Technology Market Outlook 2030")

Technology Market Outlook 2030") Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Vehicle-to-Grid technology market is valued at USD ~, represents a strategically important segment of the national energy transition, integrating electric mobility with grid flexibility and distributed energy systems. The market scale reflects growing monetization of bidirectional charging hardware, fleet aggregation platforms, and grid services participation. Demand is shaped by the convergence of renewable energy penetration, grid congestion challenges, and federal fleet electrification mandates. Utilities increasingly rely on mobile battery assets to stabilize frequency, manage peak loads, and support resilience strategies, positioning V2G as a structural enabler of next-generation power infrastructure rather than a niche pilot solution.

Within the country, the market is concentrated in major urban and innovation-driven regions such as the West Coast, the Northeast corridor, and selected metropolitan hubs in the South and Southwest. These regions dominate due to advanced utility deregulation frameworks, high electric vehicle adoption, and early implementation of distributed energy resource programs. At the same time, global technology influence is shaped by leading automotive manufacturers and power electronics firms headquartered in innovation-centric regions abroad, whose investments in bidirectional charging standards and vehicle platforms strongly shape domestic deployment pathways and interoperability norms.

Market Segmentation

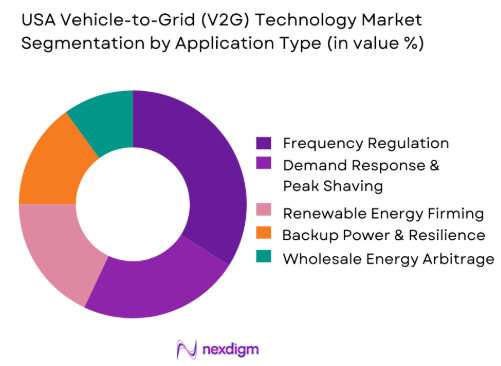

By Application Type

The USA Vehicle-to-Grid technology market is segmented by application into frequency regulation, demand response and peak shaving, renewable energy firming, backup power and resilience, and wholesale energy arbitrage. Among these, frequency regulation clearly dominates due to its immediate commercial viability and operational compatibility with fleet-based deployments. Grid operators prioritize assets capable of responding within milliseconds to stabilize system frequency, and electric vehicle batteries provide unmatched responsiveness compared to conventional resources. Fleet operators benefit from predictable dispatch schedules and standardized compensation mechanisms, making participation both financially attractive and operationally simple. In addition, regulatory frameworks enabling aggregated distributed energy resources to participate in ancillary service markets have accelerated adoption of frequency-focused V2G programs. This combination of technical suitability, revenue reliability, and regulatory clarity positions frequency regulation as the anchor application segment across utility territories nationwide.

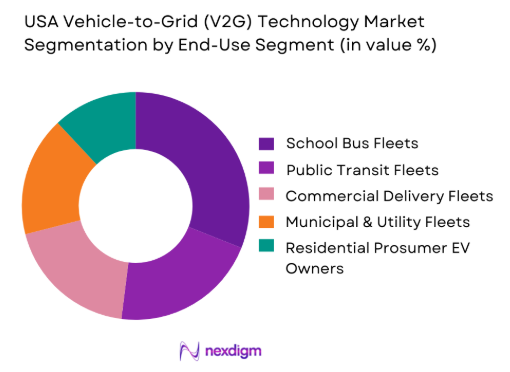

By End-Use Segment

The market is segmented into school bus fleets, public transit fleets, commercial delivery fleets, municipal and utility fleets, and residential prosumer electric vehicle owners. School bus fleets dominate the segment landscape because they combine predictable operational schedules with centralized charging infrastructure and strong access to public funding programs. These fleets remain idle during peak grid demand periods, enabling utilities to draw on stored energy without affecting transport operations. Public sector procurement frameworks further accelerate adoption by bundling vehicles with charging and grid-integration infrastructure. Additionally, school districts often participate in resilience and sustainability initiatives, making them ideal partners for early-stage V2G commercialization. The alignment of operational feasibility, financial incentives, and policy support has firmly positioned school bus fleets as the most scalable and economically attractive end-use segment in the current market structure.

Competitive Landscape

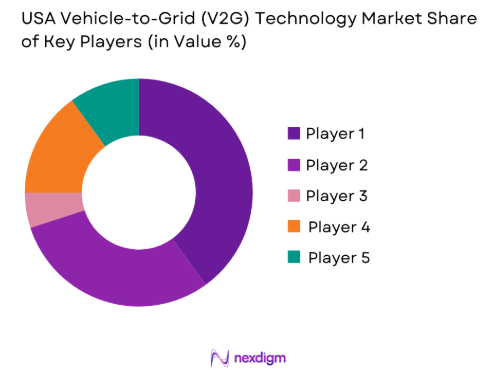

The USA Vehicle-to-Grid (V2G) Technology market is dominated by a few major players, including Nuvve Corporation and global or regional brands like ABB E-mobility, Siemens Smart Infrastructure, and Schneider Electric. This consolidation highlights the significant influence of these key companies.

| Company | Established | Headquarters | Core Focus | V2G Platform Type | Key End-Use | Utility Partnerships | Fleet Contracts | Grid Market Access |

| Nuvve Corporation | 2010 | California, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Fermata Energy | 2010 | Virginia, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| ABB E-mobility | 2010 | North Carolina, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Siemens Smart Infrastructure | 1847 | Georgia, USA | ~ | ~ | ~ | ~ | ~ | ~ |

| Schneider Electric | 1836 | Massachusetts, USA | ~ | ~ | ~ | ~ | ~ | ~ |

USA Vehicle-to-Grid (V2G) Technology Market Analysis

Growth Drivers

Grid Flexibility and Renewable Integration Needs

The increasing penetration of variable renewable energy sources has intensified the need for fast-responding grid flexibility solutions. Vehicle-to-Grid technology directly addresses this requirement by transforming electric vehicles into distributed storage assets that can balance intermittent generation and demand volatility. As utilities face rising costs associated with traditional peaking plants and stationary storage, V2G offers a scalable and cost-efficient alternative. The ability to aggregate thousands of mobile batteries into virtual power plants enhances grid stability while creating new revenue streams for fleet owners. This cause-and-effect relationship between renewable integration challenges and distributed flexibility demand is a fundamental driver of sustained V2G adoption across utility territories.

Federal Fleet Electrification Mandates

Public sector electrification mandates covering school districts, municipalities, and federal agencies have accelerated deployment of electric fleets at unprecedented scale. These mandates do not only increase the number of connected batteries but also create centralized charging environments ideal for bidirectional energy flow. As agencies seek to maximize return on infrastructure investments, V2G becomes a natural extension of fleet electrification strategies. The outcome is a structural shift in procurement logic, where charging equipment is evaluated not just as a cost center but as a revenue-generating grid asset. This transition fundamentally reshapes how public fleets justify capital allocation toward advanced charging systems.

Challenges

High Capital Cost of Bidirectional Infrastructure

The upfront investment required for bidirectional chargers, grid upgrades, and advanced energy management software remains a major barrier to widespread adoption. Compared to conventional charging systems, V2G-enabled infrastructure requires more sophisticated power electronics, cybersecurity features, and interconnection equipment. These higher costs extend payback periods, particularly for smaller fleet operators and municipalities with constrained budgets. Without standardized incentive frameworks and financing mechanisms, many potential adopters remain hesitant to commit to large-scale deployment. This capital intensity slows market penetration despite strong long-term economic logic.

Regulatory Fragmentation Across States

The absence of uniform interconnection standards and compensation models across utility jurisdictions creates uncertainty for market participants. Fleet operators and technology providers must navigate a patchwork of rules governing grid access, export tariffs, and market participation eligibility. This fragmentation increases project complexity and raises transaction costs, discouraging national-scale rollouts. Utilities also face regulatory risk when integrating mobile assets into system planning processes. Until clearer and more harmonized frameworks emerge, regulatory inconsistency will continue to act as a drag on the pace of commercialization.

Opportunities

School Bus and Public Fleet Electrification Programs

Large-scale public fleet electrification initiatives present a unique opportunity to embed V2G capabilities at the infrastructure design stage. By integrating bidirectional charging into funded vehicle programs, stakeholders can bypass retrofit costs and accelerate commercialization timelines. These programs also create highly visible demonstration projects that build confidence among utilities, regulators, and private fleet operators. The resulting ecosystem effect extends beyond transportation, positioning public fleets as cornerstone assets in local energy resilience strategies. This opportunity supports both rapid scaling and long-term market normalization.

Virtual Power Plant Expansion

The rapid development of virtual power plants creates a natural growth pathway for V2G aggregation platforms. As utilities increasingly rely on distributed energy resources to meet peak demand and reliability targets, aggregated EV batteries offer unmatched scalability. The integration of V2G into virtual power plant frameworks enables dynamic load balancing, emergency response, and localized grid support. This convergence unlocks recurring service revenues and strengthens the business case for both technology providers and fleet operators. Over time, this opportunity is expected to reposition V2G from an ancillary service solution to a core grid asset class.

Future Outlook

The USA Vehicle-to-Grid technology market is positioned to transition from early commercialization to structural integration within the national energy system. As utilities evolve from centralized generation models toward distributed flexibility architectures, V2G will become a foundational layer supporting resilience, decarbonization, and grid modernization. The next phase of development will be characterized by deeper OEM involvement, standardized regulatory frameworks, and expanding participation in wholesale and ancillary service markets. This strategic evolution will redefine electric vehicles as active grid participants rather than passive energy consumers.

Major Players

- Nuvve Corporation

- Fermata Energy

- ABB E-mobility

- Siemens Smart Infrastructure

- Schneider Electric

- Hitachi Energy

- Enel X North America

- ENGIE North America

- DENSO

- Nissan Energy

- Ford Pro Energy Solutions

- Hyundai Motor Group

- Wallbox Chargers

- EVBox

- ChargePoint

Key Target Audience

- Electric vehicle manufacturers and OEM energy divisions

- Utility companies and grid operators

- Public and private fleet operators

- Renewable energy developers and virtual power plant operators

- Investments and venture capitalist firms

- Regulatory Commission state public utility commissions

- Charging infrastructure developers and network operators

- Battery and power electronics suppliers

Research Methodology

Step 1: Identification of Key Variables

The research begins with mapping the complete ecosystem of stakeholders influencing the USA Vehicle-to-Grid technology market. This includes utilities, fleet operators, OEMs, and technology vendors. Secondary intelligence sources and proprietary datasets are used to identify deployment patterns, revenue models, and regulatory touchpoints shaping market dynamics.

Step 2: Market Analysis and Construction

Historical and current market data is compiled to assess penetration of bidirectional infrastructure and aggregation platforms. Revenue flows from grid services participation are analyzed to construct a bottom-up market model. This ensures alignment between technology deployment and commercial outcomes.

Step 3: Hypothesis Validation and Expert Consultation

Key assumptions are validated through structured interviews with industry executives, utility planners, and fleet energy managers. These interactions provide insight into operational challenges, interconnection processes, and evolving business models.

Step 4: Research Synthesis and Final Output

Findings from primary and secondary research are synthesized to build a coherent market narrative. Continuous cross-validation ensures consistency across segmentation, competitive positioning, and future outlook analysis.

- Executive Summary

- Research Methodology (Market definitions and scope boundaries, terminology and abbreviations, V2G and V2X taxonomy and use case mapping, market sizing logic by enabled vehicles chargers and dispatched capacity, revenue attribution across hardware software aggregation and services, primary interview program with utilities OEMs charging operators and aggregators, data triangulation and validation approach, assumptions limitations and data gaps)

- Definition and Scope

- Market Genesis and Evolution of Bidirectional Charging in the USA

- V2G Value Stack Across Vehicle Charger Aggregator and Market Operator

- Interconnection Rules and Market Participation Pathways for DER Aggregations

- Standards Landscape for Bidirectional Charging and Communication

- Utility Programs and Fleet Led Deployment Models

- Growth Drivers

Rising grid peak demand and flexibility needs

Fleet electrification scale up in buses and commercial vehicles

DER market participation enablement for aggregated resources

Resilience demand for critical facilities and microgrids

Time of use rates and demand charge avoidance economics - Challenges

Bidirectional vehicle availability constraints by model lineup

Interconnection timelines and export permitting complexity

Battery warranty concerns and cycle life perception barriers

Measurement verification and settlement complexity for V2G services

Cybersecurity and data governance requirements for grid connected assets - Opportunities

Depot led V2G for school buses and municipal fleets

Bundled charger plus software plus revenue share programs

Integration with onsite solar storage and building energy management

Automated dispatch optimization and performance guarantees

Standardized contracting templates for utilities and fleets - Trends

Shift from pilots to programmatic fleet deployments

Growth of virtual power plant models using EV fleets

Standardization push for interoperability and plug to market workflows

Increasing focus on resilience events and grid emergency programs

Commercialization of bidirectional fast charging hardware portfolios - Regulatory & Policy Landscape

SWOT Analysis

Stakeholder & Ecosystem Analysis

Porter’s Five Forces Analysis

Competitive Intensity & Ecosystem Mapping

- By Value, 2019–2024

- By Enabled Vehicle Base, 2019–2024

- By Bidirectional Charger Installed Base, 2019–2024

- By Dispatchable Capacity and Events Delivered, 2019–2024

- By Fleet Type (in Value %)

Electric school bus fleets

Municipal and public sector fleets

Commercial delivery and logistics fleets

Light duty consumer EVs

Workplace and campus fleets - By Application (in Value %)

Peak shaving and demand response

Frequency regulation and ancillary services

Emergency backup and resilience power

Renewable smoothing and curtailment reduction

Capacity and resource adequacy participation - By Technology Architecture (in Value %)

AC bidirectional charging systems

DC bidirectional charging systems

Onboard inverter based bidirectional platforms

Offboard inverter based bidirectional platforms

Multi port depot bidirectional charging hubs - By Connectivity Type (in Value %)

Utility managed V2G programs

Aggregator managed V2G platforms

OEM managed energy services

Charger network managed V2G services

Market operator integrated dispatch platforms - By End-Use Industry (in Value %)

Electric utilities and community choice aggregators

School districts and fleet operators

Charging infrastructure operators

Commercial building owners and microgrid developers

Energy retailers and virtual power plant operators - By Region (in Value %)

California and West Coast markets

Northeast ISO markets

Texas ERCOT market

Midwest and Great Lakes markets

Southeast regulated utility markets

- Competitive ecosystem structure across aggregators charger OEMs and utilities

- Positioning driven by dispatch performance interoperability and scale readiness

- Partnership models across OEMs fleets and grid operators

- Cross Comparison Parameters (bidirectional charger efficiency, export power rating and duty cycle, standards compliance readiness, aggregation platform dispatch latency, metering and settlement capability, cybersecurity posture and device management, program revenue capture and contract flexibility, warranty alignment and battery impact controls)

- SWOT analysis of major players

- Pricing and commercial model benchmarking

- Porter’s Five Forces

- Detailed Profiles of Major Companies

Nuvve

Fermata Energy

The Mobility House

Rhombus Energy Solutions

Wallbox

ABB

Siemens

Schneider Electric

Eaton

ChargePoint

Autogrid

EnergyHub

dcbel

Enel X

Bidgely

- Fleet operator decision logic for participation and uptime

- Utility program design priorities and performance requirements

- Aggregator contracting models and revenue share structures

- Site host economics for demand charges and resilience value

- Risk factors across warranty liability and operational constraints

- By Value, 2025–2030

- By Enabled Vehicle Base, 2025–2030

- By Bidirectional Charger Installed Base, 2025–2030

- By Dispatchable Capacity and Events Delivered, 2025–2030

Technology Market Outlook 2030")

Technology Market Outlook 2030")

Technology Market Outlook 2030")

Technology Market Outlook 2030")

Technology Market Outlook 2030") Request a Sample

Request a Sample Technology Market Outlook 2030") Ask for Customization

Ask for Customization Technology Market Outlook 2030") Get a Quote

Get a Quote Technology Market Outlook 2030") Enquire Now

Enquire Now Technology Market Outlook 2030")