Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Windshields market current size stands at around USD ~ million, reflecting sustained replacement demand driven by vehicle parc aging, collision frequency, and rising complexity of laminated safety glass. Growth is reinforced by expanding ADAS-compatible glazing, broader insurance coverage for glass claims, and service network density. Value capture concentrates around premium interlayers, acoustic laminates, and HUD-ready assemblies, supported by recalibration requirements and installer capability expansion across OEM and aftermarket channels nationwide.

Demand concentrates in California, Texas, Florida, New York, and Illinois due to dense vehicle ownership, higher mileage exposure, and severe weather incidence. Metropolitan corridors such as Los Angeles, Dallas–Fort Worth, Miami, New York City, and Chicago exhibit mature installer ecosystems, insurer-linked repair networks, and calibration infrastructure. State safety compliance, urban fleet density, and logistics hubs reinforce regional clustering of service capacity and specialized glazing inventory availability.

Market Segmentation

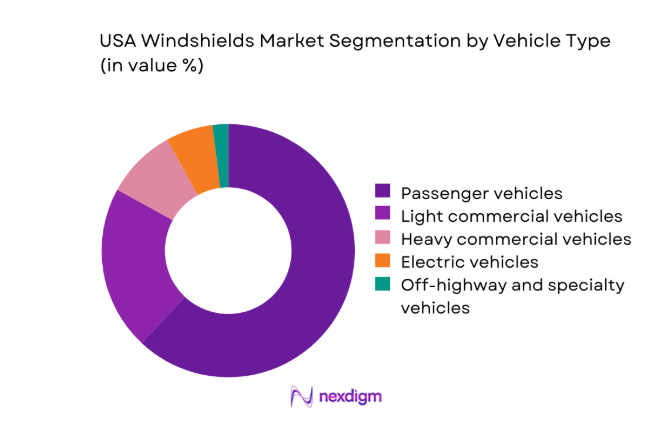

By Vehicle Type

Passenger vehicles dominate windshield demand due to higher fleet density, daily mileage intensity, and urban exposure to road debris and collision frequency. Electric vehicles increasingly require specialized laminated glass compatible with camera housings and HUD integration, accelerating premium segment penetration. Light commercial vehicles sustain consistent replacement cycles driven by last-mile delivery operations and extended operating hours. Heavy commercial and specialty vehicles contribute smaller shares, constrained by longer replacement intervals and lower sensor density, yet exhibit rising complexity from fleet safety mandates and telematics integration.

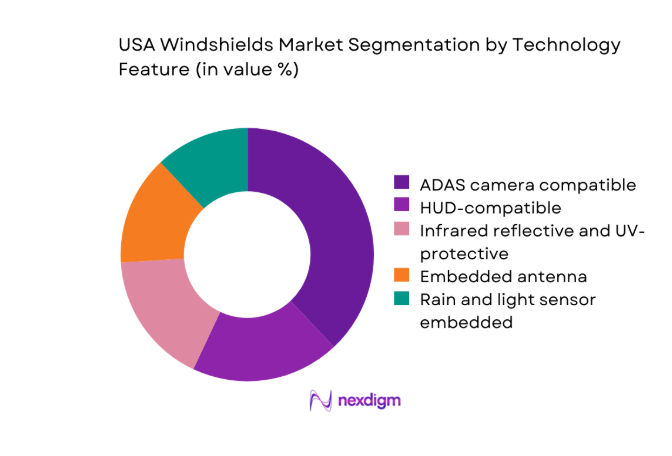

By Technology Feature

ADAS-compatible windshields lead adoption as camera calibration requirements become standard in collision repairs and replacements. HUD-ready laminates expand within premium passenger segments, supported by OEM integration roadmaps. Infrared reflective and UV-protective glass grows with climate-driven comfort needs and energy efficiency focus. Embedded antenna solutions support connectivity use cases, while rain and light sensor integration continues to diffuse across mid-range vehicles. Technology convergence increases average complexity per replacement, elevating service capability requirements across installer networks.

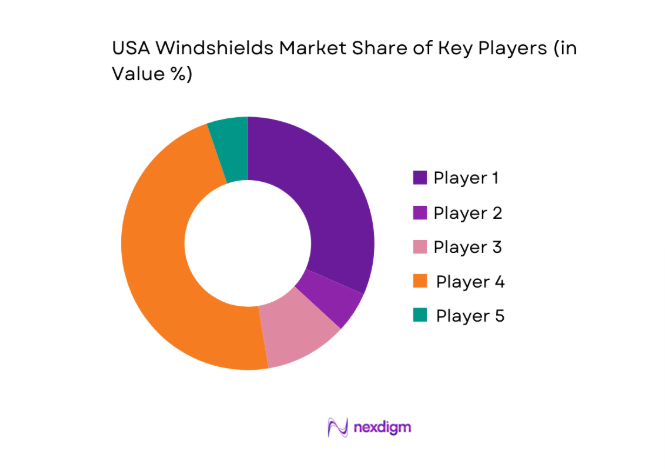

Competitive Landscape

The competitive landscape features vertically integrated glass producers, national service chains, and regional installers aligned with insurer referral networks and OEM standards. Differentiation centers on calibration capability, geographic coverage, turnaround time, and compliance readiness for safety glazing requirements.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Safelite Group | 1947 | Columbus, Ohio | ~ | ~ | ~ | ~ | ~ | ~ |

| AGC Automotive Americas | 1907 | Tokyo, Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Fuyao Glass America | 1987 | Fuqing, China | ~ | ~ | ~ | ~ | ~ | ~ |

| Pilkington North America | 1826 | Lathom, UK | ~ | ~ | ~ | ~ | ~ | ~ |

| Saint-Gobain Sekurit | 1665 | Courbevoie, France | ~ | ~ | ~ | ~ | ~ | ~ |

USA Windshields Market Analysis

Growth Drivers

Rising vehicle parc and aging fleet replacement cycles

Rising vehicle parc and aging fleet replacement cycles increase windshield replacement frequency across metropolitan corridors. State transportation agencies recorded roadway vehicle registrations exceeding 280000000 in 2023, with average vehicle age surpassing 12 in 2024. Older fleets correlate with higher glass fatigue and seal degradation incidents. Urban congestion increased annual vehicle miles traveled beyond 3300000000000 in 2024, elevating debris impact exposure. Insurance claim filings for glass damage rose with weather volatility, while Department of Transportation safety campaigns reinforced windshield integrity compliance. Collision repair backlogs across 2022–2024 expanded service throughput requirements, sustaining replacement demand for laminated safety glass nationwide.

Increasing ADAS penetration requiring windshield replacement recalibration

Increasing ADAS penetration requiring windshield replacement recalibration structurally raises service demand. National Highway Traffic Safety Administration reported advanced driver assistance features present in over 170000000 registered vehicles during 2024. Camera-equipped windshields mandate post-installation calibration aligned with OEM procedures. State inspection programs incorporated sensor alignment checks across 2023–2024, increasing replacement complexity. Federal crash avoidance initiatives cited reductions in lane-departure incidents linked to camera systems across 2022–2025. Service networks expanded calibration bays by thousands of units nationwide, while technician certification counts grew materially. Calibration downtime extends service cycles, increasing installed glass turnover and supporting sustained replacement volumes.

Challenges

High replacement cost of ADAS and HUD-compatible windshields

High replacement cost of ADAS and HUD-compatible windshields constrains consumer acceptance and insurer reimbursement efficiency. Department of Transportation service advisories during 2023 documented calibration equipment procurement requirements exceeding 15000 per bay, increasing installer capital burden. OEM procedures mandate multi-point calibration, extending average service time beyond 120 minutes per replacement. State insurance regulators flagged rising claim disputes across 2022–2024 due to parts compatibility and recalibration protocols. Urban repair centers reported appointment backlogs during peak storm seasons. Technician certification requirements expanded across 2024, limiting labor availability. These frictions suppress throughput scalability and slow premium windshield adoption across non-luxury segments.

Calibration complexity and technician skill gaps

Calibration complexity and technician skill gaps limit service quality and geographic coverage. Federal workforce statistics across 2023 showed automotive glass technician vacancy rates exceeding 8 in major metros, reflecting skills shortages. OEM service bulletins updated calibration procedures multiple times during 2022–2025, increasing retraining frequency. State safety inspections added camera alignment checkpoints, raising compliance pressure on small installers. Average technician training cycles extended beyond 40 hours annually, reducing productive capacity. Rural coverage gaps persist due to limited access to calibration equipment. These constraints elevate service variability, increase rework incidents, and delay deployment of advanced glazing solutions outside primary urban corridors.

Opportunities

Aftermarket ADAS calibration service expansion

Aftermarket ADAS calibration service expansion presents scalable growth potential as feature penetration deepens. National safety programs reported camera-equipped vehicle counts increasing by tens of millions across 2022–2025, expanding recalibration needs after glass replacement. State transportation departments approved mobile calibration units for roadside service pilots in 2024, improving rural reach. Technician certification enrollments rose materially across community training programs. Fleet operators mandated calibration verification after windshield service for vehicles operating above 50000 annual miles. Mobile service adoption improved first-time fix rates and reduced downtime hours per incident. These shifts support network densification and higher service attach rates alongside replacement volumes.

Partnerships with insurers for preferred glass networks

Partnerships with insurers for preferred glass networks create durable demand visibility and workflow standardization. State insurance departments approved network-based claims routing frameworks across 2023–2024, accelerating insurer-to-installer referrals. Digital claims processing volumes increased materially as policyholders adopted app-based reporting. Repair cycle times improved with pre-authorized calibration protocols, reducing average vehicle downtime by multiple hours per claim. Insurer scorecards tied reimbursement tiers to compliance metrics, expanding adoption of certified procedures. Regional catastrophe response drills in 2024 coordinated surge capacity for hail events. These arrangements stabilize installer utilization and incentivize investments in calibration infrastructure nationwide.

Future Outlook

The market trajectory remains supported by expanding ADAS penetration, insurer network consolidation, and mobile calibration deployment through 2030. Regulatory emphasis on sensor integrity will standardize recalibration practices, while premium glazing adoption broadens beyond luxury segments. Regional capacity build-out and technician certification pipelines are expected to reduce service bottlenecks and improve turnaround consistency.

Major Players

- Safelite Group

- AGC Automotive Americas

- Fuyao Glass America

- Pilkington North America

- Saint-Gobain Sekurit

- PGW Auto Glass

- Vitro Automotive Glass

- Guardian Glass

- Xinyi Glass Holdings

- Nippon Sheet Glass

- Corning Incorporated

- Carlite

- Benson Auto Glass

- TruRoad Auto Glass

- American Glass Distributors

Key Target Audience

- Automotive OEMs and Tier-1 glazing integrators

- National and regional auto glass service chains

- Fleet operators and mobility service providers

- Insurance carriers and claims administrators

- Investments and venture capital firms

- Government and regulatory bodies with agency names including the National Highway Traffic Safety Administration and state Departments of Transportation

- Automotive dealership service networks

- ADAS calibration equipment and software providers

Research Methodology

Step 1: Identification of Key Variables

Core variables were defined across vehicle parc characteristics, ADAS feature penetration, replacement cycles, calibration requirements, and service network density. Regulatory standards, insurer routing practices, and technician certification norms were scoped to frame operational constraints. Supply chain availability of laminated and specialty glass was mapped across regions.

Step 2: Market Analysis and Construction

Primary demand pathways were constructed using replacement triggers, collision incidence patterns, and calibration mandates. Regional service capacity, urban–rural coverage gaps, and installer capability maturity were modeled. Technology feature diffusion and policy compliance thresholds were integrated to reflect service complexity.

Step 3: Hypothesis Validation and Expert Consultation

Assumptions were validated through structured discussions with installers, calibration specialists, fleet maintenance managers, and safety compliance professionals. Procedural updates, training cycles, and equipment readiness were cross-checked against regulatory guidance and insurer network requirements to refine operational realities.

Step 4: Research Synthesis and Final Output

Findings were synthesized into coherent market narratives linking regulatory drivers, service capacity, and technology adoption. Cross-segment implications were consolidated to inform strategic positioning. Insights were stress-tested for consistency across regions and use cases to ensure actionable outputs.

- Executive Summary

- Research Methodology (Market Definitions and scope alignment for windshield categories, OEM and aftermarket shipment tracking by vehicle class, Teardown analysis of laminated and tempered glass assemblies, Distributor and installer channel surveys across US regions, ASP benchmarking by glazing technology and vehicle segment, Regulatory and safety standard mapping including FMVSS 205)

- Definition and Scope

- Market evolution

- Usage and replacement pathways

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising vehicle parc and aging fleet replacement cycles

Increasing ADAS penetration requiring windshield replacement recalibration

Higher insurance coverage for glass damage claims

Growth in electric vehicles with advanced glazing requirements

Rising demand for acoustic and solar control windshields

Expansion of mobile windshield replacement services - Challenges

High replacement cost of ADAS and HUD-compatible windshields

Calibration complexity and technician skill gaps

Supply chain volatility for specialty laminated glass

OEM part pricing pressures and insurer reimbursement limits

Fragmentation of independent installer networks

Regulatory compliance costs for safety glazing standards - Opportunities

Aftermarket ADAS calibration service expansion

Partnerships with insurers for preferred glass networks

Growth in acoustic and solar control windshield upgrades

Fleet service contracts with logistics and ride-hailing operators

Recycling and circular economy programs for automotive glass

Localization of laminated glass manufacturing capacity - Trends

Integration of sensors and antennas into windshields

Rising adoption of HUD-compatible laminated glass

Mobile on-site replacement and calibration services

Consolidation among aftermarket glass service chains

Use of advanced interlayers for noise and heat reduction

Digital claims processing and scheduling by insurers - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Vehicle Type (in Value %)

Passenger cars

Light commercial vehicles

Heavy commercial vehicles

Electric vehicles

Off-highway and specialty vehicles - By Glass Type (in Value %)

Laminated windshields

Tempered rear and side glass

Acoustic laminated glass

Solar control glass

Heated windshields - By Technology Feature (in Value %)

ADAS camera compatible windshields

HUD-compatible windshields

Rain and light sensor embedded windshields

Infrared reflective and UV-protective windshields

Embedded antenna and connectivity windshields - By Sales Channel (in Value %)

OEM factory-fitment

Authorized dealer service

Independent aftermarket installers

Insurance-referred repair networks

Online glass replacement platforms - By End Use (in Value %)

New vehicle production

Collision repair and replacement

Wear-and-tear replacement

Fleet maintenance programs

Specialty vehicle retrofits

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Geographic coverage, Product portfolio breadth, ADAS calibration capability, OEM partnerships, Installer network scale, Pricing competitiveness, Service turnaround time, Warranty and aftersales support)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Safelite Group

AGC Automotive Americas

Fuyao Glass America

Pilkington North America

Saint-Gobain Sekurit

PGW Auto Glass

Vitro Automotive Glass

Guardian Glass

Xinyi Glass Holdings

Nippon Sheet Glass

Corning Incorporated

Carlite (Central Glass)

Benson Auto Glass

TruRoad Auto Glass

American Glass Distributors

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now