Download PDF

Download PDFMarket Overview

The USA Wiring Harnesses market current size stands at around USD ~ million, reflecting broad deployment across automotive, industrial machinery, aerospace, defense platforms, and infrastructure equipment nationwide. Demand is shaped by increasing electrification, integration of electronic subsystems, and rising requirements for safety-critical connectivity. Production ecosystems combine domestic assembly with cross-border component flows, while tiered supplier structures support OEM platforms. High-voltage architectures, data-intensive systems, and reliability specifications continue to elevate technical complexity across applications.

Demand concentration is strongest in automotive manufacturing corridors across the Midwest and Southeast, with clusters near vehicle assembly plants, powertrain facilities, and logistics hubs. Aerospace and defense demand concentrates around established industrial regions with deep supplier ecosystems and certification capabilities. Industrial automation demand aligns with manufacturing-intensive states supported by reshoring incentives. Port access and cross-border trade corridors influence component inflows, while federal safety standards and state-level incentives shape adoption of advanced electrical architectures.

Market Segmentation

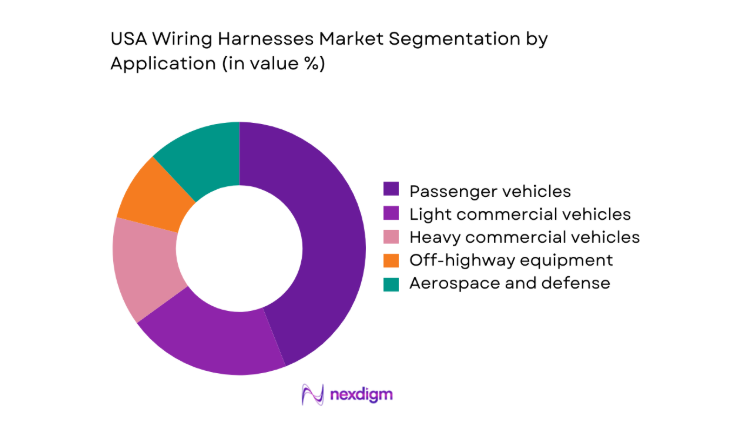

By Application

Automotive applications dominate due to continuous platform refresh cycles, expanding electronic content per vehicle, and growing integration of advanced driver assistance systems. Passenger and light commercial vehicles account for the largest deployment volumes, while heavy commercial vehicles and off-highway equipment drive demand for ruggedized harnesses with higher thermal and vibration tolerances. Aerospace and defense programs contribute steady demand through long lifecycle platforms and stringent certification requirements. Industrial machinery and automation add incremental demand as factories adopt connected equipment and safety interlocks. Replacement demand from the installed base sustains aftermarket volumes, supported by service networks and fleet maintenance practices across transportation and industrial sectors.

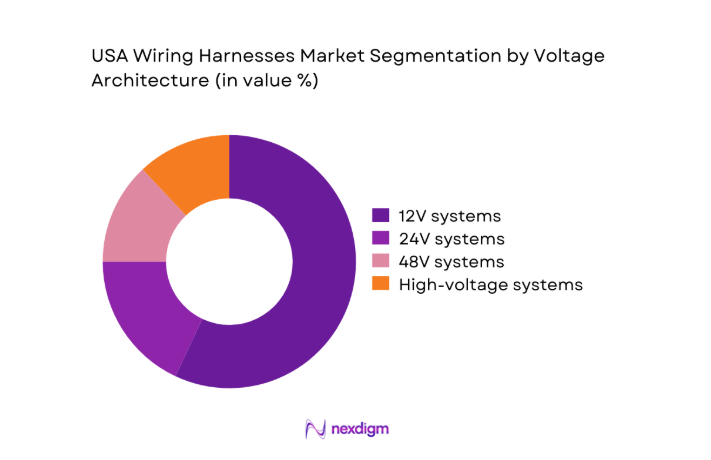

By Voltage Architecture

Low-voltage systems remain dominant due to legacy platforms and wide deployment across conventional vehicles and equipment. However, adoption of 48V architectures is expanding in mild-hybrid platforms to support auxiliary loads and efficiency features. High-voltage systems are gaining relevance with electrified powertrains and energy storage integration, requiring specialized insulation, shielding, and connectorization. Mixed-voltage architectures increase system complexity, driving demand for modular harness designs and zonal architectures. Safety standards and certification requirements elevate engineering content for high-voltage deployments, while serviceability considerations influence architecture choices across fleets and industrial equipment platforms.

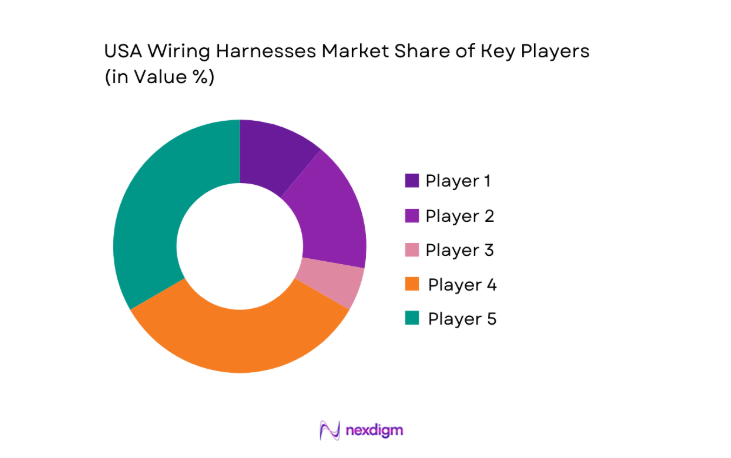

Competitive Landscape

The competitive environment features vertically integrated suppliers and specialized manufacturers supporting OEMs and Tier-1 integrators. Capabilities center on engineering depth, manufacturing scale, quality systems, and logistics execution aligned with platform launch schedules and lifecycle support.

| Company Name | Establishment Year | Headquarters | Formulation Depth | Distribution Reach | Regulatory Readiness | Service Capability | Channel Strength | Pricing Flexibility |

| Aptiv PLC | 1994 | Ireland | ~ | ~ | ~ | ~ | ~ | ~ |

| Lear Corporation | 1917 | United States | ~ | ~ | ~ | ~ | ~ | ~ |

| Yazaki Corporation | 1941 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Sumitomo Electric Industries | 1897 | Japan | ~ | ~ | ~ | ~ | ~ | ~ |

| Leoni AG | 1917 | Germany | ~ | ~ | ~ | ~ | ~ | ~ |

USA Wiring Harnesses Market Analysis

Growth Drivers

Rising electrification and EV adoption across US fleets

Electrification momentum across fleets accelerates wiring harness demand as vehicle production integrates higher voltage architectures and distributed electronic modules. In 2023, charging ports installed across public corridors exceeded 210000, expanding grid-connected vehicle interfaces and safety interlocks. Federal clean transportation programs allocated USD ~ million toward corridor readiness, enabling higher utilization of battery systems. By 2024, EV registrations reached 1400000 units nationwide, increasing demand for high-voltage connectors, shielding, and thermal management. Utility interconnection standards updated in 2022 expanded permissible onboard power flows to 19,200 watts for bidirectional charging pilots, increasing harness complexity across power electronics integration in fleet depots.

Increasing electronic content per vehicle and equipment

Electronic content growth raises harness density as advanced driver assistance systems, connectivity modules, and sensor arrays expand. In 2023, new light vehicle platforms integrated 120 sensors on average across safety, powertrain, and infotainment domains. Vehicle software modules exceeded 150 control units per platform in 2024, driving multi-domain signal routing and redundancy. Industrial equipment retrofits in 2022 added 24 safety interlocks per production cell, increasing cable routing points. Federal workplace safety updates required additional emergency circuits in automated cells across 2024. Telecommunications backhaul upgrades supported in 2023 expanded in-vehicle data rates to 10 gigabits, increasing shielding and connector performance requirements.

Challenges

Supply chain disruptions for copper and specialty connectors

Material availability volatility constrains harness production planning. In 2023, refined copper inventories across domestic warehouses fell below 18 days of forward coverage during port congestion events. Specialty connector lead times extended to 26 weeks in 2024 due to tooling bottlenecks and compliance testing queues. Rail freight dwell times increased by 6 days in 2022 across Midwest corridors, delaying inbound components to assembly plants. Federal transport safety audits in 2023 introduced additional documentation steps for hazardous material handling, extending customs clearance cycles. Industrial action disruptions across key ports in 2024 constrained inbound cable assemblies, affecting just-in-time schedules for vehicle launches.

Labor-intensive manufacturing and workforce shortages

Harness assembly remains labor intensive, and workforce availability constrains output. In 2023, vacancy rates across skilled assembly roles reached 9 across manufacturing counties with automotive concentration. Training throughput in certified electrical technician programs graduated 42,000 workers in 2024, insufficient for replacement needs driven by retirements. Overtime hours in harness assembly facilities rose to 11 hours weekly per worker in 2022, elevating fatigue risks. Workplace safety incident reports increased by 1,200 cases across manual crimping stations in 2023. Federal apprenticeship funding of USD ~ million supported automation training in 2024, but adoption lags due to retooling cycles.

Opportunities

Growth of EV and charging infrastructure wiring systems

Public and private charging deployments expand addressable demand for power cabling, connectors, and safety interlocks. In 2023, utility-approved interconnection permits exceeded 65,000 for depot charging installations supporting fleet electrification. Building codes updated in 2024 mandated conduit readiness for 2 parking bays per new commercial site, expanding embedded wiring demand. Federal infrastructure programs funded USD ~ million for corridor upgrades in 2022, accelerating site construction timelines. By 2025, grid operators reported 14 regional transmission upgrades supporting fast charging clusters. These indicators support sustained demand for high-voltage harnesses integrated with power electronics and thermal protection across depots and corridors.

Lightweighting through aluminum and hybrid harness designs

Weight reduction initiatives create opportunities for aluminum and hybrid conductors across vehicle platforms. In 2024, average mass reduction targets of 30 kilograms per light vehicle platform drove substitution trials in body and lighting circuits. Materials testing standards updated in 2023 validated aluminum conductor performance across 1,000 hour thermal cycling protocols. Fleet efficiency programs introduced in 2022 linked vehicle certification credits to mass reduction thresholds of 2 percent per model refresh. Domestic smelting capacity expansions in 2024 improved conductor availability. These indicators favor scalable adoption of hybrid harness architectures balancing conductivity, weight, and manufacturability across electrified and conventional platforms.

Future Outlook

The market outlook through 2030 reflects continued electrification, deeper electronic integration, and expanding charging infrastructure. Platform redesigns will favor zonal architectures and modular harnessing to manage complexity. Regulatory alignment on safety and interoperability will shape engineering requirements, while reshoring incentives influence manufacturing footprints. Automation in assembly and testing is expected to improve resilience and throughput across supply chains.

Major Players

- Aptiv PLC

- Lear Corporation

- Yazaki Corporation

- Sumitomo Electric Industries

- Leoni AG

- Furukawa Electric

- Motherson Group

- TE Connectivity

- Coroplast Fritz Müller

- PKC Group

- Kromberg & Schubert

- Nexans Autoelectric

- Amphenol

- Judd Wire

- Delphi Technologies

Key Target Audience

- Automotive OEM procurement teams

- Tier-1 system integrators and platform leads

- Fleet operators and mobility service providers

- Industrial automation equipment manufacturers

- Defense acquisition program offices

- State Departments of Transportation and the National Highway Traffic Safety Administration

- Utilities and charging infrastructure developers

- Investments and venture capital firms

Research Methodology

Step 1: Identification of Key Variables

Core variables included platform architecture shifts, electrification penetration, voltage migration, and regulatory compliance requirements across automotive, industrial, and defense applications. Demand drivers and constraints were mapped across OEM sourcing practices, supplier capacity, and logistics reliability.

Step 2: Market Analysis and Construction

Application-level demand pathways were constructed using production footprints, platform refresh cycles, and infrastructure deployment programs. Supply-side capabilities were mapped across domestic assembly, component sourcing, certification readiness, and logistics corridors.

Step 3: Hypothesis Validation and Expert Consultation

Operational assumptions were validated through structured consultations with manufacturing engineers, compliance specialists, and fleet maintenance leaders. Scenario testing assessed resilience under material volatility, workforce constraints, and regulatory updates.

Step 4: Research Synthesis and Final Output

Findings were synthesized into application, architecture, and channel perspectives to align strategic implications with procurement, engineering, and policy considerations. Cross-validation ensured internal consistency across drivers, challenges, and opportunities.

- Executive Summary

- Research Methodology (Market Definitions and application scope mapping, OEM and Tier-1 procurement interviews, Teardown-based BOM and cost modeling, Vehicle production and platform tracking, Import-export and domestic manufacturing analysis, Regulatory and safety compliance review, Dealer and aftermarket channel surveys)

- Definition and Scope

- Market evolution

- Usage pathways across vehicle and equipment platforms

- Ecosystem structure

- Supply chain and channel structure

- Regulatory environment

- Growth Drivers

Rising electrification and EV adoption across US fleets

Increasing electronic content per vehicle and equipment

ADAS and infotainment integration driving wiring complexity

Reshoring and nearshoring of automotive manufacturing

Infrastructure spending on commercial and off-highway equipment

Stricter safety and emissions regulations increasing sensorization - Challenges

Supply chain disruptions for copper and specialty connectors

Labor-intensive manufacturing and workforce shortages

Design complexity with mixed-voltage architectures

Cost pressure from OEMs and margin compression

Quality and reliability risks in high-voltage harnesses

Long qualification cycles with OEM platforms - Opportunities

Growth of EV and charging infrastructure wiring systems

Lightweighting through aluminum and hybrid harness designs

Modular and zonal electrical architectures

Aftermarket replacement demand from aging vehicle parc

Automation and digital manufacturing in harness assembly

Defense and aerospace electrification programs - Trends

Shift toward zonal architectures reducing wiring length

Integration of high-speed data and fiber optics

Increased use of aluminum to offset copper price volatility

Adoption of digital twins and virtual harness design

Standardization of connectors for EV platforms

Automation of crimping, routing, and testing processes - Government Regulations

- SWOT Analysis

- Stakeholder and Ecosystem Analysis

- Porter’s Five Forces Analysis

- Competition Intensity and Ecosystem Mapping

- By Value, 2019–2024

- By Volume, 2019–2024

- By Installed Base, 2019–2024

- By Average Selling Price, 2019–2024

- By Application (in Value %)

Passenger vehicles

Light commercial vehicles

Heavy commercial vehicles

Off-highway and agricultural equipment

Aerospace and defense platforms

Industrial machinery and automation - By Material Type (in Value %)

Copper wiring harnesses

Aluminum wiring harnesses

Hybrid copper-aluminum harnesses

Fiber optic integrated harnesses - By Component Type (in Value %)

Powertrain wiring harnesses

Chassis wiring harnesses

Body and lighting wiring harnesses

Dashboard and cockpit wiring harnesses

Battery and high-voltage wiring harnesses

Infotainment and connectivity harnesses - By Voltage Architecture (in Value %)

12V systems

24V systems

48V mild-hybrid systems

High-voltage EV systems - By Sales Channel (in Value %)

OEM direct supply

Tier-1 integrators

Aftermarket and replacement

Contract manufacturing and EMS partners

- Market structure and competitive positioning

Market share snapshot of major players - Cross Comparison Parameters (manufacturing footprint, OEM platform coverage, high-voltage harness capability, cost competitiveness, delivery reliability, quality certifications, design and engineering support, aftermarket reach)

- SWOT Analysis of Key Players

- Pricing and Commercial Model Benchmarking

- Detailed Profiles of Major Companies

Aptiv PLC

Lear Corporation

Yazaki Corporation

Sumitomo Electric Industries

Leoni AG

Furukawa Electric

Motherson Group

TE Connectivity

Delphi Technologies

Coroplast Fritz Müller

PKC Group

Kromberg & Schubert

Nexans Autoelectric

Amphenol

Judd Wire

- Demand and utilization drivers

- Procurement and tender dynamics

- Buying criteria and vendor selection

- Budget allocation and financing preferences

- Implementation barriers and risk factors

- Post-purchase service expectations

- By Value, 2025–2030

- By Volume, 2025–2030

- By Installed Base, 2025–2030

- By Average Selling Price, 2025–2030

Request a Sample

Request a Sample Ask for Customization

Ask for Customization Get a Quote

Get a Quote Enquire Now

Enquire Now