Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA wiper systems market is valued at approximately USD ~ billion based on a recent historical assessment derived from Federal Highway Administration vehicle parc statistics and U.S. automotive production data, reflecting combined OEM installation and aftermarket replacement demand for windshield and rear wiping systems. Market growth is primarily driven by a national vehicle parc exceeding 285 million registered vehicles and annual light vehicle production above 10 million units, both of which sustain recurring blade replacement cycles and integrated wiper module installations across passenger and commercial vehicles.

Automotive manufacturing hubs and distribution corridors including Michigan, Ohio, Indiana, Tennessee, and Texas dominate the USA wiper systems market due to concentration of vehicle assembly plants, tier-one automotive suppliers, and nationwide aftermarket logistics networks. These regions benefit from established automotive supply chains, skilled mechanical component manufacturing labor, and proximity to OEM customers and distribution centers. Strong fleet density and highway usage in these states also support high replacement frequency, reinforcing regional dominance in both production and consumption of wiper systems.

Market Segmentation

By Product Type

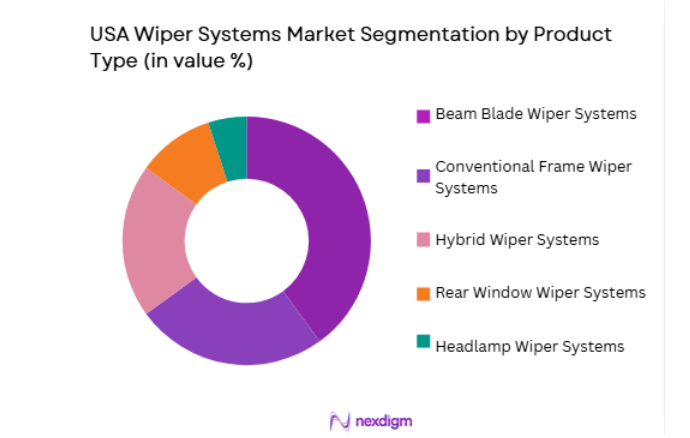

USA Wiper Systems market is segmented by product type into conventional frame wiper systems, beam blade wiper systems, hybrid wiper systems, rear window wiper systems, and headlamp wiper systems. Recently, beam blade wiper systems has a dominant market share due to factors such as superior aerodynamic performance, longer service life, and compatibility with modern curved windshields. Automakers increasingly adopt frameless beam blades as standard equipment because they reduce wind lift, noise, and streaking at highway speeds while maintaining consistent windshield contact. Consumer preference in the aftermarket also favors beam blades due to perceived premium quality and durability, reinforcing higher sales volumes across both OEM and replacement channels.

By Vehicle Type

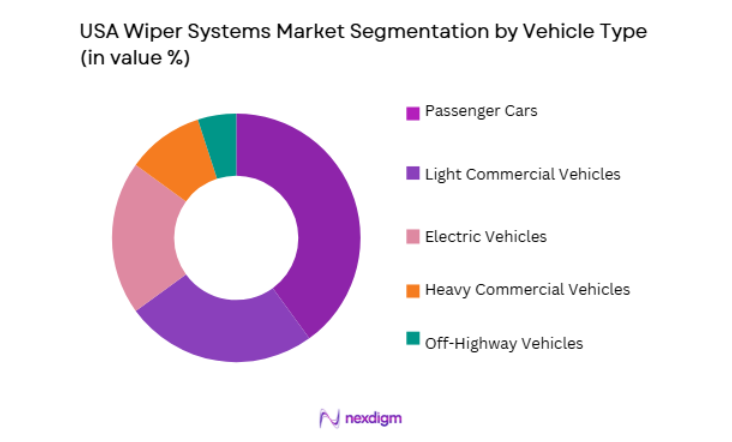

USA Wiper Systems market is segmented by vehicle type into passenger cars, light commercial vehicles, heavy commercial vehicles, electric vehicles, and off-highway vehicles. Recently, passenger cars has a dominant market share due to factors such as high ownership density, widespread daily usage, and large installed base across the national vehicle fleet. Passenger vehicles require multiple wiper blades per unit and experience frequent replacement driven by climatic exposure and annual mileage. Continuous production of sedans, SUVs, and crossover vehicles ensures sustained OEM installation demand, while extensive aftermarket servicing networks further amplify replacement consumption within the passenger car segment.

Competitive Landscape

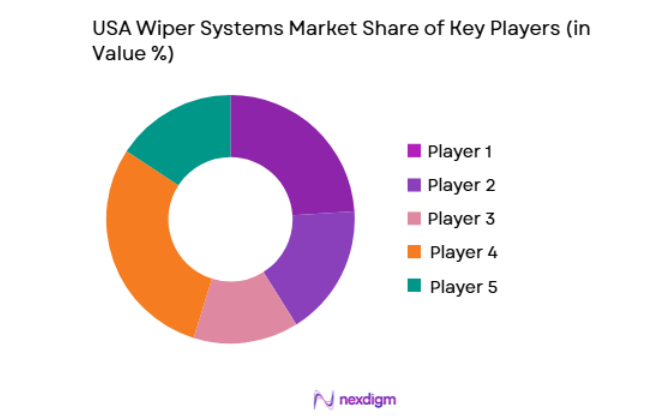

The USA wiper systems market is moderately consolidated with global automotive component manufacturers dominating OEM supply through long-term platform contracts, while the aftermarket remains competitive with multiple brand portfolios and retail distribution channels. Leading suppliers leverage advanced rubber compounds, aerodynamic blade designs, and integrated sensor technologies to differentiate products. Scale manufacturing, global sourcing, and established relationships with vehicle manufacturers allow major firms to maintain strong positioning, while regional aftermarket brands compete primarily on price and distribution reach.

| Company Name | Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | OEM Supply Presence |

| Bosch | 1886 | Germany | ~ | ~ | ~ | ~ | ~ |

| Denso Corporation | 1949 | Japan | ~ | ~ | ~ | ~ | ~ |

| Valeo | 1923 | France | ~ | ~ | ~ | ~ | ~ |

| Trico Products | 1917 | USA | ~ | ~ | ~ | ~ | ~ |

| Mitsuba Corporation | 1946 | Japan | ~ | ~ | ~ | ~ | ~ |

USA Wiper Systems Market Analysis

Growth Drivers

Expansion of Vehicle Parc and Replacement Cycle Intensity

The expansion of vehicle parc and replacement cycle intensity is a major growth driver for the USA wiper systems market because windshield wiper blades are consumable safety components requiring periodic replacement due to rubber degradation from ultraviolet radiation, temperature variation, and mechanical wear. The United States vehicle fleet exceeds 285 million registered vehicles, creating a vast installed base that continuously generates aftermarket demand independent of new vehicle sales cycles. Average blade replacement intervals of six to twelve months in many climatic regions increase recurring purchase frequency across retail channels. Passenger vehicles typically use two front blades and often a rear blade, multiplying unit consumption across the national fleet. Commercial vehicles and fleets operate at higher annual mileage and environmental exposure, accelerating wear and increasing replacement rates. Seasonal weather conditions including snow, ice, rain, and dust further intensify blade deterioration across diverse geographic regions. Retail distribution networks ensure wide availability of replacement blades through automotive stores, mass merchants, and service centers. This structurally recurring consumption pattern ensures stable revenue generation across the USA wiper systems market.

Technological Advancement in Aerodynamic and Smart Wiper Systems

Technological advancement in aerodynamic and smart wiper systems drives growth in the USA wiper systems market because modern vehicles increasingly require high-performance wiping solutions compatible with curved windshields, high driving speeds, and advanced driver assistance sensors. Beam blade designs with integrated spoilers maintain consistent windshield contact and reduce wind lift at highway speeds, improving safety and visibility performance. Automakers adopt premium aerodynamic blades as standard equipment in mid-range and high-end vehicles, raising average system value per vehicle. Integration of rain sensors and automatic wiping control enhances driver convenience and safety, encouraging adoption of integrated wiper modules. Electric vehicles require optimized aerodynamic components to reduce drag and improve efficiency, further supporting advanced blade designs. Heated wiper systems for cold climates and coated rubber compounds for durability extend product life and premium pricing potential. OEMs increasingly outsource complete wiper modules including motors, linkages, and blades to specialized suppliers, increasing system complexity and revenue scope. Continuous innovation in materials and integration therefore elevates technological value across the USA wiper systems market.

Market Challenges

Price Competition and Margin Pressure in Aftermarket Blades

Price competition and margin pressure in aftermarket blades present a significant challenge in the USA wiper systems market because replacement wiper blades are widely commoditized products sold across retail chains, automotive stores, and online platforms with intense brand competition. Numerous manufacturers offer visually similar beam and frame blades, reducing differentiation and driving price-based purchasing behavior among consumers. Retailers often promote private-label or low-cost imported blades to increase margins, displacing premium brands. High promotional activity and discounting erode supplier profitability in the replacement segment. Consumers frequently prioritize price over durability or performance, limiting willingness to pay for advanced technologies. Distribution intermediaries capture significant margin share, further compressing manufacturer returns. Short product lifecycles and rapid model turnover require frequent tooling and packaging updates without proportional price increases. Smaller aftermarket brands struggle to maintain brand recognition and distribution presence against established global suppliers. Persistent commoditization therefore constrains profitability across the USA wiper systems aftermarket.

Durability Performance Constraints in Extreme Climatic Conditions

Durability performance constraints in extreme climatic conditions challenge the USA wiper systems market because rubber wiping elements degrade rapidly under ultraviolet exposure, ozone, freezing temperatures, and abrasive contaminants such as dust and road salt. Geographic climate diversity across the United States exposes wiper blades to severe heat in southern regions and ice accumulation in northern states, accelerating material fatigue and cracking. Ice adhesion and snow loading can damage blade frames and motors, increasing warranty claims for suppliers. Heavy rainfall regions require prolonged wiping operation that increases mechanical wear on blades and linkages. Frequent temperature cycling causes rubber hardening and loss of flexibility, reducing wiping efficiency and creating streaking. Manufacturers must balance cost with material performance when selecting rubber compounds and coatings. Advanced materials increase durability but raise production costs in price-sensitive markets. Ensuring consistent performance across all climatic conditions therefore remains a persistent engineering and cost challenge for wiper system manufacturers.

Opportunities

Integration of Advanced Driver Assistance Sensor Compatible Wiper Systems

Integration of advanced driver assistance sensor compatible wiper systems represents a major opportunity in the USA wiper systems market as vehicles increasingly incorporate cameras and sensors mounted near windshields requiring unobstructed visibility and coordinated cleaning functions. Autonomous driving and safety systems depend on clear sensor fields, creating demand for precision wiping zones and integrated washer delivery systems. Specialized blade geometries and motion control ensure complete clearing of camera and radar areas on windshields. OEMs seek integrated visibility modules combining sensors, heaters, and wiping mechanisms within single assemblies. This integration increases system complexity and supplier value contribution per vehicle. Electric and autonomous vehicles accelerate adoption of sensor-optimized wiper architectures. Suppliers capable of co-engineering wiping and sensing solutions can secure long-term OEM platform contracts. Growing regulatory emphasis on advanced safety features further expands sensor installation density in vehicles. Sensor-compatible wiping technology therefore creates high-value innovation opportunities across the USA wiper systems market.

Premiumization through Heated and Coated Wiper Blade Technologies

Premiumization through heated and coated wiper blade technologies offers significant growth potential in the USA wiper systems market because extreme weather conditions create demand for enhanced durability and performance beyond standard rubber blades. Heated blades prevent ice buildup and freezing adhesion in cold climates, improving winter driving safety and convenience. Hydrophobic and wear-resistant coatings extend blade lifespan and improve water clearing efficiency, supporting premium positioning. Consumers in northern regions and commercial fleets are willing to pay higher prices for long-life and all-weather performance blades. OEM adoption of heated windshield zones and advanced defrosting systems complements premium blade technologies. Replacement cycles for premium blades are longer but unit value is significantly higher, increasing revenue per installation. E-commerce channels enable targeted marketing of premium weather-specific blades to regional consumers. As climate resilience and durability expectations rise, premium wiper blade technologies represent a strong value expansion opportunity in the USA wiper systems market.

Future Outlook

The USA wiper systems market is expected to grow steadily over the next five years supported by sustained vehicle parc expansion, increasing electric vehicle production, and continued innovation in aerodynamic and sensor-integrated wiping technologies. Replacement demand will remain structurally strong due to consumable blade lifecycles. Regulatory emphasis on visibility safety and advanced driver assistance systems will further support technological upgrades. Premiumization and smart integration trends are anticipated to raise system value across both OEM and aftermarket segments.

Major Players

- Bosch

- Denso Corporation

- Valeo

- Trico Products

- Mitsuba Corporation

- Magneti Marelli

- Federal-Mogul Motorparts

- HELLA

- DOGA Group

- Nippon Wiper Blade

- Am Equipment

- PIAA Corporation

- ITW Automotive

- Johnson Electric

- WEXCO Industries

Key Target Audience

- Automotive OEM manufacturers

- Automotive component suppliers

- Automotive aftermarket distributors

- Fleet operators

- Commercial vehicle manufacturers

- Electric vehicle manufacturers

- Investments and venture capitalist firms

- Government and regulatory bodies

Research Methodology

Step 1: Identification of Key Variables

Key variables including vehicle parc size, annual automotive production, blade replacement intervals, climatic exposure patterns, and OEM installation rates were identified to define structural demand drivers and segmentation parameters within the USA wiper systems market.

Step 2: Market Analysis and Construction

Market sizing integrated automotive production data, vehicle fleet statistics, and blade consumption ratios across OEM and aftermarket channels to construct total demand estimates and segment distribution across vehicle and product categories.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with automotive engineers, aftermarket distributors, and fleet maintenance operators validated replacement cycles, durability expectations, pricing structures, and technology adoption trends influencing wiper system demand.

Step 4: Research Synthesis and Final Output

Quantitative modeling and qualitative insights were synthesized into a comprehensive market framework covering segmentation, competitive structure, technological evolution, and growth outlook across the USA wiper systems industry.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Increasing vehicle parc and replacement cycles

Advancements in aerodynamic and beam blade technologies

Expansion of electric and premium vehicle segments - Market Challenges

Price competition in low-margin aftermarket blades

Material durability issues in extreme climates

OEM cost reduction pressures on suppliers - Market Opportunities

Integration of smart rain-sensing and adaptive wiping systems

Growth in electric vehicle specific wiper designs

Premiumization through heated and coated blades - Trends

Shift toward frameless beam blade designs

Adoption of integrated washer and wiper modules

Use of advanced rubber and composite blade materials - Government regulations

- SWOT analysis

- Porters 5 forces

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Conventional Frame Wiper Systems

Beam Blade Wiper Systems

Hybrid Wiper Systems

Rear Window Wiper Systems

Headlamp Wiper Systems - By Platform Type (In Value%)

Passenger Cars

Light Commercial Vehicles

Heavy Commercial Vehicles

Electric Vehicles

Off-Highway Vehicles - By Fitment Type (In Value%)

OEM Installed Wiper Systems

Aftermarket Replacement Wiper Systems

Integrated Sensor Wiper Systems

Heated Wiper Systems

Aerodynamic Performance Wiper Systems - By EndUser Segment (In Value%)

Automotive OEM Manufacturers

Fleet Operators

Automotive Aftermarket Retailers

Commercial Vehicle Operators

Specialty Vehicle Manufacturers - By Procurement Channel (In Value%)

Direct OEM Supply Contracts

Automotive Component Distributors

Aftermarket Retail Chains

- Market Share Analysis

- Cross Comparison Parameters (Blade Technology, Vehicle Compatibility, Durability Rating, Distribution Channel, Price Tier, Aerodynamic Design, Sensor Integration, Climate Performance)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

Bosch

Denso Corporation

Valeo

Trico Products

Mitsuba Corporation

Federal-Mogul Motorparts

Magneti Marelli

ASMO Co.

HELLA

DOGA Group

PIAA Corporation

ITW Global Automotive

Mitsubishi Electric Automotive

OSRAM Automotive

AIDO Industry

- Automotive OEMs demand integrated aerodynamic wiping solutions

- Fleet operators prioritize durability and replacement cost efficiency

- Aftermarket retailers focus on high-turnover blade products

- Commercial vehicle operators require heavy-duty wiping performance

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now