Download PDF

Download PDF Download PDF

Download PDFMarket Overview

Based on a recent historical assessment, the USA Wealth Management Market oversees approximately USD ~ trillion in assets under management, according to data published by the Investment Company Institute and the Federal Reserve. The market is driven by strong equity market capitalization exceeding USD 50 trillion, a large high-net-worth population, expanding retirement savings accounts, and institutional advisory mandates across private banking, registered investment advisory firms, and asset management institutions operating nationwide.

New York serves as the primary financial hub due to its concentration of global asset managers, investment banks, and regulatory institutions, while California hosts a significant base of technology-driven wealth clients and venture capital wealth creation. Chicago and Boston maintain strong institutional advisory ecosystems. High household net worth exceeding USD ~trillion nationally supports sustained advisory demand, reinforced by advanced digital investment platforms and diversified capital markets infrastructure.

Market Segmentation

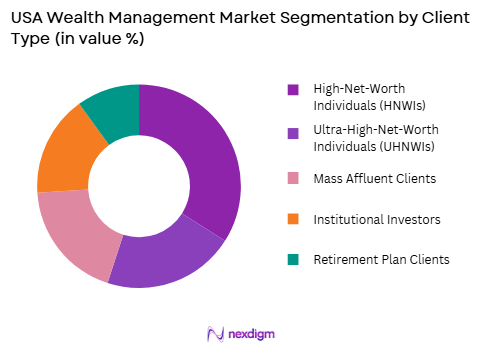

By Client Type

By Product Type: USA Wealth Management Market market is segmented by product type into High-Net-Worth Individuals (HNWIs), Ultra-High-Net-Worth Individuals (UHNWIs), Mass Affluent Clients, Institutional Investors, and Retirement Plan Clients. Recently, High-Net-Worth Individuals (HNWIs) have a dominant market share due to factors such as substantial equity ownership, business ownership liquidity events, diversified portfolio allocation needs, estate planning complexity, tax optimization requirements, and strong private banking relationships supported by nationwide advisory networks and digital portfolio management systems.

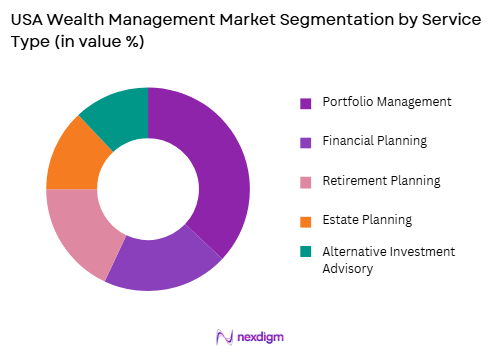

By Service Type

By Product Type: USA Wealth Management Market market is segmented by product type into Portfolio Management, Financial Planning, Retirement Planning, Estate Planning, and Alternative Investment Advisory. Recently, Portfolio Management has a dominant market share due to factors such as active equity participation, diversified asset allocation strategies, exchange-traded fund expansion, algorithm-driven advisory tools, fiduciary compliance standards, and the integration of ESG frameworks and private market exposure within structured discretionary mandates offered by national advisory institutions.

Competitive Landscape

The USA Wealth Management Market demonstrates high concentration among global asset managers, private banks, and registered investment advisory firms. Consolidation has increased through mergers between brokerage platforms and digital advisory providers. Large institutions leverage scale, research capabilities, diversified product offerings, and technology-driven client platforms to retain dominant positions, while independent advisors compete through personalized service models and fiduciary advisory structures.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue (USD) | Assets Under Management (USD) |

| BlackRock | 1988 | New York, USA | ~ | ~ | ~ | ~ | ~ |

| Vanguard | 1975 | Pennsylvania, USA | ~ | ~ | ~ | ~ | ~ |

| Fidelity Investments | 1946 | Massachusetts, USA | ~ | ~ | ~ | ~ | ~ |

| Morgan Stanley Wealth Management | 1935 | New York, USA | ~ | ~ | ~ | ~ | ~ |

| JPMorgan Asset & Wealth Management | 1799 | New York, USA | ~ | ~ | ~ | ~ | ~ |

USA Wealth Management Market Analysis

Growth Drivers

Expansion of Equity Market Capitalization and Wealth Creation Through Capital Markets

The sustained growth of U.S. equity market capitalization, supported by corporate profitability, technology sector expansion, and deep capital markets, has significantly increased investable assets managed by wealth advisors across the country. Public market valuations exceeding USD 50 trillion provide a broad asset base for discretionary portfolio mandates and long-term capital appreciation strategies. Liquidity events from mergers, acquisitions, and initial public offerings generate substantial wealth for entrepreneurs and executives seeking structured advisory services. Retirement account contributions across defined contribution plans further expand assets under advisory management. Diversified asset classes including exchange-traded funds and private equity enhance portfolio complexity, increasing demand for professional allocation expertise. Strong investor participation in equities sustains brokerage and advisory revenue growth. Digital brokerage platforms integrate seamlessly with wealth management services, expanding client onboarding efficiency. Institutional custody infrastructure strengthens operational scalability for advisory firms. Regulatory frameworks emphasizing fiduciary standards enhance investor confidence. This capital market-driven wealth expansion underpins long-term structural growth within the USA Wealth Management Market.

Demographic Shifts and Intergenerational Wealth Transfer Dynamics

The transition of substantial financial assets from aging baby boomers to younger generations is creating one of the largest intergenerational wealth transfers in U.S. history, intensifying demand for structured estate planning and advisory oversight. Households collectively hold net worth exceeding USD 150 trillion, much of which is allocated to financial assets requiring professional management. Beneficiaries increasingly seek comprehensive advisory services combining tax planning, philanthropy structuring, and diversified portfolio strategies. Younger high-income professionals favor digital advisory tools and hybrid advisory engagement models. Family office structures expand to manage concentrated wealth pools derived from private business ownership and investment holdings. Advisors must integrate multi-generational risk tolerance preferences within asset allocation frameworks. Tax efficiency strategies gain prominence amid evolving fiscal policies. Trust structures and estate planning vehicles increase complexity in advisory mandates. Wealth managers leverage technology platforms to facilitate secure client communication and reporting. These demographic and structural transitions collectively drive sustained advisory demand across multiple wealth tiers nationwide.

Market Challenges

Fee Compression and Competitive Pressure from Low-Cost Passive Investment Platforms

The proliferation of low-cost exchange-traded funds and passive index strategies has intensified pricing pressure across the USA Wealth Management Market, challenging traditional active management fee structures. Investors increasingly compare advisory fees against low-expense passive alternatives, compelling firms to justify value through differentiated services. Robo-advisory platforms provide automated portfolio allocation at significantly reduced cost, increasing competition in the mass affluent segment. Margin compression affects mid-sized advisory firms lacking economies of scale. Institutional investors negotiate lower management fees for large mandates. Technology investments required to maintain competitive digital interfaces increase operational expenses. Client expectations for transparency and performance reporting have risen substantially. Consolidation among advisory firms accelerates as smaller players struggle to maintain profitability. Regulatory scrutiny of fee disclosures increases compliance burdens. These structural pricing pressures create ongoing margin management challenges within the industry.

Regulatory Complexity and Fiduciary Compliance Obligations

The USA Wealth Management Market operates under layered regulatory oversight including Securities and Exchange Commission supervision, state-level registration requirements, and fiduciary duty standards. Advisors must adhere to strict suitability and disclosure obligations when recommending investment products. Evolving regulations concerning retirement accounts and best interest standards require continuous compliance monitoring. Cybersecurity oversight adds additional operational requirements. Reporting transparency standards increase administrative workload. Cross-border advisory services introduce international compliance considerations. Documentation requirements for alternative investments and private placements are extensive. Smaller advisory firms face disproportionate compliance cost burdens. Regulatory examinations necessitate detailed recordkeeping and audit readiness. This multifaceted regulatory landscape increases operational complexity while reinforcing investor protection standards.

Opportunities

Integration of Artificial Intelligence and Personalized Portfolio Customization Platforms

The deployment of artificial intelligence within portfolio management systems presents transformative opportunities for scalable yet personalized wealth advisory services. AI-driven analytics enable dynamic asset allocation adjustments based on real-time market conditions and client behavior data. Automated rebalancing tools enhance efficiency and reduce manual oversight costs. Predictive modeling supports proactive tax-loss harvesting strategies. Client portals provide interactive dashboards for performance monitoring and goal tracking. Natural language processing tools enhance client communication responsiveness. Data-driven personalization improves client retention and cross-selling effectiveness. Cloud-based infrastructure increases scalability across advisory networks. Strategic technology partnerships accelerate innovation cycles. Enhanced cybersecurity integration protects digital advisory ecosystems. These advancements enable firms to expand service offerings while maintaining fiduciary oversight standards.

Expansion of Alternative Investments and Private Market Access for Accredited Investors

Growing investor interest in private equity, venture capital, real estate, and hedge funds creates substantial expansion opportunities within diversified wealth portfolios. Accredited investors increasingly allocate capital beyond traditional public equities and fixed income instruments. Wealth managers can structure feeder funds and co-investment opportunities to broaden private market participation. Institutional-grade due diligence processes enhance risk assessment in illiquid asset classes. Portfolio diversification into alternatives may improve long-term risk-adjusted returns. Structured products provide customized exposure aligned with client objectives. Demand for environmental and impact-oriented private investments is rising. Advisory platforms integrate reporting tools for illiquid asset performance tracking. Strategic partnerships with private market sponsors enhance product availability. This shift toward broader asset class diversification strengthens long-term revenue growth potential across the USA Wealth Management Market.

Future Outlook

Over the next five years, the USA Wealth Management Market is expected to maintain expansion supported by capital market growth, technological innovation, and demographic wealth transitions. Digital advisory platforms and AI-enabled portfolio management systems will increase operational efficiency and personalization. Regulatory clarity around fiduciary standards is likely to reinforce investor confidence. Alternative investments and ESG-focused mandates are anticipated to further diversify portfolio structures and sustain advisory demand.

Major Players

- BlackRock

- Vanguard

- Fidelity Investments

- Morgan Stanley Wealth Management

- JPMorgan Asset & Wealth Management

- Goldman Sachs Asset Management

- Charles Schwab

- Bank of America Merrill Lynch

- UBS Wealth Management Americas

- Wells Fargo Advisors

- T. Rowe Price

- Edward Jones

- Raymond James

- Northern Trust

- Franklin Templeton

Key Target Audience

- Asset management firms

- Private banks

- Registered investment advisory firms

- Family offices

- Institutional investors

- Investments and venture capitalist firms

- Government and regulatory bodies

- Pension funds

Research Methodology

Step 1: Identification of Key Variables

Key variables including assets under management, client demographics, service segmentation, and regulatory frameworks were identified using Federal Reserve and Investment Company Institute publications. Macroeconomic and capital market indicators were incorporated into the analytical framework.

Step 2: Market Analysis and Construction

Market construction was based on officially reported assets under management and capital market valuation data. Segmentation was developed by mapping client categories and advisory service models across institutional and retail wealth channels.

Step 3: Hypothesis Validation and Expert Consultation

Industry assumptions were validated through consultation with portfolio managers, compliance specialists, and financial analysts. Cross-verification ensured alignment with publicly disclosed financial statements and regulatory filings.

Step 4: Research Synthesis and Final Output

Quantitative findings and qualitative insights were consolidated into a structured analytical model. Outputs were reviewed for logical coherence, factual consistency, and regulatory alignment before final report preparation.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Rising Household Financial Assets and Equity Market Participation

Growing Demand for Retirement and Estate Planning Services

Expansion of Digital Advisory and Robo Advisory Platforms - Market Challenges

Market Volatility Impacting Portfolio Performance

Regulatory Compliance and Fiduciary Standards

Fee Compression and Competitive Pricing Pressure - Market Opportunities

Integration of Artificial Intelligence in Portfolio Construction

Expansion of ESG and Sustainable Investment Solutions

Cross Border Wealth Advisory for Global Investors - Trends

Shift Toward Passive and ETF Based Investment Strategies

Increasing Adoption of Hybrid Human Digital Advisory Models - Government Regulations

- SWOT Analysis

- Porter’s Five Forces

- By Market Value, 2020-2025

- By Installed Units, 2020-2025

- By Average System Price, 2020-2025

- By System Complexity Tier, 2020-2025

- By System Type (In Value%)

Discretionary Portfolio Management

Non Discretionary Advisory Services

Financial Planning Services

Robo Advisory Solutions

Alternative Investment Advisory - By Platform Type (In Value%)

Private Banking Platforms

Independent Registered Investment Advisors

Broker Dealer Platforms

Digital Wealth Management Platforms

Hybrid Advisory Platforms - By Fitment Type (In Value%)

Fee Only Advisory Model

Commission Based Model

Hybrid Fee Commission Model

Subscription Based Wealth Services - By End User Segment (In Value%)

High Net Worth Individuals

Ultra High Net Worth Individuals

Mass Affluent Investors

Family Offices

- Market Share Analysis

- Cross Comparison Parameters (Assets Under Management, Fee Structure Model, Minimum Investment Threshold, Digital Advisory Integration, Product Diversification Breadth, Client Segmentation Focus, Portfolio Customization Capability, Alternative Investment Access)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Morgan Stanley Wealth Management

Merrill Lynch Wealth Management

UBS Wealth Management USA

J P Morgan Wealth Management

Goldman Sachs Private Wealth Management

Charles Schwab Corporation

Fidelity Investments

Vanguard Personal Advisor Services

Edward Jones

Raymond James Financial

Wells Fargo Advisors

Ameriprise Financial

Northern Trust Wealth Management

Citi Private Bank

Bank of America Private Bank

- Growing Demand for Personalized Portfolio Strategies

- Increased Allocation toward Alternative and Private Market Investments

- Rising Preference for Digital Client Reporting and Transparency

- Succession Planning Needs among Aging High Net Worth Client

- Forecast Market Value, 2026-2035

- Forecast Installed Units, 2026-2035

- Price Forecast by System Tier, 2026-2035

- Future Demand by Platform, 2026-2035

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now