

Broadcom

Marvell Technology

Renesas Electronics

STMicroelectronics

Qualcomm Technologies

Bosch Mobility

Continental AG

ZF Friedrichshafen

Aptiv

Denso

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Shipment Volume, 2025–2030

- By Active Systems, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now