Download PDF

Download PDF Download PDF

Download PDFMarket Overview

The USA Wireless EV Charging Systems Market is gaining traction as electric mobility infrastructure expands across passenger and commercial vehicle segments. Based on a recent historical assessment by the U.S. Department of Energy and industry-backed infrastructure disclosures, investments directed toward wireless charging pilots and deployments contribute to a market value exceeding USD ~ million, supported by federal funding allocations under clean transportation programs and private sector capital inflows. Growing EV adoption, urban fleet electrification, and smart city integration are primary demand catalysts.

Major urban centers such as California’s metropolitan regions, New York, and Texas lead deployment due to high EV registrations and proactive state-level clean energy incentives. California remains particularly dominant because of substantial zero-emission of vehicle mandates and infrastructure grants administered through state energy agencies. Strong collaboration between automotive OEMs, utilities, and municipal authorities further accelerates installations. Advanced research ecosystems and pilot roadway electrification initiatives reinforce technological leadership across these states.

By Product Type

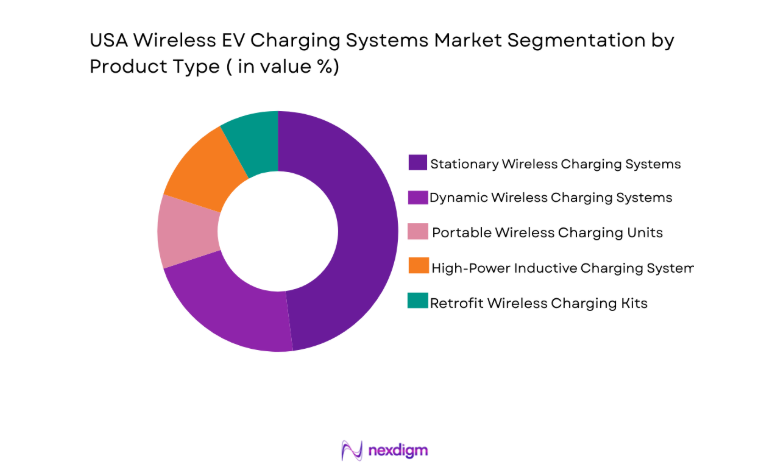

USA Wireless EV Charging Systems market is segmented by product type into Stationary Wireless Charging Systems, Dynamic Wireless Charging Systems, Portable Wireless Charging Units, High-Power Inductive Charging Systems, and Retrofit Wireless Charging Kits. Stationary Wireless Charging Systems currently hold the dominant share due to higher commercialization levels, established pilot deployments in residential and fleet environments, lower installation complexity compared to roadway systems, and strong OEM compatibility with passenger EV platforms. Their scalability in parking-based infrastructure and alignment with existing grid systems further reinforce market leadership.

By Platform Type

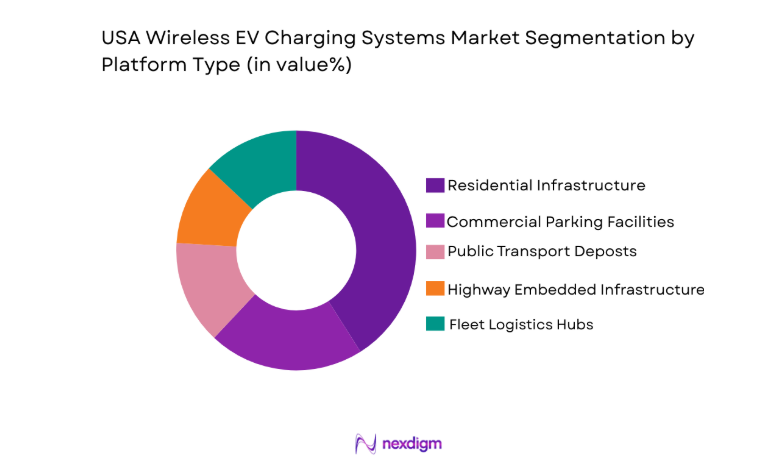

USA Wireless EV Charging Systems market is segmented by platform type into Residential Infrastructure, Commercial Parking Facilities, Public Transit Depots, Highway Embedded Infrastructure, and Fleet Logistics Hubs. Residential Infrastructure dominates due to increasing home EV installations, convenience-driven consumer behavior, integration with smart home energy systems, and supportive residential charging incentives. Higher adoption of premium EVs equipped with wireless compatibility further strengthens this segment’s position.

Competitive Landscape

The USA Wireless EV Charging Systems Market reflects moderate consolidation, with technology-driven firms collaborating closely with automotive OEMs and infrastructure providers. Strategic alliances, patent ownership, and grid integration expertise determine competitive positioning. Established players leverage pilot deployments and standards participation to expand market presence while emerging companies focus on efficiency optimization and dynamic charging innovation.

|

Company Name |

Establishment Year | Headquarters | Technology Focus | Market Reach | Key Products | Revenue | Wireless Efficiency Rate |

| WiTricity Corporation | 2007 | USA | ~ | ~ | ~ | ~ | ~ |

| Qualcomm Technologies | 1985 | USA | ~ | ~ | ~ | ~ | ~ |

| Plugless Power | 2009 | USA | ~ | ~ | ~ | ~ | ~ |

| HEVO Inc | 2011 | USA | ~ | ~ | ~ | ~ | ~ |

| Momentum Dynamics | 2009 | USA | ~ | ~ | ~ | ~ | ~ |

USA Wireless EV Charging Systems Market Analysis

Growth Drive rs

rs

Federal Infrastructure Funding for Electrification Projects

Federal programs supporting clean transportation allocate substantial capital toward advanced charging technologies, accelerating commercialization of wireless EV charging platforms across urban and highway environments. Legislative initiatives aimed at decarbonizing transport networks encourage utilities and municipalities to integrate innovative charging mechanisms within broader electrification roadmaps. Public funding reduces deployment risk for early-stage technologies by subsidizing pilot installations and demonstration corridors in high-traffic metropolitan areas. Coordinated investments between transportation departments and energy agencies create structured procurement pipelines that support domestic technology developers. The presence of national decarbonization targets drives alignment between automotive manufacturers and wireless charging innovators seeking scalable infrastructure compatibility. Incentive-backed deployments in transit fleets and government vehicles provide stable demand that strengthens supply chain confidence and component manufacturing expansion. Financial certainty from multi-year infrastructure commitments improves investor sentiment and accelerates venture capital participation in wireless power transfer ecosystems. Long-term policy clarity reduces uncertainty regarding interoperability standards and safety regulations, allowing companies to focus on performance optimization and system efficiency enhancements.

Rapid Growth of Electric Vehicle Adoption and Premium Feature Integration

Expanding electric vehicle ownership across passenger and commercial segments increases the addressable base for advanced charging solutions that enhance user convenience and reduce cable dependency. Premium EV manufacturers differentiate their models through seamless charging experiences, promoting factory-installed compatibility with inductive charging pads. Consumer preference for automated and contactless systems aligns with broader digitalization trends, reinforcing willingness to adopt wireless technologies. Fleet operators managing delivery vans and ride-hailing vehicles seek operational efficiency improvements that minimize manual handling and downtime. The integration of autonomous vehicle pilots further amplifies demand for cable-free charging infrastructure compatible with self-parking capabilities. Increased residential charging installations provide natural entry points for stationary wireless systems that complement existing electrical configurations. Technology standardization efforts within automotive consortia accelerate interoperability between vehicles and charging hardware suppliers. Growing environmental awareness and sustainability commitments among corporations encourage investment in next-generation charging technologies that align with carbon reduction strategies.

Market Challenges

High Infrastructure Deployment Costs and Grid Integration Complexity

Installing wireless charging infrastructure requires significant upfront capital investment in inductive pads, power electronics, and grid interconnection systems that exceed conventional plug-in charger costs. Roadway-embedded dynamic systems involve civil engineering modifications that increase construction expenditure and extend deployment timelines. Utilities must evaluate load management requirements to prevent localized grid congestion caused by high-power wireless charging clusters. Interoperability testing and compliance verification add further development expenses for both hardware providers and automotive manufacturers. Limited economies of scale during early commercialization phases constrain cost reductions and widen pricing gaps compared to wired alternatives. Municipal approval processes and permitting requirements introduce additional administrative complexity that slows project execution. Insurance and safety certification costs increase due to electromagnetic field assessments and public exposure considerations. Financing large-scale deployments remains challenging without guaranteed utilization rates that justify long-term return on investment projections.

Technological Standardization and Efficiency Optimization Barriers

Achieving consistent performance across varying vehicle models and charging environments requires harmonized technical standards that are still evolving within industry consortia. Differences in coil design, frequency selection, and alignment tolerances create interoperability risks that complicate widespread adoption. Energy transfer efficiency, while improving, must consistently match or exceed wired charging benchmarks to satisfy regulatory and consumer expectations. Thermal management considerations during high-power wireless charging demand advanced engineering solutions to maintain system reliability. Cybersecurity integration within wireless charging communication protocols introduces additional development layers to protect connected infrastructure. Limited field data from long-term deployments restricts comprehensive validation of durability and lifecycle performance. Automotive OEMs may hesitate to commit to specific technologies until standardization stabilizes, slowing ecosystem expansion. Public perception concerns regarding electromagnetic exposure require transparent communication and compliance with federal safety guidelines to build consumer confidence.

Opportunities

Integration with Autonomous Mobility and Smart City Infrastructure

Autonomous vehicle fleets require fully automated charging solutions that eliminate manual plug-in processes and enable continuous operational cycles within urban mobility networks. Wireless charging embedded in parking zones and transit hubs aligns with intelligent transportation systems designed to optimize traffic flow and energy usage. Smart city initiatives funded by municipal governments provide strategic platforms for integrating wireless charging into broader digital infrastructure upgrades. Data analytics capabilities associated with connected charging systems create opportunities for dynamic load management and predictive maintenance services. Collaboration with urban planners enables deployment models that minimize visual clutter and enhance public space design. Electric bus depots adopting inductive charging can streamline fleet operations and reduce maintenance complexity. Corporate campuses investing in sustainable mobility solutions represent high-value deployment environments for stationary wireless platforms. Integration with renewable energy microgrids offers additional potential for clean power utilization and decentralized energy resilience.

Expansion of Fleet Electrification and Commercial Logistics Applications

Commercial fleet operators prioritize uptime and operational efficiency, making automated wireless charging attractive for high-utilization vehicles such as delivery vans and municipal service fleets. Depot-based stationary charging systems reduce wear on connectors and simplify maintenance scheduling. Integration with fleet management software enables synchronized charging cycles aligned with route planning and battery health optimization. Public transit agencies exploring electrification strategies can leverage wireless charging at designated stops to extend vehicle range without prolonged downtime. Retail and logistics hubs seeking sustainability certification may adopt wireless charging to enhance environmental performance metrics. Government procurement programs supporting zero-emission fleets create structured demand channels for large-scale deployments. Industrial parks and distribution centers represent concentrated clusters where infrastructure investment yields predictable utilization patterns. Strategic partnerships between fleet operators and technology providers can accelerate cost reductions through volume-based procurement agreements.

Future Outlook

Over the next five years, the USA Wireless EV Charging Systems Market is expected to expand steadily as EV adoption accelerates and infrastructure modernization progresses. Technological refinements in inductive efficiency and alignment precision will enhance system reliability. Regulatory clarity and federal incentives will support pilot-to-commercial transition phases. Increasing collaboration between OEMs and infrastructure developers will strengthen interoperability. Demand from fleet electrification and autonomous mobility programs will further reinforce long-term growth potential.

Major Players

- WiTricity Corporation

- Qualcomm Technologies

- PluglessPower

- HEVO Inc

- Momentum Dynamics

- Toyota Motor Corporation

- BMW Group

- Hyundai Motor Company

- Siemens AG

- ABB Ltd

- InductEV

- Continental AG

- Tesla Inc

- ElectreonWireless

- Delta Electronics

Key Target Audience

- Investments and venture capitalist firms

- Government and regulatory bodies

- Electric vehicle manufacturers

- Automotivecomponentsuppliers

- Fleet operators

- Utility companies

- Smart city infrastructure developers

- Transportation authorities

Research Methodology

Step 1: Identification of Key Variables

Comprehensive identification of technological, regulatory, and demand-side variables influencing the USA Wireless EV Charging Systems Market was conducted. Primary data points included infrastructure investments, EV adoption volumes, and pilot deployment metrics. Secondary validation relied on government energy databases and corporate disclosures.

Step 2: Market Analysis and Construction

Quantitative modeling incorporated 2024 financial disclosures and federal infrastructure allocation records. Market share allocation was derived from deployment density and commercialization status of leading technologies. Segmentation structures were validated through cross-industry benchmarking.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts including charging infrastructure engineers and policy analysts reviewed preliminary findings. Technical feasibility assessments ensured alignment with current inductive efficiency benchmarks. Feedback loops refined competitive positioning and adoption trend assumptions.

Step 4: Research Synthesis and Final Output

Validated data was consolidated into structured analytical frameworks. Forecast modeling incorporated regulatory momentum and EV penetration trajectories. Final synthesis ensured coherence across segmentation, competitive mapping, and strategic insights.

- Executive Summary

- Research Methodology (Definitions, Scope, Industry Assumptions, Market Sizing Approach, Primary & Secondary Research Framework, Data Collection & Verification Protocol, Analytic Models & Forecast Methodology, Limitations & Research Validity Checks)

- Market Definition and Scope

- Value Chain & Stakeholder Ecosystem

- Regulatory / Certification Landscape

- Sector Dynamics Affecting Demand

- Strategic Initiatives & Infrastructure Growth

- Growth Drivers

Federal EV infrastructure funding allocations

Rising electric fleet electrification mandates

Advancements in inductive charging efficiency

Growth of smart city transportation projects

Increasing consumer preference for automated charging - Market Challenges

High initial infrastructure installation costs

Standardization and interoperability constraints

Grid load management complexities

Limited large scale commercial deployments

Regulatory approval and safety compliance delays - Market Opportunities

Expansion of dynamic in-road charging corridors

Integration with autonomous vehicle ecosystems

Utility managed wireless fleet depots - Trends

Increased pilot deployments across urban corridors

Strategic OEM technology partnerships

Development of high power wireless bus depots

Integration with vehicle to grid platforms

Miniaturization of onboard receiver modules - Government Regulations & Defense Policy

Federal infrastructure investment programs for EV charging

State level zero emission transportation mandates

Safety and electromagnetic compliance certification frameworks - SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Market Value, 2019-2025

- By Installed Units, 2019-2025

- By Average System Price, 2019-2025

- By System Complexity Tier, 2019-2025

- By System Type (In Value%)

Static Inductive Charging Systems

Dynamic In-Road Wireless Charging Systems

Resonant Inductive Charging Systems

Capacitive Wireless Charging Systems

High Power Depot-Based Wireless Chargers - By Platform Type (In Value%)

Passenger Electric Vehicles

Electric Buses

Light Commercial Electric Vehicles

Heavy Duty Electric Trucks

Autonomous Electric Vehicles - By Fitment Type (In Value%)

OEM Integrated Systems

Aftermarket Retrofit Kits

Fleet Depot Installations

Public Parking Infrastructure Integration

Residential Garage Installations - By End User Segment (In Value%)

Private EV Owners

Public Transit Authorities

Logistics and Fleet Operators

Corporate Mobility Service Providers

Municipal Government Agencies - By Procurement Channel (In Value%)

Direct OEM Partnerships

Government Infrastructure Contracts

Utility-Led Deployment Programs

Public Private Partnerships - By Material / Technology (in Value %)

Magnetic Resonance Coupling

Electromagnetic Induction Coils

Ferrite Core Materials

High Frequency Power Electronics

Smart Grid Integrated Control Systems

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (Technology Capability, Charging Efficiency, System Scalability, OEM Partnerships, Power Output)

- SWOT Analysis of Key Competitors

- Pricing & Procurement Analysis

- Key Players

WiTricity Corporation

Electreon Wireless

Plugless Power

HEVO Inc

Momentum Dynamics Corporation

InductEV Inc

Qualcomm Halo Technologies

Siemens AG

ABB Ltd

Toyota Motor Corporation

Hyundai Motor Company

Tesla Inc

Toshiba Corporation

ZF Friedrichshafen AG

Continental AG

- Fleet operators prioritize uptime optimization and automation

- Transit agencies adopt depot-based wireless charging for route efficiency

- Private EV owners demand seamless residential integration

- Municipalities leverage wireless charging for smart mobility pilots

- Forecast Market Value, 2026-2030

- Forecast Installed Units, 2026-2030

- Price Forecast by System Tier, 2026-2030

- Future Demand by Platform, 2026-2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now